Aircraft Seat Actuation Systems Market Size, Share & Industry Analysis, By End User (OEM Line-fit, and Retrofit/Aftermarket), By Airport Type (Narrowbody Aircraft, Widebody Aircraft, Regional Transport Aircraft, and Helicopters), By Mechanism (Linear, Rotary, and Hybrid (Dual-Motion)), By Seat Class (First, Business, Premium-Economy, and Economy), By Component (Actuator Motor, Gearbox and Screw Assembly, Control Electronics (PCU), and Harness and Sensors) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

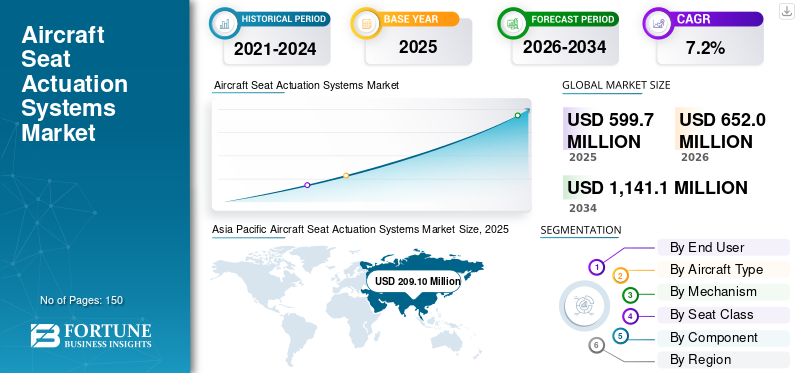

The global aircraft seat actuation systems market size was valued at USD 599.7 million in 2025. The market is projected to grow from USD 652.0 million in 2026 to USD 1,141.1 million by 2034, exhibiting a CAGR of 7.2% during the forecast period. Asia Pacific dominated the global market with a market share of 34.86% in 2025.

Aircraft seat actuation systems are the mechanical, hydraulic, or electromechanical assemblies that move and lock aircraft seat components such as recline, legrest, lumbar support, height, and track position using motors, gearboxes, linkages, valves, sensors, and controllers. They deliver smooth, safe adjustment, meet crashworthiness requirements, and integrate with cabin power and crew/passenger controls. The aircraft seat actuation systems market supports powered seat functions such as recline, legrest, lumbar and seat-pan adjustments across commercial aircraft and helicopters. Demand is shaped by new aircraft deliveries (line-fit), high fleet utilization that accelerates replacements and ongoing cabin refresh programs that improve passenger experience. Narrowbody fleets dominate volume, while premium cabins and premium-economy drive higher actuation content per seat. Technology is moving toward lighter and quieter electromechanical designs with smarter control electronics, sensors and diagnostics to cut maintenance time and reduce in-service failures. Retrofit momentum and spares demand keep the market resilient even when delivery schedules fluctuate.

Key players such as Safran, RTX, Moog, Honeywell, Astronics, ITT, Crane, Bühler Motor, NOOK Industries, and Rollon boost growth through reliable electromechanical designs, scalable manufacturing, faster spares support, and integration-ready actuation modules.

Download Free sample to learn more about this report.

AIRCRAFT SEAT ACTUATION SYSTEMS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 599.7 million

- 2026 Market Size: USD 652.0 million

- 2034 Forecast Market Size: USD 1,141.1 million

- CAGR: 7.20% from 2026–2034

- Asia Pacific dominated the global market with a market share of 34.86% in 2025.

- The retrofit/aftermarket segment is anticipated to rise with a CAGR of 8.1% over the forecast period.

- The regional transport aircraft segment is projected to grow at a CAGR of 7.0% over the forecast period.

North America

In 2025, the North America market value stood at USD 176.8 million is estimated to reach USD 192.4 million in 2026.

Europe

Europe is projected to record a growth rate during the forecast period of 7.0%

Asia Pacific

Asia Pacific held the dominant share in 2024, valuing at USD 193.7 million, and also maintained the leading share in 2025, with USD 209.1 million.

U.S.

The U.S. market can be analytically approximated at around USD 168.1 million in 2026, accounting for a CAGR of 7.1%.

Japan

The Japan market share in 2026 is estimated at around USD 36.3 million, accounting for roughly 7.0% of CAGR during the forecast period.

Read More

AIRCRAFT SEAT ACTUATION SYSTEMS MARKET TRENDS

Electrification and Smarter Seats is an Emerging Market Trend

Aircraft seat actuation is shifting from simple motion hardware to integrated, electronics-heavy systems. OEMs are standardizing powered functions beyond premium cabins, while airlines push modular seat architectures that are easier to upgrade. Hybrid motion designs, quieter gear trains and better sensing are gaining attention as they improve feel and reduce nuisance failures. Control electronics are becoming more software-driven, enabling diagnostics, faster troubleshooting and condition-based maintenance. At the same time, suppliers are designing lighter, more power-efficient actuators to help airlines balance passenger comfort with fuel-burn pressure and stricter performance targets.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Passenger Experience Expectations and Fleet Expansion are Core Market Driver

The main driver for aircraft seat actuation systems market growth are airlines want better passenger experience while flying more people. Fleet growth especially narrow body adds seat shipsets, while higher utilization increases replacement demand. Airlines also compete on comfort and differentiation, pushing powered recline, leg rests, and adjustability into more seat models. On the OEM side, line-fit adoption increases as factory installation reduces downtime and ensures certification is cleaner. As carriers run tighter schedules, they value actuation systems that are reliable, quick to service and supported by strong spares availability.

MARKET RESTRAINTS

Certification Burden, Cost and Power Constraints are the Key Market Restraints

Seat actuation adoption is restrained by certification timelines, integration complexity and the cost sensitivity of high-volume cabins. Airlines scrutinize weight, power draw and maintainability especially in economy as every added component can impact fuel burn and dispatch reliability. Program delays also occurs, thus in-flight entertainment and cabin management systems must be validated together. Supply chain volatility in motors, electronics, and precision mechanical parts can force longer lead times and higher prices, making airlines defer upgrades or choose simpler manual solutions.

MARKET OPPORTUNITIES

Cabin Refresh Cycles and Premium-Economy Growth Create a Long Aftermarket Runway Market Opportunity

A major opportunity for the market lies in retrofit and spares as large installed fleets will demand replacement motors, gear assemblies and control units as utilization remains high. Premium-economy expansion is also pulling more powered features into mid-cabin, increasing content per aircraft without relying only on wide bodies. Another opportunity is “plug-and-play” retrofit kits that shorten modification time and reduce certification complexity. Suppliers that offer fast lead-times, interchangeable modules and digital troubleshooting tools can win recurring revenue through MRO networks, leasing transitions and airline-led cabin branding programs.

MARKET CHALLENGES

Reliability Under High-Cycle Use and Supply Continuity are Major Market Challenges

The biggest challenge is delivering consistent reliability in a harsh, high-cycle operating environment. Seat actuators face repetitive loads, spills, passenger misuse and constant vibration small design weaknesses can turn into large warranty and AOG costs. Another challenge is maintaining supply continuity across motors, gear machining, electronics and sensors while meeting aviation-grade traceability and quality standards. Additionally, interoperability is another difficulty with each seat platform having unique packaging and interfaces, so scaling “standard” modules without sacrificing performance takes strong engineering, testing capacity, and disciplined configuration control is challenging.

Segmentation Analysis

By End User

More New Aircraft Deliveries Drives OEM Line-fit Segment Growth

Based on the End User, the market is segmented into OEM Line-fit and Retrofit/Aftermarket.

The OEM line-fit segment is anticipated to account for the largest aircraft seat actuation systems market share. OEM line-fit demand rises as airlines accept new aircraft with factory-integrated powered seating, avoiding retrofit downtime. Line-fit systems simplify certification, improve reliability, and standardize spares and maintenance across growing fleets.

The retrofit/aftermarket segment is anticipated to rise with a CAGR of 8.1% over the forecast period.

By Aircraft Type

Higher Utilization and Densification Leads to Stronger Narrowbody Demand

Based on aircraft type, the market is segmented into narrowbody aircraft, widebody aircraft, regional transport aircraft and helicopters.

In 2025, the narrowbody aircraft segment dominated the global market. Narrowbody demand leads as these fleets fly the most cycles and expand fastest. Heavy daily utilization increases wear, pushing airlines to adopt durable actuation that reduces failures and supports tighter seat layouts.

The regional transport aircraft segment is projected to grow at a CAGR of 7.0% over the forecast period.

By Mechanism

Demand for Simple, Reliable Motion Leads to Linear Mechanism Segment Growth

Based on the mechanism, the market is segmented into linear, rotary, and hybrid (dual-motion).

The linear segment is anticipated to witness a dominating market share over the forecast period. Linear mechanisms stay in demand due to compact fit, predictable stroke control and proven durability for recline and legrest functions. They are easier to integrate, certify, troubleshoot, and replace at scale.

The hybrid (dual-motion) segment is projected to grow at a high CAGR of 7.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Seat Class

Owing to Biggest Installed Seat Base, Economy Segment Dominates Market

Based on sear class, the market is segmented into first, business, premium-economy, and economy.

The economy led segment dominated the market share. Economy demand dominates as it accounts for most seats worldwide. Airlines focus on cost-efficient and high-cycle components that can withstand frequent use while enabling incremental comfort upgrades without major weight penalties.

In addition, business segment is projected to grow at a CAGR of 7.6% during the study period.

By Component

Higher Demand for Load-Bearing Precision Requirements Leads to Gearbox & Screw Assembly Segment Growth

Based on component, the market is segmented into actuator motor, gearbox and screw assembly, Control Electronics (PCU) and harness and sensors.

The gearbox and screw assembly segment dominated the segmental market share. Gearbox and screw assemblies are growing as they convert motor torque into smooth and controlled seat movement under passenger loads. Robust designs reduce backlash, noise and maintenance, improving service life.

In addition, Control Electronics (PCU) are projected to grow at a CAGR of 7.7% during the study period.

Aircraft Seat Actuation Systems Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific and Rest of the World.

North America

Asia Pacific Aircraft Seat Actuation Systems Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the North America market value stood at USD 176.8 million is estimated to reach USD 192.4 million in 2026 and secure the position of the second-largest region in the market. The demand is driven by strong OEM integration, premium cabin upgrades and a deep MRO/retrofit ecosystem. Airlines and suppliers prioritize reliable actuation, spares availability and certification-ready solutions for fast cabin refresh cycles.

U.S Aircraft Seat Actuation Systems Market

Based on North America’s strong contribution, the U.S. market can be analytically approximated at around USD 168.1 million in 2026, accounting for a CAGR of 7.1%. Demand is high due to large installed fleets, frequent cabin refresh cycles and strong supplier presence. Airlines push reliability and turnaround speed, sustaining both OEM line-fit content and steady aftermarket replacements.

Europe

Europe is projected to record a growth rate during the forecast period of 7.0%, which is the third highest among all regions, and reach a valuation of USD 169.9 million by 2026. Demand is supported by major aircraft and tier supply chains, strict certification discipline and widebody/premium seating content. Airlines increasingly retrofit for passenger experience, while suppliers push lightweight, efficient, low-noise electromechanical actuation.

U.K Aircraft Seat Actuation Systems Market

The U.K. market in 2026 is estimated at around USD 26.9 million, representing roughly 7.3% CAGR. This growing demand is linked to seat and systems engineering capability and premium-heavy long-haul operations. Airlines prioritize passenger experience upgrades, while suppliers support certification, integration and retrofit kits aligned to fleet plans.

Germany Aircraft Seat Actuation Systems Market

Germany’s market is projected to reach approximately USD 39.8 million in 2026. This is due to strong aerospace manufacturing, tier integration and focus on quality and compliance. Airlines and suppliers prefer robust, low-maintenance actuators and electronics that reduce downtime and simplify supportability.

Asia Pacific

Asia Pacific held the dominant share in 2024, valuing at USD 193.7 million, and also maintained the leading share in 2025, with USD 209.1 million. This could be due to fleet growth, rising passenger volumes, and aggressive narrow body induction. Additionally, carriers invest in densification, premium-economy rollout, and reliability improvements, lifting both line-fit volumes and retrofit activity.

Japan Aircraft Seat Actuation Systems Market

The Japan market share in 2026 is estimated at around USD 36.3 million, accounting for roughly 7.0% of CAGR during the forecast period. The demand is stable and quality-led, driven by reliability expectations and structured maintenance planning. Airlines adopt proven actuation architectures and upgrade programs that improve seat comfort, reduce failures and simplify long-term support.

China Aircraft Seat Actuation Systems Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 77.0 million. The product demand rises with rapid fleet additions and expanding domestic networks. Narrow body deliveries, densification, and growing premium-economy adoption boost seat actuation content while local support capacity strengthens aftermarket pull.

India Aircraft Seat Actuation Systems Market

The India’s market in 2026 is estimated at around USD 41.8 million. This growth is due to fast capacity expansion, high utilization and heavy narrowbody ordering. Airlines need durable, quick-service actuation systems to minimize AOG risk and support frequent cabin reconfigurations.

Rest of the World

The rest of the world include Middle East & Africa and Latin America. These regions are expected to witness moderate growth in this market space during the forecast period. The Middle East & Africa and Latin America market is set to reach a valuation of USD 35.4 million and USD 26.0 million in 2026. This is due to fleet renewal, connectivity-led cabin upgrades, and expanding regional travel. Middle East carriers emphasize premium seating performance, while Latin America focuses on cost-effective retrofits and maintenance-friendly actuation packages.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Accelerate Aircraft Seat Actuation Adoption through Innovation and Retrofit Momentum

Key players such as Astronics, Bühler Motor, Crane, Moog, ITT Inc., RTX, Honeywell, NOOK Industries, Rollon, and Safran are pushing aircraft seat actuation growth by improving reliability, lowering weight and increasing seat-feature adoption across cabins. Their focus on compact motors, efficient gear-and-screw assemblies, smarter control electronics (PCUs), and robust sensors/harnessing helps airlines reduce maintenance events and improve passenger experience.

OEM programs benefit from their qualification depth and production scalability, while the aftermarket gains from faster spares availability and retrofit-ready kits. Partnerships, platform line-fit wins, and continued motion-control innovation are expanding penetration, especially in narrowbody and premium-economy seating.

LIST OF KEY AIRCRAFT SEAT ACTUATION SYSTEMS COMPANIES PROFILED

- Astronics Corporation (U.S.)

- Bühler Motor GmbH (Germany)

- Crane Company (U.S.)

- Moog Inc. (U.S.)

- ITT INC. (U.S.)

- RTX (U.S.)

- Honeywell International Inc. (U.S.)

- NOOK Industries, INC. (U.S.)

- Rollon S.p.A. (Italy)

- SAFRAN (France)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Safran finalized its purchase of Collins Aerospace’s flight control and actuation operations systems used across commercial and military aircraft and helicopters strengthening Safran’s position in high-value actuation.

- April 2025: Collins Aerospace launched new aftermarket seating upgrades aimed at improving the passenger experience, built around its Pinnacle main-cabin seat offering.

- March 2025: ITT’s Enidine and Compact businesses highlighted motion-control solutions and an updated product customization software capability, emphasizing reliability and faster configuration for customers.

- December 2024: Woodward announced that it has entered into a definitive agreement to buy Safran Electronics & Defense’s electromechanical actuation business across the U.S., Mexico, and Canada, expanding Woodward’s aerospace/industrial control portfolio.

- August 2022: Marsh Brothers Aviation landed a four-year supply agreement with Aviation Fabricators (AvFab) to provide seat actuator valves, after supporting AvFab in fixing a supply chain disruption.

REPORT COVERAGE

The aircraft seat actuation systems market report provides a detailed view of market size and forecasts across all segments covered in the report. It explains the key forces shaping demand, including market drivers, restraints, opportunities, and the trends expected to influence growth through the forecast period. In addition, it includes porters five forces analysis to assess competitive pressure and supplier/customer leverage, along with a structured review of retrofit and cabin-upgrade programs influencing aftermarket demand. The report tracks major competitive moves such as partnerships, strategic agreements, mergers and acquisitions, and other industry developments, and compares market presence across major regions. Finally, it presents a clear competitive landscape with estimated market shares and profiles of leading companies operating in the sector.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.2% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By End User, By Aircraft Type, By Mechanism, By Seat Class, By Component, and Region |

|

By End User |

· OEM Line-fit · Retrofit/Aftermarket |

|

By Aircraft Type |

· Narrowbody Aircraft · Widebody Aircraft · Regional Transport Aircraft · Helicopters |

|

By Mechanism |

· Linear · Rotary · Hybrid (Dual-Motion) |

|

By Seat Class |

· First · Business · Premium-Economy · Economy |

|

By Component |

· Actuator Motor · Gearbox and Screw Assembly · Control Electronics (PCU) · Harness and Sensors |

|

By Region |

· North America (End User, Aircraft Type, Mechanism, Seat Class, Component, and Country) o U.S. (End User) o Canada (End User) · Europe (By End User, Aircraft Type, Mechanism, Seat Class, Component, and Country/Sub-region) o U.K. (End User) o Germany (End User) o France (End User) o Russia (End User) o Rest of Europe (End User) · Asia Pacific (By End User, Aircraft Type, Mechanism, Seat Class, Component, and Country/Sub-region) o China (End User) o India (End User) o Japan (End User) o Rest of Asia Pacific (End User) · Rest of the World (By End User, Aircraft Type, Mechanism, Seat Class, Component, and Country/Sub-region) o Middle East & Africa (End User) o Latin America (End User) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 599.7 million in 2025 and is projected to reach USD 1,141.1 million by 2034.

In 2025, the market value stood at USD 176.8 million.

The market is expected to exhibit a CAGR of 7.2% during the forecast period of 2026-2034.

The linear segment is expected to dominate the market.

Rising Passenger Experience Expectations and Fleet Expansion are the Core Market Driver

Astronics Corporation, Bühler Motor GmbH, Crane Company, Moog Inc., ITT INC., RTX are few major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us