Airport Operations Control Center (AOCC) Market Size, Share & Industry Analysis, By Deployment Mode (Cloud/SaaS AOCC, Hybrid AOCC, and On-premise AOCC), By Airport Operational Profile (International Transfer Hub, Domestic Hub, Cargo-Heavy/Integrator Node, and Others), By Offering Type (Platform License (Perpetual/Term), Modular Software Subscriptions, Managed AOCC, Systems integration & migration services, & Others), By End User (Airport Authority-Led, Privatized Airport Operator, PPP/Concession Operator, and Airport group), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

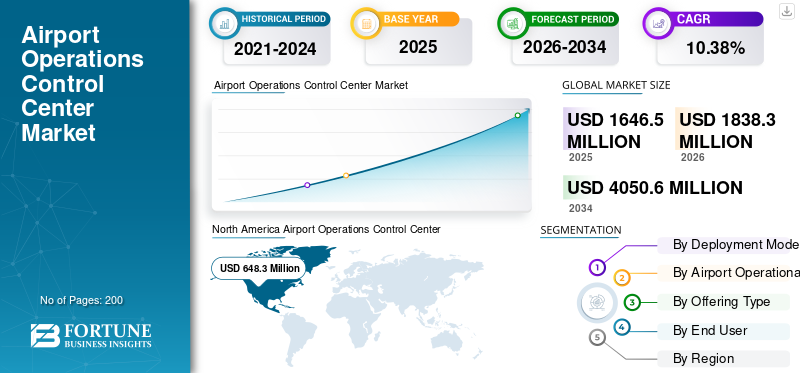

The global Airport Operations Control Center (AOCC) market size was valued at USD 1646.5 million in 2025. The market is projected to grow from USD 1,838.3 million in 2026 to USD 4050.6 million by 2034, exhibiting a CAGR of 10.38% during the forecast period. North America dominated the global airport operations control center (AOCC) market with a market share of 39.37% in 2025.

AOCC facilitates seamless airport operations across expanding complexes, linking runways, terminals, air traffic control, and ground services amid surging global air travel. Driven by urbanization and rising passenger volumes, these centers prioritize real-time coordination for diverse stakeholders, including airlines, ground handlers, and security teams, while addressing capacity constraints through efficient technologies and integration with regional traffic systems.

Key players include Collins Aerospace for integrated control software, Indra Avitech for advanced monitoring platforms, and operators such as Amsterdam Schiphol Airport managing high-volume networks.

Download Free sample to learn more about this report.

Airport Operations Control Center Market Key Takeaways

- 2025 Market Size: USD 1,646.5 million

- 2026 Market Size: USD 1,838.3 million

- 2034 Forecast Market Size: USD 4,050.6 million

- CAGR: 10.38% from 2026–2034

- North America dominated the Airport Operations Control Center (AOCC) market with a 39.37% share in 2025.

- The hybrid AOCC segment is projected to grow at a CAGR of 10.32% during the forecast period.

- The domestic hub segment is expected to register a CAGR of 10.49% over the forecast period.

North America

North America generated USD 648.3 million in revenue in 2025.

Europe

Europe is projected to reach USD 510.9 million by 2026.

Asia Pacific

Asia Pacific is expected to reach USD 367.1 million by 2026.

U.S.

The U.S. AOCC market is estimated to reach USD 440.9 million by 2026.

Japan

Japan’s AOCC market is projected to reach USD 70.9 million by 2026.

Read More

AIRPORT OPERATIONS CONTROL CENTER (AOCC) MARKET TRENDS

Real-Time Data Analytics and Automation is a Market Trend

Real time data analytics and automation emerge as a dominant trend in the market as operators integrate diverse live feeds, baggage systems, weather, security queues, and passenger flows into unified dashboards for proactive decisions. This fusion enables machine learning forecasts of transfer bottlenecks, allowing actions such as expedited passenger processing or staffing adjustments, slashing misconnects and delays.

- In November 2025, According to Assaia's 2025 Turnaround Report, airports and airlines using artificial intelligence to handle aircraft turnarounds are witnessing significant operational and financial improvements. Between April 2024 and March 2025, the study witnessed over 450,000 AI-enabled turnarounds at 15 airports in North America and Europe.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rise in Real Time Coordination to Handle Air Traffic is Anticipated to Drive Market Growth

Rising demand for real-time coordination drives AOCC adoption amid surging air traffic. Operators integrate air traffic control feeds, baggage systems, and ground handling data into unified dashboards, enabling swift gate reassignments and resource shifts during peaks using AI powered big data analytics. Furthermore, EUROCONTROL's A-CDM standards promote collaborative and real time decision making among airport partners ATC, airlines, ground handlers through timely information sharing and milestones for turnarounds. This enhances real-time coordination in AOCC by improving traffic predictability, optimizing resources.

MARKET RESTRAINTS

Cybersecurity Vulnerabilities is a Market Restraint

Adoption of Airport Operations Control Centers (AOCCs) is hampered by cybersecurity flaws as linked systems expose vital operations to sophisticated attacks. Multiple entry points for breaches are created by real-time data exchange between airlines, ATC, and ground handlers, which might possibly disrupt flights or compromise passenger information. Operators must maintain ongoing vigilance and multi-layered defenses to protect IoT sensors, cloud platforms, and legacy integrations from ransomware and state sponsored attacks.

MARKET OPPORTUNITIES

Expansion of Airport Hubs in Developing Countries Creates New Market Opportunities

Expansion of airport hubs in developing countries creates prime opportunities for Airport Operations Control Centers (AOCC) market growth as new infrastructure demands integrated command systems from the outset. Operators leverage AOCC for seamless coordination of expanded runways, terminals, and ground services, enabling scalable operations without legacy constraints. This aligns with rising air connectivity needs, where centralized monitoring optimizes traffic flow and stakeholder collaboration in high-growth regions.

- In November 2025, Bishoftu International Airport (BIA), a flagship greenfield project intended to serve Ethiopia and the larger African area, is being developed by Ethiopia. The goal of the new airport, which is about 40 kilometers southwest of Addis Ababa, is to relieve the increasing capacity constraints brought on by heavy traffic at Addis Ababa Bole International Airport (ADD).

MARKET CHALLENGES

Staff Training Gaps Present a Major Market Challenge

Staff training gaps emerge as a major challenge in AOCC deployments, where operators lack proficiency in managing complex real-time interfaces and analytics dashboards. Legacy staff accustomed to traditional operations or legacy systems struggle with integrated systems requiring cross functional collaboration among ATC, handlers, and airlines. This skills deficit delays full AOCC activation, as inadequate training leads to error prone decisions during peaks, undermining efficiency gains. Moreover, continuous upskilling programs become essential yet resource-intensive, slowing market penetration at expanding hubs.

Segmentation Analysis

By Deployment Mode

Improved Cost Efficiency to Propel Cloud/SaaS AOCC Segmental Growth

Based on the deployment mode, the market is segmented into cloud/SaaS AOCC, hybrid AOCC and on-premise AOCC.

The cloud/SaaS AOCC segment is anticipated to account for the largest Airport Operations Control Center (AOCC) market share. The high segmental share is primarily attributed as Cloud/SaaS solutions typically operate on a subscription-based, "pay-as-you-go" model which is cost efficient to many operators and end users.

The hybrid AOCC segment is anticipated to rise with a CAGR of 10.32% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Airport Operational Profile

High Volume Connectivity Demands To Boost International Transfer Hub Segment Growth

Based on airport operational profile, the market is segmented into international transfer hub, domestic hub, cargo-heavy/integrator node and others.

In 2025, the international transfer hub segment dominated the global market. This dominance of the segment is due to their massive transit volumes, demanding real-time AOCC coordination for seamless connections across multiple airlines and time-sensitive gates.

The domestic hub segment is projected to grow at a CAGR of 10.49% over the forecast period.

By Offering Type

Rise in adoption of Cloud Based Services Anticipated to boost Systems Integration & Migration Services Segment

Based on the offering type, the market is segmented into platform license (perpetual/term), modular software subscriptions, managed AOCC, systems integration & migration services and continuous improvement/analytics-as-a-service.

The systems integration & migration services segment is anticipated to witness a dominating market share over the forecast period. The growth in the segment is owing to the necessity of integrating security and guaranteeing compliance across cloud environments. Moreover, businesses need migration assistance when they migrate to the cloud for increased efficiency, agility, and customer satisfaction.

The managed AOCC segment is projected to grow at a high CAGR of 11.04% over the forecast period.

By End User

Regulatory Framework to boost Airport Authority led Segment

Based on end user, the market is segmented into airport authority-led, privatized airport operator, PPP/concession operator and airport group (multi-airport rollouts).

The airport authority led segment dominated the segmental market share. The airport authority is the main organization in charge of overall airport security since the legislative framework imposes strict safety and security standards on all airport operations. This drives the segmental growth during the study period.

In addition, privatized airport operators are projected to grow at a CAGR of 10.96% during the study period.

Airport Operations Control Center (AOCC) Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

North America

North America Airport Operations Control Center (AOCC) Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 612.3 million, and also maintained the leading share in 2025, with USD 648.3 million. The market in North America is expected to increase due to strong infrastructure improvements and heavy passenger traffic at key hubs and government funding.

U.S Airport Operations Control Center (AOCC) Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 440.9 million in 2026, accounting for roughly 10.38% of global CAGR. Domestic airline expansions and smart airport initiatives accelerate AOCC upgrades for seamless operations at busy facilities such as Atlanta and Dallas.

Europe

Europe is projected to record a growth rate during the forecast period of 10.56%, which is the second highest among all regions, and reach a valuation of USD 510.9 million by 2026. Centralized AOCC platforms are pushed across linked hubs by strict safety rules and A-CDM compliance.

U.K Airport Operations Control Center (AOCC) Market

The U.K. AOCC market in 2026 is estimated at around USD 177.8 million, representing roughly 11.00% CAGR of global market.

Germany Airport Operations Control Center (AOCC) Market

Germany’s AOCC market is projected to reach approximately USD 140.5 million in 2026.

Asia Pacific

Asia Pacific is estimated to reach USD 367.1 million in 2026 and secure the position of the third-largest region in the market and fastest growing during the study period. The demand for integrated control systems is fueled by growing regional connectivity, rapid urbanization, and new mega-airports.

Japan Airport Operations Control Center (AOCC) Market

The Japan AOCC market in 2026 is estimated at around USD 70.9 million, accounting for roughly 10.85% of CAGR during the forecast period.

The implementation of AOCC at various airports such as Tokyo Narita and Haneda is driven by aging infrastructure retrofits and strict timeliness requirements.

China Airport Operations Control Center (AOCC) Market

China’s AOCC market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 127.8 million. The growth in the country is owing to the massive state backed airport builds in tier-2 cities creating opportunities for scalable cloud-based AOCC deployments.

India Airport Operations Control Center (AOCC) Market

The India AOCC market in 2026 is estimated at around USD 100.9 million. Airport privatization and capacity expansions at Delhi and Mumbai necessitate advanced real-time coordination systems.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America. These regions are expected to witness moderate growth in this market space during the forecast period. The Middle East & Africa and Latin America market is set to reach a valuation of USD 146.7 million and USD 92.1 million in 2026. Airport privatizations in Dubai, Ethiopia, Brazil, and Mexico, among others fuel AOCC upgrades amid rising regional travel and capacity pressures.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships by Leading Players Propel AOCC Market Growth

AOCC market features a semi-consolidated structure, with leading firms such as Thales Group, Collins Aerospace, and Indra Avitech holding strong positions. Their competitive edge derives from strategic collaborations and internal synergies to deliver advanced integrated solutions amid widespread airport modernization initiatives.

Other notable contenders include SITA, Frequentis, and Honeywell. These providers target market expansion through new contracts and alliances to enhance their global presence in the coming years.

- In December 2025, as part of a collaboration with local partner SOFRATESA, Thales is scheduled to modernize Panama's Civil Aviation Authority (AAC) air traffic control center. Delivering a wide range of air traffic management solutions, such as voice recording systems (VRS), aeronautical message handling systems (AMHS), and air traffic control (ATC) systems, is part of the project.

LIST OF KEY AIRPORT OPERATIONS CONTROL CENTER COMPANIES PROFILED

- SITA (Switzerland)

- Amadeus IT Group (Spain)

- Indra Sistemas (Spain)

- Thales Group (France)

- Frequentis AG (Austria)

- ADB SAFEGATE (Belgium)

- Veovo (U.K.)

- Damarel Systems International (U.K.)

- Collins Aerospace (U.S.)

- Honeywell Aerospace (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2024: Adani Airport Holdings Ltd. (AAHL) awarded Thales group a contract to design, integrate, and implement a new cloud-based APOC platform across all of its airports.

- September 2024: The SITA Airport Management solution will be implemented at Manaus Airport, Porto Velho Airport, Rio Branco Airport, Boa Vista Airport, Cruzeiro do Sul Airport, Tabatinga Airport, and Tefé Airport by Amazon Airport Concessionaire, which runs seven airports as part of the VINCI Airports Network.

- April 2025: Veovo and Gatwick Airport collaborate to create Integrated Airport Control, an AOP for integrated, predictive maintenance and decision-making throughout the airport.

- June 2025: In order to optimize the management of its ground operations and the rotation of aircraft prior to takeoff, Indra has entered into a strategic partnership with Finnish airport company Finavia to implement its A-CDM/i-AOP (airport collaborative decision-making/initial airport operations plan) system at Helsinki Airport, Finland's main airport.

- July 2023: SITA's Airport Management Systems has been chosen by Noida International Airport (NIA) to assist in automating and streamlining airport operations. With an emphasis on optimizing efficiency to both travelers and airlines, SITA's AMS will assist NIA's integrated approach to airport operations.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.38% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Deployment Mode, Airport Operational Profile, Offering Type, End User, and Region |

|

By Deployment Mode |

· Cloud/SaaS AOCC · Hybrid AOCC · On-premise AOCC |

|

By Airport Operational Profile |

· International transfer hub · Domestic hub · Cargo-heavy/integrator node · others |

|

By Offering Type |

· Platform license (perpetual/term) · Modular software subscriptions · Managed AOCC · Systems integration & migration services · Continuous improvement/analytics-as-a-service |

|

By End User |

· Airport authority-led · Privatized airport operator · PPP / concession operator · Airport group (multi-airport rollouts) |

|

By Region |

· North America (By Deployment Mode, Airport Operational Profile, Offering Type, End User, and Country) o U.S. (End User) o Canada (End User) · Europe (By Deployment Mode, Airport Operational Profile, Offering Type, End User, and Country/Sub-region) o U.K. (End User) o Germany (End User) o France (End User) o Russia (End User) o Rest of Europe (End User) · Asia Pacific (By Deployment Mode, Airport Operational Profile, Offering Type, End User, and Country/Sub-region) o China (End User) o India (End User) o Japan (End User) o South Korea (End User) o Rest of Asia Pacific (End User) · Rest of the World (By Deployment Mode, Airport Operational Profile, Offering Type, End User, and Country/Sub-region) o Middle East & Africa (End User) o Latin America (End User) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1646.5 million in 2025 and is projected to reach USD 4050.6 million by 2034.

In 2025, the market value stood at USD 648.3million.

The market is expected to exhibit a CAGR of 10.38% during the forecast period.

By deployment mode, the cloud/SaaS AOCC segment is expected to dominate the market.

The rise in real time coordination to handle air traffic is anticipated to drive the market growth.

Thales Group, Collins Aerospace, and Indra Avitech, SITA are few major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us