Aircraft Paint Market Size, Share & Industry Analysis by Aircraft Type (Commercial Aviation (Narrow Body and Wide Body), Regional Jets, Business Jets, Military Aviation (Fighter Jets, Military Transport Aircraft and Military Trainer Aircraft), and Helicopters (Military Helicopters and Commercial Helicopters)), By Category (Exterior Paint, Interior Paint, and Component Paint), By End-user (OEM and MRO), By Paint Type (Polyurethane Paints, Epoxy Paints, Acrylic Paints, Fluoropolymer Paints, and Others), and Regional Forecast, 2026-2034

Aircraft Paint Market Size and Future Outlook

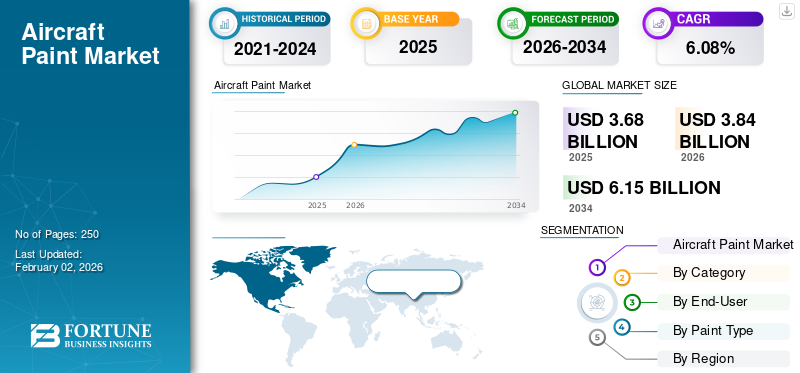

The global aircraft paint market size was valued at USD 3.68 billion in 2025. The market is projected to grow from USD 3.84 billion in 2026 to USD 6.15 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 6.08% during the forecast period. North America dominated the aircraft paint market with a market share of 32.08% in 2025.

The aviation paint sector refers to the specialized segment of the coatings industry that produces high-performance paints and finishes designed specifically for aircraft exteriors, interiors, and components. These coatings serve a dual purpose: aesthetic enhancement and functional protection. They safeguard aircraft structures from corrosion, UV radiation, extreme temperature variations, and chemical exposure, while also contributing to aerodynamics and brand identity through airline liveries. Modern aviation paints must balance durability, lightweight formulation, and environmentally friendly, adhering to strict aerospace and regulatory standards such as REACH, EPA, and SAE specifications.

The market growth is primarily driven by rising global aircraft production, expanding MRO (Maintenance, Repair & Overhaul) activities, and technological innovations in coating chemistry. As airlines increase fleet utilization and repainting cycles tighten, the demand for quick-curing, fuel-efficient, and low-VOC coatings has surged. Additionally, the rapid expansion of low-cost carriers in the Asia Pacific, coupled with defense modernization programs in the U.S., India, and the Middle East, further boosts consumption. The increasing shift toward eco-friendly, chrome-free primers and nanotechnology-based coatings reflects an industry-wide transition to sustainability and operational efficiency.

The competitive landscape is moderately consolidated, dominated by multinational coating specialists with established OEM and MRO partnerships. Key market participants include AkzoNobel N.V. (Netherlands), PPG Industries, Inc. (U.S.), and Mankiewicz Gebr. & Co. (Germany), Sherwin-Williams Aerospace (U.S.), BASF SE (Germany), and Axalta Coating Systems (U.S.). These companies lead through continuous innovation in polyurethane and fluoropolymer formulations, development of digital painting solutions such as VR-based training and visualizers, and strategic alliances with major OEMs such as Boeing and Airbus. As the aviation industry prioritizes lightweight materials, sustainability, and brand differentiation, the aircraft paint market is poised for sustained growth through 2032 and beyond.

Download Free sample to learn more about this report.

Aircraft Paints Market Key Takeaways

- 2025 Market Size: USD 3.68 Billion

- 2026 Market Size: USD 3.84 Billion

- 2034 Forecast Market Size: USD 6.15 Billion

- CAGR: 6.08% from 2026–2034

- North America dominated the aircraft paint market with a 32.08% share in 2025.

- Commercial aviation held the largest aircraft type segment with a 57.14% share in 2026.

- Exterior paint dominated the market with a 66.23% share in 2026.

North America

North America generated USD 1.18 billion in 2025, accounting for 32.08% of global market revenue.

Europe

Europe held a 27.88% market share and was valued at USD 1.03 billion in 2025.

Asia Pacific

Asia Pacific reached USD 0.94 billion in 2025, representing 25.40% of global revenue and is projected to witness the fastest growth.

U.S.

The market is projected to reach USD 0.89 billion by 2026, supported by strong OEM and MRO activities.

Japan

The market is projected to reach USD 0.18 billion by 2026, driven by fleet expansion and aviation industry growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Fleet Expansion and MRO Growth to Propel Product Demand

The strongest driver of the market is the expanding global aircraft fleet and the rapid growth of MRO (Maintenance, Repair & Overhaul) activities. As commercial aviation recovers post-pandemic, airlines are aggressively adding new aircraft and refurbishing existing fleets, increasing demand for repainting, corrosion protection, and livery updates. The rising utilization of narrow-body aircraft in high-frequency routes further accelerates repaint cycles every 5–7 years. Additionally, growing regional connectivity across Asia Pacific and the Middle East fuels repainting demand in emerging MRO hubs. The expanding business jet market also contributes, emphasizing luxury finishes and customized coatings, propelling aircraft paint market growth.

- July 2025 – Ryanair extended its aircraft painting contract with MAAS Aviation until 2035 to repaint over 500 aircraft, supporting its expanding fleet and livery standardization programs.

MARKET RESTRAINTS:

High VOC Regulations and Complex Application Processes to Limit Industry Growth

A major restraint in the aviation paint industry is the tightening of VOC (Volatile Organic Compound) and chrome-based paint regulations, which limit the use of traditional solvent-based coatings. Meeting REACH, EPA, and OSHA compliance requires extensive R&D investment and reformulation, increasing production costs. Additionally, the complex and labor-intensive paint application process, involving surface stripping, masking, and multi-layer curing, extends aircraft downtime and raises operational costs. Smaller MRO facilities often struggle to adopt eco-friendly alternatives due to high equipment upgrade costs. These factors collectively slow the market penetration of advanced coating systems in cost-sensitive regions.

- April 2025 – AkzoNobel and Airbus co-developed a low-VOC exterior coating system for the A321neo, aligning with stricter EU environmental compliance standards.

MARKET OPPORTUNITIES:

Sustainable and Lightweight Coatings to Create New Revenue Streams

The shift toward sustainable, chrome-free, and weight-optimized coatings presents a strong growth opportunity. Next-generation polyurethane and fluoropolymer systems are designed to reduce aircraft weight, enhance fuel efficiency, and extend repaint intervals. Lightweight coatings also support airlines’ decarbonization goals and lifecycle cost reduction. Emerging nanocomposite and self-healing coatings are set to redefine performance standards by minimizing surface damage and maintenance frequency. As OEMs push for greener production lines, suppliers developing low-emission and water-based coating systems will capture long-term contracts.

- May 2025 – PPG announced a USD 380 million investment in a new aerospace coatings facility in North Carolina to expand production of sustainable, high-durability aviation coatings.

AIRCRAFT PAINT MARKET TRENDS:

Digitalization and Smart Application Systems to Transform Coating Operations

Digital technologies are revolutionizing the aircraft paints industry with virtual reality (VR) training, AI-based color visualization, and robotic paint application systems. VR-assisted training reduces material waste and improves precision, while digital color visualizers allow the real-time customization of liveries for OEMs and operators. Robotic paint booths improve consistency, lower human error, and enhance efficiency for large fleet operators. These innovations help balance sustainability with production scalability. The convergence of digital tools and automation is setting a new benchmark for quality control and operational throughput in aerospace coatings.

- April 2025 – AkzoNobel and International Aerospace Coatings (IAC) launched a VR-based paint training system to standardize global MRO coating quality and reduce rework rates.

MARKET CHALLENGES:

Raw Material Shortages and Skilled Labor Gaps to Disrupt Production

The market faces recurring challenges from raw material supply constraints and a shortage of skilled applicators. Key resins, pigments, and solvents often experience price volatility, leading to extended lead times and higher costs for MRO operators. Simultaneously, the scarcity of certified painters trained for aerospace coatings—especially in Asia and the Middle East—creates operational bottlenecks. The need for precision, multi-layer application expertise, and compliance with OEM standards makes workforce training critical. These challenges risk delaying repaint schedules and reducing throughput at busy MRO hubs.

Download Free sample to learn more about this report.

Segmentation Analysis

By Aircraft Type

Commercial Aviation Led the Market as Fleet Expansion and Livery Branding Drive Repaint Demand

On the basis of aircraft type, the market is classified into commercial aviation, regional jets, business jets, military aviation, and helicopters.

The commercial aviation segment dominated the global aircraft paint market share in 2026 with 57.14%. Commercial aviation remains the largest segment in the market, accounting for over 60% of the global demand. The expanding narrow-body fleet, driven by surging short- and medium-haul air travel, results in frequent repainting cycles and large-scale liveries. Airlines are prioritizing fuel-efficient coatings and low-VOC paints to meet environmental mandates while preserving brand aesthetics. The growth in low-cost carriers and high aircraft utilization further sustains repaint demand.

- July 2025 – PPG Aerospace signed a multi-year contract with Ryanair to supply eco-efficient exterior coatings for its Boeing 737-8200 fleet.

The regional jets segment is anticipated to expand at a CAGR of 6.12% over the forecast period.

By Category

Exterior Paints Dominate Due to Larger Surface Coverage and High Performance Requirements

On the basis of category, the market is classified into exterior paint, interior paint, and component paint.

The exterior paint segment accounted for a dominating market share of 66.23% in 2026. Exterior paints account for the majority of aviation paint consumption, supported by vast surface areas and stringent performance needs against UV, temperature, and chemical exposure. This segment benefits from both OEM and MRO demand, as airlines frequently update liveries and ensure aerodynamic efficiency through smooth coating finishes. Advances in polyurethane and fluoropolymer technologies are extending repaint intervals, improving lifecycle economics.

- May 2025 – AkzoNobel introduced its Aerobase NextGen exterior coating for the Airbus A350 series, reducing paint weight by 15% and improving durability.

The interior paint segment is estimated to grow at a CAGR of 5.38% over the forecast period.

By End-user

MRO Segment Dominates as Fleet Maintenance and Livery Renewal Fuel Recurring Demand

On the basis of end-user, the market is classified into OEM and MRO.

The MRO segment accounted for a dominating market share in 2024. The MRO segment leads the market, accounting for approximately two-thirds of total revenue. Regular repainting cycles every 5–7 years, driven by corrosion control and airline rebranding, ensure consistent aftermarket demand. The rise of independent MRO hubs in Asia Pacific and the Middle East is expanding capacity for paint and livery services. Meanwhile, eco-friendly repaint processes are becoming a competitive differentiator.

- April 2025 – Lufthansa Technik inaugurated a new wide-body paint hangar in Malta dedicated to sustainable aircraft repainting and MRO services.

The OEM segment is anticipated to expand at a CAGR of 5.38% over the analysis period, & Dominated with a share 24.18% in 2026

By Paint Type

Polyurethane Paints Dominate Owing to Superior Durability and Gloss Retention

Based on paint type, the market is segmented into polyurethane paints, epoxy paints, acrylic paints, fluoropolymer paints, and others.

The polyurethane paints segment held the dominating position in 2026 with 48.06% share. Polyurethane paints lead the market with around 45–50% share, driven by their excellent weather resistance, chemical stability, and aesthetic finish. They are the preferred topcoat for commercial, business, and military aircraft, providing extended service life and low maintenance. Innovations in lightweight, chrome-free, and low-VOC polyurethane systems are strengthening adoption across OEM and MRO operations worldwide.

- June 2025 – AkzoNobel Aerospace Coatings launched a new polyurethane-based system for the Airbus A320neo family, offering improved fuel efficiency through weight reduction.

The fluoropolymer paints segment is poised to expand at the fastest CAGR of 6.83% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

Aircraft Paint Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

The North American market was valued at USD 1.18 billion in 2025, capturing 32.08% of global revenue, and is estimated to reach USD 1.23 billion in 2026. The dominance is driven by a strong OEM presence (Boeing, Lockheed Martin, and Gulfstream) and extensive MRO networks. The U.S. leads aircraft deliveries and fleet repaint activities, supported by defense modernization programs and commercial fleet renewal. The adoption of eco-efficient and chrome-free coatings is increasing across the region as sustainability standards rise. The integration of advanced fluoropolymer and polyurethane systems continues to shape demand. The U.S. market is projected to reach USD 0.89 billion by 2026.

- February 2025 – PPG Aerospace expanded its aerospace coatings facility in Georgia, U.S., to support contracts with Boeing and the U.S. Air Force.

Europe

In 2025, Europe held 27.88% of the global market, reaching a valuation of USD 1.03 billion, and is projected to grow to USD 1.06 billion in 2026. Europe’s market is witnessing strong growth driven by joint defense projects, border monitoring initiatives, and the modernization of existing fleets. Europe remains a key aviation paint hub, supported by Airbus manufacturing in France and Germany, as well as major coating producers such as AkzoNobel, Mankiewicz, and BASF. The region’s strict VOC and REACH regulations are accelerating the shift toward water-based and chrome-free systems. European MRO centers especially in Germany, the U.K., and Italy are pioneering sustainable paint application processes. The rising adoption of fluoropolymer coatings in wide-body aircraft production further supports long-term growth. The UK market is projected to reach USD 0.29 billion by 2026, while the Germany market is projected to reach USD 0.25 billion by 2026.

Asia Pacific

The market in Asia Pacific reached USD 0.94 billion in 2025, representing 25.40% of total market revenue, and is projected to reach USD 0.98 billion in 2026. The Asia Pacific region experiences rapid growth and is expected to grow at the highest CAGR over 2025-2032. The fastest growth of the region is fueled by massive fleet expansion across China, India, Japan, and Southeast Asia. Rising middle-class travel, low-cost carrier proliferation, and regional connectivity are driving record aircraft deliveries. The rapid development of MRO hubs in Singapore, India, and China is boosting the demand for high-performance and quick-curing coatings. Local production by companies such as Nippon Paint and Kansai Paint is improving cost competitiveness and regional supply resilience.

Rest of the World

In 2025, Rest of the World generated USD 0.54 billion, contributing 14.64% to global market revenue, and is projected to grow to USD 0.55 billion in 2026. Over the forecast period, Latin America & Africa and the Middle East regions would grow at a CAGR of 4.2% over the forecast period. The Middle East & Africa market is driven by fleet repainting programs from major airlines such as Emirates, Qatar Airways, and Saudia, alongside defense aircraft modernization in the UAE and Saudi Arabia. The region’s harsh climate demands UV- and heat-resistant coatings with extended durability. Latin America’s market is growing steadily, supported by the modernization of regional and narrow-body fleets across Brazil, Mexico, and Colombia. Embraer’s strong presence drives local OEM paint demand, while expanding MRO hubs in Brazil and Panama create new repainting opportunities. The Japan market is projected to reach USD 0.18 billion by 2026, the China market is projected to reach USD 0.27 billion by 2026, and the India market is projected to reach USD 0.23 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Companies Deploy Strategic Partnerships and Sustainable Innovations to Secure a Competitive Edge

The aircraft paint market is moderately consolidated, led by key global players such as AkzoNobel N.V., PPG Industries, and Mankiewicz Gebr. & Co., Sherwin-Williams, BASF SE, Axalta Coating Systems, and Hentzen Coatings. These companies dominate through extensive OEM partnerships, global MRO networks, and specialized product portfolios catering to both commercial and defense aircraft. Competition centers on low-VOC, chrome-free, and weight-reducing formulations as sustainability and fuel efficiency become key differentiators. Continuous innovation in polyurethane and fluoropolymer coatings and expansion in Asia Pacific and Middle Eastern MRO hubs are reshaping market leadership scenario.

- May 2025 – PPG Industries partnered with Boeing to develop advanced sustainable aerospace coatings under its Desothane line, aimed at reducing lifecycle emissions and improving coating durability.

LIST OF KEY AIRCRAFT PAINT COMPANIES PROFILED:

- AkzoNobel N.V. (Netherlands)

- PPG Industries, Inc. (U.S.)

- Mankiewicz Gebr. & Co. (Germany)

- Sherwin-Williams Aerospace Coatings (U.S.)

- BASF SE (Germany)

- Axalta Coating Systems (U.S.)

- Hentzen Coatings, Inc. (U.S.)

- Nippon Paint Holdings Co., Ltd. (Japan)

- Kansai Paint Co., Ltd. (Japan)

- Henkel AG & Co. KGaA (Germany)

KEY INDUSTRY DEVELOPMENTS:

- July 2025 – Ryanair extended its long-term paint agreement with MAAS Aviation until 2035, covering the repainting of over 500 aircraft. The deal ensures livery consistency across its growing fleet and supports sustainable paint operations in Europe, reinforcing MAAS’s leadership in aircraft repainting services.

- July 2025 – AkzoNobel partnered with LandLocked Aviation Services to deliver advanced coatings for the U.S. Navy’s P-8 Poseidon fleet, enhancing corrosion resistance and lifecycle performance. The partnership broadens AkzoNobel’s defense portfolio and supports Boeing’s military aircraft maintenance operations.

- June 2025 – AkzoNobel and IFI Coatings entered a licensing partnership for the Alumigrip 4250 topcoat system, allowing broader distribution of aerospace-qualified coatings for general aviation and helicopter OEMs. This collaboration improves market reach and accelerates delivery timelines in regional manufacturing hubs.

- June 2025 – International Aerospace Coatings (IAC) secured over USD 240 million in investment-grade financing for global expansion. The funds will be used to build new hangars and boost painting capacity in the U.S. and Europe to meet growing demand for aircraft repainting services. The financing reflects the rising importance of aircraft paint operations in MRO and brand management strategies for airlines.

- May 2025 – PPG invested USD 380 million to build a new aerospace coatings and sealants facility in Shelby, North Carolina, aimed at expanding production capacity and shortening lead times for OEM and MRO customers. The investment is expected to strengthen PPG’s position in the global aerospace coatings supply chain.

- April 2025 – AkzoNobel and International Aerospace Coatings (IAC) launched a virtual reality (VR) paint training program, enabling technicians to practice paint application digitally. The initiative aims to reduce waste, improve coating consistency, and standardize training across global MRO facilities.

- March 2025 – Sherwin-Williams expanded its Aircraft Color Visualizer platform, adding four new aircraft models to enable OEMs and operators to preview custom liveries in real time. The upgrade enhances customer engagement and shortens design-to-approval cycles for business jet and airline clients.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.08% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Aircraft Type

By Category

By End-User

By Paint Type

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.68 billion in 2025 and is projected to reach USD 6.15 billion by 2034.

In 2025, the North American market value stood at USD 1.18 billion.

The market is expected to exhibit a CAGR of 6.08% during the forecast period of 2026-2034.

In 2024, the polyurethane paints segment led the market by paint type.

The rising fleet expansion and MRO growth are key factors propelling industry expansion.

PPG Industries, Inc. (U.S.) and Nippon Paint Holdings Co., Ltd. (Japan) are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us