Airport Automation Market Size, Share & Industry Analysis, By Class (Class A, Class B, and Class C), By Deployment (On Premise, Hybrid, and Cloud), By Operations (Airside, Landside, and Terminal Side), By Application (Baggage Handling Systems, Passenger Processing, Security Systems, Air Traffic Management (ATM), and IT Solutions and Automated Ground Handling), By Function (Passenger Processing & Identity, Baggage & Cargo Automation, Airside Operations & A-CDM, Security Screening Orchestration, Ramp, Fleet & GSE Digitization, & Others), and Regional Forecast, 2026-2034

Airport Automation Market Size and Future Outlook

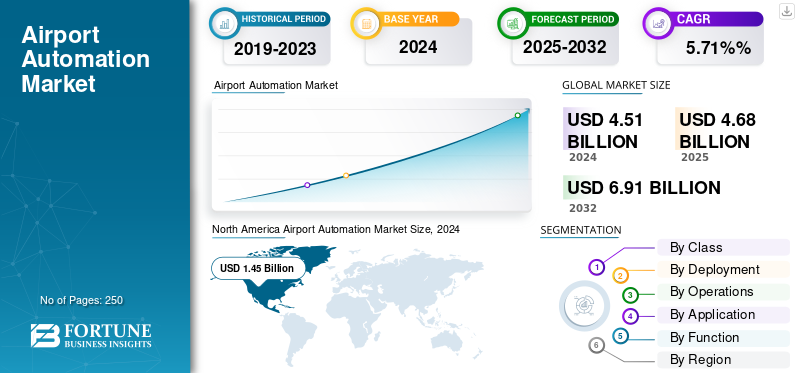

The global airport automation market size was valued at USD 4684.9 million in 2025. The market is projected to grow from USD 4877.9 million in the year 2026 to USD 8,181.50 million by 2034, exhibiting a CAGR of 6.70% during the forecast period. North America dominated the airport automation market with a market share of 32.21% in 2025

Airport automation is the integrated stack of software, controls, connected devices, and data services that digitizes airport operations end-to-end, covering passenger processing (self-service, e-gates, and biometrics), baggage and cargo (controls/WCS, RFID/RTLS, and early-bag storage), airside coordination (A-CDM, AODB, stand/gate/resource management, and A-SMGCS inputs), security screening orchestration (CT, automated baggage tray return, and lane control), ramp and GSE telematics, and landside/retail optimization.

Growth is accelerating as passenger volumes rebound and peak more sharply, forcing higher throughput without new concrete; as biometrics and common-use platforms unlock touchpoint-to-touchpoint orchestration; as screening fleets modernize and shift to hybrid edge-cloud operations; and as sustainability programs (e.g., e-GSE charging, sub-metering) demand tighter OT integration and cyber-resilience. Mature standards such as CUPPS/CUSS, ACRIS/AIDX for data exchange, EUROCONTROL A-CDM for milestone predictability, ICAO/ECAC security and environmental guidelines, and ISA/IEC-62443 for OT security, reduce integration friction and de-risk phased brownfield upgrades.

The competitive landscape is layered: platform and common-use leaders SITA and Amadeus (CUPPS/CUSS, AODB/RMS, and A-CDM); airside/tower and surveillance specialists Indra, ADB SAFEGATE, Thales, and Saab; baggage system integrators Vanderlande, BEUMER Group, Siemens Logistics (Körber), Daifuku/Glidepath, Alstef; identity/biometrics providers NEC, IDEMIA, Vision-Box; security screening and lane orchestration Leidos, Smiths Detection, OSI Systems (Rapiscan); passenger-flow analytics such as Veovo; and global integrators/cloud partners (T-Systems, IBM, DXC, Accenture, TCS, and Wipro) for integration, MLOps, SOC and managed services. Architecturally, winning programs pair deterministic edge control (PLC/SCADA, e-gate decisions, and lane controllers) with cloud analytics, event streaming, and digital twins, exposed via APIs to airlines, handlers, and border agencies. Commercially, outcome-based SLAs, managed services, and modular kits minimize downtime and spread capex, turning discrete automation systems into a standards-driven operating platform that raises capacity, resilience, and ESG performance simultaneously.

Download Free sample to learn more about this report.

AIRPORT AUTOMATION MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 4,684.9 Million

- 2026 Market Size: USD 4,877.9 Million

- 2034 Forecast Market Size: USD 8,181.50 Million

- CAGR: 6.70% from 2026–2034

- North America dominated the airport automation market with a 32.21% share in 2025.

- Passenger Processing application is projected to account for 26.34% of the market in 2026.

- Hybrid deployment is expected to lead with a 45.56% market share in 2026.

North America

North America generated USD 1,508.87 million in 2025 and is projected to reach USD 1,574.34 million in 2026.

Europe

Europe accounted for USD 1,192.18 million in 2025 and is expected to grow to USD 1,235.84 million in 2026.

Asia Pacific

Asia Pacific reached USD 924.68 million in 2025 and is projected to attain USD 972.02 million in 2026, registering the highest growth potential through 2034.

U.S.

The airport automation market is projected to reach USD 1,461.28 million by 2026.

China

The airport automation markets is projected to reach USD 92.25 million by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Throughput, Reliability, and Biometric Self-Service Shift Leading To Segmental Growth

The biggest demand-side pull is the need to move more passengers, more predictably, without the need for new concrete. Airports are scaling self-bag-drop, e-gates, and biometric “One ID” systems to compress queue times and stabilize staffing. At the same time, checkpoint modernization (using CT scanners with tray return) increases lane throughput and smooths peaks in traffic flowing to gates. These upgrades are modular, standards-based (CUPPS/ACRIS), and increasingly orchestrated by analytics, allowing brownfield sites to phase deployments around live operations. Airlines benefit via faster turns and more punctual off-blocks; airports unlock higher commercial yield through steadier pacing to retail. Crucially, device fleets are now monitored and serviced centrally, which improves availability and reduces life-cycle costs.

- In January 2024, Manchester Airports Group chose Veovo for group-wide passenger-flow management; the U.S. TSA awarded Smiths Detection a contract for full-size checkpoint CT systems to accelerate screening throughput.

MARKET RESTRAINTS

Legacy integration, OT-cyber, and Multi-year Brownfield Constraints Growth

Adoption is tempered by the complexity of integrating new platforms into decades-old OT (BHS PLC/SCADA, and access control) and airline/border IT systems. Cyber segmentation between IT and OT (ISA/IEC 62443), data protection obligations, and certification for safety-critical towers add time and cost. Brownfield realities, night works, limited outage windows, and multi-stakeholder approvals stretch schedules, particularly when central systems (baggage, AODB, and RMS) are touched. Financing also tends to skew toward staged releases, requiring roadmaps that demonstrate value at each tranche. Vendors that pre-integrate with airline DCS, border APIs, and existing controls shorten risk, but governance still dictates careful phasing.

- In January 2024, Heathrow selected the BEUMER Group to design and install a state-of-the-art replacement baggage system for Terminal 2, a six-year transformation step that illustrates the programmatic nature and duration of critical brownfield upgrades.

MARKET OPPORTUNITIES

Brownfield Modernization and Outcome-Based Service Models Pose as a Major Opportunity

The richest upside is in brownfield programs that replace end-of-life baggage controls, refresh screening fleets, and layer passenger-journey orchestration, delivering measurable gains (pax/minute, OTP, and mishandled-bag reduction) without major civil works. Airports increasingly procure “platform + managed service” bundles such as edge devices paired with cloud analytics, uptime SLAs, and predictive maintenance. This shifts spend from lumpy capital expenditure to planned operating expenditure, opens multi-airport portfolio deals, and speeds up the replication of best practices. As passenger traffic normalizes, mid-market hubs (class B) can leapfrog with standardized kits (SBD/e-gates, RMS/A-CDM) and shorter outages.

- May 2024: Heathrow’s Terminal 2 baggage system replacement with BEUMER unlocks central-area transformation; OSI Systems announced an approximately USD 42 million order for checkpoint and hold-baggage screening at an international airport, underscoring sustained refresh cycles.

AIRPORT AUTOMATION MARKET TRENDS

Hybrid Edge-cloud and Integrated Tower/Terminal Platforms are Key Market Trends

Architectures are converging on deterministic edge control (e-gate decisions, CT lane controllers, and ‘BHS PLCs) orchestrated by cloud analytics for forecasting, digital twins, and fleet health, joined by event streams and open APIs. The same pattern extends to airside: an integrated controller working position fuses tower and apron awareness, enhancing decision support and collaboration with A-CDM milestones. Benefits include lower latency for safety-critical steps, centralized monitoring across airports, and faster software iteration. As estates grow, SIEM/SOAR and cloud-based asset management reduce mean-time-to-repair and simplify compliance.

- April 2024: Hamburg Airport achieved full operational efficiency status with ADB SAFEGATE’s OneControl ICWP, integrating air travel and ground situational awareness; Manchester Airports Group partnered with Veovo to deploy predictive flow technology across its airports.

MARKET CHALLENGES

Change Management, Certification, and Supply Chain Cadence Constraints Market

Even with clear ROI, programs face people/process hurdles such as re-rostering, union engagement, and training for biometric/AI-assisted workflows. Security fleets must be certified, integrated with lane automation, and supported by spares/logistics, exposing lead-time risk and vendor capacity constraints. Data governance and privacy impact assessments add steps where journeys cross airline, airport, and border domains. Ultimately, success hinges on maintaining device availability at scale; poor uptime erodes passenger trust and undermines KPI gains. Mature operators mitigate this with staged pilots, clear SLAs, and cross-functional playbooks that couple IT, OT, and streamline operations.

- In May 2024, TSA’s award to Smiths Detection for full-size checkpoint CT systems and OSI Systems’ approximately USD 42 million screening contract highlighted the ongoing need for certified equipment, fleet sustainment, and coordinated deployment across complex operational environments.

Download Free sample to learn more about this report.

Segmentation Analysis

By Function

Passenger Processing & Identity Leads Due to Fast Delivery

On the basis of function, the market is classified into passenger processing & identity, baggage & cargo automation, airside operations & A-CDM, security screening orchestration, ramp, fleet & GSE digitization, landside, curb & parking, retail & non-aero, and energy, facilities & sustainability.

Passenger processing & identity is the largest slice as it delivers fast, visible wins without tearing up terminals. Airports are scaling self-bag-drop, e-gates, and biometric “One ID” to cut queue times, stabilize staffing, and improve on-time performance. Data from these touchpoints feeds queue prediction and dynamic lane balancing, compounding ROI as volumes normalize. Mature standards (CUPPS/ACRIS), cloud-based IAM, and privacy-by-design make multi-airline and border integrations smoother, allowing brownfield sites to upgrade in phases. Adoption also benefits retail pacing and security throughput, creating a reinforcing cycle of benefits across the terminal.

- Manchester Airports Group selected Veovo for group-wide passenger flow management (April 2024); TSA ordered HI-SCAN 6040 CTiX from Smiths Detection (January 2024) to speed checkpoints.

By Application

Rising Passenger Air Traffic is a Major Reason for Growth in Passenger Processing Segment

Based on application, the market is classified into baggage handling systems, passenger processing, security systems, Air Traffic Management (ATM), and IT solutions and automated ground handling.

The passenger processing application segment accounting for a dominating airport automation market share of 26.34% in 2026. Passenger processing spans the entire curb-to-gate journey (self-service check-in, SBD, ID checks, queue prediction, and self-boarding), so every dollar spent touches millions of passengers and multiple KPIs, pax/minute, 95th-percentile wait, and staff per lane. Airlines often co-fund under common-use models, helping airports phase deployments with minimal downtime. Modern APIs enable identity signals to trigger lane allocations, boarding calls, and baggage reconciliation, while cloud dashboards make SLA breaches actionable in real-time. In short, it’s where capacity creates immediate gains in experience.

- Heathrow chose BEUMER to replace Terminal 2’s baggage backbone, a precursor to front-of-house automation (January 2024); whereas MAG’s Veovo deal highlights predictive, staffing-aware flow tools (April 2024).

By Deployment

Hybrid Deployment Dominates due to Deterministic Control

Based on deployment, the market is classified into on-premises, hybrid, and cloud.

The hybrid segment will accounting for dominating market share of 45.56% in 2026. Hybrid wins as airports need deterministic control at the edge (BHS PLC/SCADA, e-gate decisions, and lane controllers) and elastic analytics in the cloud (forecasting, digital twins, and SIEM/SOAR). This separation enhances resilience, reduces latency, and simplifies IT/OT cyber segmentation. As fleets of scanners, cameras, check-in kiosks, and gates expand, cloud-enabled health monitoring and predictive maintenance reduce life-cycle costs, while standard APIs accelerate multi-site rollouts. The hybrid segment also suits concessions and multi-airport groups that centralize analytics while preserving local operations.

- In April 2025, TSA’s checkpoint modernization sustained momentum with a USD 96.8 million Smiths’ CT order (January 2024) and OSI Systems’ USD 42 million screening package (May 2024), edge hardware paired with cloud-supported fleets.

By Operations

Terminal Side Segment Dominate Owing to Shorter Queues and Higher Commercial Yield

Based on the operations, the market is segmented into airside, landside, and terminal side.

Terminal-side automation focuses on the highest-frequency choke points, check-in, bag drop, screening, boarding, and retail, so improvements here directly translate into shorter queues, steadier passenger pacing, and higher commercial yield. CT scanners and tray-return systems increase lane throughput; identity orchestration stabilizes boarding flows; and upgraded BHS reduces failure-induced delays. These programs are modular, quick to install, and measurable, which suits the constraints of brownfield sites.

- In January 2024, Heathrow’s Terminal 2 awarded BEUMER a multi-year BHS replacement project to de-risk central operations. Meanwhile, in April 2024, MAG adopted Veovo’s flow platform across three airports, thereby tightening staffing and SLA control.

To know how our report can help streamline your business, Speak to Analyst

By Class

Class B Segment Upgrades Deliver Best Carpex Ratio to Passenger Impact

Based on the class, the market is segmented into class A, class B, and class C.

Class B segment is expected to hold highest market share of 44.18% in 2026, Class B airports experience big-hub congestion but move faster: standardized SBD/e-gates at the front, A-CDM/RMS in operations, and targeted BHS controls deliver step-changes without requiring mega-projects. Boards prefer shorter outage windows, predictable KPIs, and SaaS/managed-service offerings. Vendors increasingly use package “airport-in-a-box” modules, allowing multi-airport groups to replicate successes. As traffic rebounds, class B upgrades deliver the best ratio of capex to passenger impact.

- In September 2023, CVG approved an eight-year USD 137 million BEUMER contract to design, install, operate, and maintain a new BHS, a classic mid-market modernization blueprint.

Airport Automation Market Regional Analysis

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Airport Automation Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 1508.87 Million in 2025, representing 32.21% of the global market share, and is projected to reach USD 1574.34 Million in 2026. North American growth is anchored in checkpoint modernization and life-cycle sustainment, with hybrid estates (edge lane control + cloud analytics) improving availability and throughput. Airports phase in journey orchestration where airline partnerships align; data from CT lanes, e-gates, and BHS feeds predictive staffing and OTP controls. Federal funding de-risks nationwide adoption and standardization. The U.S. market is projected to reach USD 1461.28 million by 2026.

- TSA awarded Smiths Detection USD 96.8 million for CT systems (January 2024) and OSI Systems USD 42 million for checkpoint/hold baggage screening (May 2024), reinforcing terminal-side capacity and reliability.

Europe

The Europe market was valued at USD 1192.18 Million in 2025, capturing 25.45% of global revenue, and is estimated to reach USD 1235.84 Million in 2026. Europe excels in A-CDM, safety nets, and ECAC Standard 3 baggage, favoring platformized data exchange and integration between towers and terminals. Privacy-by-design slows nothing when architectures are modular and standards-driven. Large brownfield baggage programs unlock terminal reconfigurations and improved pacing for security and boarding, while A-CDM sharpens milestone predictability at constrained hubs. The UK market is projected to reach USD 143.63 million by 2026, while the Germany market is projected to reach USD 53.11 million by 2026.

Asia Pacific

In 2025, Asia Pacific held 19.74% of the global market, reaching a valuation of USD 924.68 Million, and is projected to grow to USD 972.02 Million in 2026. The Asia Pacific region experiences rapid airport automation market growth and is expected to grow at the highest CAGR by 2034 in Airport Automation. Asia Pacific leads on volume and policy-backed seamless borders, making biometrics and self-service the default at major hubs. Operators pair identity with baggage and A-CDM to absorb peaks without adding stands. Greenfield-quality brownfields (Japan, Singapore, and Korea) enable rapid, standards-based upgrades with privacy-by-design. Cloud analytics sits above edge control to coordinate multi-terminal flows and disruptions. The result is fast cycle times and consistent experience. The Japan market is projected to reach USD 92.25 million by 2026, while the China market is projected to reach USD 195.91 million by 2026, and the India market is projected to reach USD 104.78 million by 2026.

Middle East & Africa

Middle East & Africa contributed approximately USD 568.17 Million to the global market in 2025, accounting for 12.13% share, and is expected to reach USD 595.9 Million in 2026. Over the forecast period, the Middle East region is expected to grow at a CAGR of 6.49% for the market. Gulf hubs compete on end-to-end experience, bundling biometrics, smart security, stand/gate optimization, and apron safety into integrated platforms. Decisive governance and greenfield-quality airport infrastructure compress timelines from pilot to production. Cloud-assisted command layers coordinate multiple terminals and operators, while edge automation maintains latency-critical control.

Rest of the World

In the rest of the world, the Latin America region captured 10.48% of the global market in 2025, generating USD 490.94 Million in revenue, and is projected to reach USD 499.77 Million in 2026. Latin America and Africa operators prioritize predictability, resource use, and OTP; A-CDM provides the shared truth to align airlines, handlers, and ATC. With milestones stabilized, airports layer passenger self-service and BHS controls to avoid heavy civil works. Concession models favor modular, replicable stacks, and managed services.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and Sustainable Innovations Define Competitive Edge

The airport automation market is moderately consolidated, led by key global players such as AkzoNobel N.V., PPG Industries, Mankiewicz Gebr. & Co., Sherwin-Williams, BASF SE, Axalta Coating Systems, and Hentzen Coatings. These companies dominate the market through extensive OEM partnerships, global MRO networks, and specialized product portfolios that cater to both commercial and defense aircraft. Competition centers on low-VOC, chrome-free, and weight-reducing formulations, as sustainability and fuel efficiency become key differentiators. Continuous innovation in polyurethane and fluoropolymer coatings, along with expansion in Asia Pacific and Middle Eastern MRO hubs, is reshaping market leadership.

LIST OF KEY AIRPORT AUTOMATION COMPANIES PROFILED

- SITA (Switzerland)

- Amadeus IT Group (Spain)

- ADB SAFEGATE (Belgium)

- Indra Sistemas (Spain)

- Thales Group (France)

- Vanderlande (Netherlands)

- BEUMER Group (Germany)

- Daifuku (Japan)

- NEC Corporation (Japan)

- Leidos (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2023 – CVG partnered with BEUMER Group to design, install, operate, and maintain a next-gen baggage system under a USD 137 million eight-year deal to boost capacity, reliability, and throughput. The program aims to reduce mishandled bags and enable more efficient staffing during peak periods.

- January 2024 – Heathrow selected BEUMER Group to replace Terminal 2’s baggage handling system for resilience and smoother passenger flows. The multi-year modernization is expected to improve terminal uptime and free up resources to scale front-of-house automation, such as self-bag-drop and biometric boarding.

- January 2024 – TSA awarded Smiths Detection a USD 96.8 million contract for HI-SCAN 6040 CTiX checkpoint CT scanners, to accelerate screening and reduce divestment. The rollout is expected to increase lane throughput, reduce queues, and support hybrid edge-cloud fleet management across U.S. airports.

- April 2024 – Manchester Airports Group partnered with Veovo for group-wide Passenger Flow Management to predict queues and optimize staffing. The deployment is going to improve on-time performance and passenger experience across Manchester, Stansted, and East Midlands through data-driven, curb-to-flight orchestration.

- May 2024 – OSI Systems (Rapiscan) won a USD 42 million order from an international airport for checkpoint and hold-baggage screening, including RTT-110. The package aims to standardize security lanes, reduce false alarms, and enable centralized health monitoring for enhanced availability.

- November 2024 – Hamburg Airport launched ADB SAFEGATE OneControl Integrated Controller Working Position to full operations, integrating air and ground situational awareness. The platform will enhance tower-terminal collaboration and improve departure predictability, aligning with A-CDM processes.

REPORT COVERAGE

The global airports automation market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The airport automation market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attribute | Detaits |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.70% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Class, Deployment, Operations, Application, Function, and Region |

| By Class |

|

| By Deployment |

|

| By Operations |

|

| By Application |

|

| By Function |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4684.9 million in 2025 and is projected to reach USD 8,181.50 million by 2034.

In 2025, the market value stood at USD 1508.87 million.

The market is expected to exhibit a CAGR of 6.70% during the forecast period.

The airside segment led the market in the operations segment.

Throughput, reliability, and biometric self-service shift leading to segmental growth.

SITA (Switzerland), Amadeus IT Group (Spain), and Thales Group (France) are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us