Server Operating System Market Volume, Share & Industry Analysis, By Operating System (Windows, Linux, UNIX, and Others), By Virtualization Status (Virtual Machine, Physical, and Virtualized), By Subscription Model (Non-paid Subscription and Paid Subscription), By Enterprise Type (Large Enterprises and Small & Medium Enterprises), and Regional Forecast, 2026-2034

Server Operating System Market Size

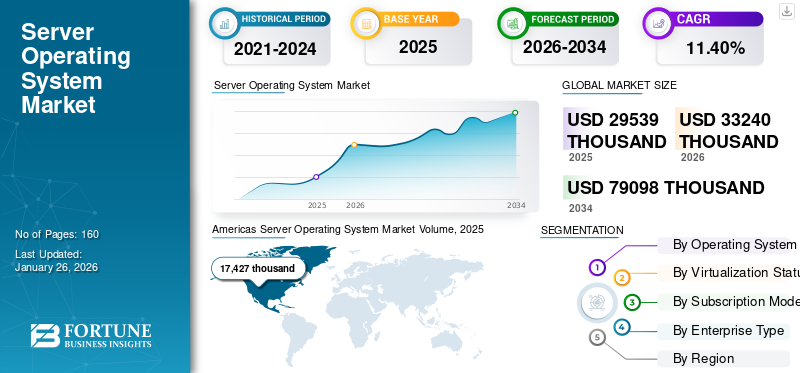

The global server operating system market volume was 29,539 thousand in 2025 and is projected to grow from 33,240 thousand in 2026 to 79098 thousand by 2034, exhibiting a CAGR of 11.40% during the forecast period. Americas dominated the global server operating system market with a share of 59.00% in 2025.

A server OS (Operating System) runs on a server in a client-server infrastructure and offers several services to client machinery over the network. It practices a software’s strength to run various applications and programs. It also provides advanced features to manage, run, monitor, and regulate applications, processes, and client devices like different servers, such as a web server, application servers, file servers, database servers, mail servers, and many more.

Key players in the market are developing advanced server-based operating systems for web servers that function in a client/server architecture to cater to the demand for computers on the network. Servers, including web, mail, file, database, application, and print, rely on operating systems to assist users with various functions. Windows Server, MacOS X Server, and Linux versions, such as Red Hat Enterprise Linux (RHEL) and SUSE Linux-based Enterprise Server OS, are popular operating systems for a wide range of applications in data centres. A server operating system assists organizations in running large programs and handling complex tasks, such as data transfers. Also, the rising adoption of cloud platforms and data centre infrastructure is driving the demand for server OS. Thus, with the rise in usage of virtual or cloud-based solutions, companies are keen on offering advanced server OS. For instance,

- November 2021 - Red Hat, Inc., an operating system solutions provider, launched an advanced version of the Linux 8.5 Red Hat Enterprises Linux platform. This Linux operating system platform offers extended functionality across data centers, clouds, and traditional data center operations. The platform enables IT teams to expand their capabilities to build transformative applications required for businesses.

The COVID-19 pandemic caused significant disruption across all industries in the global economy, which resulted in severe recessions across the world. The outbreak declined the overall end-user spending on data center infrastructure. Due to such factors, spending on global IT technology declined in the short term during the COVID-19 outbreak. This factor weakened the growth of the global server operating system market. However, the growing shift of enterprises toward cloud systems, rising work-from-home & BYOD trends, and other factors are expected to strengthen the market during the forecast period.

Download Free sample to learn more about this report.

Server Operating System Market Trends

Increasing Adoption of Hybrid Cloud Environments for Server Infrastructure to Support Market Growth

A hybrid cloud environment is a mixture of cloud-driven resources and on-premises IT architecture, where on-premises and cloud systems work collectively to accomplish an enterprise’s IT objectives to aid business processes. It offers various benefits, such as investment protection, agility & scalability with government rules and regulations, and numerous cost-saving opportunities, especially for small enterprises.

Globally, enterprises are adopting hybrid and public cloud-based applications to meet their business requirements. The rising number of cloud-based server users and the surge in enterprise spending on embracing cloud services have propelled the market growth. According to a Forbes survey, in 2020, enterprises across the world invested around USD 12 million annually in cloud services.

Many companies in the market are deploying cloud-based applications to access web-based applications to store data from a remote server with the help of software and hardware resources. According to the IDC predictions, more than 40% of enterprise applications will be deployed on cloud infrastructure by 2024. Furthermore, the increasing adoption of Linux-based operating systems, with the surge in server deployments by enterprises, is expected to boost the server operating system market share.

Server Operating System Market Growth Factors

Rising Adoption of Cloud Platform and Infrastructure to Surge Demand for Server OS

Rising adoption of cloud platforms & infrastructure and surging data center infrastructure investments by the leading players are aiding the market growth. The expansion of current advanced infrastructure is expected to boost the number of cloud server users across the globe. The key cloud computing service providers are investing a considerable amount of money in the development of cloud infrastructure around the globe. For instance,

- In February 2023, Oracle Corporation announced a new plan for public cloud in Saudi Arabia with an investment of USD 1.5 billion, considering the increasing demand for cloud services.

- In July 2021, Google LLC launched an advanced cloud infrastructure development project in India. Similarly, in the earlier year, the company invested around USD 4.5 billion in Jio Platforms to push digitization efforts in the country. In July 2021, Google LLC had around 79 cloud zones, 26 cloud regions, and 146 cloud availability points across the world.

Thus, the server operating system provides several functionalities for a data center, such as a central interface for managing multiple users, implementing security solutions, and performing other administrative processes. An increase in data center deployments across the globe, owing to a surge in the adoption of managed services, has propelled the global market share.

RESTRAINING FACTORS

High Server Downtime and Costs Related to Deployment May Hinder Market Growth

High costs related to server downtime of operating systems and deployment can hinder the market growth. According to the Information Technology Intelligence Consulting Corporation (ITIC), in 2020, downtime costs for a single server were valued at around USD 100,000 for one hour of downtime that was relatively expensive. However, the server downtime cost was valued at USD 1,670 per minute/per server. Also, around 88% of the respondents’ calculated one-hour downtime costs for the companies is USD 301,000 or more. Such a high cost of server downtime might hinder the server OS market growth.

Download Free sample to learn more about this report.

Server Operating System Market Segmentation Analysis

By Operating System Analysis

Linux Segment Captured Largest Market Share Owing to Diverse Product Advantages

By operating system, the market is divided into Windows, Linux, UNIX, and others.

The Linux segment is projected to dominate the market with a share of 63.73% in 2026. This high demand is owing to the product’s advantages, including open source, low cost, strong performance, compatibility, and security. Further, the Windows segment is anticipated to grow at a significant rate owing to advanced multi-layer security and modernization of workloads on Azure on cloud and on-premises.

UNIX and other segments are expected to demonstrate a significant growth rate during the forecast years as they provide multitasking and multi-user capabilities. UNIX is an extensively used operating system across computing mobile devices, including desktop operating systems, netbooks, and server systems.

To know how our report can help streamline your business, Speak to Analyst

By Virtualization Status Analysis

Enhanced Flexible Capabilities of Virtual Machine Analytics to Drive Market Growth

Based on virtualization status, the market for server operating systems is divided into virtual machine, physical, and virtualized.

The virtual machine segment is expected to lead the market, contributing 64.74% globally in 2026 and is projected to register a leading CAGR during the forecast period as the primary goal of Virtual Machines (VMs) is to run an operating system from the same hardware. At the same time, virtual machine analytics are most preferred by the enterprises. Without virtualization, running several OS, such as Linux Kernel and Windows, would require the use of two distinct physical units. The physical and virtualized segments are expected to record a significant CAGR during the forecast period.

By Subscription Model Analysis

Diversity in Services to Fuel Adoption of Paid Subscription-based Operating System

By subscription model, the market is divided into paid subscription and non-paid subscription.

The paid subscription segment will account for 56.71% market share in 2026. It offers highly secured and efficient performance to clients. Paid subscriptions include maintenance, upgradation, technical support, and many other services. Thus, with the increasing cyber threats, industries are keen on implementing the paid subscription model.

The non-paid subscription segment is projected to record the highest CAGR during the forecast period. Small and medium-sized enterprises or companies with limited IT funding are adopting non-paid subscription models. Also, a rising number of startups are contributing to the growth of non-paid subscriptions as they usually have less funds.

By Enterprise Type Analysis

Growing IT Funding to Boost Product Adoption in Large Enterprises

By enterprise type, the market is segmented into large enterprises and small & medium enterprises.

The large enterprises segment is expected to account for 52.18% of the market in 2026. It requires higher security, stability, and volume. Thus, the investment in server operating systems is expected to increase.

The small and medium enterprises segment is predicted to showcase the highest CAGR during the forecast period. The small & medium enterprises segment is also adopting the operating system on a cloud server instead of investing in on-premises servers. It requires less on-board staff to maintain and properly run the server, thus making the deployment cost-efficient.

REGIONAL INSIGHTS

The report’s scope includes three major regions: the Americas, Europe, the Middle East & Africa, and Asia Pacific.

North America

Americas Server Operating System Market Volume, 2025 (thousand)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 59.00% to the global market in 2025, with a valuation of USD 17427 thousand, and is projected to reach USD 19419 thousand in 2026. A server operating system is used to manage several applications, such as storage management, server management, and others using AI technology. Furthermore, government investments across the region are anticipated to drive the market growth. The U.S. market is projected to reach 11,182 thousand by 2026.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

The Asia Pacific market was valued at USD 4953 thousand in 2025, capturing 16.80% of global revenue, and is estimated to reach USD 5723 thousand in 2026. The increasing number of data centres, along with a surge in investments by leading players in Asia Pacific, will drive the market. India and China have the highest number of colocation data centres, 160 and 87, respectively. An increase in digital technology penetration in countries such as India, China, Japan, and others is expected to create ample opportunity for key players in the market. The computing systems in the colocation data centres use server-based operating systems. Hence, it is expected to drive the market growth in these countries. The Japan market is projected to reach 1,003 thousand by 2026, the China market is projected to reach 1,678 thousand by 2026, and the India market is projected to reach 879 thousand by 2026.

Europe and the Middle East & Africa

Europe accounted for USD 7159 thousand in 2025, representing 24.20% of the global market share, and is projected to reach USD 8098 thousand in 2026. An increase in overall ICT spending across Europe has increased the demand for server operating systems to assist organizations in the digital transformation of businesses. According to Forrester's Data Center Map, there are more than 139 colocation data centres in 16 countries across the Middle East. An increase in the number of colocation data centres is expected to create ample opportunity for the key players in the market. The UK market is projected to reach 821 thousand by 2026, while the Germany market is projected to reach 827 thousand by 2026.

Key Industry Players

Emphasis of Key Players on Developing Server Operating Systems to Strengthen Market Competition

The companies operating in the market, such as Google LLC (Alphabet Inc.), Microsoft Corporation, Amazon Web Services (AWS), IBM Corporation (Red Hat, Inc.), and others, are developing OS integrated with advanced technologies.

List of Top Server Operating System Companies:

- Microsoft Corporation (U.S.)

- Red Hat, Inc. (IBM Corporation) (U.S.)

- Google LLC (U.S.)

- Amazon Web Services, Inc. (U.S.)

- Fujitsu Ltd. (Japan)

- NEC Corporation (Japan)

- Apple Inc. (U.S.)

- Hewlett Packard Enterprise (U.S.)

- Dell Technologies Inc. (U.S.)

- Canonical Ltd. (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- January 2024 – Microsoft unveiled the first preview of the Windows Server 2025. It is the first server operating system type of the next Windows Server LTSC (Long-Term Servicing Channel) Preview and is called Windows Server Insider Preview 26040.

- May 2023 – Red Hat announced the release of Red Hat Enterprise Linux 8.8 and 9.2. These releases will drive Red Hat’s efforts to streamline and simplify difficult Linux platform operations over the hybrid cloud, from data centers to edge deployments and public clouds.

- January 2023 - Dell Technologies expanded its PowerEdge Servers portfolio to provide enhanced performance and energy-efficient design. It was developed to fast-track reliability and performance for powerful computing over core data centers, edge locations, and large-scale public clouds.

- November 2022 – Microsoft Corporation introduced the SQL server 2022 platform for on-premises and cloud services. Through this launch, enterprises using on-premises deployment models can access cloud solutions and then easily move to the cloud when required.

- May 2022 – Red Hat, Inc. announced a collaboration with Samsung Electronics Co., Ltd. to work on next-generation memory software that helps the software and hardware perform better across a diverse server environment.

- May 2022 – Red Hat, Inc. announced its strategic partnership with General Motors to help with its Red Hat In-Vehicle Operating System. General Motors’ Ultifi software platform requires robust cybersecurity protection, and for this, RedHat provides its certified Linux-based system.

REPORT COVERAGE

The research report provides an in-depth analysis of the market. It focuses on key aspects, such as leading companies and top product applications. Besides this, the report offers insights into the latest market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several key factors contributing to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

CAGR |

Growth rate of 11.40% from 2026 to 2034 |

|

Unit |

Volume (Thousand) |

|

Segmentation |

By Operating System

By Virtualization Status

By Subscription Model

By Enterprise Type

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market is expected to reach 79098 thousand by 2034.

The market volume stood at 29,539 thousand in 2025.

The market is expected to record a CAGR of 11.40% during the forecast period of 2026-2034.

The Linux operating system segment is expected to lead the market with the highest CAGR during the forecast period.

Rising adoption of cloud-based environments and increasing investments by leading players in developing cloud infrastructure are key drivers for the market’s growth.

Microsoft Corporation, Google LLC (Alphabet Inc.), Amazon Web Services (AWS), Red Hat, Inc., Fujitsu Ltd., NEC Corporation, and Apple Inc. are the top companies in the market.

The paid subscription model segment holds the highest market share.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us