Aircraft Fire Protection System Market Size, Share & Industry Analysis, By Product Type (Fire Detection Systems, Fire Suppression/Extinguishing Systems, Control, Annunciation & Integration Kits, & Others), By Aircraft Type (Commercial Aircraft, Business Jets, Military Aircraft, & Others), By Application (Engine & APU Fire Detection, Cargo Compartment Smoke Detection, Cabin Safety Fire Protection, Avionics/Equipment Bay Detection), By End User (Aircraft OEMs (Line-Fit), Commercial Airlines & Operators, Military Operators/Defense Agencies, MRO Providers), & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

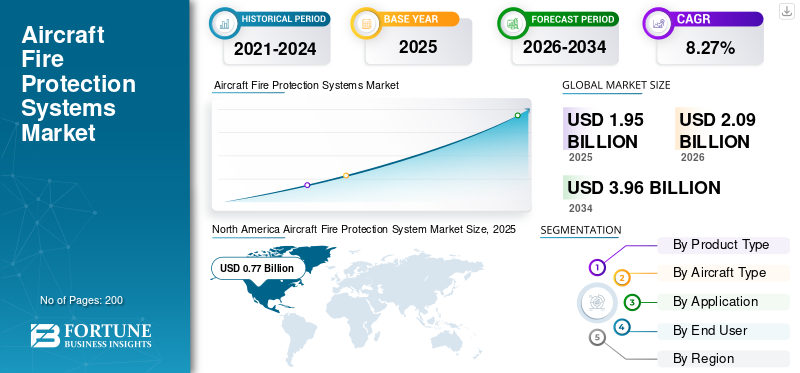

The global aircraft fire protection system market size was valued at USD 1.95 billion in 2025. The market is projected to grow from USD 2.09 billion in 2026 to USD 3.96 billion by 2034, exhibiting a CAGR of 8.27% during the forecast period. North America dominated the global aircraft fire protection system market with a market share of 39.48% in 2025.

Aircraft fire protection systems are fixed installations on multiengine aircraft designed to detect and extinguish fires in high-risk zones such as engines, cargo, and others. Key components include fire detectors (rate-of-rise, optical, smoke), control panels, extinguisher bottles with Halon or clean agents, diverter valves, nozzles, and metering devices for precise agent discharge. These systems safeguard engines, APUs, cargo compartments, lavatories, wheel wells, and avionics bays across commercial, military, and general aviation platforms.

Leading players such as Meggitt develop electronic controls for major OEMs, Diehl Aviation advances multi-sensor detectors; Honeywell innovates for lithium-ion fire detection, and H3R supplies FAA-approved Halon extinguishers.

Download Free sample to learn more about this report.

AIRCRAFT FIRE PROTECTION SYSTEM MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.95 Billion

- 2026 Market Size: USD 2.09 Billion

- 2034 Forecast Market Size: USD 3.96 Billion

- CAGR: 8.27% from 2026–2034

- North America dominated the aircraft fire protection system market with a 39.48% share in 2025.

- The fire detection systems segment accounted for the largest market share in 2025.

- The commercial aircraft segment dominated the market in 2025.

Asia Pacific

Asia Pacific is projected to reach USD 0.60 billion in 2026 and is the fastest-growing regional market.

Europe

Europe is expected to reach USD 0.53 billion in 2026, growing at a CAGR of 8.41%.

North America

North America reached USD 0.77 billion in 2025, maintaining its leading market position.

U.S.

The market is projected to reach nearly USD 0.50 billion in 2026, growing at a CAGR of 8.28%.

Japan

The market is expected to reach around USD 0.10 billion in 2026.

Read More

AIRCRAFT FIRE PROTECTION SYSTEM MARKET TRENDS

Use of AI-driven Sensors for Detection is a Market Trend

AI-driven sensors for aircraft fire detection emerge as a market trend due to their superior speed and accuracy over traditional rate of rise or smoke detectors, addressing critical needs in high-risk areas such as cargo holds, where low cabin pressure causes smoke to disperse slowly. Positioned for integration in new aircraft deliveries and retrofits, they align with lightweight, electric architecture shifts, driving adoption as airlines prioritize rapid response.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rise in Global Air Traffic Anticipated to Drive Market Growth

Rising global air traffic acts as a primary driver for the aircraft fire protection system market growth as sustained increases in passenger volumes and flight frequencies necessitate more aircraft deliveries from manufacturers such as Boeing and Airbus, each requiring certified fire detection and suppression installations in engines, cargo holds, and cabins. Emerging markets in Asia Pacific, Africa, and Latin America fuel this expansion through growing middle-class demand, low-cost carrier proliferation, and improved connectivity, compelling airlines to equip expanding fleets with reliable safety systems to meet FAA and EASA mandates.

MARKET RESTRAINTS

High Development and Certification Costs are a Market Restraint

High development and certification costs serve as a key market restraint for aircraft fire protection systems as regulators such as the FAA and EASA enforce rigorous airworthiness standards that demand exhaustive validation of detection sensors, suppression agents, and integration under extreme flight conditions, including vibration, low pressure, and temperature swings. These processes involve detailed failure mode analyses, flight demonstrations, and conformity inspections across multiple variants, often managed separately from design phases, leading to inefficiencies and prolonged timelines that escalate expenditure.

MARKET OPPORTUNITIES

Retrofitting Aging Fleet Creates New Market Opportunities

Retrofitting aging fleets presents a major market opportunity for aircraft fire protection systems as older aircraft fleets operated by airlines worldwide must upgrade to comply with evolving FAA and EASA safety regulations mandating Halon replacement with eco-friendly agents and improved detection in cargo holds and engines. These modifications enhance safety amid rising incident risks from lithium batteries in cargo, while structural adaptations allow integration of lightweight composites that boost fuel efficiency without full fleet replacements.

MARKET CHALLENGES

Supply Chain Disruptions Present a Major Market Challenge

Supply chain disruptions challenge the aircraft fire protection systems market as critical components such as specialized composites for lightweight detectors and non-Halon suppression agents face delays from geopolitical tensions, raw material shortages, and supplier qualification issues. Furthermore, the integration testing for Halon replacements in cargo aircraft holds further amplifies vulnerabilities, as limited qualified vendors struggle with aviation-grade material procurement amid global logistics strains, slowing innovation deployment despite urgent safety needs.

Segmentation Analysis

By Product Type

Regulatory Mandates to Propel Fire Detection Systems Segmental Growth

Based on the product type, the market is segmented into fire detection systems, fire suppression/extinguishing systems, control, annunciation & integration kits, and others.

The fire detection systems segment is anticipated to account for the largest market share. Regulatory mandates from FAA and EASA propel growth in the fire detection systems segment by requiring redundant smoke and heat sensors in cargo compartments, lavatories, and inaccessible areas per standard “FAR/JAR 25.854-858”, ensuring crew alerts within one minute of fire onset to enable timely suppression.

The fire suppression/extinguishing systems segment is anticipated to rise with the highest CAGR of 8.49% over the forecast period.

By Aircraft Type

Commercial Aircraft Segment Led Market Due to Large Fleet Size

Based on aircraft type, the market is segmented into commercial aircraft, business jets, military aircraft, and others.

In 2025, the commercial aircraft segment dominated the global market. This dominance of the segment is due to its massive fleet sizes operated by global airlines, requiring mandatory redundant detection and suppression.

The military aircraft segment is projected to grow at a high CAGR of 8.69% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Presence of Flight Critical Components to Boost Engine & APU Fire Detection Segment Growth

Based on the application, the market is segmented into engine & APU fire detection, cargo compartment smoke detection, cabin safety fire protection, avionics/equipment bay detection, and others.

The Engine & APU fire detection segment is anticipated to witness a dominating market share over the forecast period. One of the main factors driving the expansion of the segment is the presence of flight-critical components in the engine and Auxiliary Power Unit (APU) sections.

The cargo compartment smoke detection segment is projected to grow at a high CAGR of 8.96% over the forecast period.

By End User

Aging Aircraft Fleet Boosted MRO Providers Segment

Based on end user, the market is segmented into aircraft OEMs (line-fit), commercial airlines & operators, military operators/defense agencies, MRO providers, and others.

The MRO providers segment dominated the market share as airlines are required by aviation authorities (FAA, EASA) to retrofit older aircraft with cutting-edge equipment to comply with safety and environmental regulations, which boosts MRO business.

In addition, aircraft OEMs (line-fit) are projected to rise at a high CAGR of 8.81% during the study period.

Aircraft Fire Protection System Market Regional Outlook

By region, the market is divided into Rest of the World, Europe, Asia Pacific, and North America.

North America

North America Aircraft Fire Protection System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the leading aircraft fire protection system market share in 2024, valued at USD 0.71 billion, and reinforced its dominance in 2025 by climbing to USD 0.77 billion. This upward trajectory is primarily attributed to Boeing's high-rate manufacturing of the 737 and 787 platforms, where certified fire detection systems are increasingly embedded as standard equipment.

U.S. Aircraft Fire Protection System Market

Given North America’s strength and the U.S.’s outsized contribution, the U.S. market is estimated to reach nearly USD 0.50 billion in 2026, growing at an approximate CAGR of 8.28%. Growth momentum stems from robust MRO activity upgrading legacy aircraft with Halon alternatives and multi-sensor detection systems, complemented by defense contracts focused on UAV fire safety.

Europe

Europe is set to achieve an 8.41% CAGR during the forecast period, the second-highest globally, and reach USD 0.53 billion by 2026. Market expansion is propelled by Airbus A320neo and A350 production programs mandating EASA-approved cargo hold suppression systems, along with increasing retrofit requirements across older fleets.

U.K Aircraft Fire Protection System Market

In the U.K., the market is projected to total approximately USD 0.17 billion in 2026, advancing at a CAGR of about 8.85%. Growth is supported by Rolls-Royce’s integration of advanced APU fire sensors and defense-oriented retrofit programs spearheaded by BAE Systems.

Germany Aircraft Fire Protection System Market

Germany’s market is expected to reach a valuation of USD 0.15 billion in 2026. Growth in Germany is owing to Diehl Aviation's multi-sensor developments for Airbus platforms and Lufthansa Technik's MRO upgrades.

Asia Pacific

Asia Pacific is projected to attain a size of USD 0.60 billion by 2026, emerging as the third-largest and fastest-growing region over the study period. This momentum is fueled by aggressive fleet expansions of low-cost carriers, which are driving demand for scalable fire protection systems tailored to narrow-body aircraft amid surging air traffic.

Japan Aircraft Fire Protection System Market

In Japan, the market is expected to reach around USD 0.10 billion by 2026, contributing about 8.66% to the overall CAGR, supported by regional jet upgrades led by Mitsubishi and Kawasaki with an emphasis on lightweight composite-based fire suppression solutions.

China Aircraft Fire Protection System Market

China is poised to rank among the largest markets in Asia Pacific, with revenues forecast at nearly USD 0.20 billion in 2026, driven by COMAC C919 certification and rising domestic OEM demand for engine, APU detection, and cargo fire safety systems.

India Aircraft Fire Protection System Market

India’s market is estimated at USD 0.17 billion in 2026, propelled by IndiGo and Air India's large narrow-body aircraft orders requiring advanced line-fit fire protection systems for high-density operations.

Rest of the World

The rest of the world, including the Middle East & Africa and Latin America, is anticipated to experience steady growth, reaching USD 0.09 billion and USD 0.05 billion, respectively, in 2026, supported by Emirates and LATAM wide-body fleet expansions and safety-driven aircraft modernization initiatives.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships Fuel Aircraft Fire Protection Market Expansion

The aircraft fire protection systems market features a consolidated structure, with leading companies in the industry such as Meggitt, Honeywell, and Diehl Aviation, holding strong positions through strategic OEM collaborations. Increasing strategic partnerships drive the aircraft fire protection systems market as Meggitt teams with Boeing for electronic controls, Honeywell partners on lithium detection upgrades, and Diehl integrates sensors into Airbus platforms, enhancing supply chain reliability amid production ramps.

Furthermore, other players, including H3R Aviation, Collins Aerospace, and Kidde Technologies, target expansion via joint ventures for Halon alternatives and retrofit programs, securing aftermarket dominance.

LIST OF KEY AIRCRAFT FIRE PROTECTION SYSTEM COMPANIES PROFILED

- Meggitt PLC (U.K.)

- Honeywell International Inc. (U.S.)

- Diehl Aviation (Germany)

- H3R Aviation (U.S.)

- Collins Aerospace (U.S.)

- Kidde Technologies (U.S.)

- Aerocon Engineering (U.S.)

- Gielle Industries (Italy)

- Advanced Aircraft Extinguishers (U.K.)

- Halma plc (U.K.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: The U.K.-based inventor and producer of high-performance notification, initiation, and fire detection systems, E2S, has been bought by Halma plc.

- October 2025: Aircraft registered in Europe will no longer be permitted to carry Halon 1211 fire extinguishers after 31 December 2025, with the exception of specific cargo comparison and fuel inerting applications that employ Halon 1301. H3R Aviation has introduced a line of Halotron BRx extinguishers.

- September 2025: The U.S. Department of Agriculture (USDA) and Perimeter Solutions, a prominent global producer of premium fire retardant and firefighting foam concentrates, today announced the signing of a revolutionary five-year agreement.

- April 2025: Collins Aerospace and Satair extended their arrangement to provide cabin interior parts for an additional four years. With distribution rights for Collins' portfolio of oxygen systems, Goodrich lighting solutions, and beverage manufacturers for Airbus, the agreement continues to guarantee prompt and effective product delivery.

- February 2024: The Civil Aviation Administration of China (CAAC) accredited AMETEK Ameron, a pioneer in aviation safety equipment that offers repair and overhaul solutions for a variety of aircraft applications, for its Baldwin Park, California plant.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.27% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Aircraft Type, Application, End User, and Region |

|

By Product Type |

· Fire Detection Systems · Fire Suppression/Extinguishing Systems · Control, Annunciation & Integration Kits · Others |

|

By Aircraft Type |

· Commercial Aircraft · Business Jets · Military Aircraft · Others |

|

By Application |

· Engine & APU Fire Detection · Cargo Compartment Smoke Detection · Cabin Safety Fire Protection · Avionics/Equipment Bay Detection · Others |

|

By End User |

· Aircraft OEMs (Line-Fit) · Commercial Airlines & Operators · Military Operators/Defense Agencies · MRO Providers · Others |

|

By Region |

· North America (By Product Type, Aircraft Type, Application, End User, and Country) o U.S. (Aircraft Type) o Canada (Aircraft Type) · Europe (By Product Type, Aircraft Type, Application, End User, and Country /Sub-region) o U.K. (Aircraft Type) o Germany (Aircraft Type) o France (Aircraft Type) o Russia (Aircraft Type) o Rest of Europe (Aircraft Type) · Asia Pacific (By Product Type, Aircraft Type, Application, End User and Country/Sub-region) o China (Aircraft Type) o India (Aircraft Type) o Japan (Aircraft Type) o South Korea (Aircraft Type) o Rest of Asia Pacific (Aircraft Type) · Rest of the World (By Product Type, Aircraft Type, Application, End User and Country/Sub-region) o Middle East & Africa (Aircraft Type) o Latin America (Aircraft Type) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.95 billion in 2025 and is projected to reach USD 3.96 billion by 2034.

In 2025, the market value in North America stood at USD 0.77 billion.

The market is expected to exhibit a CAGR of 8.27% during the forecast period of 2026-2034.

By product type, the fire detection systems segment is expected to dominate the market.

Rise in global air traffic anticipated to drive market growth.

Meggitt PLC (U.K.), Honeywell International Inc. (U.S.), Diehl Aviation (Germany), H3R Aviation (U.S.), and Collins Aerospace (U.S.) are a few major players in the global market.

North America dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us