Aircraft Sequencing System Market Size, Share & Industry Analysis, By System Type (Arrival Sequencing (AMAN/XMAN), Departure Sequencing (DMAN), Integrated Arrival/Departure Suites, and Cloud Service-based Sequencing), By Solution (Software and Service), By Airport Type (Global Hub Airports, Point-to-Point O&D Airports, Regional/Remote & Emerging Airports, and Others), By Application (Runway Capacity & Throughput Optimization, Punctuality & On-Time Performance (OTP) Protection, Fuel Burn & CO₂ Emissions Reduction, & Others), By End User, and Regional Forecast, 2026-2034

Aircraft Sequencing System Market Size and Future Outlook

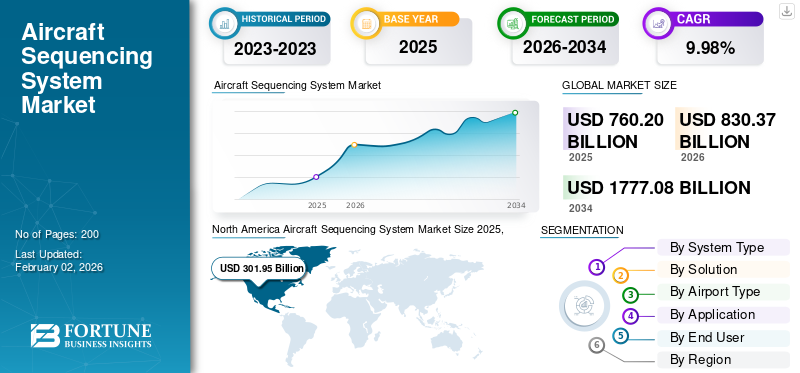

The global aircraft sequencing system market size was valued at USD 760.20 million in 2025. The market is projected to grow from USD 830.37 million in 2026 to USD 1777.08 million by 2034, exhibiting a CAGR of 9.98% during the forecast period. North America dominated the aircraft sequencing system market with a market share of 39.61% in 2025.

The Aircraft Sequencing System (ASS) market covers digital tools such as AMAN, DMAN, and integrated A/D managers that calculate and optimize the order and timing of arriving and departing flights. Due to this, controllers can use runway and airspace capacity more safely and efficiently. These systems pull in flight plans, surveillance (radar/ADS-B), network slots, and airport data and generate target times and display sequences on controller timelines or HMIs. These are often tightly coupled with A-CDM and surface management.

Key players include Thales, Indra, Leonardo, Saab, Frequentis, DFS Aviation Services, and SITA. These companies focus on rolling out integrated AMAN/DMAN and cloud-enabled solutions across Europe and other high-density hubs.

Download Free sample to learn more about this report.

AIRCRAFT SEQUENCING SYSTEM MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 760.20 Million

- 2026 Market Size: USD 830.37 Million

- 2034 Forecast Market Size: USD 1,777.08 Million

- CAGR: 9.98% from 2026–2034

- North America dominated the aircraft sequencing system market with a 39.61% share in 2025.

- Integrated arrival/departure suites led the market by system type in 2025.

- Air Navigation Service Providers (ANSPs) dominated the market by end user in 2025.

North America

North America generated USD 301.95 million in 2025 and maintained the leading regional position.

Europe

Europe market projected to reach USD 159.31 million in 2026.

Asia Pacific

Asia Pacific fastest-growing region with a CAGR of 10.70% during the forecast period.

U.S.

Aircraft sequencing system market projected to reach USD 200.64 million in 2026.

Japan

Aircraft sequencing system market projected to reach USD 34.79 million in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Air Traffic and Automation Push Demand for Intelligent Sequencing Systems

The significant rise in global air traffic in commercial and military sectors has created a high demand for advanced aircraft sequencing systems that improve safety and efficiency. Contemporary airports encounter capacity limitations, prompting operators to implement automated sequencing solutions for accurate scheduling and decreased congestion. Automation, aided by AI and data analytics, enables improved coordination between various aircraft during takeoff and landing, thereby reducing the chances of human error. Furthermore, the increasing need for sustainable aviation practices encourages airlines to utilize sequencing systems that enhance fuel efficiency and reduce taxiing time, thereby improving both environmental and operational performance.

MARKET RESTRAINTS

High Integration Costs and System Complexity May Limit Widespread Adoption

Aircraft sequencing technologies improve operational efficiency; however, their high implementation and integration costs continue to be a major restraint. Many legacy platforms require hardware and software upgrades, demanding custom interfaces with existing avionics. Airlines and smaller defense operators hesitate due to uncertain return on investment and complex certification requirements. The interoperability issues between civil and military traffic management systems also slow down the adoption. Furthermore, the lack of standardized communication protocols across various air traffic control regions makes large-scale deployment difficult, creating bottlenecks for global harmonization despite evident operational benefits.

MARKET OPPORTUNITIES

Next-Generation Air Mobility and Smart Airports to Create Market Opportunities

The rise of Urban Air Mobility (UAM), autonomous aircraft, and smart airport initiatives presents an opportunity for next-generation sequencing systems. These technologies require dynamic airspace coordination tools that can manage high-density, low-altitude traffic, and mixed vehicle types. Airports investing in digital twin infrastructure, machine learning, and predictive analytics are seeking adaptive sequencing software to improve throughput and passenger flow. Seamless integration with cloud-based air traffic management platforms and distributed computing also opens opportunities for scalable, cross-border operations. As global aviation authorities focus on modernization activities, vendors providing modular and interoperable sequencing systems will capture a significant aircraft sequencing system market share.

AIRCRAFT SEQUENCING SYSTEM MARKET TRENDS

AI-driven and Collaborative Sequencing Systems Transform Air Traffic Management

The market is shifting toward AI-enabled and data-driven solutions that are capable of adaptive scheduling and real-time decision-making, driven by the increasing demand for efficient air traffic management. Advanced algorithms analyze factors such as weather, aircraft type, and runway configuration to dynamically optimize sequencing. Collaborative Decision Making (CDM) is gaining traction among airports, airlines, and air traffic control agencies, allowing for shared situational awareness. The integration of satellite-based navigation and 5G communication further supports predictive sequencing, thereby reducing delays and fuel consumption. These innovations signal an evolution from rule-based systems to intelligent, self-learning platforms that enhance overall airspace efficiency and safety.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Complex Airspace Integration and Real-Time Coordination Barriers to Create Market Challenges

One of the major challenges in the market is integrating diverse aircraft types and traffic flows within increasingly congested global airspace. Coordinating manned, unmanned, and commercial aircraft in real time demands advanced interoperability between air traffic control systems, onboard systems, and satellite communication networks. Variations in regional air traffic management policies and legacy infrastructure create bottlenecks that limit synchronization and scalability. Furthermore, ensuring ultra-low latency and reliability during high-volume operations remains difficult as even brief communication lags or data inconsistencies can disrupt sequencing precision and compromise overall flight safety.

Segmentation Analysis

By System Type

Rising Focus on Coordinated Runway Sequencing to Fuel Integrated Arrival/Departure Suites Segment Growth

On the basis of system type, the market is classified into Arrival sequencing (AMAN / XMAN), Departure sequencing (DMAN), integrated arrival/departure suites, and cloud service-based sequencing.

The integrated arrival/departure suites segment dominated the market in 2025. The growth of this segment is driven by the need to manage arrivals and departures as a single flow, allowing hubs to unlock extra runway capacity and reduce delays that standalone AMAN or DMAN tools cannot address completely.

The cloud service-based sequencing segment is expected to grow at the highest CAGR of 7.55% over the forecast period.

By Solution

Rising Investments in Advanced Prediction and Optimization Software to Drive Software Segment Growth

In terms of solution, the market is bifurcated into software and service.

The software segment captured the largest share of the market in 2025. The segment grows as airports and air traffic controlling systems, along with Air Navigation Service Providers (ANSPs), spend more on optimization engines, AI-based prediction, and modular add-ons.

The service segment is expected to grow at the highest CAGR of 6.40% over the forecast period.

By Airport Type

Rising Air Traffic Complexity and Sequencing Needs Fuels Global Hub Airports Segment Expansion

Based on airport type, the market is segmented into global hub airports, point-to-point O&D airports, regional / remote & emerging airports, and others.

The global hub airports segment held the dominant position in 2025. The growth of this segment is driven by increased investment activities due to rising air traffic and mixed aircraft fleets, making sequencing essential for maintaining traffic flow.

The point-to-point O&D airports segment is set to flourish and grow at a CAGR of 7.17% over the forecast period.

By Application

Growing Focus on Improving Runway Throughput to Propel Runway Capacity & Throughput Optimization Segment Growth

Based on application, the market is segmented into runway capacity & throughput optimization, punctuality & On-Time Performance (OTP) protection, fuel burn & CO₂ emissions reduction, and disruption management & operational resilience.

The runway capacity & throughput optimization segment held the dominating position in 2025. This segment grows as operators rely on sequencing methods to achieve more safe movements per hour from existing infrastructure, after hitting severe physical limits on new runway construction.

The disruption management & operational resilience segment will witness a growth rate of 6.47% during the forecast period.

By End User

National Air Traffic Management (ATM) Modernization Priorities to Strengthen Air Navigation Service Provider Segmental Growth

Based on end user, the market is segmented into air navigation service provider, airport operators, and defense/military air bases.

The Air Navigation Service Provider (ANSPs) segment dominated the market in 2025. The segmental growth is driven by increased national investments and modernization programs by air navigation service providers, which prioritize control tower automation for safe and efficient operations.

The airport operators segment will witness a growth rate of 7.09% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

Aircraft Sequencing System Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America held the dominant share in 2024, valued at USD 277.70 million. It maintained its leading position in 2025, with a value of USD 301.95 million. The region dominates the aircraft sequencing system market and is anticipated to grow due to sustained traffic density at major hubs and ongoing ATM modernization. In the U.S., the product demand is supported by airlines and ANSPs seeking to cut fuel burn and improve on-time performance using integrated AMAN/DMA. In 2026, the U.S. market is estimated to reach USD 200.64 million.

North America Aircraft Sequencing System Market Size 2025,(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe and Asia Pacific

Regions such as Europe and Asia Pacific are anticipated to witness a notable aircraft sequencing system market growth in the coming years. During the forecast period, the Asia Pacific market is projected to record a growth rate of 10.70%, which is the highest among all the regions. It is the fastest-growing, owing to rapid air traffic expansion, aggressive airport infrastructure build-out, and the need to bring newer hubs straight into modern, digital tower and sequencing architectures. Supported by these factors, China is anticipated to record a valuation of USD 73.71 million, Japan to record USD 34.79 million, and India to record USD 58.05 million in 2026. After Asia Pacific, the market in Europe is estimated to reach USD 159.31 million in 2026. This growth is driven by the need to improve operational efficiency in takeoff and landing systems, optimizing air traffic and meet sustainability goals. In the region, the U.K. and Germany are projected to reach USD 52.46 million and 43.94 million respectively in 2026.

Rest of the World

The Middle East & Africa and Latin America regions are expected to experience a steady growth over the forecast period. The rest of the world region is expanding, owing to the rise in commercial aviation where major airlines are increasingly adopting sequencing technologies to optimize operations and manage traffic flow. The Middle East & Africa market is set to hit a valuation of USD 76.54 million in 2026. The Latin America market is expected to touch a value of USD 47.32 million in the same year.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations and AI Integration to Shape the Competitive Landscape

This market is moderately consolidated with a few primes and strong regional specialists. Key aircraft sequencing system contributors such as Thales Group, Saab AB, Honeywell Aerospace, and Indre Sistemas operate alongside government-backed programs including Eurocontrol, the FAA’s NextGen initiative, and SESAR Joint Undertaking. Companies are focusing on adaptive, AI-driven sequencing tools that cut taxi and runway delays while boosting overall airside efficiency. Aviation industry alliances with airport operators and navigation service providers allow field demonstrations, while regional production and modular system improvements promote standardization across international air traffic networks.

LIST OF KEY AIRCRAFT SEQUENCING SYSTEM COMPANIES PROFILED

- Thales Group (France)

- Indra Sistemas S.A. (Spain)

- Leonardo S.p.A. (Italy)

- Frequentis AG (Austria)

- Saab AB (Sweden)

- DFS Aviation Services GmbH (Germany)

- SITA (Switzerland)

- NATS Holdings Limited (U.K.)

- Honeywell International Inc.(U.S.)

- Raytheon Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: According to the Common Project One Regulation by European Commission, Extended AMAN must be put into place within 180 nautical miles (333 km or 45 minutes of flight time) of the 20 busiest airports in the EU. This includes cross-border coordination between ATC centers, specific air traffic control (ATC) protocols, and auxiliary technology.

- July 2025: Thales received recognition for the effective implementation of an Approach Spacing Tool (AST) in Hong Kong, which minimizes CO2 emissions and fuel consumption by optimizing arrival spacing.

- December 2024: Using the Digital Platform created by Indra, EUROCONTROL, successfully deployed the first digital platform for air traffic control in a public cloud with the assistance of ATOS and Microsoft. It is an international civil-military organization tasked with assisting the European aviation sector and designated as the Network Manager.

- June 2024: Indra and DFS Aviation Services partnered to deploy the AMAN arrival management system in Bucharest's Terminal Manoeuvring Area (TMA). Air traffic management activities in the area are expected to undergo a radical change as a result of this cooperative effort, which comprises both upgraded and basic Arrival Manager AMAN features.

- March 2024: SITA and DFS Aviation Services (DAS) announced their partnership to create an Arrival Manager (AMAN) and Departure Manager (DMAN) solution. In line with the two organizations' Memorandum of Cooperation (MoC), this strategic alliance seeks to transform air traffic controllers and improve operational effectiveness at airports across the globe.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key aircraft sequencing system industry developments, and details on partnerships, mergers and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attributes | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.98% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By System Type, Solution, Airport Type, Application, End User, and Region |

| By System Type |

|

| By Solution |

|

| By Airport Type |

|

| By Application |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 760.20 million in 2025 and is projected to reach USD 1777.08 million by 2034.

In 2025, the market value stood at USD 301.95 million.

The market is expected to exhibit a CAGR of 9.98% during the forecast period of 2026-2034.

The integrated arrival/departure suites segment led the market by system type in 2025.

Rising air traffic and automation are the key factors driving the demand for aircraft sequencing systems.

Thales Group (France), Indra Sistemas S.A. (Spain), Leonardo S.p.A. (Italy), Frequentis AG (Austria), and Saab AB (Sweden) are some of the major players in the market.

North America dominated the market with the largest share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us