Amino Resins Market Size, Share & Industry Analysis, By Type (Urea Formaldehyde (UF), Melamine Formaldehyde (MF), Melamine Urea Formaldehyde (MUF), and Others), By Application (Wood Panels & Engineered Wood, Paper Impregnation & Laminates, Coatings, Molding Compounds, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

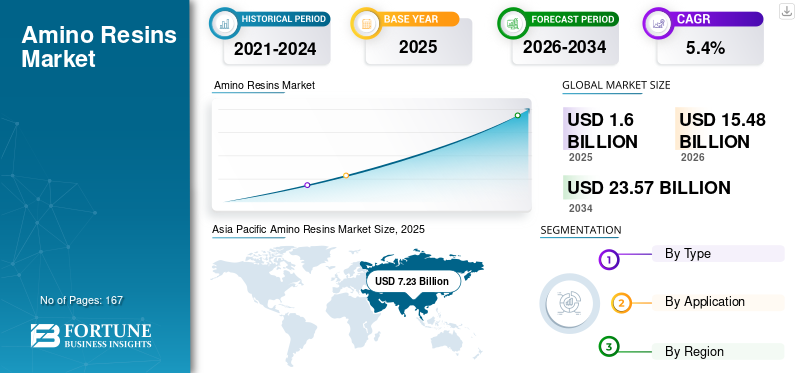

The global Amino Resins market size was valued at USD 14.69 billion in 2025. The market is projected to grow from USD 15.48 billion in 2026 to USD 23.57 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. Asia Pacific dominated the global market with a market share of 49.21% in 2025.

Amino resins are thermosetting polymers primarily derived from the reaction of formaldehyde with urea, melamine, or a combination of both. They are widely used due to their strong adhesive performance, hardness, surface durability, and chemical resistance, making them essential in various applications, including wood-based panels, decorative laminates, coatings, molding compounds, and paper impregnation. Their ability to deliver cost-effective bonding strength and surface quality continues to support the large-scale adoption of their products across the construction, furniture, and industrial manufacturing sectors. As global demand for engineered wood products, durable coatings, and decorative surfaces expands, amino resins remain a foundational material within these value chains.

The market is shaped by established chemical producers with strong capabilities in resin formulation, large-scale polymerization, and the development of downstream applications. Key players include BASF, Hexion, Dynea, DIC Corporation, and OCI Global, whose portfolios cover urea formaldehyde, melamine formaldehyde, melamine urea formaldehyde, and specialty amino resin grades. Their continued investment in low-emission formulations, improved curing efficiency, and application-specific performance reinforces their competitive positioning across global end-use industries.

Download Free sample to learn more about this report.

AMINO RESINS MARKET TRENDS

Rising Shift Toward Low-Emission and Enhanced-Performance Resin Leads to Market Trends

Producers are increasingly focused on developing low-formaldehyde and ultra-low emission resins to comply with tightening environmental and indoor air quality regulations. These advancements support sustained use in wood panels, laminates, and coatings while maintaining mechanical performance and cost efficiency. In engineered wood and decorative applications, modified resins are gaining preference due to their improved moisture resistance, enhanced surface finish, and compatibility with modern manufacturing processes.

- Global formaldehyde emission standards for wood-based panels continue to influence resin formulation strategies, reinforcing demand for compliant amino resin systems.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Demand for Engineered Wood and Decorative Surfaces Drives Market Growth

The construction, furniture, and interior fit-out industries continue to increase their consumption of particleboard, MDF, plywood, and laminates, thereby directly strengthening demand for amino resins. These resins provide the bonding strength, rigidity, and surface quality required for high-volume panel production. As urbanization accelerates and residential and commercial construction activities expand, especially in the Asia Pacific, such resins remain integral to engineered wood manufacturing. Growth in global furniture production and wood panel manufacturing capacity directly drives the global amino resins market growth during the forecast period.

MARKET RESTRAINTS

Formaldehyde Emission Concerns and Regulatory Pressure Limit Market Expansion

Despite performance advantages, such resins face challenges related to formaldehyde emissions and evolving environmental regulations. Compliance with stringent emission standards increases formulation complexity and production costs. In some applications, alternative binder systems are being evaluated, particularly where sustainability considerations outweigh cost and performance benefits. Governments and environmental agencies worldwide, such as the U.S. Environmental Protection Agency (EPA) and the European Union (through REACH regulations), have imposed strict limits on formaldehyde emissions in consumer products, including furniture, flooring, and insulation. Therefore, concerns about formaldehyde emissions and regulatory pressure may limit market expansion.

- The International Agency for Research on Cancer (IARC) has classified formaldehyde as a Group 1 human carcinogen, providing the scientific basis for these regulations.

MARKET OPPORTUNITIES

Increasing Demand for Decorative Laminates and Surface Finishes To Create Lucrative Opportunities

Ongoing innovation in melamine-based and modified amino resin systems is creating opportunities in higher-value applications such as premium laminates, industrial coatings, and specialty molding compounds. Improved resin efficiency, faster curing, and enhanced moisture resistance enable manufacturers to meet both performance and environmental requirements, supporting a gradual expansion of the market beyond traditional uses. In decorative surfaces and laminates for countertops, flooring, and cabinetry, melamine-formaldehyde resins offer high hardness, scratch resistance, chemical resistance, and an appealing finish. This growing consumer desire for durable and aesthetically pleasing interior décor directly increases the demand for these resins.

Segmentation Analysis

By Type

Urea Formaldehyde Segment Leads Due to Cost Efficiency and Large-Scale Panel Production

Based on type, the market is segmented into urea formaldehyde (UF), melamine formaldehyde (MF), melamine urea formaldehyde (MUF), and others.

To know how our report can help streamline your business, Speak to Analyst

The urea formaldehyde segment accounted for the largest amino resins market share in 2025, supported by its widespread use in particleboard and MDF manufacturing. UF resins offer an optimal balance between bonding strength and cost efficiency, making them the preferred choice for high-volume wood panel applications. Their dominance is reinforced by extensive use in furniture, flooring substrates, and interior construction materials. Hence, UF resins remain the primary binder system for cost-sensitive engineered wood products worldwide.

The melamine urea formaldehyde segment is the fastest-growing at a CAGR of 5.5%, driven by rising demand for enhanced moisture resistance and durability in exterior-grade and premium interior panels. MUF resins bridge the performance gap between UF and MF systems, supporting accelerated adoption across laminates and higher-performance wood products. Melamine adds hardness, chemical resistance, and thermal stability compared to standard Urea-Formaldehyde (UF), making it ideal for high-quality surfaces and demanding applications.

By Application

Wood Panels & Engineered Wood Dominate Due to Structural Performance For Large-Scale Panel Manufacturing

Based on application, the market is segmented into wood panels & engineered wood, paper impregnation & laminates, coatings, molding compounds, and others.

The wood panels & engineered wood segment accounted for the largest share in 2025, driven by the extensive use of such resins in particleboard, MDF, plywood, and other composite wood products. These resins, particularly urea formaldehyde and melamine urea formaldehyde, provide the bonding strength, rigidity, and surface uniformity required for large-scale panel manufacturing. Their fast-curing characteristics and compatibility with high-speed pressing lines make them indispensable for high-volume production of furniture and construction materials.

- The global expansion of MDF and particleboard production capacity will continue to drive demand for amino resins in engineered wood applications.

The paper impregnation & laminates segment represents a significant CAGR of 6.4% and a steadily growing application area for these resins. These resins are widely used to impregnate decorative and overlay papers, which are then used in laminates for flooring, furniture surfaces, wall panels, and countertops. Melamine formaldehyde and melamine urea formaldehyde resins are particularly valued in this segment for their surface hardness, scratch resistance, and aesthetic durability.

Amino Resins Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Amino Resins Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 7.23 billion, and is expected to maintain the leading share in 2026, with USD 7.66 billion. The region’s dominance is underpinned by its extensive manufacturing base for wood panels, furniture, laminates, and construction materials. Rapid urbanization, population growth, and ongoing residential and commercial infrastructure development continue to drive strong demand for engineered wood products, particularly in China, Southeast Asia, and India.

China Amino Resins Market

Based on Asia Pacific’s strong contribution and China’s manufacturing strength, the China market is recorded at USD 3.91 billion in 2025, accounting for roughly 27% of global revenues.

India Amino Resins Market

The Indian market in 2025 secured USD 0.79 billion. The nation’s growth is supported by growing demand for high-quality engineered wood products, laminates, and specialty coatings.

North America

North America remains a significant regional market, reaching USD 2.37 billion in 2025. North America remains a significant regional market, supported by stable construction activity, remodeling demand, and consistent furniture production. The region benefits from established wood panel manufacturing infrastructure and strong enforcement of indoor air quality and emission standards. These factors encourage the adoption of low-emission and compliant amino resin systems, particularly in residential and commercial building materials.

U.S. Amino Resins Market

The U.S. market in 2025 is estimated at USD 2.04 billion, accounting for approximately 14% of global revenues.

Europe

Europe is projected to experience a growth rate of 4.6% in the coming years, reaching a valuation of USD 3.72 billion by 2025. Europe represents a mature but regulation-driven market for amino resins. Stringent environmental policies and formaldehyde emission limits have a significant influence on resin formulation and application practices. As a result, demand is shifting increasingly toward melamine-modified and ultra-low-emission resin systems, particularly in applications such as furniture, flooring, and decorative surfaces.

Germany Amino Resins Market

The Germany market reached USD 0.93 billion in 2025, equivalent to around 6% of global revenues. Germany leads in technological innovation for formaldehyde reduction, aligning with global sustainability goals and boosting market growth through advanced solutions.

U.K. Amino Resins Market

The U.K. market in 2025 recorded USD 0.54 billion, accounting for roughly ~3% of global revenues. This growth is supported by expanding demand from the construction and automotive industries for applications such as adhesives and coatings.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth during the forecast period. The Latin America market reached a valuation of USD 0.74 billion in 2025, supported by expanding residential construction, gradual industrialization, and rising furniture production, which in turn supports the increasing use of engineered wood products. Brazil and Mexico remain key contributors to regional demand.

In the Middle East & Africa, amino resin consumption is supported by construction activity, interior fit-out projects, and the growing adoption of engineered wood materials in residential and commercial buildings. The Middle East & Africa market reached USD 0.62 billion in 2025.

Brazil Amino Resins Market

The Brazilian market reached around USD 0.32 billion in 2025, accounting for roughly 2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Process Efficiency and Low-Emission Innovation Define Competitive Positioning

The global market for amino resins is shaped by manufacturers with strong formulation expertise, large-scale production capabilities, and close alignment with downstream wood-based panels and laminate producers. Competitive differentiation is increasingly focusing on emission reduction, curing efficiency, and application-specific performance, rather than volume alone. Key players, including BASF, Hexion, Dynea, Prefere Resins, and Aica Kogyo, maintain strong positions through diversified product portfolios and long-term customer relationships. Other participants continue to strengthen competitiveness through specialty resin development and regional capacity expansion. Across the market, innovation is centered on ultra-low emission resins, improved melamine-modified systems, and energy-efficient curing technologies. Companies that strike a balance between regulatory compliance, cost efficiency, and performance reliability continue to lead, as amino resins remain an essential ingredient in the global construction and furniture industries.

LIST OF KEY AMINO RESINS COMPANIES PROFILED

- Allnex GMBH (Germany)

- Arclin, Inc. (USA)

- BASF SE (Germany)

- Chang Chun Group (China)

- DIC Corporation (Japan)

- Dynea AS (Norway)

- Hexion Inc (U.S.)

- Neo Paints (India)

- Ningbo Inno Pharmchem Co., Ltd. (China)

- OCI Global (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- April 2023: BASF SE and SWISS KRONO Group are expanding their long-term partnership to develop more sustainable solutions and processes, including biomass-balanced amino resins. The product will have a significantly lower product carbon footprint (PCF) than its conventional counterparts while maintaining its properties and qualities.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.4% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Type, Application, End-Use Industry, and Region |

|

By Type |

· Urea Formaldehyde (UF) · Melamine Formaldehyde (MF) · Melamine Urea Formaldehyde (MUF) · Others |

|

By Application |

· Wood Panels & Engineered Wood · Paper Impregnation & Laminates · Coatings · Molding Compounds · Others |

|

By Region |

· North America (By Type, By Application, and Country) o U.S. (By End-Use Industry) o Canada (By End-Use Industry) · Europe (By Type, By Application, and Country/Sub-region) o Germany (By End-Use Industry) o U.K. (By End-Use Industry) o France (By End-Use Industry) o Italy (By End-Use Industry) o Rest of Europe (By End-Use Industry) · Asia Pacific (By Type, By Application, and Country/Sub-region) o China (By End-Use Industry) o Japan (By End-Use Industry) o India (By End-Use Industry) o South Korea (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry) · Latin America (By Type, By Application, and Country/Sub-region) o Brazil (By End-Use Industry) o Mexico (By End-Use Industry) o Rest of Latin America (By End-Use Industry) · Middle East & Africa (By Type, By Application, and Country/Sub-region) o Saudi Arabia (By End-Use Industry) o South Africa (By End-Use Industry) o Rest of the Middle East & Africa (By End-Use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 14.69 Billion in 2025 and is projected to reach USD 23.57 Billion by 2034.

Recording a CAGR of 5.4%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The wood panels & engineered wood application segment led in 2025.

Asia Pacific held the highest market share in 2025.

Expanding demand for engineered wood and decorative surfaces drives market growth.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us