AI in Radiology Market Size, Share & Industry Analysis, By Component (Software and Services), By Deployment (Cloud-based, On-Premise, and Hybrid), By Technology (Computer Vision/Deep Learning, Natural Language Processing, and Others), By Modality (CT Scan, MRI, X-ray, Ultrasound, Mammography, and Others), By Application (Screening & Early Detection, Diagnosis & Characterization, Quantification, Monitoring & Follow-up, and Others), By End User (Hospitals & ASCs, Diagnostic Imaging Centers, Academic & Research Institutes, and Others), and Regional Forecast, 2026-2034

AI in Radiology Market Size and Future Outlook

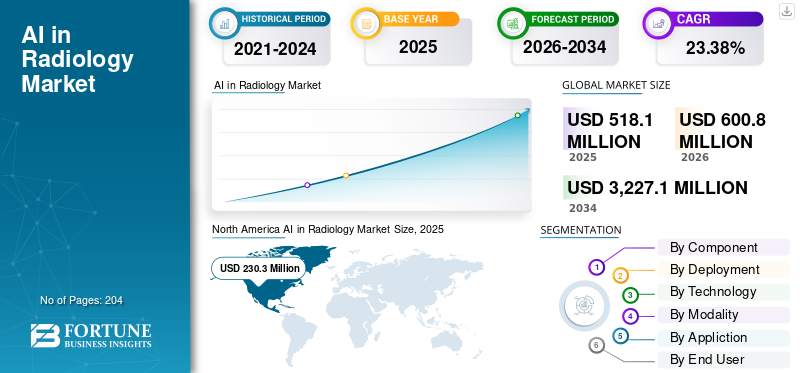

The global AI in radiology market size was valued at USD 518.1 million in 2025. The market is projected to grow from USD 600.8 million in 2026 to USD 3,227.1 million by 2034, exhibiting a CAGR of 23.38% during the forecast period. North America dominated the AI in radiology market with a market share of 44.45% in 2025.

AI in radiology involves employing artificial intelligence, mainly through computer vision/deep learning and more recently, natural language processing, to analyze medical images and radiology information in standard clinical practices. It aids radiologists by enhancing the detection and prioritization of critical findings, facilitating consistent lesion segmentation and measurement, and expediting reporting via structured documentation and follow-up suggestions. Factors shaping this market encompass increasing imaging volumes in CT, X-ray, MRI, ultrasound, and mammography, ongoing shortages of radiologists leading to higher turnaround-time demands, and an escalating need for consistent measurements in oncology, cardiology, and neurology disciplines.

Major companies such as Siemens Healthineers, Koninklijke Philips N.V., Canon Medical, and Fujifilm are enhancing AI-driven imaging processes via cohesive software frameworks.

Download Free sample to learn more about this report.

AI in Radiology Market Key Takeaways

- 2025 Market Size: USD 518.1 million

- 2026 Market Size: USD 600.8 million

- 2034 Forecast Market Size: USD 3,227.1 million

- CAGR: 23.38% from 2026–2034

- North America dominated the AI in radiology market with a 44.45% share in 2025.

- The services segment is anticipated to grow at a CAGR of 20.04% during the forecast period.

- The cloud-based segment is anticipated to grow at a CAGR of 28.97% during the forecast period.

North America

North America remained the leading regional market, reaching USD 230.3 million in 2025.

Europe

Europe is projected to grow at a CAGR of 22.40% and reach USD 143.0 million by 2026.

Asia Pacific

Asia Pacific is expected to reach USD 132.8 million by 2026, strengthening its position as the third-largest regional market.

U.S.

The market is estimated to reach USD 238.6 million in 2026, accounting for approximately 39.7% of global revenue.

Japan

The market is estimated to reach USD 28.1 million in 2026, representing roughly 4.7% of global revenues.

Read More

AI in Radiology Market Trends

Integration of AI with PACS/RIS and Cloud Platforms Enabling Scalable Deployments is a Significant Trend

The merging of AI with PACS/RIS and cloud platforms is establishing a distinct market trend, as providers prefer AI to function within current radiology workflows rather than as an independent tool. Integrating AI into PACS/RIS and providing it through the cloud allows hospitals to implement it once and expand its use across various locations, modalities, and applications without needing repeated local setups. Moreover, cloud-native integration facilitates centralized updates to models, monitoring, and governance, thereby decreasing the burden on IT and enhancing result consistency. This is particularly crucial as imaging volumes increase and systems require quicker deployment of new algorithms for triage, quantification, and reporting assistance. These factors are supporting the global AI in radiology market growth.

- For instance, in January 2026, Konica Minolta Healthcare and deepc announced a partnership to bring AI to the Exa Platform, enabling connectivity between deepc’s radiology AI operating system and Konica Minolta’s platform.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rapid Growth in Imaging Volumes and Shortage of Radiologists to Propel Market Growth

The swift increase in imaging volumes is compelling radiology departments to interpret more studies daily, all while preserving quality and turnaround times. Simultaneously, a shortage of radiologists is leading to an expanding gap between supply and demand, resulting in higher backlogs and an increased risk of burnout. This synergy makes the economic appeal of AI adoption significant as it can prioritize critical cases, automate assessments, and standardize documentation, enabling teams to manage increased workloads without a corresponding rise in personnel. With the growing demand for imaging in both acute and chronic settings, health systems are placing greater emphasis on AI that seamlessly fits into standard workflows and minimizes manual processes. Organizations focused on the workforce have emphasized that shortages and increasing imaging demand are leading threats to radiology, underscoring the need for efficiency tools. All these factors cumulatively drive the global market growth.

- For instance, in December 2025, Aidoc announced that WellSpan Health would expand Aidoc aiOS across its enterprise after proven clinical and financial gains, explicitly noting the importance of augmenting radiologists amid today’s physician shortage and citing high-volume usage to reduce bottlenecks and improve turnaround time.

MARKET RESTRAINT

Data Privacy and Interoperability Concerns to Hamper Market Growth

Data privacy and interoperability issues may restrain the market as most solutions must move sensitive DICOM images and results across PACS/RIS/EHR and cloud stacks, where any weak link increases breach risk and compliance exposure. When data governance is unclear or security controls are inconsistent across sites, providers slow or limit AI rollouts to avoid regulatory and reputational risk. Interoperability is an equally practical blocker. If AI outputs cannot be reliably written back into PACS viewers and structured reports, radiologists end up with extra clicks and manual transcription, reducing ROI and adoption. These gaps increase integration cost, extend validation timelines, and make multi-site scaling harder, especially for hybrid environments. As a result, buyers often prioritize vendors with strong security posture and standards-based integration, while delaying broader deployment where systems are fragmented. This results in limiting the market growth to certain extent.

- For instance, The European Health Data Space (EHDS) Regulation was officially published on March 5, 2025 and entered into force on March 26, 2025, marking the start of a transition phase with stricter expectations around secure exchange and interoperable handling of electronic health data.

MARKET OPPORTUNITIES

Rising Investments by Major Cloud and Healthcare Companies and Partnerships to Offer Market Growth Opportunities

Increased funding from hyperscale cloud companies and leading healthcare IT vendors is generating a significant market potential for AI in radiology, as they reduce the obstacles such as data migration, extensive imaging storage, security/compliance issues, and workflow integration with PACS/RIS that usually hinder adoption. With cloud platforms incorporating healthcare-quality imaging services and reference architectures, AI vendors can implement algorithms more swiftly across multi-site networks without the need for extensive on-premises infrastructure. Collaborations also facilitate the integration of AI with enterprise imaging platforms, reducing procurement timelines and enhancing scalability for healthcare systems. This trend favors broader algorithm reach, ongoing model enhancements, and centralized oversight/governance, essential conditions for enterprise deployment. Consequently, the ecosystem is transitioning to cloud-native enterprise imaging with integrated AI, enabling bigger contract values and quicker geographic growth. All these factors would drive the market growth in the coming years.

- For instance, in November 2024, Intelerad and Amazon Web Services (AWS) announced an expanded strategic alliance to deliver a unified, cloud-native medical imaging infrastructure using AWS HealthImaging.

MARKET CHALLENGES

Significant Implementation Expenses and Necessity for IT Infrastructure in Smaller Hospitals to Present Major Obstacles

Significant implementation expenses and IT infrastructure demands pose a genuine obstacle for smaller hospitals, as radiology AI typically necessitates PACS/RIS integration, secure storage, dependable network bandwidth, and computing power to execute algorithms swiftly in clinical settings. Numerous rural and community locations also do not have specialized imaging IT teams, making the deployment a complex process (interfaces, validation, cybersecurity assessments, clinician training) instead of just a straightforward software installation. These initial expenses can postpone buying choices, particularly when funds are already allocated for scanner enhancements and fundamental IT updates. Inadequate infrastructure further complicates maintaining AI performance over time (updates, oversight, and data management), raising perceived risks and overall ownership costs. Consequently, smaller hospitals frequently limit AI implementation to one or two high-return use cases rather than expanding it throughout the organization. All the factors cumulatively affect the market growth.

- For instance, according to an article published in June 2025, rural medical centers are often left behind in advanced AI adoption due to high computational costs and resource requirements.

AI in Radiology Market Segmentation Analysis

By Component

Increasing Demand from Hospitals to Propel Software Segment Growth

Based on component, the market is divided into software and services.

The software segment captured the largest global AI in radiology market share in 2025. This has been observed as hospitals and imaging networks prefer software subscriptions since they can scale across modalities and sites without adding proportional headcount, while vendors can deliver frequent model updates, new modules, and performance monitoring through the same platform. Additionally, increasing number of collaborations between operating players also supported the segment growth.

- For instance, in March 2025, RamSoft and CARPL.ai announced the integration of CARPL’s 150+ AI applications into RamSoft’s PowerServer and OmegaAI RIS/PACS platforms, enabling radiologists to access and deploy AI tools directly inside the PACS environment.

The services segment is anticipated to rise with a CAGR of 20.04% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

High Number of Installations in Smaller Hospitals Supported the On-premise Segmental Dominance

Based on deployment, the market is divided into on-premise, cloud-based, and hybrid.

The on-premise segment captured the largest global AI in radiology market share in 2025. This is due to hospitals favoring on-premises systems to maintain radiology data within their network for data management, cybersecurity assessment, and clinical risk mitigation, instead of sending feeds outside. Additionally, the integration is easier and numerous solutions are tailored to work seamlessly with current infrastructure, resulting in minimal IT alterations and more manageable uptime. Furthermore, the segment is set to hold 39.4% share in 2026.

- For instance, in November 2025, RapidAI announced the U.S. FDA clearance for Rapid Aortic, noting its integration into Rapid Edge Cloud, described as a cloud platform with on-premise capabilities to ensure continuous service during disruptions.

The cloud-based segment is anticipated to rise with a CAGR of 28.97% over the forecast period.

By Technology

Advantages of Computer Vision Technology to Boost Computer Vision/Deep Learning Segmental Growth

In terms of technology, the market is divided into natural language processing, computer vision/deep learning, and others.

The computer vision/deep learning segment dominated the global market in 2025. These models deliver immediate operational ROI by enabling triage, prioritization, and standardized interpretation, which are used at scale in daily reading workflows. Deep learning also performs best for complex visual patterns (subtle bleeds, emboli, nodules, fractures). Hence, hospitals typically start their AI journey with CV-based algorithms before expanding into text-centric use cases. Furthermore, the segment is set to hold 77.7% share in 2026.

- For instance, in January 2026, Aidoc announced the U.S. FDA clearance for a comprehensive AI triage solution powered by its CARE foundation model, combining multiple acute CT indications into a single workflow.

The natural language processing segment is anticipated to rise with a CAGR of 31.42% over the forecast period.

By Modality

Generation of Large Study Volumes to Boost CT Scan Segmental Growth

In terms of modality, the market is divided into CT Scan, MRI, X-ray, ultrasound, mammography, and others.

The CT scan segment captured the highest share of the global market in 2025. CT scan is the workhorse modality for acute, high-stakes conditions such as stroke, head trauma, pulmonary embolism, aortic disease, and emergency oncology, where minutes matter and AI-driven triage/measurement delivers immediate clinical and operational ROI. CT also generates large study volumes in ED and inpatient settings for the translation of even small efficiency gains into reasonable throughput improvements. Additionally, new product launches by operating players also supported the segment growth. Furthermore, the segment is set to hold 32.0% share in 2026.

- For instance, in November 2025, RapidAI announced that it secured five new U.S. FDA clearances, expanding its Rapid Enterprise Platform, including modules supporting head CT comparisons and CT-based stroke/aortic workflows.

The mammography segment is anticipated to rise with a CAGR of 27.41% over the forecast period.

By Application

High Usage in Diagnosis & Characterization to Boost Segmental Growth

On the basis of application, the market is divided into screening & early detection, diagnosis & characterization, quantification, monitoring & follow-up, and others.

The diagnosis & characterization segment captured the highest share of the global market in 2025. The application maps to the largest day-to-day clinical workload as radiologists spend most of their time identifying findings, characterizing lesions, and deciding next steps across CT/X-ray/MRI. In addition, diagnosis AI is used continuously across inpatient and outpatient imaging, making it easier to justify enterprise subscriptions. Characterization tools also reduce downstream costs by supporting risk stratification and follow-up recommendations, which improves care pathway standardization. Furthermore, the segment is set to hold 33.9% share in 2026.

- For instance, in February 2026, RevealDx announced the U.S. FDA clearance for RevealAI-Lung, an AI tool designed specifically for lung nodule characterization to help radiologists make more informed follow-up recommendations.

The quantification segment is anticipated to rise with a CAGR of 24.63% over the forecast period.

By End User

High Utilization by Hospitals & ASCs to Support Segment’s Leading Position

Based on end user, the market is segmented into hospitals & ASCs, diagnostic imaging centers, academic & research institutes, and others.

In 2025, the hospitals & ASCs segment held the leading position in the global market. They control the largest share of high-acuity imaging volumes (ED, stroke, trauma, PE) where AI triage and decision support deliver immediate clinical value and measurable operational ROI. In addition, hospitals often buy AI as part of multi-year enterprise imaging contracts, increasing deal sizes and recurring revenue. ASCs benefit as they expand outpatient imaging throughput and want faster turnaround times with standardized quality. Furthermore, the segment is set to hold 61.9% share in 2026.

- For instance, in October 2025, Philips announced that Philips AI Manager became available nationwide across all four regional health authorities in Norway, enabling hospitals across the country to integrate scalable AI solutions into clinical practice.

In addition, the diagnostic imaging centers segment is projected to witness a growth rate of 27.18% during the forecast period.

AI in Radiology Market Regional Outlook

By geography, the market is divided into Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

North America

North America AI in Radiology Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America emerged as the market leader, commanding a valuation of USD 200.5 million in 2024 and dominated in 2025, accounting for USD 230.3 million. This sustained dominance is driven by the high imaging volumes in ED and chronic care, strong reimbursement/quality-focus pathways, and mature cloud and cybersecurity infrastructure across the region.

U.S. AI in Radiology Market

The U.S. dominated the North American market and can be analytically approximated at around USD 238.6 million in 2026, accounting for roughly 39.7% of the global market.

Europe

Europe is expected to follow a steady growth trajectory, registering a CAGR of 22.40% during the forecast period, and reaching a market size of USD 143.0 million by 2026. Increasing population screening programs, focus on reducing backlogs and improving efficiency, and an emphasis on standards-based interoperability are key factors accelerating market expansion in the region.

U.K. AI in Radiology Market

The U.K. market is estimated to reach around USD 32.1 million in 2026, representing roughly 5.3% of global revenues.

Germany AI in Radiology Market

The Germany market size is projected to reach approximately USD 40.0 million in 2026, equivalent to around 6.7% of global sales.

Asia Pacific

Asia Pacific is projected to touch USD 132.8 million by 2026, strengthening its position as the third-largest regional market. The rapid expansion of imaging capacity coupled with growing private hospital and imaging chain networks are expected to act as key growth catalysts across the region.

Japan AI in Radiology Market

The Japan market is estimated at around USD 28.1 million in 2026, accounting for roughly 4.7% of global revenues.

China AI in Radiology Market

The China market is projected to reach revenues of around USD 32.9 million in 2026, representing roughly 5.5% of global sales.

India AI in Radiology Market

The India market is estimated at around USD 21.6 million in 2026, accounting for roughly 3.6% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa markets are anticipated to depict moderate growth rates during the forecast period. The Latin American market is expected to reach USD 35.8 million by 2026. The GCC market in the Middle East & Africa is expected to achieve a valuation of USD 10.4 million by 2026.

South Africa AI in Radiology Market

The South Africa market is projected to reach around USD 6.6 billion in 2026, representing roughly 1.1% of global market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Emphasize Platform-led Strategies and AI Incorporation to Strengthen their Market Share

The global AI in radiology market shows a semi-consolidated structure, led by large imaging and informatics companies such as GE Healthcare, Siemens Healthineers, Koninklijke Philips N.V., Canon Medical, FUJIFILM, and others. Major players are strengthening their positions through platform-led strategies, embedding AI directly into PACS/RIS and enterprise imaging stacks to enable multi-site deployments and recurring subscriptions.

Other significant players include Aidoc, Viz.ai, RapidAI, Lunit, Qure.ai, Annalise.ai, and Rad AI, and others. These players are increasingly focusing on new product launches and partnerships to widen their market presence.

- For instance, in October 2025, RSNA Ventures announced a strategic partnership with Rad AI to deliver RSNA’s peer-reviewed knowledge directly into radiologists’ workflows via Rad AI’s platform.

LIST OF KEY AI in RADIOLOGY COMPANIES PROFILED

- Siemens Healthineers AG (Germany)

- General Electric Company (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Aidoc (Israel)

- Rad AI (U.S.)

- ai, Inc. (U.S.)

- ai. (U.S.)

- iSchemaView, Inc. (RapidAI) (U.S.)

- ai Technologies Private Limited (India)

- deepc GmbH (Germany)

- Lunit Inc. (South Korea)

KEY INDUSTRY DEVELOPMENTS

- February 2026: GE HealthCare announced a USD 35 million expansion with BARDA to advance AI-powered ultrasound for trauma care and emergency preparedness.

- January 2026: Bristol Myers Squibb partnered with Microsoft to advance AI-driven early detection of lung cancer, deploying FDA-cleared radiology AI algorithms via Microsoft’s Precision Imaging Network.

- November 2025: GE HealthCare announced an agreement to acquire Intelerad for USD 2.3 billion, aimed at building a cloud-first, AI-enabled enterprise imaging ecosystem with AI/workflow orchestration and SaaS imaging software.

- November 2025: Siemens Healthineers presented new AI-enabled radiology services (AI-enablement services and related offerings) to support imaging operations and help address workflow and staffing pressures.

- November 2025: a2z Radiology AI received FDA clearance for a2z-Unified-Triage, a multi-condition triage tool for abdomen–pelvis CT to flag and prioritize urgent findings.

REPORT COVERAGE

The global AI in radiology market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, and the introduction of new products. Furthermore, it outlines collaborations, mergers, and acquisitions, along with significant advancements in the industry within the market. The global market forecast report additionally offers a comprehensive competitive landscape with details on market share and the profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 23.38% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Component, Deployment, Technology, Modality, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Modality |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 518.1 million in 2025 and is projected to reach USD 3,227.1 million by 2034.

In 2025, the market value stood at USD 230.3 million.

The market is expected to exhibit a CAGR of 23.38% during the forecast period of 2026-2034.

By component, the software segment led the market in 2025.

Rapid growth in imaging volumes, shortage of radiologists, and increasing demand for AI triage and efficiency tools are key factors primarily driving market expansion.

Siemens Healthineers AG, Koninklijke Philips N.V., Aidoc, and Rad AI are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 204

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us