Plastic Waste Management Market Size, Share & Industry Analysis, By Source (Industrial Waste and Municipal Waste), By Material (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polystyrene and Others), By Product Type (Packaging, Construction, Automotive, Electrical & Electronics and Others), By Treatment Method (Collection, Recycling and Disposal {Landfilling & Incineration}) and Regional Forecast, 2026-2034

Plastic Waste Management Market Size and Industry Overview

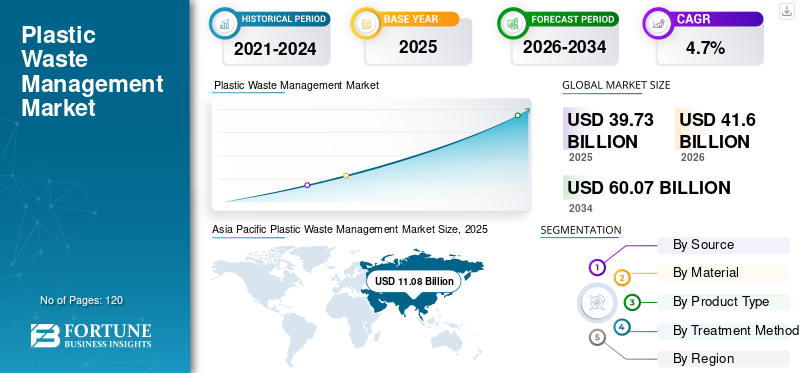

The global plastic waste management market size was valued at USD 39.73 billion in 2025. The market is projected to grow from USD 41.60 billion in 2026 to USD 60.07 billion by 2034, exhibiting a CAGR of 4.70% during the forecast period. Asia Pacific dominated the plastic waste management market with a market share of 33.67% in 2025. Moreover, the plastic waste management market in the U.S. is set to witness strong growth, reaching USD 9.01 billion by 2034. This surge is driven by rising environmental concerns, increasing plastic consumption, and strict regulations promoting recycling and sustainable waste disposal.

In general, the accumulation of used plastic objects in the environment is defined as plastic waste. Over 50% of the plastic produced around the world is used for single-serve purposes. Such plastic is non-degradable and can remain intact over a long period when discarded. Improper treatment of plastic waste results in serious environmental and human health issues. Plastic releases harmful chemicals and can easily pollute land and water resources. Marine species consume plastic trash and through the food chain, when humans consume these species, it leads to immune disorders, birth defects, or cancer. Therefore, with increasing consumption of plastic products, adoption of this waste management technique for plastics has become a necessity.

Outbreak of covid-19 has significant impact on growth of the global market. The year-on-year growth rate is estimated to decline for this year as compared to historic years due to supply chain disruption. Therefore, the market is expected to grow at lower CAGR during this year.

Download Free sample to learn more about this report.

Plastic Waste Management Market Key Takeaways

- 2025 Market Size: USD 39.73 billion

- 2026 Market Size: USD 41.60 billion

- 2034 Forecast Market Size: USD 60.07 billion

- CAGR: 4.70% from 2026–2034

- Asia Pacific dominated the plastic waste management market with a 33.67% share in 2025.

- HDPE, LDPE, and LLDPE together accounted for over 35% of the market in 2025.

- The packaging segment is projected to grow at a CAGR of 3.4% during the forecast period.

North America

North America accounted for the second-largest revenue share in the global market.

Asia Pacific

Asia Pacific accounted for the largest revenue share in the market in 2025.

Europe

Europe accounted for the third-largest revenue share in the market in 2025.

U.S.

The U.S. is one of the largest producers of plastic waste in the world.

Japan

Japan is witnessing steady growth in plastic waste management through increasing recycling and sustainability initiatives.

Read More

PLASTIC WASTE MANAGEMENT MARKET TRENDS

Download Free sample to learn more about this report.

New Innovations in Waste Treatment to Boost Market Growth

Technological innovations such as Machine Learning (ML) and big data are setting up new growth opportunities in plastic waste management. These technologies are capable of saving time as well as enable efficient resource planning. This in turn would reduce the overall cost of operation. Also, ocean plastic trash identification through satellites could point out the exact location of concentrated areas. Using such technologies, companies are saving their time & resources to collect plastic trash.

PLASTIC WASTE MANAGEMENT MARKET GROWTH FACTORS

Exciting Initiatives by Leading Players to Fuel the Market

Many leading global companies operating across the plastic value chain have joined their hands together to end plastic pollution. For instance, in January 2019, over 30 global companies established a new global ‘Alliance to End Plastic Waste’ in London to eliminate plastic pollution, especially plastic entering into oceans. This alliance has committed an investment of US$ 1.5 billion over the next five years. Moreover, it has developed a global vision and thorough strategies to tackle this issue. These strategies include four key areas such as infrastructure development, innovative technologies for plastic waste management, education & engagement at all levels of communities, and cleaning up existing concentrated plastic polluted areas. Such initiatives are encouraging the adoption of plastic waste management services to achieve the goal of eliminating plastic pollution in the future.

RESTRAINING FACTORS

High Operating Cost of Plastic Waste Management is a Key Challenge for Market Growth

Plastic waste management is a complex process and requires high capital investment to efficiently operate the various tasks, including waste collection and disposal. Moreover, it requires skilled and highly motivated laborers to process the waste. This in turn further increases the operating costs and affects profit margins. However, with increasing adoption of latest technologies, the impact of this restraint is expected to become less over the forecast period.

PLASTIC WASTE MANAGEMENT MARKET SEGMENTATION ANALYSIS

By Source Analysis

Industrial Waste Segment to Remain the Largest Plastic Waste Source in the Plastic Waste Management Market

Based on source, the market is segmented into industrial waste and municipal waste. Among these, industrial waste is the largest and fastest-growing segment in the market. Industries are considered as largest source of plastic waste. The growth of this segment is mainly attributed to the rapid industrialization in the developing economies. Due to strict environmental regulations, it is mandatory for manufacturing industries to dispose plastic waste properly. Moreover, plastic recycling is playing an important role to achieve economically and environmentally sustainable goals.

Municipal plastic waste contains plastic waste mainly generated from households & commercial estates. The growth of this segment is highly dependent on separation of plastic waste from other municipal solid waste. However, increasing population and rapid urbanization is creating lucrative opportunities for the growth of this segment over the forecast period. The World Bank estimated that municipal plastic waste accounted for 12% share in global plastic waste generation in terms of volume.

By Material Analysis

Polyethylene Segment Dominated the Global Market in 2026

Based on material, the market is categorized into polyethylene, polypropylene, polyethylene terephthalate, polystyrene, and others. Polyethylene is the largest produced and consumed polymer across the world. HDPE, LDPE, & LLDPE together accounted for over 35% share in terms of consumption, followed by polypropylene. Due to robust performance properties, polyethylene is widely adopted in different end-use industries such as packaging, construction, and electronics, among others. Therefore, increasing demand for polyethylene by these end-use industries is expected to drive the dominance of the segment in this market share. Also, the segment is projected to register higher growth rate during the forecast period.

By Product Type Analysis

Packaging Segment Held Major Share in the Global Market

Based on product type, this market is categorized into packaging, construction, automotive, electrical & electronics, and others. Among these, packaging accounted for the largest revenue share in 2026. Owing to increasing adoption of plastic for the production of packaging products, the segment is projected to be the fastest growing with a CAGR of 3.4% during the forecast period. In order to avoid increasing plastic pollution, most of the packaging manufacturers are shifting their preferences towards sustainable plastic packaging solutions. This in turn is expected to boost demand for plastic waste recycling processes during the forecast period.

By Treatment Method Analysis

To know how our report can help streamline your business, Speak to Analyst

Collection Segment to Account for the Major Market Share

Based on treatment method, the market is categorized into collection, recycling, and disposal. Among these, the collection segment accounted for the largest revenue share in the market in 2026. Collection of plastic waste is a complex process and accounts for high operating cost. The selection of optimized processes and proper use of resources play an important role in the plastic waste collection process.

Disposal segment held the second largest share in the market. The segment is further divided into landfilling and incineration. Among these, landfilling held the largest market share in 2019. Landfilling is a widely adopted plastic waste management method in many countries, except European countries. Properly landfilled plastic waste has potential to be used in recreational activities.

REGIONAL PLASTIC WASTE MANAGEMENT MARKET ANALYSIS

Asia Pacific Plastic Waste Management Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the largest revenue share in the market in 2025. Also, the region is projected to be the fastest growing at a CAGR of 4.0% during the forecast period. Increasing per capita plastic waste generation and rapid urbanization & industrialization are key driving factors boosting the need for this type of waste management for plastics in Asia Pacific. China is the largest contributor to the plastic waste generation, accounting for more than 60% share. India is expected to register fastest growth in the regional market during the forecast period. Implementation of strict environmental policies and high collection rates of plastic waste are driving the plastic waste management market growth in developed countries such as Japan, South Korea, Australia, and New Zealand. However, lack of proper collection & management and existence of ‘throw away culture’ represents key challenges for growth of the market in the developing economies of Asia Pacific.

North America accounted for the second-largest revenue share in the global market. The region is a well-established market in terms of collection & treatment. Large presence of solid waste management companies and their distribution network is the key growth factor for the North America market. Within the region, the U.S. accounted for the largest share in 2025 and the region is projected to grow at a rate of 2.4% over the forecast period. The U.S. is one of the largest producers of plastic waste in the world. Despite higher collection rates, the plastic recycling rate in the United States is less at around 9-10%.

Europe accounted for the third largest share in the market in 2025. In Europe, most of the collected plastic waste is utilized for energy generation. The adoption of the new ‘Circular Economy Action Plan’ and ‘The European Green Deal’ are projected to have significant impact on growth of this market in Europe. The European Green Deal provides a roadmap for boosting the circular economy, restoring biodiversity, and cutting down pollution. Germany held the largest market share in 2025. Owing to high per capita plastic waste generation, Germany is expected to maintain its dominance over the forecast period.

LIST OF KEY PLAYERS PROFILED IN REGIONAL PLASTIC WASTE MANAGEMENT MARKET:

- Waste Management Inc. (USA)

- SUEZ Group (France)

- Veolia Environment S.A. (France)

- Biffa PLC (U.K.)

- Clean Harbors Inc. (USA)

- Covanta Holdings Corporation (USA)

- Hitachi Zosen Corporation (Japan)

- Remondis AG & Co. Kg (Germany)

- Republic Services Inc. (USA)

- Stericycle Inc. (USA)

- ALBA Group (Germany)

- Recology (USA)

- TANA Oy (Finland)

- Envac Group (Sweden)

KEY INDUSTRY DEVELOPMENTS:

- June 2021 – Biffa plc acquired the only post-consumer plastic recycling facility of Green Circle Polymers based in Scotland. The strategic acquisition was done to achieve the goal of expanding company’s plastic recycling capability by 2030.

- May 2021 – UPS Healthcare and Stericycle entered into partnership to provide medical waste classification and disposal services. With this partnership, both companies are aiming to protect health and contribute the plastic circular economy in a responsible, safe, and sustainable way.

- December 2020 – SUEZ and LyondellBasell together acquired a Belgium based plastic recycling company named ‘TIVACO’. The acquired company will operate as a part of Quality Circular Polymers (QCP). With this acquisition, the QCP expanded its production capacity to 55 kilo tons per annum.

REPORT COVERAGE

The plastic waste management market report provides both qualitative & quantitative insights on the waste management processes and practices for plastics across the world. Quantitative insights include market sizing in terms of value (US$ Billion) across each segment, sub-segment, and region profiled in the scope of study.

Also, it provides market share analysis and growth rates of segment, sub-segment and key counties across each region. Qualitative insight covers elaborative analysis of market drivers, restraints, growth opportunities, and key trends related to the market. Competitive landscape section covers detailed company profiling of the key players operating in the plastic waste management industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Source

|

|

By Material

|

|

|

By Product Type

|

|

|

By Treatment Method

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global plastic waste management market size was valued at USD 39.73 billion in 2025 and is projected to reach USD 60.07 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period.

Growing at a CAGR of 4.7%, the market will exhibit significant growth in the forecast period (2026-2034).

The market is primarily driven by rising environmental concerns, increasing plastic consumption, and government regulations promoting recycling and sustainable disposal. Corporate initiatives and technological innovations are further accelerating adoption.

Asia Pacific dominated the market in 2025 with a 33.67% share and is expected to grow at the fastest rate. Growth is fueled by rapid industrialization, urbanization, and high plastic waste generation in countries like China and India.

The market is segmented into industrial waste and municipal waste. Industrial waste is the largest source due to strict regulatory disposal requirements and the high volume of plastic used in manufacturing.

Polyethylene is the most commonly processed plastic due to its widespread use in packaging, construction, and electronics. It accounted for over 35% of global plastic consumption in 2025.

The main treatment methods include collection, recycling, and disposal (landfilling and incineration). Among these, collection accounted for the largest share in 2025, while recycling is gaining momentum due to circular economy goals.

Leading companies are forming global alliances and investing in innovative technologies. For example, the Alliance to End Plastic Waste has pledged $1.5 billion to improve infrastructure, support cleanups, and promote education on plastic sustainability.

The key challenge is the high operational cost, including labor, technology, and infrastructure. Additionally, low recycling rates, especially in developed nations like the U.S., hinder circular economy efforts.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us