Waste to Energy Market Size, Share & Industry Analysis, By Technology (Thermochemical, Biochemical), By Waste Type (Municipal Solid Waste, Process Waste, Agricultural Waste, Others), By Application (Electricity, Heat) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

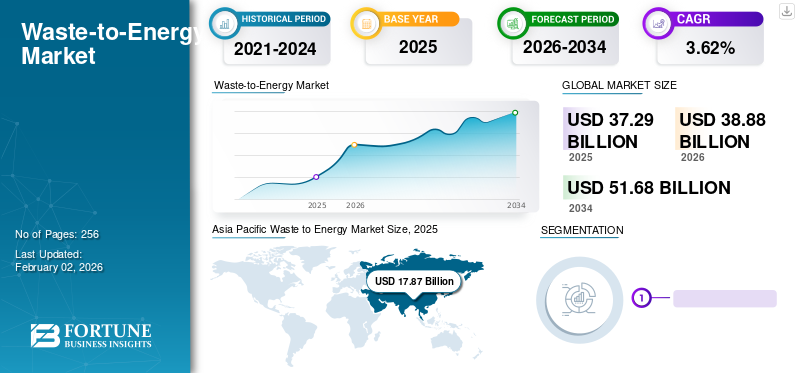

The global waste to energy market size was valued at USD 37.29 billion in 2025 and is projected to grow from USD 38.88 billion in 2026 to USD 51.68 billion by 2034, exhibiting a CAGR of 3.62% during the forecast period. Asia-Pacific dominated the waste to energy market with a market share of 48.24% in 2025. The Waste-to-energy market in the U.S. is projected to grow significantly, reaching an estimated value of USD 3.49 billion by 2032.

Waste to Energy (WtE), also known as energy from waste, uses thermochemical and biochemical technologies to recover energy from urban waste, producing electricity, steam, and fuels. These new technologies can reduce the original waste volume by 90%, depending on the composition and use of outputs. WtE plants offer two significant benefits: environmentally safe waste management and disposal and clean electric power generation. The growing use of WtE as a method to dispose of solid and liquid wastes and produce electricity has dramatically reduced the environmental impacts of municipal solid waste management, including emissions of greenhouse gases.

Download Free sample to learn more about this report.

GLOBAL WASTE TO ENERGY (WtE) MARKET OVERVIEW:

Market Size:

- 2025 Value: USD 37.29 billion

- 2026 Value: USD 38.88 billion

- 2032 Forecast Value: USD 51.68 billion, with a CAGR of 3.62% from 2026–2034

Market Share:

- Regional Leader: Asia Pacific held the 48.24% market share in 2025, driven by increasing urbanization, waste generation, and strong government initiatives, especially in countries like Japan, China, and India.

- Fastest-Growing Region: Asia Pacific remains the fastest-growing region due to economic growth, government investments in clean energy, and the circular economy trend.

- Technology Leader: Biochemical Technology led the market owing to its wide use in anaerobic digestion and biogas production—aligned with EU renewable energy goals.

- Application Leader: Electricity Generation dominated the market in 2023, fueled by rising global energy demands and efforts to reduce fossil fuel dependence.

Industry Trends:

- Digital Transformation: Adoption of smart systems like SCADA and PLC for real-time monitoring of WtE plants is enhancing efficiency and transparency.

- Sustainable Solid Waste Management: Growth of circular economy strategies, including material recovery, SRF (solid recovered fuel) production, and municipal support for bio-CNG plants.

- Public-Private Partnerships (PPPs): Increasing collaboration between governments and private players to scale WtE capacity, especially in emerging economies.

- Tech-driven Sorting & Automation: Emphasis on automated material recovery and creation of homogeneous waste streams at the source to improve feedstock quality.

Driving Factors:

- Rising Energy Demand & Urban Waste: Rapid industrialization and urban sprawl are contributing to increased municipal solid waste, pushing for energy recovery solutions.

- Government Incentives & Clean Energy Goals: Policy support, such as EU's 32% renewable energy target by 2030, and India’s bio-CNG missions, are fueling investments.

- Environmental Benefits & GHG Reduction: WtE is emerging as a dual solution for waste disposal and GHG mitigation, offering a cleaner alternative to landfilling.

- Increasing Adoption in Industrial & Agri-sectors: Industries like food processing, dairy farms, and wastewater treatment are adopting WtE to lower operational costs.

- Innovation in SRF & Waste Fuels: Advanced facilities, such as Porcarelli Group’s STADLER SRF plant, are showcasing high-volume waste conversion efficiency.

The COVID-19 pandemic disrupted the global economy by halting the operations of major industries, including recycling waste and energy-generating industries. The global solid waste management system met both opportunities and threats owing to the spread of COVID-19. In response to the increasing pressure of resource consumption and environmental impact, more attention was focused on elevating the sustainability of the waste management system. For instance, the Sustainable Development Goals (SDGs) highlighted increasing the percentage of renewable energy, paying particular attention to MSW management, and reducing waste generation through recycling and re-use. Achieving those global goals relied on a sustainable-developing solid waste industry, such as the Waste-to-energy (WtE), Waste to Material (WTM), and other waste disposal industries.

Waste to Energy Market Trends

Digitalization in Waste Management Techniques to Spur Market Opportunities

Strict government policies related to rising greenhouse gas emissions result in the innovation of green technology to develop clean energy. Governments worldwide are investing in renewable energy sources to reduce dependence on fossil fuels, complementing the adoption of WtE technologies. In addition, favorable incentives and programs have been introduced in all regions to promote effective waste collection and processing, creating significant growth potential for the waste to energy industry as it could help initiate appropriate technology for producing energy. For example, the creation of sorted, homogeneous streams of waste at the source is the gold standard of best practice. This creates opportunities for distributed recycling and upcycling activities.

Subsequently, digitization of waste collection and trading of these sorted materials allows for greater community participation in the waste collection. For example, the waste management facilities with a Programmable Logic Controller (PLC) and Supervisory Control and Data Acquisition (SCADA) monitoring system can be automatically monitored and operated from a centralized control station to ensure efficiency and minimum manual operation. Thereby, the adoption of digital technologies in waste collection and disposal operations will not only provide information but will also improve data quality and better insights into a waste stream during processes.

Download Free sample to learn more about this report.

Waste to Energy Market Growth Factors

Increase in Production of Clean Energy from Waste Drives Market Growth

The increasing industrialization and urbanization, accompanied by economic growth, results in waste generation, environmental threats, and carbon dioxide (CO2) emissions. The commercial and residential waste era has also increased significantly, with global changes in people's life patterns. Waste to energy has a role to play in achieving the transformation to a sustainable energy ecosystem acting as an energy source to reduce greenhouse gas (GHG) emissions, a clean demand response option, a design consideration of eco-industrial parks, and sometimes the only option for end-of-life waste treatment.

Additionally, the continuously rising demand for energy globally due to the increasing population and rapid industrialization and urbanization is one of the critical drivers of the global market. For example, per the Asian development bank WtE circular research report, the amount of waste produced from municipal waste is projected to reach 3.4 billion tons by 2050 due to economic development, population growth, and urbanization. Thereby, significant investment in project processes is being initiated to reduce environmental concerns and waste, providing growth opportunities for the waste to energy industry. For example, in July 2022, Hanoi, the Capital of Vietnam, aimed to recycle at least 80 percent of household solid waste into power by 2025. The city has received six project proposals with a total handling capacity of about 10,500 tons of waste.

Increasing Application of Waste Management Services to Fuel Market Growth

Waste management is still one of the key challenges across major developing countries. Over a billion tons of waste is generated from agriculture, municipal, and industrial activities. Multiple industries around the globe are focusing on reducing energy consumption to reduce cost by adopting WtE techniques. Waste to energy techniques, such as thermochemicals, can help end-users to alter waste management in an earnings opportunity for multiple applications such as food processing, dairy farms, and wastewater treatment. The processes involve converting liquid and solid waste into syngas by chemical reaction. Subsequently, the syngas or synthesis gas can be turned into electricity, gas fuel, and other valuable products

Through such a process, the solid waste generated is no longer unavailable as they are used as feedstocks for gasifiers and converted into valuable electricity and heat, thus, reducing the cost of disposal and landfilling space. In addition, heating activity in various dairy farms accounts for approximately 40% of the electricity consumption. Thereby, the enchantment of efficient systems such as electricity production from waste is likely to propel waste growth in the energy market in the forecast period.

In July 2022, Porcarelli Group’s STADLER designed, developed, and installed an innovative plant for Eco.Ge.Ri is used to produce SRF (solid recovered fuel) from industrial waste. The plant is one of Europe's most innovative technology-based plants, which is responsible for diverting around 150,000 tons of non-recyclable waste from landfills annually.

RESTRAINING FACTORS

WtE Remains a Costly Option for Waste Disposal and Energy Generation over Other Services

Governments worldwide are increasingly adopting better municipal solid waste management practices, which include treating waste with various WtE technologies as one of the most viable options for disposing of MSW and energy generation. Multiple factors influence the choice of WtE technology, and every region needs to have a specific context for implementing the most reasonable solutions. This has resulted in the WtE sector being very complex and fragmented in policies and regulations with substantial untapped potential.

Furthermore, WtE is often considered a costly option for waste disposal and energy generation compared to other fossil fuel-powered alternatives. There is a disconnect as the environmental and social benefits of WtE are not valued in comparison with established renewable alternatives such as wind and solar energy. Furthermore, energy generation from waste suffers from the limited availability of resources. Thus, the power generation capacity gets hampered compared to other conventional energy resources, due to which specific considerations such as availability and a steady supply of raw materials, choice of technology, and suitable regulatory framework conditions, among others, should be given additional consideration in the market development.

Waste to Energy Market Segmentation Analysis

By Technology Analysis

Biochemical to Hold Dominant Market Share Due to Crucial Role in Reducing Waste

Based on technology, the market is divided into biochemical and thermochemical. In biochemical technology, the anaerobic digestion technology has wide acceptance for biogas production. The growing trend of electricity production through biomass will likely result in the dominance of biochemical technology in the global waste to energy market share. In June 2018, the EU institutions agreed on a new Renewable Energy Directive for the next decade, including a legally-binding EU-wide target of 32% for renewable energy by 2030, in which the biogas sector will undoubtedly contribute to achieving this goal.

Furthermore, in thermochemical technology, incineration holds a significant share of WtE technology compared to other thermochemical technology such as thermal technology. This trend will likely continue owing to relatively low technology costs, market maturity, and high efficiency of about 25%. In addition, incineration is suitable in urban and rural areas and takes in all types of waste.

By Waste Type Analysis

Municipal Solid Waste Dominates Market Due to Increasing Consumption of Goods

Based on waste type, the market is segmented into municipal solid waste, process waste, agricultural waste, and others.

Municipal solid waste segment will account for 49.48% market share in 2026, offices, shops, schools, hospitals, hotels, and other institutions. In addition, process waste is produced mainly due to industrial activities and has surged over time due to rise in industrial activities. However, government entities such as the U.S. Environmental Protection Agency (EPA) have set up a framework that focuses on re-using the waste produced as raw material, which is likely to promote the re-use of waste produced from industrial processes.

Furthermore, agricultural waste also holds a significant share of the WtE conversion due to its considerable adoption in the gasification and pyrolysis process. In the waste to energy market forecast timeframe, the increase in waste from residues and agricultural production will likely drive the waste to energy market growth from agricultural waste. Other waste types, such as manure waste, waste from silts, pesticides, herbicides, and so on are also adopted for energy conversion.

To know how our report can help streamline your business, Speak to Analyst

By Application Analysis

High Electricity Production from Waste Results in Dominating Share of Electricity Application

Based on application, the market is bifurcated into electricity and heat. Increasing electricity from clean energy sources to reduce the dependency on fossil fuels and reduce CO2 emission results in high electricity output from waste sources.

The generation of usable heat from waste is widely used for various heating purposes across residential and industrial areas and also holds a significant market share. The generation of heat as a byproduct of energy from waste with additional earnings results in the remarkable growth of WtE for heat generation applications.

REGIONAL INSIGHT

The market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Waste to Energy Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The market in Asia Pacific reached USD 17.87 billion in 2025, representing 48.24% of total market revenue, and is projected to reach USD 18.76 billion in 2026, resulting in increased waste production. Furthermore, various governments are supporting the establishment WtE facilities, which will result in the dominating share of Asia Pacific over the forecast period. For instance, Japan has been one of the leading countries in waste-to-energy in the Asia Pacific market. Japan’s waste-to-energy market is mostly driven by highly efficient solid waste management and financial support from national and local governments in small and large-scale projects. Moreover, the country plans to introduce new waste management and recycling technologies to preserve the environment by effectively turning waste into resources. The Japan market is projected to reach USD 1.88 billion by 2026, the China market is projected to reach USD 6.6 billion by 2026, and the India market is projected to reach USD 4.81 billion by 2026.

Europe

In 2025, Europe held 39.85% of the global market, reaching a valuation of USD 14.96 billion, and is projected to grow to USD 15.49 billion in 2026. Europe has a very mature market owing to the presence of various waste to energy facilities/plants along with an increasing amount of energy generation and valuable materials for recycling from municipal solid waste. The UK market is projected to reach USD 2.5 billion by 2026, while the Germany market is projected to reach USD 4.07 billion by 2026.

North America

The North America market was valued at USD 2.8 billion in 2025, capturing 7.50% of global revenue, and is estimated to reach USD 2.92 billion in 2026. Furthermore, North America will hold a significant share of the market outlook in the forecast period due to substantial waste generation and a rising focus on managing waste. For example, according to the latest figures from the U.S. Environmental Protection Agency, the EPA’s accepted best practice to manage solid wastes sustainably mainly focuses on factors such as waste source reduction and recovery, energy recovery, treatment, and disposal, among others. The U.S. market is projected to reach USD 2.73 billion by 2026.

Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 0.49 billion, representing 1.30% of global demand, and is projected to grow to USD 0.51 billion in 2026. Moreover, countries across the Middle East & Africa and Latin America are experiencing a significant increase in waste-to-energy plants with the growing trend of a circular economy, which majorly focuses on waste management.

Latin America

Latin America maintained a strong presence in the global market, reaching USD 1.18 billion in 2025, accounting for 3.11% share, and is expected to reach USD 1.21 billion in 2026.

List of Key Companies in Waste to Energy Market

Key Participants Concentrate on Enhancing their Business Capacities

Waste to energy recovers energy from waste treatment, usually in the form of heat or electricity. The market is fragmented at the local level as many key players develop significant businesses to cater to local needs. The most prominent companies operating in this market include Veolia, China Everbright International, and Covanta.

Unsurprisingly, the global market has witnessed significant growth opportunities around the world due to the encouragement of governments, states, and local authorities to reduce pollution and landfill, majorly in developing countries, along with the search for more sustainable alternative fuel sources and associated increased public spending on WtE technologies.

For example, as part of its ESG commitment, HDFC Bank is proud to partner with Indore Clean Energy Private Limited (ICEPL) for the development of 550 tons per day of municipal solid waste (MSW) into compressed biogas (CBG) plant – the largest bio-CNG - Plant in Asia. Indore Clean Energy Pvt Ltd (ICEPL) is backed by the Green Growth Equity Fund (GGEF), India's most prominent climate protection fund, with anchor investors, including NIIF and the U.K. government.

List of Key Companies Profiled:

- Veolia (France)

- Huawei Enterprise (China)

- China Everbright Limited (China)

- Wheelabrator Technologies Inc. (New Hampshire)

- SUEZ (Paris)

- Covanta (U.S.)

- EDF (France)

- Ramboll Group (Denmark)

- AVR (Rotterdam-Botlek)

- Allseas (Switzerland)

- Attero (India)

- Viridor (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- June 2022 – AVR decided to explore the possibility of locally managing its hazardous flue gas cleaning residues by partnering with Swedish company HaloSep AB. The HaloSep operation is a distinct solution that turns hazardous waste into harmless and helpful snatches. Choosing HaloSep's solution would make AVR in Rotterdam more circular by recovering material resources and reducing the plant's environmental footprint.

- June 2022 – Veolia tendered the sales of Suez's U.K. waste business segment and continues to build the global pioneer of ecological transformation. The project focuses on ecological change by bringing together Veolia and most of Suez's international activities. The merger has already proved to help add new skills, technologies, and regions. Additionally, it will speed up the execution of the strategic program Impact 2023, strengthen Veolia's international presence, and increase invocation capacity.

- April 2022 - Veolia announced that it would initiate two new projects for developing local, sustainable and low-carbon energy sources. In Finland, the company is launching the world's largest bio refinery project producing CO2-neutral bio-methanol from the pulp manufacturing process. Secondly, the Group is partnering with Waga Energy to commission the largest biomethane production unit to recover biogas from a non-hazardous landfill in France.

- April 2022 - Viridor announced the sale of its landfill and landfill gas business to Frank Solutions Limited. The deal involves the operation and management of 44 sites across the U.K. The deal will enable Viridor to continue delivering the strategy of growing its core business areas of energy recovery and polymer reprocessing while pushing ahead with its plans to be net zero by 2040.

- January 2022 - AVR – Duiven WtE Plant is a 30MW biopower project developed in multiple phases and is set to generate 263GWh electricity, offsetting 400,000t of CO2 emissions per year.

REPORT COVERAGE

The research report comprehensively assesses the global market by offering valuable insights, industry-related information, and historical data. Several methodologies and approaches are adopted to make meaningful assumptions and views. Furthermore, the research report provides a detailed analysis and information per market segment, helping our readers get a comprehensive global industry overview.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.62% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Technology

|

|

By Waste Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

The Fortune Business Insights study shows that the global market was USD 37.29 billion in 2025.

The global market is projected to grow at a CAGR of 3.62% in the forecast period.

The market size of Asia Pacific stood at USD 17.87 billion in 2025.

Based on technology, biochemical segment holds the dominating share in the global market.

The global market size is expected to reach USD 51.68 billion by 2034.

The key market drivers are adopting clean energy and growing waste management application.

The top players in the market are Veolia, AVR, China Everbright Limited, Attero, and Viridor.

- 2021-2034

- 2025

- 2021-2024

- 256

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us