Liquid Waste Management Market Size, Share & Industry Analysis, By Source (Residential, Commercial & Industrial), By Industrial (Paper & Pulp, Chemical & Petrochemicals, Food & Beverages, Textile & Tannery and Others) and Regional Forecast, 2026-2034

Liquid Waste Management Market Size and Industry Overview

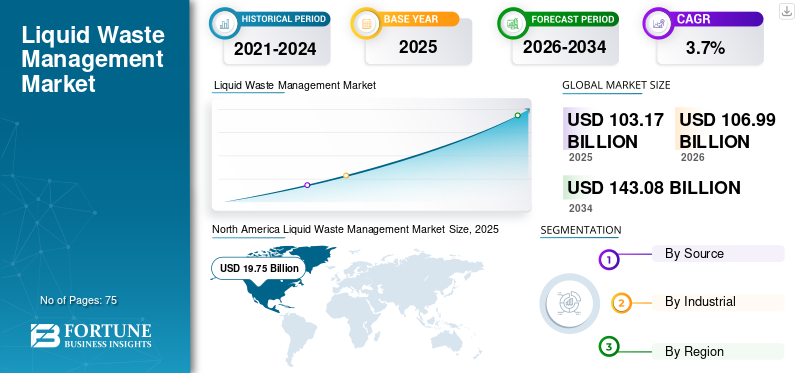

The global liquid waste management market size was valued at USD 103.17 billion in 2025. The market is projected to grow from USD 106.99 billion in 2026 to USD 143.08 billion by 2034, exhibiting a CAGR of 3.70% during the forecast period. Industry growth is driven by rising wastewater generation, stringent environmental regulations, industrial expansion, and circular economy adoption across residential, commercial, and industrial sectors. North America dominated the liquid waste management market, with a 29.96% market share in 2018. Moreover, the U.S. liquid waste management market is projected to reach USD 22.29 billion by 2026, driven by growing environmental regulations and industrial waste disposal needs.

The global liquid waste management market continues to expand in response to accelerating wastewater generation across residential, commercial, and industrial segments. The waste management market size is supported by rising urbanization, industrial output, and stricter compliance frameworks governing treatment and disposal. Current estimates indicate steady market growth through 2032, with mid-to-high single-digit expansion rates underpinned by infrastructure investments and regulatory enforcement.

Industrial sectors account for the largest share of liquid waste volumes, driven by chemical processing, food production, and energy-intensive manufacturing. Industrial effluent treatment remains capital-intensive, shaping procurement decisions and vendor selection criteria. Meanwhile, municipal systems are under pressure to upgrade aging infrastructure, particularly in developed economies.

North America dominated early adoption due to mature regulatory systems and established treatment networks. However, the Asia-Pacific region is projected to grow at a faster pace, reflecting industrial expansion and increased environmental scrutiny. China and India are key contributors, supported by public-private partnerships and capacity-building programs.

From an operational perspective, liquid waste management companies are prioritizing enhancing operational efficiency through automation, real-time monitoring, and modular treatment technologies. Cost structures remain influenced by energy usage, chemical inputs, and compliance costs. Hazardous liquid waste management represents a specialized segment with higher margins but stricter handling protocols. Increasing emphasis on circular economy principles is shifting industry focus toward resource recovery, including water reuse and energy extraction.

Despite favorable growth visibility, the market faces constraints related to infrastructure funding gaps, fragmented regulatory enforcement in emerging markets, and technological adoption barriers. Nevertheless, long-term demand fundamentals remain intact, driven by regulatory alignment and sustainability targets. The liquid waste management industry is transitioning from compliance-driven services to integrated resource management models, creating differentiated opportunities for technology providers and operators capable of delivering scalable and efficient solutions.

Download Free sample to learn more about this report.

Liquid Waste Management Market Key Takeaways

- 2025 Market Size: USD 103.17 billion

- 2026 Market Size: USD 106.99 billion

- 2034 Forecast Market Size: USD 143.08 billion

- CAGR: 3.70% from 2026–2034

- North America dominated the liquid waste management market with a 29.96% share in 2018.

- The commercial segment accounted for a 5.8% market share in 2018.

- The paper & pulp industry held a major market share in 2025.

North America

North America held the largest market share in 2025, valued at USD 19.75 billion.

Asia Pacific

Asia Pacific is projected to be the fastest-growing region during the forecast period.

Europe

Europe recorded high wastewater treatment connectivity, with Germany reaching 96% population coverage for secondary wastewater treatment systems.

U.S.

The market projected to reach USD 22.29 billion by 2026.

Japan

The market emphasizes advanced wastewater recycling, resource efficiency, and sustainable liquid waste treatment technologies.

Read More

Key Market Dynamics

Liquid Waste Management Market Trends:

Download Free sample to learn more about this report.

Liquid Waste Disposal Using Sunlight To Be The Key Market Trend

Researchers have developed an environmentally friendly and economical technology to degrade contaminated liquid waste using sunlight. This new technology is expected to significantly reduce the waste-management expenditures of several industries.

Disposal of liquid waste has always been challenging for industries, especially those operating in the manufacturing sector. The existing technologies available for waste disposal are costly, owing to which many industries do not follow the protocols for liquid waste disposal. According to the Asia Journal of Chemistry, this novel technique will be enormously efficient in the degradation of toxic chemicals generated by companies in various industries such as pharmaceuticals, textiles, paper, agrochemicals, and others.

The liquid waste management market is witnessing structural shifts aligned with sustainability and operational efficiency objectives. One prominent trend is the integration of circular economy principles into treatment processes, enabling water reuse, nutrient recovery, and energy generation from waste streams. This transition is gradually reshaping procurement criteria among industrial buyers.

Digitalization is increasingly embedded within liquid waste management systems. Operators are deploying sensor-based monitoring, predictive maintenance tools, and data analytics platforms to optimize treatment cycles and reduce downtime. These technologies are particularly relevant in large-scale industrial effluent facilities where variability in waste composition is high.

Decentralized treatment solutions are gaining traction, especially in regions with limited centralized infrastructure. Modular systems allow flexibility in scaling operations and are favored in remote industrial clusters. This trend supports faster deployment and reduces capital intensity in early-stage projects. Another observable shift is the consolidation among liquid waste management companies. Larger players are acquiring niche technology providers to strengthen their treatment portfolios and expand geographic reach. This consolidation is influencing competitive dynamics and pricing strategies.

Waste management market trends also reflect increasing regulatory convergence globally. Countries are aligning discharge standards, particularly for hazardous liquid waste, creating a more uniform compliance environment. This reduces uncertainty for multinational operators but raises entry barriers for smaller players. Sustainability reporting requirements are influencing corporate behavior. Industrial clients are increasingly evaluating waste management partners based on environmental performance metrics, not just cost. This has implications for service differentiation and long-term contract structures.

Market Growth Factors:

An increasing population & rapid urbanization lead to a higher need for liquid waste treatment

As the population is growing, the amount of liquid waste produced is rising, which further leads to the higher necessity of liquid waste treatment systems globally. According to the United Nations Report, the global population is expected to reach 8.5 billion by 2030, 9.7 billion by 2050, and surpass 11 billion by 2100. Moreover, rapid urbanization across the world is fueling the need for wastewater treatment in urban areas. According to the World Health Organization (WHO), the urban population in the world is projected to grow by 1.63% and 1.44% per year during 2020-25 and 2025-30, respectively. According to the United Nations, by 2050, over 68% of the world’s population is expected to live in urban areas.

Rising awareness about water pollution through water campaigns is boosting the market growth.

Wastewater includes a number of pollutants and contaminants such as pathogenic micro-organisms, heavy metals, plant nutrients, and organic pollutants. When improperly treated wastewater is discharged into the environment, it can cause severe damage to the aquatic ecosystem as well as to humans. For instance, eutrophication is caused by excessive nutrients received by water bodies from agricultural run-offs. According to the UN-Water Analytical brief report, eutrophication reduced the biodiversity of rivers, lakes & wetlands by one-third across the world. Therefore, to increase awareness about water pollution, both the government & private sector water companies are launching water campaigns. For instance, the ‘Love Water’ campaign was launched in U.K. in 2019. Over 40 environmental groups, water companies, charities, and regulatory authorities joined hands to raise awareness about water pollution and the importance of water in the future. Such activities are expected to boost demand for liquid waste treatment over the forecast period.

Stringent government regulations are forcing manufacturers to adopt wastewater treatment.

Government authorities such as the Environmental Protection Agency (EPA) imposed strict regulations on the discharge limits of pollutants in wastewater. For instance, the U.S. Environmental Protection Agency issued ‘Effluent Guideline’ regulations for industries under the Clean Water Act (CWA). The maximum contamination level allowed in discharge depends on industry type, and the levels have been set as per the performance of treatment systems. Violation of these guidelines or regulations leads to an environmental penalty. Environmental penalty results in case of surpassing the discharge levels, accidental or abnormal release of pollutants, and failure of discharge reporting. Therefore, manufacturers must treat & dispose of wastewater properly, which in turn is boosting the growth of the market of liquid waste management.

Market growth is fundamentally driven by rising wastewater generation across industrial sectors and expanding urban populations. Industrialization in emerging economies continues to increase the volume and complexity of liquid waste streams, necessitating advanced treatment and disposal solutions. Stringent environmental regulations remain a primary growth driver. Governments are enforcing stricter discharge norms, particularly for hazardous liquid waste, compelling industries to invest in compliant systems. Regulatory penalties and reputational risks further reinforce adoption.

Infrastructure modernization in developed markets is also contributing to growth. Aging treatment facilities require upgrades to meet current standards and improve efficiency. This creates sustained demand for retrofitting and technology integration. Another critical factor is the increasing focus on reducing environmental impact. Corporations are aligning with sustainability goals, driving investments in efficient liquid waste management systems. Water scarcity concerns are accelerating the adoption of recycling and reuse technologies, especially in water-stressed regions.

Public-private partnerships are facilitating large-scale project development, particularly in the Asia-Pacific and Latin America. These collaborations enable funding access and technical expertise, supporting market expansion. Cost optimization is influencing adoption patterns. Advanced technologies that enhance operational efficiency—such as membrane filtration and biological treatment systems—are gaining acceptance due to their long-term cost benefits despite higher upfront investment.

The expansion of sectors such as pharmaceuticals, food processing, and chemicals is directly contributing to increased demand. These industries generate complex waste streams requiring specialized treatment solutions, thereby expanding the addressable market.

Restraining Factors

The high cost of liquid waste treatment

Typically, the treatment capacity of an individual country is dependent on its income. In high-income countries, the treatment capacity is over 70% of the wastewater production as compared to 8% in low-income countries. Also, in comparison with solid waste, liquid waste is difficult to collect & process. The liquid waste easily pollutes the land or freshwater resources. Therefore, it should be handled carefully. Moreover, over the period, liquid waste treatment plants become less efficient due to a steady build-up within piping systems.

Despite favorable fundamentals, several restraints influence the pace and structure of market development. High capital expenditure requirements pose a barrier, particularly for advanced treatment technologies and large-scale facilities. Smaller municipalities and industrial operators often face budget constraints that delay system upgrades.

Despite favorable growth indicators, the liquid waste management market faces several structural constraints. High capital expenditure requirements remain a primary barrier, particularly for advanced treatment technologies. Small and medium enterprises often delay investments due to financial limitations. Operational costs are another concern. Energy consumption, chemical inputs, and maintenance expenses significantly impact profitability for operators. Volatility in input costs can affect pricing strategies and contract margins.

Fragmented regulatory enforcement in emerging markets creates inconsistencies in compliance. While regulations may exist, weak implementation reduces the urgency for industries to adopt advanced treatment systems. This limits market penetration for high-end solutions. Infrastructure gaps present additional challenges. Many regions lack adequate treatment facilities, leading to reliance on informal or inefficient disposal methods. Addressing these gaps requires long-term investment and coordinated policy efforts.

Technological complexity can also act as a restraint. Advanced liquid waste management systems require skilled personnel for operation and maintenance. Workforce shortages in certain regions hinder adoption and system performance. Hazardous liquid waste management involves stringent handling protocols and liability risks. Compliance failures can result in severe penalties, discouraging smaller operators from entering the segment.

Land availability constraints affect the establishment of large treatment facilities, particularly in urban areas. This increases project costs and delays implementation timelines. Market fragmentation, with numerous regional players, creates pricing pressure and limits standardization. Smaller companies may compete on cost rather than efficiency, impacting overall service quality.

Market Opportunities:

The rising water crisis globally is creating new opportunities for liquid waste management.

The lack of proper infrastructure and awareness about wastewater recycling resulted in the over-exploitation of freshwater resources across many countries. According to the United Nations Environment Program report, the demand for water will increase by 50% by 2030. Moreover, over 3.5 million people in Africa, Asia, and Latin America are infected with water-related diseases, and more than 0.8 million people die every year due to drinking contaminated water. Liquid waste management can effectively relieve the burden on freshwater resources and save many lives.

The liquid waste management market presents significant opportunities driven by evolving regulatory frameworks and technological advancements. One key opportunity lies in the adoption of resource recovery models. Converting waste into reusable water, energy, or by-products aligns with circular economy principles and creates additional revenue streams.

Emerging economies offer substantial growth potential due to rising industrial activity and increasing regulatory enforcement. Governments are prioritizing wastewater infrastructure, creating opportunities for both domestic and international players. Technological innovation remains a critical area of opportunity. Advanced treatment methods such as membrane bioreactors, zero-liquid discharge systems, and electrochemical processes are gaining traction. These technologies enable higher efficiency and compliance with stringent standards.

Digital solutions also present opportunities for differentiation. Real-time monitoring and data analytics can improve system performance and reduce operational costs. Companies offering integrated digital platforms are likely to gain a competitive advantage. Decentralized and modular treatment systems are particularly promising in regions with limited infrastructure. These solutions allow flexible deployment and scalability, catering to diverse industrial needs.

Partnership models, including joint ventures and public-private collaborations, are expanding. These arrangements facilitate knowledge transfer and access to funding, supporting market entry and expansion. The increasing focus on sustainability reporting is encouraging industries to invest in advanced waste management solutions. This trend is expected to drive demand for high-quality, compliant systems.

Liquid Waste Management Market Segmentation Analysis

By Source Analysis

To know how our report can help streamline your business, Speak to Analyst

The residential segment dominated the Global Liquid Waste Management Market in 2018

Based on the source, the global liquid waste management market is segmented into residential, commercial, and industrial.

Residential

The residential segment accounted for the largest revenue share in the global liquid waste management market in 2018. The segment is expected to lead the market of liquid waste management during the forecast period due to the higher production of wastewater through residential buildings. For instance, according to the Central Public Health & Environment Engineering Organization (CPHEEO) report, about 70-80% of total water supplied to domestic applications is converted to wastewater after use. The Commercial segment is expected to hold a 5.8% share in 2018.

Residential wastewater generation is primarily driven by urban population growth and expanding sanitation infrastructure. Municipal authorities are the primary operators, with increasing involvement of private liquid waste management companies through outsourcing models. Treatment systems in this segment focus on biological processes and conventional treatment technologies. However, aging infrastructure in developed regions requires modernization, while emerging markets are investing in capacity expansion.

Cost sensitivity remains a defining characteristic. Public funding constraints often delay upgrades, although regulatory pressure is gradually accelerating investment. Water reuse initiatives are gaining traction, particularly in water-scarce regions.

Commercial

Commercial liquid waste originates from office complexes, retail centers, hospitality facilities, healthcare institutions, and educational campuses. Waste characteristics vary widely depending on activity type, with healthcare and hospitality producing higher organic loads and chemical residues.

Commercial establishments, including hospitality, healthcare, and retail, generate diverse liquid waste streams. These facilities require tailored treatment solutions due to varying contaminant profiles. Healthcare facilities, in particular, contribute to hazardous liquid waste volumes. Compliance requirements are stringent, necessitating specialized treatment and disposal systems.

Commercial operators increasingly prefer decentralized liquid waste management systems. These systems enable on-site treatment, reducing dependency on municipal infrastructure and improving operational control. Service contracts in this segment are often structured around performance metrics, with an emphasis on enhancing operational efficiency and minimizing downtime.

Industrial

Industrial liquid waste constitutes the most complex and value-intensive segment. Effluents often contain hazardous chemicals, heavy metals, high biological oxygen demand, and variable pH levels. Treatment requires specialized processes, continuous monitoring, and strict adherence to sector-specific regulations.

The industrial segment accounts for the largest share of the liquid waste management market. Industrial effluent is complex, often containing toxic, organic, and inorganic contaminants requiring advanced treatment technologies. Industries are investing in integrated systems that combine physical, chemical, and biological processes. Zero-liquid discharge systems are gaining adoption in water-intensive sectors.

Regulatory compliance is a major driver in this segment. Stringent environmental regulations compel industries to adopt high-performance treatment systems. Non-compliance risks include financial penalties and operational shutdowns. Industrial clients prioritize reliability, scalability, and cost efficiency when selecting liquid waste management companies. Long-term contracts are common, providing stable revenue streams for service providers.

By Industrial Analysis

The industrial segment is further subdivided into paper & pulp, chemical & petrochemicals, food & beverages, textile & tannery, and others.

Paper & Pulp

The paper and pulp industry generates large volumes of organic-rich wastewater containing lignin, suspended solids, and chemical additives. Treatment emphasizes biological processing, sedimentation, and sludge management. Water reuse initiatives gain traction due to high consumption intensity.

In 2025, the paper & pulp industry held a major market share in the global liquid market, followed by the chemical & petrochemical industry. The amount of waste generated in the paper & pulp industry is high compared to other industries. In the food & beverage industry, alcohol refineries, sugar manufacturing & meat processing industries are the largest sources of wastewater generation.

This sector generates high volumes of wastewater with significant organic content. Treatment processes focus on reducing biological oxygen demand and removing suspended solids. Water reuse is increasingly adopted to reduce freshwater consumption. Companies are investing in advanced filtration and biological treatment systems to improve efficiency. Operational costs are influenced by energy consumption and chemical usage. Efficiency improvements are critical for maintaining profitability.

Chemical & Petrochemicals

Chemical and petrochemical facilities produce highly variable and often hazardous liquid waste streams. Effluents may contain solvents, acids, heavy metals, and toxic by-products requiring advanced treatment methods such as chemical neutralization, membrane filtration, and thermal processing.

The chemical and petrochemical sector produces hazardous liquid waste with complex compositions. Treatment requires advanced technologies, including chemical oxidation and membrane filtration. Regulatory scrutiny is high due to environmental risks. Companies are investing in robust compliance systems to manage liabilities.

This segment offers higher margins for service providers due to the complexity of treatment processes. However, it also involves higher operational risks.

Food & Beverages

The food and beverages sector generates wastewater with high organic load, fats, oils, and greases. Treatment focuses on biological digestion, separation technologies, and odor control. Seasonal production cycles influence waste volume variability. Sustainability considerations strongly influence procurement decisions. Companies seek waste-to-energy solutions, biogas recovery, and water reuse to align with corporate environmental goals. Providers offering integrated sustainability outcomes secure preferred supplier status.

Wastewater from this sector is rich in organic matter. Treatment focuses on biological processes and anaerobic digestion, which can also generate energy. Sustainability initiatives are driving the adoption of resource recovery systems. Companies are exploring ways to convert waste into biogas and reusable water. Seasonal production patterns influence wastewater generation, requiring flexible treatment systems.

Textile & Tannery

Textile and tannery operations produce chemically intensive effluents containing dyes, salts, chromium, and finishing agents. Treatment complexity is high, requiring multi-stage processing and strict discharge compliance.

This segment is characterized by high levels of chemical pollutants, including dyes and heavy metals. Treatment processes are complex and require multiple stages. Regulatory enforcement varies by region, affecting adoption rates. In regions with strict regulations, companies are investing in advanced treatment systems. Cost considerations remain significant, particularly for small-scale operators. This influences technology adoption and service provider selection.

Others

Other industrial sectors, including pharmaceuticals, mining, and power generation, contribute to the liquid waste management market. Each sector presents unique challenges in terms of waste composition and treatment requirements. Pharmaceutical waste often contains active compounds requiring specialized treatment. Mining operations generate wastewater with heavy metals, necessitating advanced filtration systems.

REGIONAL ANALYSIS

North America Liquid Waste Management Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America Liquid Waste Management Market Analysis:

North America held the largest market share in the global liquid waste management market in 2025, followed by the Asia Pacific. The region is expected to lead the market during the forecast period. In North America, the U.S. is a prime market for liquid waste management. In the region, over 95% of wastewater collected is treated and then recycled. Moreover, five of the biggest wastewater treatment plants are established in the U.S. For instance, Chicago & Boston have wastewater treatment plants with a capacity of 1.44 billion gallons per day and 1.27 billion gallons per day, respectively. North America witnessed a growth from USD 19.37 billion in 2017 to USD 19.75 billion in 2018.

North America dominated early adoption of advanced liquid waste management systems, supported by stringent environmental regulations and established infrastructure. The region demonstrates stable market growth driven by infrastructure upgrades and sustainability initiatives. Industrial sectors continue to invest in efficient treatment and disposal solutions. Technological adoption remains high, particularly in digital monitoring and automation, enhancing operational efficiency and compliance across residential, commercial, and industrial applications.

United States Liquid Waste Management Market:

The United States represents the largest share within North America, driven by strict regulatory enforcement and high wastewater generation. Industrial effluent treatment is a key focus area, particularly in the chemicals and energy sectors. Investment in infrastructure modernization supports market expansion. Liquid waste management companies are increasingly adopting digital tools to optimize operations and reduce costs, aligning with broader sustainability and environmental compliance objectives.

Asia-Pacific Liquid Waste Management Market Analysis:

Asia Pacific is projected to be the fastest-growing region in the global market of liquid waste management during the forecast period. Increasing population in emerging economies such as China and India, backed by the favorable growth of the industrial sector in the region, are the key factors driving the liquid waste management market growth. Moreover, increasing use of water by highly populous countries is expected to increase the need for liquid waste treatment and recycling to meet the water requirements in the future. According to the Central Pollution Control Board's estimation, India’s water demand is expected to rise to 1.5 trillion cubic meters by 2030.

Asia-Pacific is projected to grow at the fastest rate, driven by industrial expansion and rising wastewater generation. Governments are strengthening environmental regulations and increasing demand for advanced treatment solutions. Infrastructure development remains a priority, supported by public-private partnerships. The region presents significant opportunities for liquid waste management companies, particularly in decentralized systems and scalable technologies tailored to diverse industrial needs.

Japan Liquid Waste Management Market:

Japan’s market emphasizes technological sophistication and resource efficiency. Advanced liquid waste management systems are widely adopted, particularly in industrial sectors. The country focuses on water reuse and energy recovery, aligning with sustainability objectives. Aging infrastructure requires modernization, creating opportunities for technology providers. Regulatory compliance remains stringent, supporting steady demand for high-performance treatment solutions.

China Liquid Waste Management Market:

China’s liquid waste management market is expanding rapidly due to industrial growth and stricter environmental enforcement. Government initiatives are driving investment in treatment infrastructure and advanced technologies. Industrial effluent management is a key focus area, particularly in heavy industries. The market is characterized by large-scale projects and increasing participation of private operators, supporting long-term market growth.

Europe Liquid Waste Management Market Analysis:

Europe is a well-established market for liquid waste management. In most European countries, the percentage of the population connected to wastewater treatment systems is high. For instance, according to Eurostat, in 2016, 96% of the population in Germany was connected to at least one secondary urban wastewater treatment system.

Europe’s liquid waste management market is shaped by comprehensive regulatory frameworks and strong environmental commitments. Circular economy principles are deeply integrated into treatment strategies, promoting resource recovery and reuse. Market growth is steady, supported by industrial compliance requirements and infrastructure investments. Countries are focusing on reducing environmental impact through advanced technologies, creating opportunities for innovation and cross-border collaboration among service providers.

Germany Liquid Waste Management Market:

Germany leads in technological innovation within Europe’s liquid waste management industry. Strong industrial base drives demand for advanced treatment systems, particularly in the chemical and manufacturing sectors. Regulatory compliance is strict, encouraging adoption of efficient and sustainable solutions. Companies prioritize energy-efficient processes and resource recovery, aligning with national sustainability goals and reinforcing Germany’s position as a key market contributor.

United Kingdom Liquid Waste Management Market:

The United Kingdom market is characterized by regulatory alignment and increasing focus on infrastructure resilience. Wastewater generation from urban centers drives demand for upgraded treatment systems. Industrial sectors are investing in compliance-driven solutions, particularly for hazardous liquid waste. Public-private partnerships are supporting infrastructure development, while digital technologies are enhancing monitoring and operational efficiency across treatment facilities.

Latin America Liquid Waste Management Market Analysis:

In Latin America, there is a large disparity in the levels of wastewater treatment. For instance, Chile treats over 90% of its wastewater, whereas Costa Rica treats approximately 4% of its wastewater. On average, only 50% of the population in Latin America is connected to wastewater treatment facilities. However, increasing investment in the wastewater industry is projected to create market opportunities for the growth of the market in Latin America. The Development Bank of Latin America estimated that over US$33 billion will be spent on wastewater treatment.

Latin America shows moderate growth potential, supported by urbanization and industrial development. Infrastructure gaps remain a challenge, but government initiatives are improving treatment capacity. Regulatory frameworks are evolving, encouraging the adoption of advanced solutions. Public-private partnerships are playing a critical role in project implementation, creating opportunities for international liquid waste management companies to expand their presence.

Middle East & Africa Liquid Waste Management Market Analysis:

The Middle East & Africa region, South Africa, held a significant revenue share in the liquid waste management market. In GCC, most of the countries use treated wastewater for agriculture & landscape irrigation. These countries are aiming to increase the use of recycled water to reduce water shortages in the region.

The Middle East & Africa market is driven by water scarcity and industrial expansion. Investment in wastewater treatment infrastructure is increasing, particularly in urban areas. Regulatory enforcement varies, influencing adoption rates. Opportunities exist in decentralized systems and water reuse technologies, supporting sustainable resource management and reducing environmental impact across the region.

Competitive Landscape:

The liquid waste management market is moderately consolidated, with global environmental services providers competing alongside strong regional and niche operators. Competitive positioning depends on regulatory expertise, treatment capability breadth, geographic coverage, and the ability to manage complex industrial waste streams safely and compliantly.

Large multinational companies maintain leadership through vertically integrated service portfolios covering collection, transportation, treatment, recycling, and disposal. These players benefit from long-term municipal contracts, industrial framework agreements, and strong balance sheets that support capital-intensive infrastructure. Their scale enables consistent compliance across jurisdictions and investment in advanced treatment technologies, including membrane filtration, biological processing, and thermal treatment.

The competitive landscape of the liquid waste management market is moderately fragmented, with a mix of global service providers, regional operators, and specialized technology firms. Market share distribution is influenced by geographic presence, service portfolio, and technological capabilities.

Large multinational companies dominate high-value contracts, particularly in industrial and hazardous liquid waste segments. These players leverage integrated service offerings, including collection, treatment, and disposal, to secure long-term agreements. Their scale enables investment in advanced technologies and compliance systems. Regional players maintain strong positions in local markets, benefiting from established relationships and cost advantages. However, their capabilities may be limited in handling complex industrial effluent or large-scale projects.

Niche technology providers are increasingly relevant, offering specialized solutions such as membrane filtration, biological treatment systems, and digital monitoring platforms. These companies often collaborate with larger operators to deliver comprehensive solutions. Partnerships and joint ventures are common, particularly in emerging markets. These arrangements facilitate market entry and enable the sharing of technical expertise. Public-private partnerships play a significant role in infrastructure development, especially in regions with funding constraints.

Mergers and acquisitions are shaping the competitive landscape. Larger firms are acquiring smaller players to expand service portfolios and geographic reach. This trend is expected to continue as companies seek to strengthen their market position. Operational efficiency and compliance capability are key differentiators. Clients prioritize vendors that can deliver reliable performance, meet regulatory requirements, and optimize costs. Innovation is becoming a critical competitive factor. Companies investing in digital technologies and resource recovery solutions are gaining an advantage in a market increasingly focused on sustainability and efficiency.

Liquid Waste Management Industry Key Developments:

- January 2025: Veolia Environment expanded its industrial effluent treatment portfolio by deploying advanced membrane bioreactor systems, aiming to enhance operational efficiency and support large-scale chemical sector clients with improved compliance capabilities.

- October 2024: Suez Group entered a strategic partnership with a regional infrastructure firm to develop decentralized liquid waste management systems, focusing on modular treatment technologies for emerging industrial clusters in the Asia-Pacific.

- August 2024: Clean Harbors upgraded its hazardous liquid waste processing facilities with advanced thermal treatment technologies, targeting improved handling capacity and stricter environmental compliance for industrial clients.

- May 2024: Xylem Inc. introduced a digital monitoring platform integrating real-time analytics and predictive maintenance tools, designed to optimize wastewater treatment operations and reduce lifecycle costs for municipal and industrial operators.

- March 2024: Kurita Water Industries launched a new zero-liquid discharge system incorporating advanced filtration and chemical treatment processes, aimed at reducing wastewater generation and supporting circular economy principles in manufacturing sectors.

List of Top Liquid Waste Management Companies:

- Veolia Environmental Services

- SUEZ Environment SA

- Xylem

- Evoqua Water Technologies Corporation

- Covanta Holding Corporation

- Clean Harbors, Inc.

- GFL Environmental Inc.

- Cleanaway

- Aqua America Inc.

- Hulsey Environmental Services

- Enva

- Environmental Recovery Corporation

- AB Environmental

REPORT COVERAGE

The liquid waste management market report provides both qualitative & quantitative insights into liquid waste management across the world. Quantitative insights include market sizing of liquid waste management in terms of value (US$ billion) across each segment, sub-segment, and region profiled in the scope of the study. Also, it provides waste management market share analysis and growth rates of the segment, sub-segment, and key countries across each region. Qualitative insight covers the elaborative analysis of market drivers, restraints, growth opportunities, and key trends related to liquid waste management.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Source

|

|

By Industrial

|

|

|

By Geography

|

Frequently Asked Questions

According to Fortune Business Insights, the global liquid waste management market was valued at USD 103.17 billion in 2025 and is projected to reach USD 143.08 billion by 2034, growing at a CAGR of 3.7% during the forecast period.

The market of liquid waste management is projected to grow at a CAGR of 3.7% over the forecast period.

Liquid waste management involves the collection, treatment, and disposal of non-solid waste, including sewage, greywater, industrial effluents, and contaminated liquids from households, industries, and commercial sectors to reduce pollution and ensure public health.

The chemical & petrochemical, paper & pulp, textile, food & beverage, and pharmaceutical sectors are among the largest generators of liquid waste due to their extensive use of water in production processes.

Key drivers include increasing environmental awareness, stricter government regulations, rapid industrialization, and the growing need for clean water in urban and rural areas.

North America held the largest market share in 2018 due to established infrastructure and regulatory enforcement. However, Asia Pacific is expected to witness the fastest growth owing to urbanization, population expansion, and rising environmental investments.

Common technologies include membrane filtration, biological treatment, chemical precipitation, sludge digestion, and reverse osmosis. These help in reducing contaminants and recycling water efficiently.

Leading companies in the liquid waste management industry include Veolia Environmental Services, SUEZ, Xylem Inc., Evoqua Water Technologies, Covanta, and Clean Harbors, known for innovations and sustainable waste handling solutions.

- 2021-2034

- 2025

- 2021-2024

- 75

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us