Amylin Analog Drugs Market Size, Share & Industry Analysis, By Product (Symlin (pramlintide), CagriSema (cagrilintide + semaglutide), and Others), By Disease Indication (Diabetes, Obesity, and Others), By Route of Administration (Oral and Parenteral), By Distribution Channel (Hospitals Pharmacies, Drug Stores & Retail Pharmacies, Specialty Pharmacies, and Others), and Regional Forecast, 2026-2034

Amylin Analog Drugs Market Size and Future Outlook

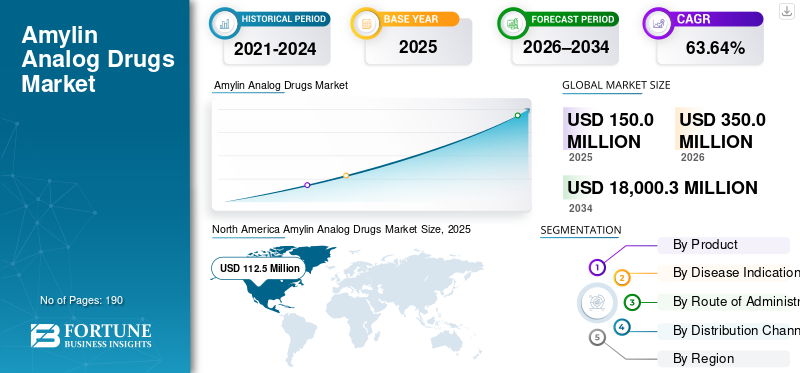

The global amylin analog drugs market size was valued at USD 150.0 million in 2025. The market is projected to grow from USD 350.0 million in 2026 to USD 18,000.3 million by 2034, exhibiting a CAGR of 63.64% during the forecast period. North America dominated the amylin analog drugs market with a market share of 75% in 2025.

The global market is poised for exponential growth in the forthcoming years. The significant growth of the market is attributed to the rising prevalence of metabolic disorders such as diabetes and obesity. Key companies operating in the market are developing innovative solutions to offer a treatment regimen for bleeding episodes. Also, robust support from regulatory bodies and rapid approvals for new drugs further strengthen market growth.

- For instance, in May 2025, AbbVie collaborated with Gubra A/S to develop GUB014295, a potential best-in-class, long-acting amylin analog for the treatment of obesity. Such strategic initiatives are anticipated to bolster the market demand.

Moreover, major players in the amylin analog drugs industry, such as Eli Lilly and Company, AstraZeneca, F. Hoffmann-La Roche Ltd, and AbbVie Inc., are operating in the market to expand their pipeline and address unmet demand.

Download Free sample to learn more about this report.

Amylin Analog Drugs Market Key Takeaways

- 2025 Market Size: USD 150.0 million

- 2026 Market Size: USD 350.0 million

- 2034 Forecast Market Size: USD 18,000.3 million

- CAGR: 63.64% from 2026-2034

- North America dominated the amylin analog drugs market with a 75% share in 2025.

- The diabetes segment dominated the market in 2025.

- The CagriSema (cagrilintide + semaglutide) segment is projected to grow at a CAGR of 114.39% during the forecast period.

North America

North America reached USD 112.5 million in 2025, maintaining its leading position in the global market.

Europe

Europe is projected to reach USD 62.7 million in 2026, registering strong regional growth.

Asia Pacific

Asia Pacific is estimated to reach USD 24.2 million in 2026, securing the third-largest regional market.

U.S.

The market is estimated to reach USD 235.1 million in 2026, accounting for approximately 67.18% of the global market.

Japan

The market is estimated to reach USD 5.3 million in 2026, representing around 1.53% of the global market.

Read More

AMYLIN ANALOG DRUGS MARKET TRENDS

Shift Toward Next-Gen, Long-Acting Amylin Agents is a Significant Market Trend Observed

A major global market trend in the market is the shift from standalone amylin to next-gen, long-acting amylin agents. These agents are paired with incretins such as GLP-1, as fixed-dose combinations. These amylin agents add satiety and reduce meal-related glucose swings, while incretins drive strong weight loss and metabolic benefits. These benefits, when combined, aim to deliver greater weight loss with better tolerability and adherence.

- For instance, in December 2025, Novo Nordisk A/s submitted New Drug Application (NDA) to the U.S. FDA for once-weekly CagriSema (cagrilintide 2.4 mg and semaglutide 2.4 mg) injection, to be used with a reduced-calorie diet and increased physical activity, to reduce excess body weight and maintain weight reduction long term in adults with obesity or overweight in the presence of at least one weight-related comorbid condition. Such development offers a significant growth opportunity for the market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Prevalence of Metabolic Disorders to Fuel Market Growth

The increasing prevalence of metabolic disorders, such as diabetes and obesity, is driving the global amylin analog drugs market demand. Rising obesity and diabetes are expanding the treatable patient pool and pushing healthcare providers to prioritize therapies that can deliver meaningful weight loss and better metabolic control. An expanding patient pool increases long-term healthcare costs and underscores the need for more effective pharmacotherapy. Next-generation amylin analogues can improve satiety and reduce post-meal metabolic stress, helping this patient pool fuel market growth.

- For instance, in 2024, the International Diabetes Federation reported 9.0 million adults worldwide were living with diabetes. Such an increasing prevalence of metabolic disorders creates demand for amylin analog drugs and boosts the market growth.

MARKET RESTRAINTS

Safety and Tolerability Concerns to Hamper Adoption of these Analogs of Medication Used to Hamper Market Growth

Safety and tolerability are key restraints for the market. In type 2 diabetes, amylin aggregates in pancreatic islets and may contribute to β-cell destruction. These mechanisms commonly trigger nausea, vomiting, and other GI effects, and combining them can increase the overall GI burden. When side effects rise, more patients pause or discontinue treatment, reducing effectiveness and slowing uptake. This forces companies to run longer dose-finding and titration studies to identify the highest tolerable dose that still delivers strong weight loss.

MARKET OPPORTUNITIES

Increasing Research and Development for Expanding Pipeline to Offer Significant Market Growth Opportunity

A key market growth opportunity for amylin analog drugs is to expand research initiatives and increase investments in the development of innovative formulations. As more companies invest, the pipeline expands from short-acting injectables to long-acting amylin-pathway drugs, and convenience and adherence also improve. This creates multiple candidates operating in the market and reduces heavy reliance on limited product offerings for obesity drugs. As a result, stronger pipelines attract funding, and faster commercialization is anticipated to drive exponential amylin analog drugs market growth.

- For instance, in June 2024, Zealand Pharma announced positive topline results from the Phase 1b 16-week multiple-ascending-dose clinical trial of the long-acting amylin analog petrelintide. Such developments offer market growth opportunities.

MARKET CHALLENGES

Payer Resistance and Pricing Pressure Pose a Critical Challenge to Market Growth

When many high-efficacy metabolic drugs compete, payers push back as covering multiple premium therapies can sharply raise pharmacy spend. As choices increase, insurers and PBMs use step therapy, prior authorization, and preferred formularies to force bigger rebates and steer patients to the lowest net-cost option. This creates pricing pressure on manufacturers, as losing “preferred” status can quickly reduce volume. Companies may then lower list/cash prices or expand discount channels to protect access. Overall, tighter payer controls slow uptake and squeeze margins, making reimbursement a real market challenge.

- For instance, in May 2025, CVS Caremark withdrew reimbursement for the weight-management drug Zepbound, which was previously included in Standard Control, Advanced Control, and Value formularies. Such factors adversely impact the adoption of these drugs, hampering the market's growth potential.

Segmentation Analysis

By Product

Ease of Adherence with Weekly Dosing of Symlin (pramlintide) to Place Them in Leading Position and Boost Segmental Growth

Based on product, the market is categorized into Symlin (pramlintide), Cagrisema (cagrilintide + semaglutide), and others.

Among these, Symlin (pramlintide) dominated the global market as it combines two complementary mechanisms that help patients eat less and better manage metabolism. The drug is administered once weekly which aligns with current metabolic prescribing habits and facilitates adherence. Strong late-stage trial momentum increases confidence among prescribers and payers. As a result, it attracts more clinical attention and commercial investment than short-acting amylin products. Furthermore, expanding the pipeline by key companies and launching new products to support segmental growth.

- For instance, in December 2024, Novo Nordisk A/S showcased positive results from REDEFINE, a phase 3 trial in the global REDEFINE programme investigating subcutaneous CagriSema (a fixed dose combination of cagrilintide 2.4 mg and semaglutide 2.4 mg) compared to the individual components cagrilintide 2.4 mg, semaglutide 2.4 mg, and placebo, all administered once-weekly. Such developments are reinforcing the segment's dominance.

CagriSema (cagrilintide + semaglutide) segment is expected to grow at a CAGR of 114.39% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Increasing Prevalence of Diabetes to Lead Segmental Growth

Based on the disease indication, the market is segmented into diabetes, obesity, and others.

In 2025, the diabetes segment dominated the market. The high share of the segment is attributed to the increasing global burden of diabetes. Patients and doctors actively track glucose outcomes, making it easier to adopt therapies that improve post-meal control. Treatment pathways are well established, supporting faster uptake of amylin analog drugs. The segment also contributes to high healthcare spending, further strengthening its dominance in the market.

- For instance, in 2024, the International Diabetes Federation reported that diabetes caused at least USD 1 trillion in health expenditure, witnessing a 338% increase over the last 17 years.

The other segment is projected to grow at a CAGR of 117.90% during the forecast period for the global market.

By Route of Administration

Effectiveness Showcased by Parenteral Therapy to Reinforce its Dominance in Market

Based on route of administration, the market is segmented into oral and parenteral.

In 2025, the parenteral route of administration dominated the market. The large share was attributed to the segment as amylin analogues are peptides, and injections deliver more consistent drug exposure than oral delivery. Injections also enable long-acting formulations, making weekly dosing realistic and improving convenience. Underscoring these advantages, many key companies are also focusing on research and development with a vast pipeline of candidates for parenteral amylin injections.

- For instance, in November 2023, Gubra dosed its first subject in the Phase 1 clinical trial of amylin agonist (GUBamy) for the treatment of obesity.

In addition, the parenteral segment is projected to grow at a CAGR of 110.87% during the study period.

By Distribution Channel

Convenience offered by Drug Stores and Retail Pharmacies to Place Them in a Leading Position

Based on distribution channel, the market is segmented into hospitals, pharmacies, drug stores & retail pharmacies, specialty pharmacies, and others.

Drug stores and retail pharmacies held a significant amylin analog drugs market share in the global market in 2025. They dominated the market as metabolic therapies are long-term and driven by recurring needs. Retail networks offer the widest access and quickest scale when demand rises. Payers also often steer prescriptions through preferred retail networks to control costs. These factors, along with reimbursement flow, keep retail pharmacies the primary channel.

- For instance, in March 2025, Novo Nordisk updated its program to enable eligible patients to redeem the USD 499/month Wegovy reimbursement offer at the retail pharmacy of their choice, reinforcing retail’s role in dispensing metabolic injectables.

The specialty pharmacies segment is projected to grow at a CAGR of 81.31% during the study period.

Amylin Analog Drugs Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Amylin Analog Drugs Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, at USD 109.9 million, and maintained its leading position in 2025, at USD 112.5 million. The market in North America is expected to grow significantly over the forecast period, driven by rising research activity and reimbursement initiatives, additionally, increasing disease prevalence and high healthcare spending are driving market growth in the region.

U.S. Amylin Analog Drugs Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 235.1 million in 2026, accounting for roughly 67.18% of the global market.

Europe

Europe is projected to grow at 70.62% over the coming years, the second-highest among all regions, and reach a valuation of USD 62.7 million by 2026. The region is expected to experience robust growth due to the growing focus of regional health systems toward prioritizing cardiometabolic risk reduction, creating demand for therapies that improve weight and metabolic markers.

U.K. Amylin Analog Drugs Market

The U.K. market in 2026 is estimated at around USD 13.1 million, representing roughly 3.74% of the global market.

Germany Amylin Analog Drugs Market

Germany’s market is projected to reach approximately USD 14.5 million in 2026, equivalent to around 4.15% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 24.2 million in 2026 and secure the position of the third-largest region in the market. Strong patient population base, prevalence of chronic diseases, and approvals for novel drugs is to drive the regional market growth. For instance, in December 2025, Danish Zealand Pharma A/S partnered with a Chinese start-up, OTR Therapeutics Co. Ltd, for the expansion of their oral obesity pipeline in an USD 30 million upfront deal.

Japan Amylin Analog Drugs Market

The Japanese market in 2026 is estimated to be around USD 5.3 million, accounting for approximately 1.53% of the global market.

China Amylin Analog Drugs Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 6.4 million, representing approximately 1.84% of global sales.

India Amylin Analog Drugs Market

The Indian market in 2026 is estimated at around USD 3.0 million, accounting for roughly 0.85% of global revenue.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 8.4 million in 2026. The region's growth is driven by rising investment and government initiatives. In the Middle East & Africa, the GCC is set to reach USD 1.9 million in 2026.

South Africa Amylin Analog Drugs Market

The South African market is projected to reach approximately USD 0.5 million by 2026, accounting for roughly 0.14% of the global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on New Product Launches by Key Players to Propel Market Progress

The global market has a consolidated market structure, with companies such as AstraZeneca, holding a large market share. The leading market share of these companies is attributed to expanding clinical pipelines, new product launches, strategic acquisitions, and investments in the sector.

- For instance, in November 2025, Pfizer announced the completion of the acquisition of Metsera.

Other notable players in the global market include Metsera, Inc. Verdiva Bio Limited, and Structure Therapeutics. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their position during the forecast period for the global market.

LIST OF KEY AMYLIN ANALOG DRUGS COMPANIES PROFILED

- Eli Lilly and Company (U.S.)

- AstraZeneca (U.K.)

- Hoffmann-La Roche Ltd (Switzerland.)

- AbbVie Inc (U.S.)

- Metsera, Inc. (U.S.)

- Verdiva Bio Limited (U.K.)

- Structure Therapeutics (U.S.)

- Hangzhou Sciwind Biosciences Co., Ltd (China)

- Novo Nordisk A/S (Denmark)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Structure Therapeutics announced the initiation of a Phase 1 clinical study of oral small molecule amylin receptor agonist, ACCG-2671, for the treatment of obesity.

- November 2025: Eli Lilly and Company showcased positive results from a Phase 2 trial evaluating the safety and efficacy of eloralintide, an investigational once-weekly, selective amylin receptor agonist.

- June 2025: Metsera, Inc. showcased positive topline data from the Phase 1 clinical trial of MET-233i, an ultra-long acting amylin analog engineered for combinability with the company’s GLP-1 receptor agonist candidate, MET-097i.

- March 2025: AbbVie Inc. collaborated with Gubra A/S to develop GUB014295, a potential best-in-class, long-acting amylin analog for the treatment of obesity.

- March 2024: Hoffmann-La Roche Ltd entered into a licensing agreement with Zealand Pharma to co-develop and co-commercialize petrelintide as a potential foundational therapy for people with overweight and obesity.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 63.64% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Product, Disease Indication, Route of Administration, Distribution Channel, and Region |

|

By Product |

· Symlin (pramlintide) · CagriSema (cagrilintide + semaglutide) · Others |

|

By Disease Indication |

· Diabetes · Obesity · Others |

|

By Route of Administration |

· Oral · Parenteral |

|

By Distribution Channel |

· Hospital Pharmacies · Drug Stores & Retail Pharmacies · Specialty Pharmacies · Others |

|

By Region |

· North America (By Product, Disease Indication, Route of Administration, Distribution Channel, and Country) o U.S. o Canada · Europe (By Product, Disease Indication, Route of Administration, Distribution Channel, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Product, Disease Indication, Route of Administration, Distribution Channel, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Product, Disease Indication, Route of Administration, Distribution Channel, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Product, Disease Indication, Route of Administration, Distribution Channel, and Country/Sub-region) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 150.0 million in 2025 and is projected to reach USD 18,000.3 million by 2034.

In 2025, the market value stood at USD 112.5 million.

The market is expected to grow at a CAGR of 63.64% over the forecast period.

By product, the Symlin (pramlintide) segment is expected to lead the market.

The increasing prevalence of metabolic disorders is driving market growth.

AstraZeneca is the major player in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us