Airborne ISR Market Size, Share, and Industry Analysis, By End User (Defense, and Homeland Security), By Platform (Manned Special-mission Aircraft, UAS, Maritime ISR Aircraft, and Others), By Solution (Systems, Services, and Software), By Application (Maritime Patrol, Airborne Ground Surveillance (AGS), Airborne Early Warnings (AEW), and Signals Intelligence (SIGINT)), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

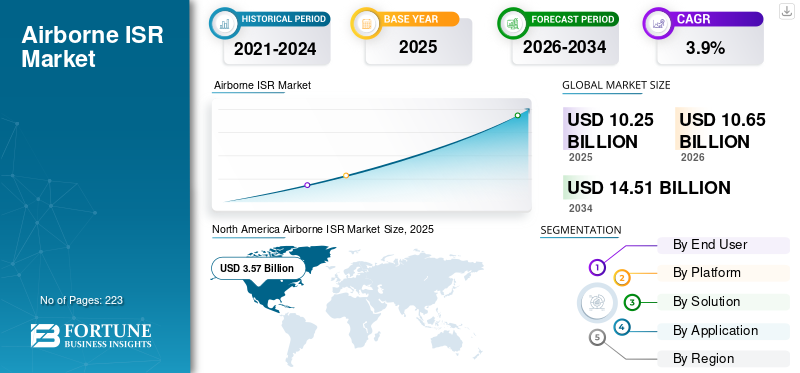

The global airborne ISR market size was valued at USD 10.25 billion in 2025. The market is projected to grow from USD 10.65 billion in 2026 to USD 14.51 billion by 2034, exhibiting a CAGR of 3.9% during the forecast period. North America dominated the global airborne ISR market with a share of 34.82% in 2025.

The growth of the airborne ISR market in aerospace and defense covers manned special-mission aircraft, unmanned systems, and maritime patrol platforms equipped to collect and deliver intelligence through EO/IR, radar (SAR/GMTI), and signals intelligence payloads. Market expansion is driven by the rising need for persistent surveillance, faster target detection and tracking, and stronger situational awareness across air, land, and maritime domains. Modern ISR programs increasingly focus on mission-system upgrades rather than only new aircraft, because modular sensors, onboard processing, and secure connectivity deliver quicker capability gains. The market is also shaped by contested electromagnetic environments, which raise requirements for resilient communications, multi-sensor fusion, and low-latency dissemination to command networks. As military operations become more joint and in coalitions, interoperability and standardized data sharing are becoming core procurement criteria. Overall, airborne ISR is evolving into a networked, upgradeable capability, where sensors, software, and sustainment are as important as the platform itself.

The market is led by major defense primes and mission-system specialists spanning platforms, sensors, and integration. Boeing and Lockheed Martin support major airborne mission platforms and long-term modernization programs, while Northrop Grumman and General Dynamics contribute deep ISR integration, C4ISR architecture, and program delivery. Raytheon and Thales are important in advanced radars, electronic systems, and secure communications that turn sensor feeds into usable tracks. BAE Systems and Elbit Systems strengthen ISR capabilities through electronic warfare, SIGINT payloads, and upgrade cycles. FLIR Systems (Teledyne FLIR) supports EO/IR payload demand, and UTC Aerospace Systems (Collins Aerospace) contributes critical avionics and mission electronics.

Download Free sample to learn more about this report.

Airborne ISR Market Takeaways

- 2025 Market Size: USD 10.25 Billion

- 2026 Market Size: USD 10.65 Billion

- 2034 Forecast Market Size: USD 14.51 Billion

- CAGR: 3.9% from 2026–2034

- North America dominated the global airborne ISR market with a 34.82% share in 2025.

- The manned special-mission aircraft segment is anticipated to dominate with a 43.92% share in 2026.

- The systems segment is anticipated to lead the market with a 62.92% share in 2026.

North America

North America maintained its leading position with a market value of USD 3.57 billion in 2025, driven by advanced defense surveillance and reconnaissance programs.

Europe

Europe is projected to reach USD 2.79 billion in 2026, supported by increasing investments in airborne intelligence and defense modernization initiatives.

Asia Pacific

Asia Pacific is estimated to reach USD 2.63 billion in 2026, fueled by rising defense spending and growing demand for border surveillance capabilities.

U.S.

The U.S. airborne ISR market is estimated to reach USD 3.23 billion in 2026, supported by extensive military intelligence, surveillance, and reconnaissance operations.

Japan

Japan is expected to witness steady growth in airborne ISR adoption, driven by increasing investments in maritime surveillance and regional security enhancement programs.

Read More

MARKET DYNAMICS

Airborne ISR MARKET DRIVERS

Rising Situational Awareness to Support Market Growth

Airborne ISR continues to receive sustained funding as it directly supports mission success in modern defense operations. Threats move quickly, operate among civilian traffic, and use deception, driving commanders to demand persistent surveillance and rapid target confirmation. ISR enables targeting support, force protection, battle damage assessment, and strategic warning, so it sits at the center of today’s decision and strike cycles. This driver is particularly strong in wide-area missions that cover large areas, such as maritime surveillance and border security, where forces must detect and classify contacts early and then maintain track custody. Electronic warfare is another major driver. As jamming and spoofing become more common, militaries invest in resilient mission systems, hardened communications, and onboard processing so ISR remains useful when links degrade. Another key driver is joint and coalition operations. Modern missions depend on shared situational awareness, elevating the importance of ISR systems that integrate cleanly into command-and-control networks and support standardized data sharing. Fleet recapitalization and obsolescence management also sustain the market, as many special-mission fleets and mission electronics are aging, forcing modernization even when new aircraft buys are delayed.

Airborne ISR MARKET RESTRAINTS

Complex Integration, Lengthy Certification, and Export Limits Are Slowing Market Growth

Airborne ISR demand is strong, but execution is often slowed by practical constraints. The first major restraint is integration complexity. ISR is a full-stack capability that combines sensors, mission computers, encryption, data links, antennas, and ground exploitation systems, with performance that depends on all parts working together. If software maturity lags, bandwidth is insufficient, or interfaces are unstable, programs risk missing performance requirements and experiencing schedule delays. Certification and airworthiness present another restraint, especially for large UAS and major mission-system modifications. Flight testing, safety assessments, and regulatory approvals are time-intensive and extend beyond initial program plans. Export controls and security restrictions further limit speed and market reach.

Advanced SIGINT, certain radar capabilities, and cryptographic components can require lengthy approvals or lead to downgraded configurations, which can delay procurement decisions. Supply-chain constraints remain relevant, especially for high-end electronics and sensor components, where long lead times can bottleneck production and upgrades. Finally, procurement complexity itself acts as a restraint. ISR programs often involve classified requirements, multiple stakeholders, and long sustainment tails, which can slow contracting and change management. These restraints don’t reduce the strategic need for airbone ISR, but they increase the competitive advantage of vendors that can integrate reliably, certify efficiently, and offer exportable configurations with predictable delivery times.

AIRBORNE ISR MARKET TRENDS

Shifting Trend toward Modernization to Boost Industry Expansion

Airborne ISR is no longer defined by a single aircraft or individual sensor. Instead, it is shaped by how effectively the ISR mission system connects to joint and coalition networks and how quickly it can be upgraded. Defense customers are pushing for modular payload integration, allowing radars, EO/IR turrets, and SIGINT suites to be refreshed without long aircraft redesign cycles. This trend is closely linked to open-architecture thinking, where the mission computer and sensor interfaces are designed for repeatable upgrades. Platforms are increasingly expected to deliver tracks, alerts, and prioritized intelligence rather than pushing raw data to the ground. That reduces bandwidth demands and improves response times in real-world operations.

Operators also seek multi-sensor fusion, with radar, imagery, and signals reinforcing each other, as single-sensor outputs can be misleading in contested environments. Another important trend is distributed ISR operations. Militaries are increasingly blending manned special-mission aircraft, UAS, and maritime patrol assets to expand coverage without relying on a small number of high-value platforms. Finally, sustainment models are evolving toward continuous modernization. Instead of waiting for major mid-life upgrades, ISR fleets are receiving smaller, more frequent software and sensor updates. Overall, the trend is clear: airborne ISR is now being treated as an upgradeable combat system rather than a fixed aircraft configuration.

Download Free sample to learn more about this report.

MARKET OPPORTUNITIES

Fleet Upgrades to Present Key Market Opportunity

The strongest opportunity in airborne ISR is upgrading existing in-service fleets. Many operators continue to fly aircraft with mixed sensor baselines, older mission computers, and limited connectivity to modern command networks. This creates a clear market for targeted upgrade packages that improve detection, tracking, identification, and dissemination without waiting for new aircraft deliveries. Radar mode upgrades, improved EO/IR performance, refreshed SIGINT payloads, and mission-computer replacements can lift capability quickly as they target the most important performance bottlenecks. A second major opportunity is resilient connectivity. Increasing jamming, spectrum congestion, and long-range operations are pushing demand for better data links, smarter bandwidth management, and systems that still deliver usable outputs when connectivity is degraded. Another high-value opportunity is onboard analytics that reduces workload.

Airborne ISR produces massive volumes of video, radar returns, and signals data, so automation that flags anomalies, correlates tracks, and cues sensors can directly improve mission tempo. Interoperability represents a commercial opportunity, not just a technical requirement. Solutions that make sharing easier across services and coalition partners while respecting security rules reduce daily friction and tend to win follow-on contracts. Finally, sustainment is a durable opportunity. ISR fleets run high hours, require frequent calibration, and need regular software patching. Vendors who bundle modernization with long-term support can build recurring revenue while improving readiness for the customer.

MARKET CHALLENGES

Difficulty in Collecting Data to Deter Market Expansion

The hardest problem in airborne ISR is not collecting data, but remaining effective under pressure and producing intelligence that can be acted on quickly. Contested environments introduce jamming, cyber disruption, and integrated air-defense threats, which force platforms to operate less predictably and manage emissions carefully. ISR systems must continue to deliver useful outputs when links are degraded, which raises the importance of onboard processing and smart sensor management. The second major challenge is data overload. Modern EO/IR, radar, and SIGINT payloads generate more information than analysts can review in real time, especially during high-tempo operations. Without strong fusion and prioritization, ISR becomes slow and loses operational value.

Automation and AI offer solutions, but they introduce a trust challenge. Outputs must be reliable, resistant to deception, and stable across software updates, explainable enough for operators to act without hesitation. Interoperability is another persistent challenge. Coalition partners often use different networks, formats, and security rules, which slows sharing and can break track continuity during operations. Finally, readiness is a daily operational challenge. ISR fleets are high-utilization assets that require trained crews, maintainers, spares, calibration, and fast software support. The market will favor solutions that combine survivability, disciplined data workflows, and dependable sustainment, as that combination is what consistently turns sensing into decisions.

SEGMENTATION Analysis

By End User

Defense Segment Dominated due to its Battle Damage Assessment

By end user, the market is segmented into defense and homeland security.

The defense segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 78.97% share. Defense customers buy airborne ISR to find, track, and classify threats faster than the opponent. ISR supports mission planning, real-time targeting, battle damage assessment, and force protection. As threats diversify, militaries invest in multi-sensor fusion and resilient data delivery to ensure decision advantage.

The homeland security segment is expected to grow at a CAGR of 4.8% over the forecast period.

By Platform

Manned Special-Mission Aircraft Led due to High-Stakes Missions

By platform, the segment is classified into manned special-mission aircraft, UAS, maritime ISR aircraft, and others.

The manned special-mission aircraft segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 43.92% share. Manned ISR aircraft remain in demand as they can host heavy, power-hungry radars and SIGINT suites, support long missions with onboard operators, and integrate securely into classified networks. They are also trusted for high-stakes missions where assured communications, mission flexibility, and payload growth margins matter.

The UAS segment is expected to grow at a CAGR of 4.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Solution

Systems Segment Dominated due to Reduce Integration Risk

By solution segment is classified into systems, services, and software.

The systems segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 62.92% share. Demand is increasingly shifting toward integrated systems as customers seek a complete ISR chain: sensors, mission computers, fusion software, secure links, and ground exploitation. Integrated solutions reduce integration risk, speed upgrades, and improve interoperability. In contested environments, a tightly-integrated ISR system performs better than disconnected components.

The software segment is expected to grow at a CAGR of 5.3% over the forecast period.

By Application

Maritime Patrol Segment Dominated due to its Ability to Detect and Classify Contacts

By application, the segment is classified into maritime patrol, airborne ground surveillance (AGS), airborne early warnings (AEW), and signals intelligence (SIGINT).

The maritime patrol segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 27.97% share. Maritime patrol ISR is growing as nations must monitor sea lanes, EEZs, and contested waters. These missions need wide-area radar, EO/IR, AIS/ESM, and long endurance to detect and classify contacts, cue response forces, and support ASW/ASuW.

The signals intelligence (SIGINT) segment is expected to grow at a CAGR of 4.7% over the forecast period.

AIRBORNE ISR MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Airborne ISR Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 3.44 Billion and also maintained its leading share in 2025 with USD 3.57 billion. North America’s airborne ISR demand stays strong as the U.S. and allies are modernizing aging special-mission fleets while pushing ISR into joint, real-time networks. Funding prioritizes upgraded radars, EO/IR, SIGINT, resilient data links, and mission software. The region also sustains high readiness needs, which keep upgrades and sustainment contracts active.

In 2026, the U.S. market is estimated to reach USD 3.23 billion. U.S. demand remains high as ISR aircraft and UAS are constantly tasked across theaters. The priority is improving survivability and speed-to-insight through better sensors, onboard processing, and secure connectivity. Recapitalization planning plus ongoing mission-system upgrades keep procurement and sustainment spend steady.

Europe

The European region is projected to record a growth rate of 4.1% and touch the valuation of USD 2.79 billion in 2026 during the forecast period. Europe is expanding airborne ISR to strengthen deterrence and reduce dependency on external suppliers. Countries are investing in persistent surveillance, coalition interoperability, and faster sensor refresh cycles. Demand is driven by border monitoring, maritime awareness, and modernization of mission systems to operate in contested electronic-warfare environments.

Asia Pacific

The market in Asia Pacific is estimated to reach USD 2.63 billion in 2026. The growth is led by the need to monitor large maritime zones and air approaches. Countries are expanding maritime patrol ISR, long-endurance UAS, and multi-mode radars to track surface and air activity. The focus is on persistent coverage, quicker cueing of response forces, and better intelligence sharing across services.

Rest of the World

The Rest of the World market is expected to record USD 1.54 billion by 2026. In the Rest of the world, the airborne ISR segment is shaped by border surveillance, counter-smuggling, and protection of critical infrastructure. Buyers tend to prioritize practical, modular solutions, EO/IR, maritime radars, and upgrade kits, as they deliver measurable outcomes without the cost and complexity of high-end, bespoke ISR fleets.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Forging Contracts to Gain Market Share

Airborne ISR competition is shaped by a concentrated group of prime contractors and subsystem leaders that collectively cover the full value chain from aircraft integration to actionable sensor output. Boeing and Lockheed Martin anchor large airborne mission platforms and long-term modernization pipelines, while Northrop Grumman and General Dynamics bring deep ISR mission-system integration, C4ISR architecture, and program-scale delivery. Raytheon and Thales play influential roles in multi-mode radar, electronic systems, and secure communications that convert airborne sensing into usable tracks.

BAE Systems and Elbit Systems strengthen the market through electronic warfare, SIGINT/ISR payloads, and rapid upgrade cycles that keep fleets relevant as threats evolve. FLIR Systems (now part of Teledyne) remains central to EO/IR payload demand, supporting persistent surveillance and targeting-quality imagery across manned and unmanned fleets. UTC Aerospace Systems (now Collins Aerospace) adds critical avionics, mission electronics, and reliability-focused subsystems that reduce downtime. Together, these players drive growth by bundling sensors, software, and sustainment into upgradeable ISR.

LIST OF KEY AIRBORNE ISR COMPANIES PROFILED

- Boeing (U.S.)

- BAE Systems (U.K.)

- Elbit Systems Ltd (Israel)

- FLIR Systems Inc (U.S.)

- Northrop Grumman (U.S.)

- General Dynamics (U.S.)

- Thales (France)

- Raytheon (U.S.)

- UTC Aerospace Systems (U.S.)

- Lockheed Martin Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025 - Voyager Technologies won a USD 21 million contract from the Air Force Research Laboratory to develop AI-powered intelligence, surveillance, and reconnaissance (ISR) capabilities for airborne missions.

- December 2025 - Volatus Aerospace Inc. received a defense contract worth up to USD 6.3 million to deliver a next-generation interim training system for ISR operations to an allied defense organization.

- December 2025 - The Naval Air Systems Command plans to award delivery orders under four basic ordering agreements to support contractor-owned, contractor-operated ISR services for land- and sea-based unmanned aerial systems.

- July 2025 - L3Harris Technologies secured a USD 300 million contract from Italy for two Gulfstream G550 aircraft equipped with an advanced electromagnetic warfare system. The company collaborated with BAE Systems, marking the first U.S. government approval for an EA-37B sale to a foreign ally.

- October 2022 - MAG Aerospace and L3Harris Technologies would supply upgraded ISR aircraft to support the U.S. Army's Theater Level High-Altitude Expeditionary Next Airborne ISR Radar (ATHENA-R) program.

REPORT COVERAGE

This report provides a concise view of the airborne ISR market share, covering key players across aircraft/UAS platforms, ISR payloads, mission systems/software, and sustainment services. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.9% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By End User · Defense · Homeland Security |

|

By Platform · Manned Special-mission Aircraft · UAS · Maritime ISR Aircraft · Others |

|

|

By Solution · Systems · Services · Software |

|

|

By Application · Maritime Patrol · Airborne Ground Surveillance (AGS) · Airborne Early Warnings (AEW) · Signals Intelligence (SIGINT) |

|

|

By Geography · North America (By End User, Platform, Solution, and Application) o U.S. (By End User) o Canada (By End User) · Europe (By End User, Platform, Solution, and Application) o U.K. (By End User) o Germany (By End User) o France (By End User) o Russia (By End User) o Rest of Europe (By End User) · Asia Pacific (By End User, Platform, Solution, and Application) o China (By End User) o Japan (By End User) o India (By End User) o Rest of Asia Pacific (By End User) · Rest of the World (By End User, Platform, Solution, and Application) o Middle East and Africa (By End User) o Latin America (By End User) |

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 10.25 billion in 2025 and is estimated to reach USD 14.51 billion by 2034.

The market is growing at a CAGR of 3.9% during the projection period (2026-2034).

The defense segment is estimated to be the leading segment in this market during the forecast period.

The manned special-mission aircraft segment led the market.

Boeing (U.S.), BAE Systems (U.K.), Elbit Systems Ltd (Israel), FLIR Systems Inc (U.S.), Northrop Grumman (U.S.), and General Dynamics (U.S.) are some of the leading players in the market.

North America held the largest shareholder in the market.

- 2021-2034

- 2025

- 2021-2024

- 223

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us