Petroleum Data Analytics Market Size, Share & Industry Analysis, By Component (Hardware, Services, and Software), By Deployment (Cloud and On-Premise), By Application (Downstream, Midstream, and Upstream), and Regional Forecast, 2026-2034

Petroleum Data Analytics Market Size and Future Outlook

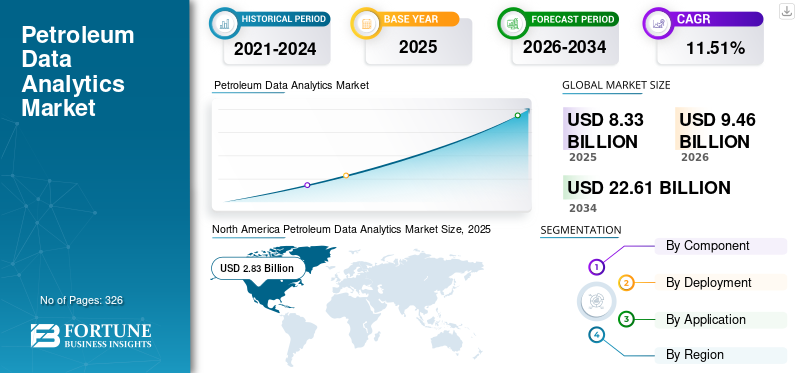

The global petroleum data analytics market size was valued at USD 8.33 billion in 2025. The market is projected to grow from USD 9.46 billion in 2026 to USD 22.61 billion by 2034, exhibiting a CAGR of 11.51% over the forecast period. North America dominated the petroleum data analytics market with a market share of 33.97% in 2025.

Petroleum data analytics refers to the use of advanced data processing, statistical models, and digital technologies to analyze large volumes of data generated across the oil and gas value chain. It involves applying tools such as artificial intelligence (AI), machine learning (ML), and predictive analytics to improve decision-making in exploration drilling and production, refining, and distribution. By leveraging real-time and historical data, companies can optimize asset performance, enhance operational efficiency, reduce costs, and improve safety. This approach also supports better reservoir management, predictive maintenance, and demand forecasting, making operations more data driven and efficient.

The growth of the market is primarily driven by the increasing need for operational efficiency and cost optimization across the oil and gas value chain. Rising data volumes from digital oilfields, IoT sensors, and seismic activities are pushing companies to adopt advanced analytics and AI-driven solutions. Additionally, the industry’s focus on predictive maintenance and asset performance management is accelerating adoption to reduce downtime and improve productivity. The growing investments in digital transformation and cloud technologies, especially by major oil companies, further support market expansion. Moreover, the need to enhance safety, regulatory compliance, and emissions monitoring is encouraging the wider deployment of data analytics solutions.

Leading companies such as SLB (Schlumberger Limited), Halliburton Company, Baker Hughes Company, IBM Corporation, and Microsoft Corporation are actively influencing the market landscape through continuous investments in digital technologies and advanced analytics platforms. These players are focusing on integrating AI, machine learning, and cloud services to enhance upstream and downstream operations. A common strategy that they are adopting is the development of digital oilfield solutions and real time data platforms to improve decision-making and operational efficiency. They are also forming strategic partnerships to expand their analytics capabilities and global reach. Additionally, these companies emphasize automation, predictive maintenance, and data-driven optimization to deliver cost savings and performance improvements for oil & gas operators.

Download Free sample to learn more about this report.

Petroleum Data Analytics Market KEY TAKEAWAYS

- 2025 Market Size: USD 8.33 billion

- 2026 Market Size: USD 9.46 billion

- 2034 Forecast Market Size: USD 22.61 billion

- CAGR: 11.51% from 2026–2034

- North America dominated the petroleum data analytics market with a 33.97% share in 2025.

- The software segment accounted for the largest market share of 47.42% in 2025.

- The on-premise segment accounted for the largest deployment share of 60.36% in 2025.

North America

North America USD 2.83 billion in 2025, driven by advanced digital infrastructure and extensive shale operations.

Asia Pacific

Asia Pacific USD 1.43 billion in 2025, supported by expanding refining capacity and increasing digital transformation.

Europe

Europe USD 1.46 billion in 2025, driven by refinery optimization, sustainability initiatives, and regulatory compliance.

U.S.

U.S. USD 2.34 billion in 2025, supported by large-scale shale operations and widespread AI-driven analytics adoption.

Japan

Japan USD 0.18 billion in 2025, driven by refinery optimization, industrial analytics, and IoT integration.

Read More

Petroleum Data Analytics Market Trends

Increasing Adoption of AI and Digital Twin Technologies to Amplify Market Growth

A key trend in the market is the rapid adoption of AI, machine learning, and digital twin technologies across oil and gas operations. According to insights from the International Energy Agency (IEA), digital technologies can improve upstream production efficiency by 10–20%, encouraging operators to deploy advanced analytics solutions. Digital twins are increasingly used to replicate complex assets such as offshore platforms, enabling real-time monitoring and simulation. For instance, companies such as Equinor and Shell have implemented digital twin models to optimize offshore operations and reduce downtime. Additionally, cloud-enabled AI platforms are helping process massive seismic datasets faster, reducing exploration timelines by up to 30% in some cases. This trend reflects a broader shift toward intelligent, data-driven operations aimed at improving performance, safety, and sustainability across the petroleum value chain.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Need for Operational Efficiency and Cost Optimization to Push the Market Growth

A primary driver of the petroleum data analytics market growth is the surging need for cost optimization and operational efficiency, especially amid crude oil price volatility. The U.S. Energy Information Administration (EIA) highlights that operational costs can account for 40–60% of the total upstream expenditure, pushing companies to adopt analytics for optimization. Predictive maintenance solutions, enabled by data analytics, can reduce equipment downtime by 30–50% and maintenance costs by 10–20%, as indicated in World Economic Forum (WEF) digital transformation studies. For example, BP and Chevron have implemented real-time analytics platforms to optimize drilling performance and reduce non-productive time. These measurable benefits make analytics a critical investment, enabling companies to enhance productivity, extend asset life, and maintain profitability even during market downturns.

Market Restraints

High Initial Investment and Integration Complexity to Limit the Market Growth

A major restraint for market expansion is the high upfront investment and complexity of integrating modern analytics systems with legacy infrastructure. According to the IEA, digital transformation in oil and gas can require investments of millions of dollars per asset, particularly for large-scale offshore operations. Many companies operate aging infrastructure where data is siloed across multiple systems, making integration difficult and time-intensive. Studies from OECD and industry bodies suggest that up to 60–70% of industrial data remains underutilized due to lack of standardization and interoperability. For smaller operators, these costs can be prohibitive, especially during periods of low oil prices. Additionally, the need for skilled data scientists and ongoing system upgrades further increases the financial burden, slowing adoption rates despite the long-term benefits of analytics.

Market Opportunities

Expansion of Cloud-Based and Real-Time Analytics Solutions to Create New Growth Avenues

A significant opportunity in the market lies in the expansion of cloud computing and real-time analytics capabilities. For example, Aramco Digital is preparing to launch Saudi Arabia’s national industrial communications network in the 450 MHz spectrum to support secure industrial IoT and edge AI applications across more than 50 industrial zones. The network will enable real-time asset monitoring, fleet tracking, smart surveillance, environmental sensing, and infrastructure control through AI-enabled smart radios, advanced sensing technologies, and reliable long-range connectivity. Real-time analytics enables operators to monitor production and equipment performance continuously, leading to faster decision-making and improved efficiency. For instance, Saudi Aramco has implemented real-time monitoring systems across its fields, enhancing production optimization and reducing operational risks. Additionally, cloud platforms allow companies to scale analytics capabilities without heavy capital investment, supporting collaboration across global operations. As more companies transition to hybrid and cloud based systems, this creates a strong opportunity for analytics vendors to deliver scalable, subscription-based solutions and drive widespread digital transformation.

Market Challenges

Data Security, Privacy, and Cybersecurity Risks to Limit Market Growth

A critical challenge in the market is the rising risk of cybersecurity threats and data breaches as operations become increasingly digitalized. According to the International Energy Agency, cyberattacks on energy infrastructure have increased significantly in recent years, with the energy sector being among the top targets globally. The World Economic Forum estimates that cyber incidents can cause operational disruptions costing millions of dollars per event. A notable example is the ransomware attack on Colonial Pipeline in the U.S. in May 2021, which disrupted fuel supply across several states and highlighted vulnerabilities in energy infrastructure. As companies adopt cloud platforms and interconnected systems, ensuring data security across multiple layers becomes complex. This requires substantial investment in cybersecurity measures, skilled personnel, and regulatory compliance, making it a persistent challenge for industry players.

Segmentation Analysis

By Component

Rising Adoption of Advanced Analytics Platforms to Impel the Software Segment Growth

Based on component, the market is segmented into hardware, services, and software.

The software segment accounted for approximately 47.42% of the market share in 2025. The software segment is the largest and fastest-growing component of the market, driven by the rising adoption of advanced analytics platforms, AI/ML tools, digital twins, and visualization solutions. Software enables the processing and interpretation of massive datasets generated across upstream, midstream, and downstream operations. Globally, oil & gas companies are increasingly investing in cloud-based and scalable analytics platforms to enhance decision-making, optimize production, and reduce operational costs. The shift toward subscription-based and SaaS models is further accelerating adoption, making advanced analytics more accessible. Additionally, software solutions are continuously evolving with the integration of real-time analytics, automation, and predictive capabilities. As the industry moves toward data-driven operations, the software segment is expected to remain the primary growth engine of the market.

The services segment is anticipated to grow at a CAGR of 11.48% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Full Control over Sensitive Operational Data Feature to Push On-Premise Segment Growth

Based on deployment, the market is segmented into cloud and on-premise.

The on-premise segment accounted for approximately 60.36% of the market share in 2025. On-premise deployment remains a dominant model in the market, particularly in regions with strict data security, regulatory requirements, and legacy infrastructure. Many oil & gas companies prefer on-premise systems to maintain full control over sensitive operational data, including reservoir information and production metrics. This model is especially prevalent among national oil companies (NOCs) and in regions such as the Middle East, where data sovereignty is a key concern. Additionally, existing investments in legacy IT infrastructure make a complete transition to cloud solutions complex and costly. On-premise systems also offer advantages in environments with limited connectivity, such as remote oilfields.

The cloud segment is expected to grow at a CAGR of 12.27% during the forecast period.

By Application

Midstream Segment Led the Market, Driven by Rising Data Analytics Adoption for Monitoring and Optimization

Based on application, the market is segmented into downstream, midstream, and upstream.

The midstream segment represented the largest petroleum data analytics market share of around 47.65% in 2025. The segment is experiencing the growing adoption of data analytics, particularly in pipeline monitoring, asset integrity management, and logistics optimization. This sector is undergoing transformation due to increasing regulatory pressure and the need for operational safety. Analytics solutions enable the real-time monitoring of pipelines, helping detect leaks and prevent failures, which can significantly reduce environmental and financial risks. For example, predictive maintenance applications can lower pipeline downtime by 20–30%, improving operational reliability. Additionally, analytics supports efficient storage and transportation planning, optimizing supply chain performance. As infrastructure expands and safety regulations tighten globally, the midstream segment is expected to witness accelerated growth, though it still represents a smaller share compared to upstream.

The downstream segment is the fastest growing segment anticipated to surge at a CAGR of 12.10% over the forecast period.

Petroleum Data Analytics Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Petroleum Data Analytics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is the dominant region in the market valued at USD 2.83 billion in 2025, accounting for approximately 33.92% of the global market. North America is a highly mature and technologically advanced market, driven primarily by extensive shale operations in the U.S. The region benefits from strong digital infrastructure and early adoption of advanced technologies such as artificial intelligence, machine learning, and cloud computing. According to the U.S. Energy Information Administration (EIA), the U.S. is one of the largest oil producers globally, contributing significantly to data generation across upstream activities. Operators in the region widely use predictive analytics to optimize drilling and reduce non-productive time, with studies indicating downtime reductions of up to 30–50%. Additionally, the presence of major technology providers and oilfield service companies accelerates innovation and deployment of advanced analytics solutions across the value chain.

U.S. Petroleum Data Analytics Market

The U.S. market reached a value of USD 2.34 billion in 2025 and is projected to touch USD 2.68 billion in 2026. The country leads due to its large-scale shale operations and advanced digital ecosystem. With oil production exceeding 12 million barrels per day (EIA), the country generates massive operational datasets. Companies extensively use AI-driven drilling optimization and predictive maintenance, improving efficiency and reducing downtime significantly. The strong cloud adoption further enhances real-time analytics capabilities.

Europe

The Europe market accounted for USD 1.46 billion in 2025, representing approximately 17.54% of global revenues. Europe represents a mature market characterized by a strong focus on efficiency, sustainability, and regulatory compliance. Oil and gas companies in the region are leveraging data analytics to optimize existing assets rather than expanding production. Major players such as BP, Shell, and TotalEnergies are actively investing in digital solutions for offshore operations and refining processes. The International Energy Agency (IEA) highlights that digital technologies can improve operational efficiency by 10–15%, which is critical for Europe’s cost-sensitive refining sector. Additionally, strict regulations such as GDPR influence how data is stored and processed, encouraging the use of secure and hybrid deployment models. The region’s emphasis on emissions reduction and energy transition further drives the adoption of analytics for monitoring and optimization.

Germany Petroleum Data Analytics Market

The Germany market touched a value of USD 0.14 billion in 2025 and is estimated to reach USD 0.15 billion in 2026. The market is driven by refining and industrial analytics, as upstream activity is limited. The country focuses on improving refinery efficiency and integrating analytics with Industry 4.0 systems. Advanced data analytics helps optimize energy usage and operational performance across facilities. Increasing emphasis on sustainability and emissions monitoring also supports adoption.

U.K. Petroleum Data Analytics Market

The U.K. market was valued at USD 0.27 billion in 2025 and is projected to reach USD 0.30 billion in 2026. The market is supported by North Sea offshore operations, which require advanced analytics for reservoir management and production optimization. Operators use digital tools to enhance recovery rates and manage aging assets. Analytics also plays a key role in decommissioning strategies. The presence of major players such as BP and Shell strengthens adoption.

Asia Pacific

The Asia Pacific market was valued at USD 1.43 billion in 2025, accounting for approximately 17.22% of global revenues. Asia Pacific is experiencing rapid growth in product adoption due to the increasing energy demand and expanding refining capacity. Countries such as China and India are heavily investing in digital transformation to improve operational efficiency and meet rising fuel consumption needs. China, for instance, is one of the largest refining hubs globally, generating vast volumes of operational data. National oil companies are implementing analytics for demand forecasting, supply chain optimization, and refinery performance improvement. Additionally, the expansion of LNG infrastructure and upstream activities in countries such as Australia and Southeast Asia is further driving the need for advanced analytics solutions.

China Petroleum Data Analytics Market

China remains the dominant contributor in the Asia Pacific region, valued at USD 0.47 billion in 2025. The China market is estimated to reach a value of USD 0.55 billion in 2026. China is a major market driven by its vast refining and petrochemical capacity. National oil companies such as CNPC and Sinopec are investing heavily in digital technologies to optimize operations. Analytics is widely used for demand forecasting and supply chain optimization. The country’s large-scale energy infrastructure generates significant data for advanced analytics applications.

India Petroleum Data Analytics Market

The India market was valued at USD 0.28 billion in 2025 and is projected to touch a value of USD 0.33 billion in 2026. The India market is expanding due to rapid refining capacity growth and rising energy demand. Companies such as Indian Oil Corporation are adopting analytics for demand forecasting and operational efficiency. Digital tools help optimize refinery performance and reduce costs. Government initiatives supporting digital transformation further accelerate adoption.

Japan Petroleum Data Analytics Market

The Japan market was valued at USD 0.18 billion in 2025 and USD 0.20 billion in 2026. The market is characterized by advanced industrial analytics and refinery optimization. Despite limited upstream activity, the country uses data analytics to improve efficiency and reduce energy consumption. Integration with IoT and automation systems enhances operational performance. Strong technological capabilities support steady adoption.

Latin America

The Latin America market accounted for USD 0.81 billion in 2025 or approximately 9.77% of global revenues. Latin America is an emerging market, driven by offshore developments and gradual digitalization of oil and gas operations. Brazil plays a central role due to its pre-salt offshore fields, which require advanced reservoir modeling and production analytics. According to global energy data, Brazil ranks among the top oil producers, generating strong demand for data-driven optimization. Mexico is also focusing on improving refining efficiency and upstream performance through analytics adoption. In addition, new oil discoveries in countries such as Guyana are creating opportunities for deploying modern analytics solutions from the outset. Predictive analytics and asset performance management tools are helping operators reduce inefficiencies and improve production outcomes, supporting the region’s digital transformation.

Middle East & Africa

The Middle East & Africa market was valued at USD 1.79 billion in 2025, driven by large-scale oil production and increasing investments in digital oilfield technologies. Countries in the Gulf Cooperation Council (GCC), particularly Saudi Arabia and the UAE, are leading the adoption of advanced analytics solutions. According to OPEC, the Middle East is one of the largest oil-producing regions globally, generating significant volumes of operational data. National oil companies such as Saudi Aramco and ADNOC are implementing AI-driven analytics to optimize production and enhance asset performance. In Africa, countries such as Nigeria and Angola are gradually adopting analytics for offshore operations and infrastructure management. Digital technologies can improve production efficiency by 10–20%, making analytics a critical tool for maximizing output and ensuring operational reliability across the region.

GCC Petroleum Data Analytics Market

The GCC market was valued at USD 1.34 billion in 2025 and is projected to touch USD 1.54 billion in 2026. The GCC region is driven by large-scale oil production and investments in digital oilfield technologies. Countries such as Saudi Arabia and the UAE are deploying AI-driven analytics to optimize production and asset performance. National oil companies such as Saudi Aramco and ADNOC lead digital transformation initiatives. Analytics helps improve efficiency and maximize output across vast oilfields.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Strong Investment in AI and Machine Learning by Key Players to Enhance their Market Share

Leading companies such as SLB (Schlumberger Limited), Halliburton Company, Baker Hughes Company, IBM Corporation, and Microsoft Corporation play a critical role in advancing the market by driving digital transformation across the oil and gas value chain. These companies are heavily investing in AI, machine learning, and cloud-based analytics platforms to enable real-time data processing and decision-making. A common focus among them is the development of integrated digital oilfield solutions that enhance drilling efficiency, reservoir management, and production optimization. They are also actively forming strategic partnerships with oil & gas operators and technology providers to expand their capabilities and global presence. Additionally, these players emphasize predictive maintenance, automation, and scalable analytics platforms to help companies reduce costs, improve asset performance, and achieve operational excellence.

List of Top Petroleum Data Analytics Companies Profiled

- SLB (U.S.)

- Halliburton Company (U.S.)

- Baker Hughes Company (U.S.)

- Weatherford International plc (U.S.)

- Siemens Energy AG (Germany)

- ABB Ltd. (Switzerland)

- Emerson Electric Co. (U.S.)

- Honeywell International Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Amazon Web Services (AWS) (U.S.)

- Google LLC (U.S.)

- IBM Corporation (U.S.)

- Palantir Technologies Inc. (U.S.)

- SAS Institute Inc. (U.S.)

- AVEVA Group plc (U.K.)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Baker Hughes expanded its Cordant™ digital solutions suite, incorporating predictive analytics for asset performance management. The company emphasized AI-enabled monitoring to reduce downtime and improve equipment reliability. This initiative aligns with the growing demand for data-driven maintenance and optimization.

- June 2024: Microsoft advanced its Azure Energy Data Services by integrating enhanced analytics and AI tools tailored for oil & gas operators. The platform enables seamless data ingestion, storage, and real-time analytics across upstream and downstream operations. This development strengthens Microsoft’s role in cloud-based petroleum analytics.

- March 2024: SLB expanded its Delfi digital platform capabilities by integrating advanced AI-driven reservoir modeling and real-time data analytics tools. The company also strengthened partnerships with cloud providers to enhance scalability and remote operations. This development supports improved decision-making and operational efficiency across upstream assets.

- October 2023: Halliburton enhanced its DecisionSpace® 365 platform with new cloud-based analytics and machine learning features. The upgrade focuses on improving drilling performance and reservoir evaluation through real-time data insights. This move reflects the company’s push toward fully digital and automated oilfield solutions.

- September 2023: AWS expanded its energy data solutions portfolio, supporting the Open Subsurface Data Universe (OSDU) framework for better data standardization. The update allows oil & gas companies to accelerate analytics workflows and improve interoperability across platforms. This initiative enhances cloud adoption in petroleum data analytics.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.51% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Component

|

|

By Deployment

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 8.33 billion in 2025 and is projected to reach USD 22.61 billion by 2034.

In 2025, the North America market value stood at USD 2.83 billion.

The market is expected to exhibit a CAGR of 11.51% during the forecast period of 2026-2034.

By component, the software segment led the market in 2025.

The rising need for operational efficiency and cost optimization is a key factor driving market expansion.

SLB, Halliburton Company, Baker Hughes Company, IBM Corporation, and Microsoft Corporation are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 326

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us