Aircraft Cooling System Market Size, Share & Industry Analysis, By System Type (Air-Cycle Cooling Systems, Liquid Cooling Systems, Vapor-Cycle Cooling Systems, and Others), By Application (Cabin & Cockpit Cooling, Avionics & Electronics Cooling, Propulsion & Engine Thermal Management, and Others), By Aircraft Type (Commercial Aircraft, Regional Aircraft, Business & General Aviation Aircraft, and Others), By Component (Heat Exchangers & Pre-Coolers, Air-Cycle Machines, and Others), By End User (OEM Line-Fit, Aftermarket/MRO/Replacement, and Others), and Regional Forecast, 2026-2034

Aircraft Cooling System Market Size and Future Outlook

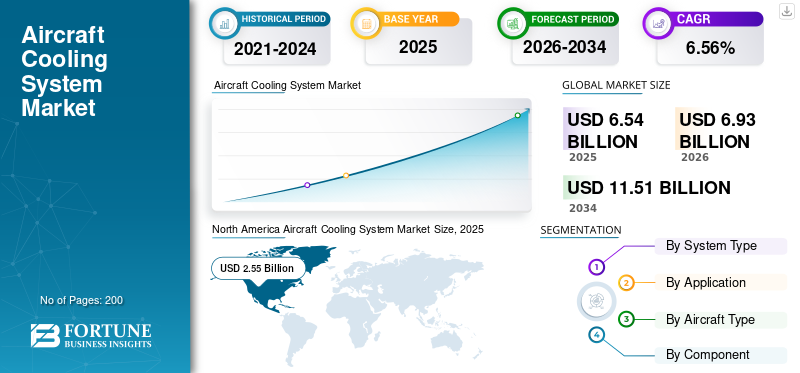

The global aircraft cooling system market size was valued at USD 6.54 billion in 2025. The market is projected to grow from USD 6.93 billion in 2026 to USD 11.51 billion by 2034, exhibiting a CAGR of 6.56% during the forecast period. North America dominated the aircraft cooling system market with a market share of 38.99% in 2025.

The aircraft cooling system market encompasses thermal management solutions for engines, avionics, environmental control systems, cabin interiors, and emerging electric aircraft platforms. Key systems include air-cycle machines, vapor-cycle systems, liquid-cooling loops, heat exchangers, ram-air cooling, and advanced electric or hybrid thermal architectures. Rising aircraft production, denser avionics, greater cabin comfort requirements, and the shift toward more-electric aircraft are driving demand. Aircraft such as the Boeing 787 highlight this transition, with electrically driven systems helping improve overall fuel efficiency. Furthermore, the market serves commercial aircraft, military platforms, rotorcraft, unmanned aerial vehicles (UAVs), and hybrid-electric aircraft.

Major players include Collins Aerospace, Honeywell International Inc., Liebherr, and AMETEK Aerospace & Defense, with focus areas spanning ECS and heat exchangers, liquid cooling, and MRO services.

Download Free sample to learn more about this report.

AIRCRAFT COOLING SYSTEM MARKET TRENDS

Shift Toward Bleedless and Electrified Cooling Architectures Accelerating Across Aviation Platforms is a Market Trend

Aircraft cooling systems are moving from conventional bleed-air architectures toward electrically driven and hybrid thermal-management designs. Boeing states that the 787 uses more electric systems to optimize performance and reduce fuel use, while Clean Aviation is developing electric ECS concepts that combine air-cycle and vapor-cycle cooling for future single-aisle aircraft. This shift is driven by the need to reduce engine power extraction, improve energy efficiency, and support higher avionics and power-electronics heat generation loads. NASA also notes that MW-scale electrified aircraft generate significant waste heat, making lightweight thermal management a critical design priority

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Fuel Efficiency Mandates and Emission Reduction Targets to Fuel Market Growth

Bleed-air extraction to power conventional ECS directly penalizes engine performance by increasing fuel consumption, making it a primary candidate for optimization as the aviation sector advances sustainable technology development. International frameworks, including CORSIA, impose carbon-reduction obligations on airlines and aircraft manufacturers, directing R&D investment toward lightweight, high-efficiency cooling components. The Montreal Protocol's mandated phase-down of high-GWP refrigerant R134a, targeting a 69% reduction by 2024 and 76% by 2027, is simultaneously accelerating the search for alternative refrigerants and the redesign of vapor-cycle cooling systems across commercial aviation ECS. Together, these regulatory pressures are transforming thermal management from a support function into a strategic differentiator for aircraft OEMs and their Tier-1 cooling system suppliers. This is expected to boost the aircraft cooling system market growth in the coming years.

MARKET RESTRAINTS

Stringent Airworthiness Certification and Long Design-In Cycles Hinder Market Growth

Aircraft cooling systems are subject to strict FAA, EASA, and national certification requirements, with extensive testing, validation, and documentation required before flight approval. The shift toward higher-efficiency ECS, bleed-free designs, and lower engine-pressure architectures often requires new system layouts rather than simple component upgrades, adding cost and development time. Advanced liquid- and two-phase-cooling suppliers face even higher entry barriers, as qualification can take years and requires dedicated test infrastructure. As a result, established aerospace suppliers with certification experience, proven products, and regulatory relationships hold a clear advantage, while newer thermal-management technologies may take longer to reach production aircraft.

MARKET OPPORTUNITIES

Hydrogen Propulsion and eVTOL Platforms Opening Entirely New Thermal Management Design Space

Conventional ram air cooling systems for fuel cell power plants impose severe performance penalties for single-aisle aircraft when fuel cell heat loads exceed 10 MW, and advanced heat exchanger technology, alongside two-phase cooling approaches, offers pathways to reduce gravimetric and volumetric heat densities, enabling design closure for future hydrogen-electric aircraft. NASA-released electrified aircraft propulsion concepts spanning urban air mobility, regional, and single-aisle markets require dedicated liquid-based thermal management systems, with cooling requirements and system weight varying significantly based on electrical component efficiencies and operating temperature limits. Battery-powered eVTOL aircraft, hydrogen fuel-cell regional jets, and hybrid-electric commuter platforms each introduce distinct thermal architectures, providing suppliers with diversified product development opportunities beyond conventional ECS.

MARKET CHALLENGES

Raw Material Volatility and Aerospace Supply Chain Fragility Disrupting Production Schedules

Aerospace cooling system suppliers face pressure from volatile material costs and supply-chain constraints. Key inputs such as aluminum, titanium, nickel alloys, advanced composites, and specialized coatings are critical for heat exchangers and thermal-management components, but pricing and availability remain unstable. Geopolitical tensions, especially around titanium supply, add further risk, while shortages in precision machining and skilled aerospace labor affect delivery schedules. These pressures make long-term cost forecasting and margin protection difficult, particularly for smaller suppliers. As aircraft production ramps up, supply reliability becomes a major challenge, increasing the risk of delays, higher prices, and supplier consolidation.

Segmentation Analysis

By System Type

Efficiency, Weight Reduction, and Proven ECS Performance to Boost Demand for Air-Cycle Cooling Systems

Based on the system type, the market is segmented into air-cycle cooling systems, liquid cooling systems, vapor-cycle cooling systems, engine & powertrain cooling systems, advanced thermal management systems, and others.

The air-cycle cooling systems segment is anticipated to account for the largest market share over the forecast period. Air-cycle cooling remains a preferred approach in aircraft environmental control systems due to its low weight, dependable operation, and strong compatibility with existing aircraft architectures.

The liquid cooling systems segment is anticipated to rise with a high CAGR of 7.11% over the forecast period.

By Application

Rising Comfort Standards and Avionics Protection Boosted Cabin & Cockpit Cooling Segment Growth

Based on application, the market is segmented into cabin & cockpit cooling, avionics & electronics cooling, propulsion & engine thermal management, electric power & battery thermal management, special-payload & mission cooling, and others.

In 2025, the cabin & cockpit cooling segment dominated the global market. Demand is increasing as airlines focus more on passenger comfort and stable cockpit conditions, especially on long-haul routes and in harsh operating environments. At the same time, the growing density of avionics and onboard electronics is increasing the need for reliable temperature control to protect system performance and safety.

The electric power & battery thermal management segment is projected to grow at a high CAGR of 7.31% over the forecast period.

By Aircraft Type

Fleet Expansion and Retrofit Activity to Boost Commercial Aircraft Segment Growth

Based on the aircraft type, the market is segmented into commercial aircraft, regional aircraft, business & general aviation aircraft, military aircraft, helicopters/rotorcraft, and others.

The commercial aircraft segment is anticipated to witness a dominating aircraft cooling system market share over the forecast period. Commercial aircraft is a major growth area as every new delivery requires integrated cooling capability, while the large existing fleet creates ongoing retrofit and upgrade demand. Airlines are also modernizing aircraft to improve efficiency and extend service life, which supports repeated demand for cooling system components.

The military aircraft segment is projected to grow at a high CAGR of 6.87% over the forecast period.

By Component

Thermal Load Management and Maintenance Demand Boosted Heat Exchangers & Pre-Coolers Segment Growth

Based on component, the market is segmented into heat exchangers & pre-coolers, air-cycle machines, compressors, pumps & fluid movers, cold plates & thermal interface modules, valves, sensors & controllers, refrigerant/coolant loops, reservoirs & accumulators, and others.

The heat exchangers & pre-coolers segment dominated the market share in 2025. The segment is growing as heat exchangers and pre-coolers are central to controlling thermal loads and maintaining stable performance across aircraft cooling systems. Their role also makes them recurring replacement items during maintenance, especially in high-utilization aircraft, where performance degradation can affect system efficiency.

In addition, compressors, pumps & fluid movers are projected to grow at a high CAGR of 7.31% during the study period.

By End User

To know how our report can help streamline your business, Speak to Analyst

Fleet Aging and Lifecycle Support Boosted Aftermarket/MRO/Replacement Segmental Growth

Based on end user, the market is segmented into OEM line-fit, aftermarket/MRO/replacement, and retrofit & upgrade programs.

The aftermarket/MRO/replacement segment dominated the market share in 2025. The segment is gaining momentum as operators of aging fleets depend on maintenance, repair, and replacement activities to keep cooling systems reliable. As these components are exposed to wear, contamination, and harsh operating conditions, they require periodic servicing, which sustains long-term aftermarket demand.

In addition, retrofit & upgrade programs are projected to grow at a CAGR of 7.12% during the study period.

Aircraft Cooling System Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Aircraft Cooling System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 2.41 billion, and also maintained the leading share in 2025, with USD 2.55 billion. North America remains a leading region for aircraft cooling systems due to its strong commercial and defense aircraft base and sustained aerospace R&D activity. The U.S. benefits from major OEM and tier-1 presence, including Collins Aerospace and Honeywell, which support thermal management and air management programs.

U.S. Aircraft Cooling System Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 1.67 billion in 2026, with a roughly 6.43% CAGR. The U.S. is the core market in North America, supported by large aircraft fleets, military modernization, and a deep aerospace supply chain. Ongoing research in electrified aircraft propulsion and thermal management is pushing demand for more efficient cooling architectures.

Europe

Europe is projected to record a steady growth rate of 6.60% during the forecast period, the second-highest among all regions, and to reach a valuation of USD 1.67 billion in 2026. Europe is seeing strong momentum in clean aviation programs and the development of next-generation environmental control systems. Publicly backed R&D initiatives are focusing on bleedless architectures, compact cooling systems, and lower power consumption, which support long-term demand.

U.K. Aircraft Cooling System Market

The U.K. market in 2026 is estimated at around USD 0.53 billion, with a CAGR of roughly 7.05% during the study period. The U.K. market is supported by its aerospace engineering ecosystem and participation in advanced aircraft thermal management research. Demand is linked to work on more-electric aircraft concepts, where efficient cooling and heat exchange are essential for future platform performance.

Germany Aircraft Cooling System Market

Germany’s market is projected to reach approximately USD 0.46 billion in 2026. Germany is an important European hub for aircraft cooling systems due to its manufacturing base and expertise in systems. Collins Aerospace operates major facilities in the country, including air management capabilities for cabin pressurization and ventilation, while other aerospace suppliers also support thermal and fluid-system engineering.

Asia Pacific

Asia Pacific is estimated to reach USD 1.53 billion in 2026 and secure the position of the third-largest region in the market and fastest growing during the study period. Asia Pacific is expanding as aircraft fleets grow, especially in commercial aviation, which increases demand for cabin, avionics, and engine cooling systems. The region is also investing in aerospace manufacturing and maintenance capability, creating opportunities for both OEM supply and aftermarket replacement demand.

China Aircraft Cooling System Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 0.49 billion. China is a major growth market due to its large-scale expansion of commercial aircraft and domestic aerospace ambitions. Rising aircraft deliveries and localization efforts are increasing the need for cooling components, thermal management systems, and long-term maintenance support.

India Aircraft Cooling System Market

The Indian market in 2026 is estimated at around USD 0.42 billion. India is gaining importance as airlines expand fleets and the domestic aerospace ecosystem becomes more active in manufacturing and MRO. Growth in air travel is supporting demand for aircraft cooling systems across commercial platforms, particularly in cabin and cockpit applications.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America. Latin America and the Middle East & Africa are smaller but relevant markets, with demand shaped by fleet utilization, hot-climate operation, and rising maintenance needs. Airlines in these regions often place strong emphasis on reliable cabin cooling and replacement of thermal components due to demanding operating environments. The Middle East & Africa and Latin America markets are set to reach valuations of USD 0.63 billion and USD 0.41 billion, respectively, in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Partnerships Shape Market Positioning

The aircraft cooling system market is moderately consolidated, with a mix of major aerospace players and specialized thermal management suppliers competing across OEM, defense, and aftermarket channels. Key companies in the market include Honeywell, Collins Aerospace, Liebherr Aerospace, Safran, Boeing, and others, with competition centered on system integration capability, certification, product reliability, and lifecycle support.

From a company perspective, innovation and partnerships are the most important growth levers. Many suppliers are investing in lighter, more energy-efficient cooling architectures, advanced heat exchangers, and integrated thermal management systems to support more-electric and electrified aircraft platforms. At the same time, partnerships with aircraft OEMs, MRO providers, and defense contractors help companies secure long-term programs, co-develop new technologies, and strengthen their position in retrofit and replacement markets.

LIST OF KEY AIRCRAFT COOLING SYSTEM COMPANIES PROFILED

- Collins Aerospace (S.)

- Honeywell International Inc. (U.S.)

- Liebherr (France)

- Meggitt PLC. (U.S.)

- Safran (France)

- AMETEK Aerospace & Defense (U.S.)

- Eaton (Ireland)

- Crane Aerospace & Electronics (U.S.)

- TAT Technologies Ltd. (Israel)

- Triumph Group (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Conflux Technology joined the Honeywell-led TheMa4HERA consortium (Thermal Management for Hybrid Electric Regional Aircraft). This Clean Aviation project aims to develop cutting-edge thermal management architectures and systems for next-generation hybrid-electric regional aircraft, with short- to medium-range aircraft scaling activities. Honeywell's international development center leads the collaboration in Brno, Czech Republic, and consists of 28 partners from ten European nations.

- September 2025: Conflux Technology revealed that it would assist Airbus' ZEROe project by developing an enhanced heat exchanger for hydrogen-electric propulsion systems via additive manufacturing.

- February 2025: A service agreement for the maintenance, repair, and refurbishment of Airbus A320 heat transfer equipment at MRO Middle East 2025 has been signed by Liebherr-Aerospace and GMR Aero Technic. To ensure the aircraft's performance and airworthiness, GMR Aero Technic will work with Liebherr-Aerospace to provide heat-transfer equipment service during maintenance checks.

- July 2024: Lockheed Martin launched a competition for the F-35 cooling system upgrade, with Honeywell and Collins Aerospace emerging as key contenders for the next-phase power and thermal management unit

- March 2024: Honeywell declared that it has successfully shown that it is possible to increase the F-35's Power and Thermal Management System (PTMS) cooling capability to 80kW. Honeywell currently substantially exceeds the 32kW cooling requirements of the U.S. military and its allies, thanks to its greatly improved cooling capability.

REPORT COVERAGE

The global aircraft cooling system industry analysis includes a comprehensive study of the market size & forecast across all market segments covered in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, Porter’s Five Forces analysis, company profiles, and the retrofitting program. Additionally, it details partnerships, mergers & acquisitions, as well as key aviation industry developments and prevalence by key regions. The global market report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.56% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By System Type, Application, Aircraft Type, Component, End User, and Region |

| By System Type |

|

| By Application |

|

| By Aircraft Type |

|

| By Component |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 6.54 billion in 2025 and is projected to reach USD 11.51 billion by 2034.

In 2025, the market value of North America stood at USD 2.55 billion.

The market is expected to exhibit a CAGR of 6.56% during the forecast period of 2026-2034.

By system type, the air-cycle cooling systems segment is expected to dominate the market.

Fuel efficiency mandates and emission reduction targets are driving fuel market growth.

Honeywell, Collins Aerospace, Liebherr Aerospace, and Safran are a few key players in the global market.

North America dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us