Aircraft Seating Market Size, Share & Industry Analysis, By Aircraft Type (Commercial, Business Jets, Regional Aircraft, and Transport Aircraft), By Class (Economy Class, Premium Economy Class, Business Class, and First Class), By Seat Type (9G Seats, 16G Seats, and 21G Seats), By Component (Structure, Foams, Actuators, Electrical Fittings, and Others), By End-use (OEM and Aftermarket), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

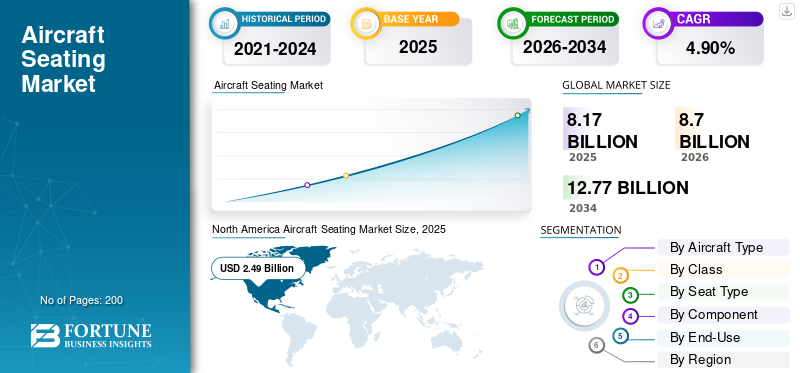

The global aircraft seating market size was valued at USD 8.17 billion in 2025. The market is projected to grow from USD 8.70 billion in 2026 to USD 12.77 billion by 2034, exhibiting a CAGR of 4.90% during the forecast period. North America dominated the aircraft seating market, with a 30.50% market share in 2025.

Aircraft seats are chairs on a commercial or military aircraft where passengers and crew are accommodated for the duration of the journey. These are usually arranged in rows, thereby ensuring passenger safety and comfort with hassle-free travel experience. Aircraft seats include components such as a structure, foam, actuators, and electrical fittings. Aircraft seating contributes considerably to the weight of aircraft interiors or aircraft. To save fuel costs and make the aircraft sustainable, lightweight designs and lightweight non-metallic materials are used to manufacture modern generation aircraft seats.

Download Free sample to learn more about this report.

Seat materials, such as seat covers and foams, are made of various materials, including nylon, synthetic leathers, silicon, polyethylene, and fireproof fabric. These materials play an important role in improving the quality of aircraft seats and life expectancy. Passenger safety, comfort, and life are largely determined by the design of the aircraft seats. The aircraft's seat is determined to be extremely secure if it pulls on high shock and stays in place during external impact. The advanced 16G and 21G seat models have high shock absorbers and an innovative design, so it offers extra safety and comfort to the passenger.

The rise in aircraft deliveries of new commercial passenger aircraft has positively driven the growth of the market in the base year. In 2021, the two major players in the aircraft manufacturing industry, Airbus and Boeing, delivered around 950 new commercial and transport aircraft and received bulk orders from major airline operators. For instance, in July 2021, United Airlines announced that it placed a 270-plane order of Boeing 737 Max and Airbus A320s to replace its older mainline aircraft. The new fleet will be 11% more energy-efficient, and the airline has taken passenger comfort as primary importance. Thus, considering the above factors, high growth numbers are anticipated during the forecast period.

The COVID-19 pandemic profoundly impacted the aviation industry and impacted the market significantly between 2020 and 2022. The global lockdown temporarily halted various activities in the aviation industry, including aircraft manufacturing, supply of raw materials, and distribution chain. These factors had a negative impact on the supply chain, leading to delays in aircraft deliveries and a pile of backlogs for key players involved in the market.

For instance, Boeing's order backlog for the MAX is 3,352 airplanes. Airbus' order backlog for the rival A320neo family is 5,765 airplanes, including 3,323 orders for the A321neo model alone. Moreover, in 2021 Boeing recorded 909 new orders for aircraft worldwide. This number is double the 2020 and 2019 orders, reaching 184 and 246, respectively.

Download Free sample to learn more about this report.

GLOBAL AIRCRAFT SEATING MARKET OVERVIEW

Market Size & Forecast

- 2025 Market Size: USD 8.17 billion

- 2026 Market Size: USD 8.70 billion

- 2034 Forecast Market Size: USD 12.77 billion

- CAGR: 4.90% from 2026–2034

Market Share

- North America led the market with a 30.50% share in 2025, driven by strong presence of aircraft OEMs and aftermarket providers.

- The commercial aircraft segment dominated by aircraft type due to increased fleet expansions and demand for modern, efficient seating.

- By seat type, 16G seats are expected to grow at the highest pace due to regulatory mandates and increased safety awareness.

Key Country Highlights

- United States: Driven by strong OEM presence and large airline fleet demand for both economy and premium cabin refits.

- India: Rising air traffic and need for 1,750 new aircraft by 2042 drive strong seat demand, especially for budget carriers.

- China: Leads in aircraft production scale in Asia-Pacific, emphasizing comfort upgrades and lightweight seat integration.

- Germany: Recaro expands seat installations for global carriers including Air India, with over 22,000 seats to be delivered.

- Italy: Geven focuses on ultra-lightweight designs like SuperEco seats for high-density aircraft configurations.

- UK: Home to Thompson Aero and Mirus Aircraft Seating, both advancing innovations in premium and sustainable seat designs.

- Japan: JAMCO Corporation continues to supply high-quality business class seats to major airlines in Asia.

Aircraft Seating Market Trends

Adoption of Lightweight Material for Aircraft Seats Manufacturing to Propel Market Growth

The escalating demand for premium economy class passengers has resulted in a greater demand for the construction of a more sophisticated seating arrangement that offers a more extensive area compared to economy-class seats. An increasing number of features will add additional weight to the aircraft. Hence, the manufacturers of aircraft seats have been focusing on enhancing their seats' lightweight characteristics while preserving their strength, integrity, and comfort. New lightweight nonmetallic materials play a major role in reducing aircraft's overall weight. Lighter aircraft seats can help reduce aircraft weight, fuel burn, and CO2 emissions. With the objective of achieving zero-emission 2050, airlines operators and OEMs worldwide are intensifying their efforts to reduce weight and devise a sustainable approach to manage the aviation industry. North America witnessed aircraft seating market growth from USD 1.96 Billion in 2022 to USD 2.12 Billion in 2023.

For instance, in March 2022, Mirus Aircraft Seating officially launched its latest derivative of the Hawk Economy Class seat that is light in sustainable weight properties. The seat is equipped with mechanical recline system and extending tray table. Moreover, the seats include sustainable seat cover materials, USB charging points for passenger convenience, and a built-in personal electronic device holder.

Aircraft Seating Market Growth Factors

Rising Passenger Air Traffic to Drive Market Growth

The escalating passenger air traffic in various regions globally is a significant factor driving the demand for airline service providers and aircraft manufacturers. Over the past decade, air travel has been proven to be the safest mode of transport, which has helped airline operators diversify their routes and destinations. There is a growing demand for new generation aircraft seats that are comfortable and safe.

Airline operators from all over the world are placing more orders for modern generation aircraft that are more efficient and provide a comfortable experience for passengers in terms of seating and cabin comfort. Moreover, the growing trend of budget airlines or low-cost carriers is one of the major contributors to placing bulk orders of aircraft. For instance, according to Airbus, India will require 1,750 new passengers and cargo aircraft over the next 20 years to meet an exponential rise in passenger and freight traffic.

Growing Adoption of IFEC Systems Integrated with Seats to Propel Market Growth

In-Flight Entertainment and Connectivity (IFEC) has been an important component of this and has assumed an increasingly important role in recent times in defining a passenger’s overall flight experience. Seat manufacturers focus on providing passengers with a comfortable, safe, and enjoyable environment. The growing adoption of seats provided by technology-based comfort and advanced features will boost the market growth in the near future. In addition, the premier airline operators are very strict about choosing the aircraft cabin interior as it creates a huge impact on passenger safety and travel experience. Moreover, the aviation industry has recognized IFE as one of the most important factors to select passengers while booking a flight ticket with a particular airline. Therefore, the abovementioned factors are expected to incite the aircraft seating market growth.

RESTRAINING FACTORS

High Cost of Parts and Components to Limit Market Growth

Cost is one of the major factors to consider while buying or manufacturing aircraft seats and related parts and components. Airlines from all over the world are looking for some pocket-friendly solutions related to aircraft seating, but the ongoing pandemic and war situation have severely disrupted supply and distribution chains. In the initial stage, the aircraft seats manufactured for premium, business class, and first-class use have a high cost that varies from manufacturer to manufacturer and cannot be compared as the seats have different features for passenger safety and comfort. For instance, business-class and first-class seats are more expensive, starting at around USD 60,000 and reaching USD 150,000. Therefore, airlines are switching to the low-cost carriers concept. Therefore, the above factors are some major reasons limiting the market growth during the forecast period.

Aircraft Seating Market Segmentation Analysis

By Aircraft Type Analysis

Increase in Airline Fleet to Boost Commercial Aircraft Type Segment in Base Year

The market is divided into commercial, business jet, regional aircraft, and transport aircraft based on aircraft type. The commercial aircraft type segment owns the largest aircraft seating market share of 33.81% in 2026, due to the rising demand for modern aircraft equipped with safe and comfortable seats, which is anticipated to fuel the market growth. Moreover, the airline operators accept the concept of low-cost subsidiary airlines to increase their revenue. Also, the demand for commercial aircraft for airline operations is increasing owing to the continuous rise in passenger air traffic around the world. According to ICAO's passenger data compilation, 100,000 flights take off and land every day all over the globe. For instance, the average duration of the flight is two hours, which would mean that around 6 million people fly somewhere every day. That's nearly 0.1% of the entire world's population. Thus, these are major factors responsible for driving the commercial aircraft type segments during 2024-2032. The transport aircraft segment is expected to hold a 17% share in 2023.

To know how our report can help streamline your business, Speak to Analyst

By Class Analysis

Rise in Passenger Traffic to drive Economy Class Segment Growth in Projection Period

Based on class, the market is segmented into economy class, premium economy class, business class, and first class. The economy class segment accounts for the largest market share of 47.29% in 2026, due to the growing demand for economy seats for budget airlines and low-cost carriers. Moreover, these modern generation economy seats are now advanced, lightweight, and made of nonmetallic material.

The premium economy segment is expected to witness significant growth during the forecast period due to the high adoption of advanced seats with reclining capabilities and attached to in-flight entertainment systems. Thus, considering the growing preferences for premium economy class seats, airline operators demand for the installation of more premium economy class seats over economy class seats.

By Seat Type Analysis

Development in Aircraft Seating to aid 16G Seats Segment to Witness High Pace Growth During 2024-2032

Based on seat type, the market is segmented into 9G seats, 16G seats, and 21G seats. The 16G seats segment is expected to witness the highest CAGR. 16G seat types offer high shock absorbance and innovative structure design; hence, providing more passenger safety and comfort. Thus, higher growth numbers are anticipated during the forecast period. Currently, all contemporary planes are fitted with 16G seats. Besides, favorable government regulations to increase the usage of 16G seat type are anticipated to drive the market growth.

- The 9G seats segment accounts for the largest market share of 64.40% in 2026.

The 21G seats segment is anticipated to grow significantly attributable to the growing procurement of modern jet commercial and business jet aircraft with luxurious seating capabilities fitted with In-Flight Entertainment and Connectivity (IFEC) for long and short duration flights.

By Component Analysis

Increasing Demand for Lightweight Aero Structure to Propel the Segment Growth in the Base Year

Based on component, the market is segmented into structure, foams, actuators, electrical fittings, and others. The structure segment is estimated to hold the largest market share of 41.60% in 2026, due to the rapidly growing aerospace industry and the increasing demand for lightweight aircraft. Thus, higher growth numbers are expected during the forecast period.

The electrical fitting segment is expected to witness higher growth numbers during the forecast period. The growth is attributed to increasing demand for IFEC systems to drive the segment growth. IFEC has been an important component of this and has assumed an increasingly important role in recent times in defining a passenger’s overall flight experience. Thus, higher growth numbers are anticipated during the projection period.

By End-Use Analysis

Rising Demand for Modern Generation Aircraft to Boost Segmental Growth

In terms of end-use, the market is segmented into OEM and aftermarket. The OEM segment has dominated the market with the highest share in the base year. The rising demand for new modern generation aircraft from emerging countries, such as India, China, and others, is expected to propel the market growth. Moreover, innovation in seating systems fitted with modern electronic equipment is expected to fuel the market growth. The major players in aircraft manufacturers, such as AirbusSE, Textron Inc., Bombardier Inc., the Boeing Company, and others, have witnessed a rise in aircraft orders from developing economies, which prompts new aircraft production.

REGIONAL INSIGHTS

North America Aircraft Seating Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed approximately USD 2.49 billion to the global market in 2025, accounting for 30.50% share, and is expected to reach USD 2.65 billion in 2026. The growth is attributed to the presence of a large number of players and the presence of aircraft manufacturers. The U.S. market is projected to reach USD 2.343 billion by 2026.

Europe

In 2025, the European market stood at USD 2.31 billion, representing 28.20% of global demand, and is projected to grow to USD 2.46 billion in 2026. The market in Europe will grow at a moderate rate due to the increase in passenger air traffic and the presence of prominent key players and OEMs such as Lufthansa Technik, Safran SA, STELIA Aerospace, and others responsible for market growth in the region. The companies also have a strong global presence in the market with extensive product portfolios, and they largely focus on innovative product development. The UK market is projected to reach USD 0.71 billion by 2026, and the German market is projected to reach USD 0.548 billion by 2026.

Asia Pacific

The Asia Pacific region captured 25.90% of the global market in 2025, generating USD 2.11 billion in revenue, and is projected to reach USD 2.26 billion in 2026. This growth is attributed to the rising expenditure in the aviation industry from economies such as India and China. China and India, alongside the remainder of Asia Pacific, are anticipated to boost the aircraft market in APAC, which will create more airplane seats. The Japan market is projected to reach USD 0.442 billion by 2026, the China market is projected to reach USD 0.691 billion by 2026, and the India market is projected to reach USD 0.537 billion by 2026.

Latin America, Middle East & Africa

In 2025, the Middle East & Africa generated USD 0.71 billion, contributing 8.60% to global market revenue, and is projected to grow to USD 0.75 billion in 2026. The market in the Middle East & Africa to grow at a steady rate due to growing investment by airlines in modifications to aircraft seats is anticipated to drive the market in the region. Moreover, the Middle East is the home of some major airlines in the aviation industry; therefore, these airline operators create demand for MRO services for aircraft seats, including seat refurbishment and overhaul. Thus, higher growth numbers are anticipated during the forecast period. Latin America recorded a market size of USD 0.56 billion in 2025, capturing 6.80% of the global market share, and is projected to reach USD 0.59 billion in 2026.

KEY INDUSTRY PLAYERS

Key Players Focus on Innovation and Advancements to Reinforce Market Position

This market is dominated by some key manufacturers such as Collins Aerospace, Geven S.p.a., RECARO Aircraft Seating GmbH & Co. KG, and Safran. The wide range of product portfolios, good relations with aircraft manufacturers and airline operators, and significant investment in R&D for aircraft seat advancements activities are strategies increasingly adopted by major companies to expand their market share. For instance, Geven, an Italian seat maker, has launched a new narrow-body economy seat as part of a larger makeover of its product line. The 7.9kg per passenger "SuperEco" seat was created to cater to the most basic and necessary needs of the high-density cabin world. Moreover, organizations extend their business by embracing methodologies such as significant spending in mergers and acquisitions, joint agreements, ability expansion, structure and designing, and focus on increasing distribution networks across the globe.

List of Top Aircraft Seating Companies:

- Collins Aerospace (U.S.)

- ACRO Aircraft Seating Ltd (U.K.)

- Aviointeriors S.p.A. (Italy)

- Expliseat SAS (France)

- Geven S.p.a. (Italy)

- HAECO (China)

- Iacobucci HF Aerospace S.p.A. (Italy)

- JAMCO Corporation (Japan)

- Adient Aerospace (U.S.)

- Mirus Aircraft Seating Ltd (U.K.)

- RECARO Aircraft Seating GmbH & Co. KG (Germany)

- STELIA Aerospace (France)

- Thompson Aero Seating Limited (U.K.)

- Zim Flugsitz GMBH (Germany)

- Safran SA (France)

- Lufthansa Technik AG (Germany)

KEY INDUSTRY DEVELOPMENTS:

- February 2024 - Recaro Aircraft Seating has been selected by Air India to supply premium economy and economy seating for its widebody expansion program, which is part of the record-breaking order of 470 aircraft. Over 22,000 Recaro seats would be installed in the airline's linefit and retrofit twin-aisle programs over the next five to six years, according to the agreement.

- November 2023 - Emirates signed several contracts with French aerospace company Safran worth a total of USD 1.2 billion that cover products from its new aircraft seats to wheels. The agreements include a USD 1 billion deal for business, premium economy, and economy class seats on Emirates' new A350 and 777X-9 jets and its existing Boeing 777-300 fleet, all at list prices.

- October 2023 - Acro Aircraft Seating was awarded a contract to retrofit Series 9 fixed-back economy-class seats to up to 15 Airbus A320 and A321 aircraft by Electra Airways, a European charter and AMCI airline. The first cargo vessel would arrive at the end of 2023, with the first Airbus A320 expected to arrive in early 2024.

- June 2023 - Acro Aircraft Seating was selected to supply Deutsche Aircraft with their Series 9 economy class seats for the D328 family of aircraft, which includes the new D328eco and a retrofit option for the proven D328 turboprop.

- June 2023 - Recaro Aircraft Seating and Embraer reached a deal to develop a Supplier Furnished Equipment (SFE) catalogue of seats for E1 and E2 aircraft. The bestselling BL3710 and SL3710 economy class seats would be included in the SFE catalog and they are available in line-fit and retrofit configurations.

REPORT COVERAGE

The global aircraft seating market research report provides a detailed analysis of the market. It focuses on key aspects such as leading companies, product types, and leading product applications. Besides this, the report offers insights into the aircraft seating market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.90% over 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Aircraft Type

|

|

By Class

|

|

|

By Seat Type

|

|

|

By Component

|

|

|

By End-Use

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 8.17 billion in 2025 and is projected to reach USD 12.77 billion by 2034

The market will exhibit a CAGR of 4.90% during the forecast period.

Commercial aircraft is the leading segment in the market.

Collins Aerospace, Geven S.p.a., RECARO Aircraft Seating GmbH & Co. KG, and Safran are the leading players in the global market?

North America dominated the market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us