Aircraft Service Stairs Market Size, Share & Industry Analysis, By Mechanism (Hydraulic Operated, Electric Operated, and Manual), By Product Type (Towable Aircraft Stairs, Self-Propelled Aircraft Stairs, and Electric / Hybrid Stairs), By Aircraft Type (Narrow-Body Aircraft, Wide-Body Aircraft, Regional Jets / Turboprops, and Business Jets), By End-User (Airlines, Airports / Ground Handling Companies, Military & Government), By Distribution / Ownership Model (Direct Purchase and Aftermarket / Refurbished Units), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

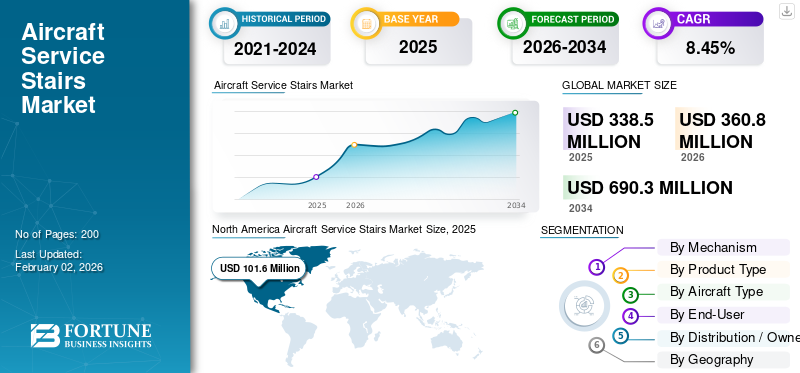

The global aircraft service stairs market size was valued at USD 338.50 million in 2025 and is projected to grow from USD 360.80 million in 2026 to USD 690.30 million by 2034, exhibiting a CAGR of 8.45% during the forecast period. North America dominated the global market with a share of 30.02% in 2025.

The aircraft service stairs market involves designing and supplying boarding stairs, which provide safe access for passengers to aircraft at remote stands or in places where fixed jet bridges are not available. The market includes towable, self-propelled, hydraulic, electric, and hybrid models and cater to a range of aircraft, from regional turboprops to wide-body planes. Increasing passenger traffic, airport infrastructure expansion, and the need for flexible ground handling solutions boost the market’s growth. Additionally, electrification and sustainability goals are influencing product development.

Key players in this market are JBT AeroTech (U.S.) TLD Group (France), Mallaghan (U.K.), TREPEL (Germany), and Weihai Guangtai (China). Regional providers such as Aero Specialties and Sovam also play a role. Competition focuses on reliability, customization, and after-sales support. There is a growing emphasis on electric stairs, modular designs, and refurbishment programs to meet new demand and aftermarket opportunities.

Download Free sample to learn more about this report.

Aircraft Service Stairs Market Key Takeaways

- 2025 Market Size: USD 338.50 million

- 2026 Market Size: USD 360.80 million

- 2034 Forecast Market Size: USD 690.30 million

- CAGR: 8.45% from 2026–2034

- North America dominated the aircraft service stairs market with a 30.02% share in 2025.

- The hydraulic operated segment is projected to account for the largest market share of 52.34% in 2026.

- The towable aircraft stairs segment is projected to hold a 37.41% market share in 2026.

North America

North America accounted for 30.02% of the global market in 2025, valued at USD 101.6 million, and is projected to reach USD 108.1 million in 2026.

Europe

Europe held a 21.65% market share in 2025, with a market value of USD 73.3 million, increasing to USD 77.8 million in 2026.

Asia Pacific

Asia Pacific represented 26.94% of global revenue in 2025, reaching USD 91.2 million, and is projected to grow to USD 98.0 million in 2026.

U.S.

U.S. The aircraft service stairs market is projected to reach USD 98.6 million by 2026.

Japan

Japan The aircraft service stairs market is projected to reach USD 18.2 million by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rapid Airport Capacity Growth and Recovery of Passenger Numbers Drive Demand for Mobile Boarding Solutions

Global air traffic recovery after the pandemic, along with an increase in point-to-point services and investments in secondary and regional airports, drives the increasing number of turnarounds and the need for flexible boarding equipment, such as mobile service stairs, where jet bridges are not available or practical. Airports that expand terminals or open new regional hubs often add or replace their ground support fleets. Operators prefer mobile stairs because they can accommodate different types of aircraft and serve remote stands. This creates consistent demand for towable and self-propelled stairs.

- For instance, in September 2025, Cambodia opened the new Techo International Airport, a large greenfield facility with plans for capacity expansion through 2030. This illustrates how new airports create long-term demand for ground support equipment, including mobile aircraft stairs.

MARKET RESTRAINTS

High Upfront Costs, Infrastructure Limits, and the Ups and Downs of Commercial Aviation Industry Slow Down Adoption

Advanced self-propelled and electric or hybrid stairs have higher buying and integration costs, such as charging stations, power upgrades at depots, and training. This makes it hard for smaller regional airports or operators with tight budgets. For many airports, the total cost of ownership still favors cheaper towable or refurbished units in the short term. This slows down full fleet upgrades. Airports and handling operators also need to plan for charger installation and grid upgrades before they can roll out electric ground support equipment, which adds extra costs and time.

- For example, in 2025, industry experts pointed out that the adoption of electric ground support equipment often gets limited by airport electrical capacity and the need for charging infrastructure; this is a challenge for operators moving to electric stairs.

MARKET OPPORTUNITIES

Electrification and Smart Technology for Stairs Create New Revenue Opportunities for Aftermarket Services

Turning stairs electric with full propulsion and battery management—along with adding telematics, predictive maintenance, and remote diagnostics opens up chances for steady income for manufacturers and service providers. Airports and handling companies that switch to electric fleets will need charging infrastructure, battery-swap or battery-service options, and software for managing their fleets. This change expands vendor relationships from simple equipment sales to long-term service contracts. Suppliers that combine hardware, charging, and fleet-management software can earn more value from each unit over time.

- In July 2025, Swissport announced an approx. USD 1.6 billion investment to electrify its global ground support equipment fleet, which includes tens of thousands of units. This shows significant moves by ground handlers toward electric fleets, boosting demand for electric stairs, chargers, and related services.

MARKET CHALLENGES

Supply Chain Delays and Cost Inflation Affecting GSE Production

Manufacturers of aircraft stairs are dealing with supply chain delays, especially for steel, aluminum, hydraulic parts, and batteries used in electric models. The pandemic, geopolitical issues, and fluctuating raw material prices have led to longer lead times and increased production costs. These issues limit the availability of new units for operators planning fleet upgrades and make airports rely on extending the life of their current units.

- In August 2022, John Bean Technologies (JBT) pointed out supply chain disruptions and rising input costs in its quarterly update, which showed the challenges facing the entire GSE manufacturing industry.

AIRCRAFT SERVICE STAIRS MARKET TRENDS

Industry-wide Push to Decarbonize and Standardize Ground Handling Accelerates eGSE Adoption

Airlines, ground handlers, and airports are increasingly setting de-carbonization targets and operational standards. This change is steering procurement policies and contracts toward electric or low-emission ground equipment. As major ground handlers test and expand electric fleets, the perceived risk for operators buying electric stairs decreases. This creates a bandwagon effect; as charging infrastructure and operator experience improve, the pace of e-stair adoption increases. Over time, regulations and airport sustainability targets will make older diesel and hydraulic units less appealing.

- For example, in May 2024, IATA’s ground-handling priorities highlighted safety, global standards, and integrating sustainability into ground handling, which supports the shift to electric and standardized GSE, including passenger stairs.

Download Free sample to learn more about this report.

Russia-Ukraine War Impact

Geopolitical Conflict Disrupts Supply Chains and Shifts Demand Patterns in Ground Support Equipment

The Russia-Ukraine conflict has greatly disrupted commercial aviation and ground support markets. Airspace closures over Russia, Ukraine, and nearby areas have led airlines to reroute flights and reduce operations to and from affected airport infrastructure. This situation has decreased the immediate need for aircraft service stairs in Eastern Europe while increasing their use at alternative hubs in Central and Western Europe. Sanctions on Russia have also blocked access to Western-made ground support equipment, forcing Russian airports to depend on domestic manufacturers or refurbished fleets.

- In March 2023, Poland’s LOT Polish Airlines announced expanded operations at Warsaw Chopin Airport to handle redirected Eastern European passenger traffic. This shows how regional hubs gained demand while Ukraine’s airports remained closed.

Segmentation Analysis

By Mechanism

Hydraulic Mechanism Leads Due to their Smoothness of Operation and Capacity for Operating a Diverse Range of Aircraft

On the basis of mechanism, the market is classified into hydraulic operated, electric operated, and manual.

Among mechanisms, hydraulic operated segment is projected to lead the market with a 52.34% in 2026, due to their reliability, smoothness of operation, and capacity for operating a diverse range of aircraft sizes from narrow-body jets to wide-bodies. Their ruggedness and relatively lesser initial cost compared to electric models render them the first choice for most airports as well as ground handling companies, especially in areas where electrification infrastructure is still in its nascent stages. Though electric stairs are becoming popular as a result of sustainability efforts, hydraulic systems retain the biggest aircraft service stairs market research market share, thanks to their long history of success and universal availability.

- For example, in June 2023, Mallaghan Engineering supplied a fleet of hydraulic passenger stairs to Dubai International Airport, confirming the ongoing popularity for hydraulic units at busy global airports.

By Product Type

Towable Aircraft Stairs Dominates Due to Low-Cost, Simple to Maintain, and Extremely Flexible for Airports Serving Mixed Fleets

In terms of product type, the market is categorized into towable aircraft stairs, self-propelled aircraft stairs, and electric / hybrid stairs.

Among product types, towable aircraft stairs segment is projected to lead the market with a 37.41% in 2026, as they are low-cost, simple to maintain, and extremely flexible for airports serving mixed fleets of regional jets, narrow-bodies, and certain wide-bodies. Towable stairs have less capital expenditure compared to self-propelled or electric/hybrid units, rendering them particularly favorable to regional airports and developing markets' operators, where budgets are tight. Their ease, coupled with ease of rapid positioning in tractors or tugs, makes them commonly adopted in civilian as well as military airfields. Though self-propelled and electric types are in increasing demand in light of efficiency and sustainability objectives.

- In April 2024, Aero Specialties delivered a fleet of towable passenger stairs to airports in the United States Northwest, highlighting sustained strong demand for this cost-effective product type.

Electric / hybrid stairs segment is expected to grow at the highest CAGR of 9.6% over the aircraft service stairs market forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Aircraft Type

Narrow-body Aircraft Leads Due to its High-Usage in Boeing Aircraft

Based on aircraft type, the market is segmented into narrow-body aircraft, wide-body aircraft, regional jets / turboprops, and business jets.

By aircraft type, the narrow body aircraft segment is projected to lead the market with a 52.78% in 2026, the dominance is attributed to the extensive global fleet of models such as Boeing 737 and Airbus 320 Families. These aircraft act as the backbone of short- and medium haul travel, accounting for the highest share of airline deliveries and daily flight operation worldwide. Airports and ground handlers thus need large quantities of service stairs that are compatible with narrow-bodies, especially in secondary airports and out-of-the-way stands where jet bridges are not available. The intense utilization of narrow-bodies in matured as well as developing markets guarantees steady demand for towable and hydraulic stairs that are specifically designed for this category.

- For example, in June 2023, Airbus said that the A320 family represented over 60% of its overall backlog of commercial aircraft orders, highlighting the dominance of narrow-body aircraft and the resultant demand for compatible service stairs.

By End-User

Airlines is the Leading End User Owing as they Control Majority of Ground Support Equipment

Based on end-user, the market is segmented into airlines, airports / ground handling companies, military & government.

At the end-user level, airlines segment is projected to lead the market with a 57.03% in 2026 in the aircraft service stairs industry because they directly control a large percentage of ground support equipment to provide efficient operation, safety, and turnaround. Major carriers purchase towbar and self-propelled stairs to aid operations at secondary airports and distant stands, especially for narrow-body fleets that dominate global passenger traffic. Airlines' focus on cost effectiveness and rapid boarding solutions guarantees a continuous replacement cycle and pushes new model adoption, such as electric and hybrid stairs in accordance with sustainability objectives.

- For example, in May 2024, IndiGo added new passenger stairs to its ground support fleet to meet increasing domestic operations in Indian tier-2 airports, demonstrating how airlines directly compel demand for such equipment.

The segment of airports / ground handling companies is set to flourish with a significant growth rate of 9.7% over the forecast period.

By Distribution / Ownership Model

Direct Purchase Dominates as Majority of Airlines, Airports, and Ground Handling Companies Prefer Ownership of Ground Support Equipment

Based on distribution / ownership model, the market is segmented into direct purchase and aftermarket / refurbished units.

Direct purchase model holds the largest of the aircraft service stairs market share since the majority of airlines, airports, and ground handling companies prefer owning such key ground support equipment to guarantee dependability and adherence to safety standards. Direct buying also allows for stair design customization to fleet-specific needs (e.g., narrow-body or wide-body series) and provides operators with long-term maintenance cycle control.

- In February 2024, Saudi Ground Services declared direct purchase of new passenger stairs under its fleet renewal program in Riyadh, where it said it preferred to own instead of lease or use refurbished ones.

The segment of aftermarket / refurbished units is set to flourish with a significant growth rate of 10.3% growth across the forecast period.

Aircraft Service Stairs Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Middle East, Africa, and Latin America.

North America

North America Aircraft Service Stairs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 101.6 million in 2025, capturing 30.02% of global revenue, and is estimated to reach USD 108.1 million in 2026. North America’s mature market is stable with demand focused on fleet replacement and policy-led movement to electric and hybrid stairs supported by sustainability initiatives in the U.S. and Canada. The U.S. market is projected to reach USD 98.6 million by 2026.

Europe

Europe enjoys widespread airport modernization and EU de-carbonization regulations, while Eastern Europe has observed increased utilization and new acquisitions as traffic has been redirected as a result of the Russia-Ukraine war. The UK market is projected to reach USD 13.9 million by 2026, and the Germany market is projected to reach USD 19.2 million by 2026. In 2025, Europe held 21.65% of the global market, reaching a valuation of USD 73.3 million, and is projected to grow to USD 77.8 million in 2026.

Asia Pacific

Asia Pacific is the region with the most rapid expansion, driven by China, India, and Southeast Asia's fast-growing passengers, combined with many Greenfield airport developments; cost-effective producers such as Weihai Guangtai are suitably placed here. The Japan market is projected to reach USD 18.2 million by 2026, the China market is projected to reach USD 43.3 million by 2026, and the India market is projected to reach USD 12.3 million by 2026. The market in Asia Pacific reached USD 91.2 million in 2025, representing 26.94% of total market revenue, and is projected to reach USD 98 million in 2026.

Rest of the world

In the rest of the world, Latin America demonstrates steady but budget-limited growth, in which used or towable stairs continue to be popular, while Africa and the Middle East are witnessing robust demand through large airport megaprojects and Gulf carrier fleet growth opportunities for cutting-edge self-propelled and electric units. In 2025, Rest of the World generated USD 72.4 million, contributing 21.30% to global market revenue, and is projected to grow to USD 76.9 million in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Market is Consolidated as Domestic Players Only Focus on Specific Requirements

With electric and hybrid models, modular designs, and cutting-edge safety features, major players concentrate on differentiating their products. Fleet support contracts, refurbishment services, and geographic reach are other factors that drive competition; larger companies target airports and ground handlers worldwide, while regional experts focus on niche or cost-sensitive markets. Weihai Guangtai, Mallaghan, TREPEL, TLD Group (France), and JBT AeroTech (USA) are some of the major participants. Regional suppliers that serve smaller airports or specific needs include Aero Specialties (U.S.) and Sovam (France). In order to stay competitive, players are increasingly implementing strategic initiatives such as joint ventures, service network expansion, and electric stair innovation.

LIST OF KEY AIRCRAFT SERVICE STAIRS COMPANIES PROFILED:

- JBT AeroTech (U.S.)

- TLD Group (France)

- Mallaghan Engineering Ltd. (U.K.)

- Stinar Corporation (U.S.)

- AERO Specialties, Inc. (U.S.)

- TIPS (Technical Industries Passenger Stairs) (Italy)

- Aviramp Ltd. (U.K.)

- Xinfa Airport Equipment Ltd. (China)

- Guangtai (Weihai Guangtai Airport Equipment Co., Ltd.) (China)

- Shenzhen CIMC-TianDa Airport Support Ltd. (China)

KEY INDUSTRY DEVELOPMENTS:

- March 2025: Guangtai formalized a MoU with SATS Ltd (Singapore) to test and trial electric ground support equipment positioning passenger stairs at the forefront of their sustainability innovation efforts.

- March 2024: Mallaghan Engineering introduced a new range of fully electric passenger stairs at the Ground Handling International conference in Lisbon, reinforcing the industry shift toward sustainable ground support equipment.

- February 2024: Saudi Ground Services procured a new fleet of hydraulic and motorized passenger stairs to support operations at Riyadh and Jeddah airports, highlighting rising investment in advanced GSE across the region.

- May 2023: India’s Airports Authority commissioned new towable passenger stairs for tier-2 and tier-3 airports, underlining demand growth driven by expanding domestic connectivity.

- July 2023: ATLAS GSE expanded its refurbishment facility in Florida to meet rising demand for cost-effective passenger stairs, showcasing the importance of the aftermarket channel.

REPORT COVERAGE

The global aircraft service stairs market analysis provides an in-depth study of market size and forecast by all market segments included in the report. It includes details on the market dynamics, market insights, and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year |

2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.45% from 2026-2034 |

| Unit | Value (USD Million) |

| By Mechanism |

|

| By Product Type |

|

| By Aircraft Type |

|

| By End-User |

|

| By Distribution / Ownership Model |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 360.80 million in 2026 and is projected to reach USD 690.30 million by 2034.

In 2025, the market value stood at USD 101.6 million.

The market is expected to exhibit a CAGR of 8.45% during the forecast period of 2026-2034.

The towable aircraft stairs segment led the market by product type.

Rapid airport capacity growth and the recovery of passenger numbers are driving demand for mobile boarding solutions.

Mallaghan Engineering (U.K.), TBD Owen Holland (U.K.), Aero Specialties (U.S.), JIANGSU Tianyi Aviation (China), Weihai Guangtai (China), ACCESSAIR Systems (Canada), and DOLL Fahrzeugbau (Germany) are some of the prominent players in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us