Aircraft Cleaning Services Market Size, Share & Industry Analysis by Service Type (Exterior Cleaning, Interior Cleaning, & Specialized Services), By Cleaning Process (Traditional Chemical-based & Water-based Cleaning, Dry Wash & Waterless Cleaning, Robotic & Automated Cleaning Solutions, and UV-light & Electrostatic Disinfection), By Service Provider (On-demand Cleaning Services, Ground Handling Operators, and MRO Cleaning Services), By End-User (Airports (Greenfield & Brownfield), Airlines and Operators, and Military & Defense Organizations), By Aircraft Type, and Regional Forecast, 2026-2034

Aircraft Cleaning Services Market Size and Future Outlook

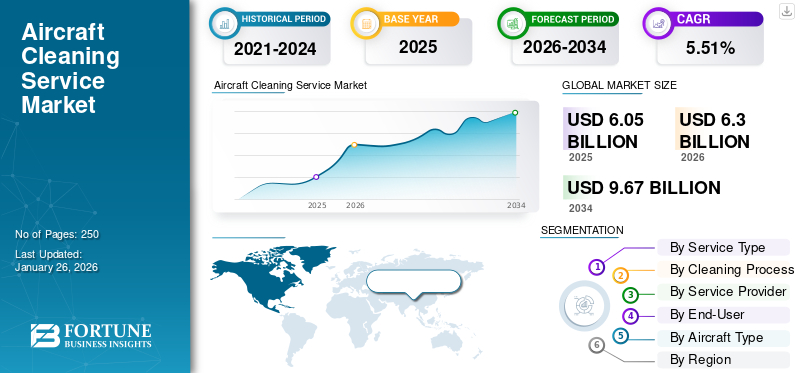

The global aircraft cleaning services market size was valued at USD 6.05 billion in 2025. The market is projected to grow from USD 6.30 billion in 2026 to USD 9.67 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 5.51% during the forecast period. North America dominated the aircraft cleaning service market with a market share of 32.06% in 2025.

The global market has emerged as a critical enabler of operational efficiency, passenger satisfaction, and regulatory compliance within the aviation industry. Airlines, airports, and maintenance providers are investing heavily in systematic cleaning and disinfection processes to maintain fleet hygiene and ensure safety. Post-COVID, the emphasis on cleanliness and passenger well-being has accelerated the adoption of advanced solutions such as UV disinfection, electrostatic spraying, and waterless cleaning methods. Moreover, with the rapid expansion of global passenger traffic — particularly in Asia Pacific and the Middle East — the need for frequent turnaround cleaning, exterior washing, and specialized interior sanitation has grown significantly. Contract awards across major airports such as the Miami International Airport (ABM, 2025) and Düsseldorf Airport (Klüh Group, 2025) underline the strong demand for outsourced professional cleaning solutions. However, the sector faces challenges in balancing sustainability goals, cost pressures, and technological transitions. Overall, the market is undergoing a structural shift from manual, chemical-heavy approaches toward automated cleaning systems and eco-friendly cleaning technologies.

Swissport International, ABM Aviation, and Immaculate Flight are recognized as leaders in the aircraft cleaning services market, each driving innovation and service quality across airports globally. Swissport has demonstrated exceptional growth, expanding to dozens of new airports and investing heavily in sustainability with its transition to electric ground support equipment and eco-friendly technologies. ABM Aviation continues to enhance operational efficiency at major U.S. hubs by focusing on reliability and rapid service. Immaculate Flight, with over 20 years of experience, provides meticulous aircraft detailing nationwide, catering to both commercial and private aviation clients with tailored cleaning solutions. These companies combine operational excellence, technological advancements, and a steadfast commitment to safety and sustainability, reinforcing their leading market positions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Rising Passenger Traffic and Hygiene Standards to Propel Service Demand

The growth of global air travel is the primary force driving the demand for aircraft cleaning services. According to IATA, the passenger traffic is forecasted to double by 2040, with Asia Pacific and the Middle East witnessing the fastest growth rates. Each additional passenger flight generates higher cleaning frequency requirements, from cabin vacuuming and lavatory sanitation to deep-cleaning cycles between long-haul operations. Commercial airlines are increasingly bound by strict hygiene regulations set by ICAO, EASA, and the FAA, which require adherence to standardized cleaning and disinfection protocols. Moreover, consumer expectations of comfort and safety heightened after the pandemic and continue to push airlines to prioritize cabin hygiene, propelling aircraft cleaning services market growth.

- For example, Delta and other major carriers announced ongoing enhancements to cleaning protocols in 2025, including electrostatic spraying and antimicrobial surface treatments. In effect, the combination of regulatory mandates and growing traffic translates into recurring cleaning demand, making it a core operational necessity rather than a discretionary expense.

MARKET RESTRAINTS:

High Operational Costs and Labor Dependency to Constrain the Market for Aircraft Cleaning

While the demand for aircraft cleaning is robust, the industry faces strong cost pressures that act as a restraint. Cleaning processes, particularly exterior fuselage washing and engine degreasing, involve high water, chemical, and labor costs. Airlines operating on thin margins often struggle to absorb these expenses, especially in emerging markets where profitability is volatile. Labor shortages and unionized staffing add to the challenge, as cleaning is labor-intensive and often scheduled during narrow turnaround windows.

- In May 2025, Denver International Airport approved over USD 25 million in cleaning contracts, underscoring the scale of expenditure airports must commit to basic sanitation. The reliance on manual labor also introduces variability in service quality and timeliness. Furthermore, environmental penalties for excessive chemical and water usage are increasing, adding compliance-related expenses. As a result, the cost burden restricts smaller service providers and regional airlines from scaling cleaning operations efficiently, creating a market imbalance.

MARKET OPPORTUNITIES:

Market Presents Growth Opportunities with the Adoption of Eco-Friendly and Automated Solutions

The transition toward sustainable and technology-driven cleaning methods presents a significant opportunity for key players. With increasing regulatory scrutiny on environmental performance, airlines are actively seeking waterless cleaning, bio-based chemicals, and robotic solutions that minimize resource usage. For instance, Schiphol Airport (October 2024) awarded contracts emphasizing sustainable cleaning practices, reflecting airports’ growing preference for environmentally friendly vendors. Similarly, UV-light and electrostatic disinfection technologies have gained traction due to their ability to quickly sanitize large cabin areas without chemical residues. Robotic cleaning units, though at a nascent stage, are being piloted in Asia and Europe, where airports are under pressure to achieve carbon neutrality. This creates opportunities for service providers to differentiate by offering innovative, eco-compliant solutions. Partnerships between airlines, MROs, and specialized cleaning firms could further accelerate adoption. As sustainability becomes a competitive differentiator, early movers in green and automated cleaning stand to capture premium contracts and long-term strategic alliances.

AIRCRAFT CLEANING SERVICES MARKET TRENDS:

UV-light and Electrostatic Disinfection Systems to Act as A Major Technological Trend

Technological innovation is rapidly reshaping the aircraft cleaning services market, driven by the dual imperatives of efficiency and sustainability. Traditional manual cleaning methods, which rely heavily on chemical detergents and water, are increasingly being replaced or supplemented by automated and eco-friendly alternatives. One of the most notable trends is the adoption of UV-light and electrostatic disinfection systems, which allow faster, chemical-free sanitization of cabin surfaces. Major airlines, including Delta and Lufthansa, have incorporated these technologies post-COVID, reducing turnaround times while enhancing passenger safety. Similarly, robotic cleaning solutions are emerging, particularly in high-volume airports across Asia and Europe, where autonomous units can clean cabin floors and sanitize lavatories with minimal human intervention. Another important trend is the rise of waterless and dry-wash techniques, which address growing environmental concerns about water consumption. These methods lower ecological impact and also reduce aircraft downtime, aligning with airlines’ operational efficiency goals. Data-driven monitoring tools are also being introduced, enabling service providers to track cleaning cycles, resource usage, and compliance through digital dashboards, improving transparency for airlines and regulators. Airports such as Schiphol (October 2024 contracts) have explicitly tied vendor selection to sustainable and technology-enabled cleaning practices, signaling an industry-wide shift.

Overall, technological advancement is moving the market from a labor-intensive model toward a hybrid of human expertise and machine efficiency. This shift is creating new competitive dynamics, where providers offering automation, eco-solutions, and digital compliance tools gain a decisive edge in securing long-term contracts.

MARKET CHALLENGES:

Fragmentation and Standardization Gaps Present Threats to Market Growth

A major challenge in the aircraft cleaning services market lies in its fragmented structure and lack of global standardization. Service providers range from multinational facility management firms such as ABM to regional contractors, resulting in highly variable service quality. This inconsistency complicates compliance for international carriers that operate across multiple jurisdictions. For example, contracts awarded at Phoenix Sky Harbor (USD 25 million to ABM in June 2024) and Düsseldorf Airport (Klüh, February 2025) illustrate how contract scope and standards differ widely across geographies. While ICAO and IATA provide general cleaning and disinfection guidance, enforcement remains decentralized, leaving interpretation to local authorities and operators. Additionally, the fragmented nature of procurement —often airport-by-airport— creates inefficiencies for large service providers seeking economies of scale. The result is a competitive market prone to underbidding, where price often outweighs innovation or sustainability credentials. This lack of harmonized standards poses a long-term challenge for global market consolidation and the establishment of universally recognized best practices.

Download Free sample to learn more about this report.

Segmentation Analysis

By Service Type

Rising Passenger Expectations and Hygiene Regulations to Fuel Interior Cleaning Demand

On the basis of service type, the market is classified into exterior cleaning, interior cleaning, and specialized services.

The interior cleaning segment is expected to lead the market, contributing 44.81% globally in 2026. The rise in global passenger traffic directly translates into higher cleaning frequency, as each flight generates the demand for cabin hygiene. Post-pandemic, passengers now view cleanliness as a core component of flight safety and comfort, compelling airlines to maintain rigorous standards. Regulatory authorities such as ICAO and FAA have also reinforced cleaning and disinfection guidelines, ensuring that compliance becomes a non-negotiable requirement for operators.

For example, Delta Air Lines, in 2025, announced enhancements to its cleaning protocols, including electrostatic spraying across cabins, reinforcing the trend toward continuous improvements in interior hygiene. This strong combination of regulatory enforcement, passenger expectations, and technological adoption ensures that interior cleaning remains the largest and fastest-growing service type in the market.

The specialized services segment is poised to exhibit significant growth over the coming years. This expansion can be credited to airline competition, where service quality, including cabin hygiene, acts as a brand differentiator. Premium carriers invest more heavily in interior and exterior upkeep to attract business travelers, while low-cost carriers adopt quick but frequent cleaning cycles to maintain high aircraft utilization. The introduction of UV-light disinfection and antimicrobial treatments further reflects the shift toward faster, more efficient cabin sanitation methods.

By Cleaning Process

Benefit of Reduced Time for Sanitation to Propel Robotic & Automated Cleaning Solutions Segment

In terms of cleaning process, the market is categorized into traditional chemical-based cleaning, water-based cleaning, dry wash & waterless cleaning, robotic & automated cleaning solutions, and UV-light & electrostatic disinfection, contributing expected share 30.46% globally in 2026.

The robotic & automated cleaning solutions segment records the strongest growth and addresses labor shortages and quick turnaround requirements. Automated systems for fuselage washing and cabin sanitation reduce time and also ensure consistency and safety for ground staff.

Traditional chemical-based cleaning remains widely used due to its cost-effectiveness and strong stain removal capacity. However, growing environmental concerns and rising water scarcity are pushing operators toward alternatives. Water-based cleaning, though effective for fuselage and engine washing, is gradually being supplemented by dry wash and waterless cleaning methods that reduce water consumption by up to 90%, aligning with global sustainability goals and airport green initiatives.

Meanwhile, the use of UV-light and electrostatic disinfection technologies surged post-COVID-19, providing airlines with faster and more reliable solutions for microbial control. These methods are particularly valuable in interior cleaning, where hygiene directly impacts passenger confidence.

In 2024, Lufthansa Technik expanded trials of UV-C cabin disinfection systems, highlighting the industry’s pivot toward advanced cleaning technologies. This evolution underscores how regulatory pressure, sustainability, and passenger expectations are reshaping cleaning process segmentation.

To know how our report can help streamline your business, Speak to Analyst

By Service Provider

MRO Cleaning Services Segment to Depict Robust Demand with Vitality for Ensuring Safety Compliance

Based on service provider, the market is segmented into on-demand cleaning services, ground handling operators, and MRO cleaning services. Each of these services plays a distinct role in meeting airline requirements.

The MRO cleaning services segment held the dominating position accounting for 44.49% market expected share in 2026. By solution, the software segment held the share of 43.81% in 2024. MRO (Maintenance, Repair, and Overhaul) cleaning services focus on deep-cleaning during scheduled maintenance checks, including engine degreasing, wheel well washing, and cabin refurbishments. These services are critical for extending aircraft lifespan and ensuring safety compliance.

On-demand cleaning providers are gaining traction due to the flexibility they offer, especially for charter operators, private jets, and smaller regional carriers. Their ability to provide specialized services, such as dry wash or antimicrobial treatments, makes them attractive for operators looking for scalable, tailored cleaning solutions.

The ground handling operators segment depicts significant growth, as they manage routine cleaning during flight turnarounds in addition to baggage, catering, and refueling operations. Their integration with airport operations ensures efficiency and cost-effectiveness, particularly for high-frequency short-haul flights. Airlines increasingly outsource to these players to reduce operational costs while maintaining compliance with hygiene regulations.

In 2025, Swissport announced expanded cleaning service offerings integrated into its ground handling portfolio, reinforcing how ground handling operators are diversifying into cleaning to capture growing demand. This segmentation reflects a balance between efficiency-driven outsourcing and specialized cleaning needs.

By End-User

Increasing Air Travel Demand Fuels Growth in the Airlines and Operators Segment

Based on end-user, the market is segmented into airports, airlines and operators, and military & defense organizations.

The airlines and operators segment is anticipated to hold a dominant market share of 55.54% in 2026, holding more than 50% share. The segment is poised for growth due to the continuing rise in global air passenger traffic, which directly translates to increased aircraft utilization and demand for thorough cleaning. According to Airports Council International (ACI World), in 2025, the global air passenger traffic is projected to reach 9.8 billion, reflecting nearly 4% increase from the previous year and signaling a strong recovery in aviation activity. This surge in passengers means more flights and quicker turnaround times, which compel airlines and operators to maintain high standards of cleanliness and hygiene to ensure passenger safety, comfort, and regulatory compliance. Rising international travel, which is growing faster than domestic routes, also drives the need for consistent sanitation to control health risks in long-haul and high-traffic environments. Additionally, airlines are increasingly adopting advanced cleaning technologies and eco-friendly products to meet sustainability goals while managing higher operational demands. This convergence of rising passenger volumes, stricter hygiene expectations, and technological advancements ensures robust growth for aircraft cleaning services focused on airlines and operators.

Supporting this, recent data from the International Air Transport Association (IATA) highlights record-high load factors and increasing flight capacities, pointing to the importance of effective cleaning services as integral to operational efficiency and passenger confidence in 2025.

The airports segment accounted for a significant market share and is expected to grow at CAGR of 5.50% over the forecast period.

By Aircraft Type

Efficient Cleaning Solutions for High-Traffic Narrow-Body Aircraft

Based on aircraft type, the market is segmented into narrow-body aircraft, wide-body aircraft, regional aircraft, business jets, general aircraft, helicopters, and military aircraft.

The narrow-body segment held the dominating position in 2024, accounting for more than 35% share. Narrow-body aircraft require specialized cleaning routines due to their high utilization in short to medium-haul flights. Cleaning methods often involve wet washing, dry washing, and polishing, with wet washing used for heavy dirt and grime removal, and dry washing suitable for routine maintenance between flights. Robotic washing solutions are increasingly used, significantly reducing water consumption and cleaning time. For instance, robotic wet washing a narrow-body aircraft typically uses 200-250 liters of water-detergent mix, whereas manual cleaning can consume up to 10,000 liters. Cleaning focuses on critical areas such as wings, tail, underbelly, and sensors to maintain aerodynamics and safety. Efficient cleaning is essential to maintain quick turnaround times in busy airports where narrow-body aircraft primarily operate.

The general aircraft segment is anticipated to expand at a CAGR of 5.30% over the analysis period.

Aircraft Cleaning Services Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Aircraft Cleaning Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America region captured 32.06% of the global market in 2025, generating USD 1.94 billion in revenue, and is projected to reach USD 2.02 billion in 2026. North America dominates the global market due to the steady service demand with stringent safety and hygiene regulations set by authorities to ensure passenger health and aircraft performance. Airlines are required to frequently clean both the exterior and interior, including cabins, engines, and landing gears, to prevent contamination and maintain operational efficiency. The region also places a strong emphasis on sustainability, encouraging the use of eco-friendly cleaning products and water-saving methods. The incorporation of advanced technologies, such as robotic cleaning and biodegradable chemicals, enhances efficiency and reduces environmental impact. This regulatory and technological focus, combined with large passenger volumes and a mature aviation sector, drives continuous demand for professional aircraft cleaning services. The U.S. market is projected to reach USD 1.78 billion by 2026.

- September 2025 – North American military aviation operators implemented advanced robotic and sensor-guided aircraft interior cleaning technologies to enhance sanitation efficiency and crew safety. This initiative integrates environmentally friendly disinfectants and data-driven cleaning schedules, aligning with stringent regulatory standards and supporting military readiness and operational compliance.

Europe

Europe maintained a strong presence in the global market, reaching USD 1.69 billion in 2025, accounting for 27.91% share, and is expected to reach USD 1.75 billion in 2026. Europe is seeing fast-tracked investments in aircraft cleaning services capabilities. Europe's market is propelled by strict hygiene regulations enforced by agencies such as the European Union Aviation Safety Agency (EASA). Airlines adhere to rigorous sanitation protocols to meet passenger safety expectations and comply with health mandates, particularly after increased awareness following global health crises. Additionally, Europe’s commitment to environmental responsibility fosters the adoption of green cleaning technologies, such as waterless cleaning and bio-based chemicals, reducing the carbon footprint of maintenance activities. Investment in aviation infrastructure and passenger growth further boost cleaning services demand, aligning with Europe's reputation for high operational and environmental standards. The UK market is projected to reach USD 0.65 billion by 2026, while the Germany market is projected to reach USD 0.22 billion by 2026.

Asia Pacific

In 2025, Asia Pacific generated USD 1.53 billion, contributing 25.37% to global market revenue, and is projected to grow to USD 1.61 billion in 2026. The Asia Pacific region experiences rapid growth and is expected to grow at the highest CAGR over the forecast period, driven by expanding air travel, increased domestic and international flights, and fleet expansions in countries such as China, India, and Southeast Asia. This surge in passengers increases the frequency and scale of cleaning operations needed to sustain safety and comfort. Airlines face pressure to maintain high hygiene standards to reassure passengers, especially in the context of health safety post-pandemic. Technological adoption is rising but variability in infrastructure requires service providers to tailor solutions to diverse markets. The combination of booming passenger numbers and rising environmental consciousness creates strong growth opportunities. The Japan market is projected to reach USD 0.34 billion by 2026, the China market is projected to reach USD 0.65 billion by 2026, and the India market is projected to reach USD 0.32 billion by 2026.

Rest of the World

Rest of the World contributed 14.65% to the global market in 2025, with a valuation of USD 0.89 billion, and is projected to reach USD 0.91 billion in 2026. Over the forecast period, the rest of the world, comprising Latin America and the Middle East & Africa regions, would witness moderate growth in this market. The rest of the world region, shows growing demand for aircraft cleaning services fueled by increasing air traffic, new airline routes, and airport infrastructure modernization. The Middle East acts as a global aviation hub with heavy traffic requiring rigorous cleaning schedules, while Latin America and Africa expand their domestic and international air travel markets. These regions are increasingly adopting international cleanliness and safety standards. The growing awareness of hygiene and passenger safety, alongside investments in sustainable cleaning practices, are key drivers for the rising need for professional aircraft cleaning services across these emerging markets.

COMPETITIVE LANDSCAPE

Key Industry Players:

Wide Range of Product Offerings Coupled with a Strong Distribution Network of Key Companies Support their Leading Position

The competitive landscape of the aircraft cleaning services market features a mix of well-established global players and emerging companies, each focused on innovation, sustainability, and comprehensive service offerings. Leading companies include Immaculate Flight, ABM Industries, and Jet Fast, known for their extensive experience and broad service portfolios covering both commercial and military aircraft. These companies leverage advanced cleaning technologies, eco-friendly products, and robotic systems to meet rising hygiene standards and operational efficiency demands.

Immaculate Flight focuses on delivering high-quality cleaning and detailing services while emphasizing sustainability. ABM Industries, a major facility solutions provider, offers wide-ranging aircraft cleaning services with strong capabilities in operational scale and customer service. Jet Fast is recognized for innovation and tailored cleaning solutions catering to diverse airline and operator needs.

Apart from these, specialized companies such as Diener Aviation Services and Sharp Details compete by targeting niche markets and offering specialized exterior and interior cleaning, including polishing and disinfecting services. The market is moderately fragmented, driven by investments in green cleaning products, strategic partnerships, and automation technologies that enhance efficiency and environmental compliance. Competition is also fueled by the increasing demand for bio-based and non-toxic cleaning chemicals, with companies continually adapting to evolving regulatory and passenger expectations. This competitive environment encourages continuous product and service innovation to maintain market leadership.

LIST OF KEY AIRCRAFT CLEANING SERVICES COMPANIES PROFILED:

- ABM Aviation (U.S.)

- PrimeFlight Aviation Services (U.S.)

- Clay Lacy Aviation (U.S.)

- Swissport (Switzerland)

- Top Flight Detailing (U.S.)

- HHS Aviation (U.S.)

- New England Aircraft Detailing (U.S.)

- RealClean Aircraft (U.S.)

- Avizone Aviation (U.S.)

- Lonestar Aviators (U.S.)

- Diener Aviation Services (U.S.)

- JetFast Cleaning (U.S.)

- Hangar 48 Detailing Company (U.S.)

- Pacific Aviation Corporation (U.S.)

- ERMC Aviation (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In August 2025, Heathrow Airport rolled out 32 cobots and UV-disinfection robots across terminals to automate floor and surface cleaning. This highlights airports’ growing shift toward automation and reduced dependence on manual cleaning labor.

- In July 2025, Tork’s Vision Cleaning system had been deployed across five of the world’s ten busiest airports, serving 1.2 billion travelers. This demonstrates the rapid expansion of data-driven cleaning technologies in global aviation hubs.

- In June 2025, Noida International Airport deployed India’s first indigenous Runway Rubber Removal Machine, reducing chemical usage and improving runway safety. The move reflects the growing adoption of sustainable cleaning solutions across airports under the “Make in India” initiative.

- In May 2025, Mumbai International Airport introduced autonomous scrubber robots in Terminal 2, enhancing hygiene and efficiency. The initiative was driven by post-pandemic passenger expectations and rising traffic, signaling greater adoption of robotic cleaning solutions.

- In May 2025, Hindustan Aeronautics Ltd expanded civilian MRO operations in Nashik, including overhauls of Embraer aircraft. The increase in deep maintenance drives higher demand for specialized aircraft cleaning services such as engine degreasing and cabin refurbishment.

- In April 2025, Lucknow International Airport introduced smart cleaning robots in Terminal 3, capable of scrubbing and drying floors autonomously. The project improves water efficiency and coverage, aligning with sustainability goals.

- In March 2025, CleanCore Solutions deployed eco-friendly terminal cleaning technology at a New York airport, replacing harsh chemicals with sustainable alternatives. This reflects the increasing push for green cleaning in aviation infrastructure.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.51% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Service Type

By Cleaning Process

By Service Provider

By End-User

By Aircraft Type

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.05 billion in 2025 and is projected to reach USD 9.67 billion by 2034.

In 2025, the North America market value stood at USD 1.94 billion.

The market is expected to exhibit a CAGR of 5.51% during the forecast period of 2026-2034.

In 2024, the narrow-body aircraft segment led the market by aircraft type.

The rising passenger traffic and hygiene standards are key factors propelling the market.

ABM Aviation (U.S.), PrimeFlight Aviation Services (U.S.), and Swissport (Switzerland) are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us