Anti-Satellite (ASAT) Weapons Market Size, Share & Industry Analysis, By Weapon Type (Direct-ascent ASAT, Co-orbital ASAT, Directed-energy ASAT, & Electronic Warfare ASAT), By Platform Basing (Ground, Space, Air-launched, and Sea), By Target Orbit (LEO, MEO, GEO, and Multi-orbit), By Component (Weapon & payload, Launcher, Guidance, Navigation & Control, Sensors & Tracking, Control & Battle Management, and Others), By End User (Military & Defense Forces, Strategic & Missile Forces, Space Commands, and Intelligence-linked National Security Agencies), and Regional Forecast, 2026-2034

Anti-Satellite (ASAT) Weapons Market Size and Future Outlook

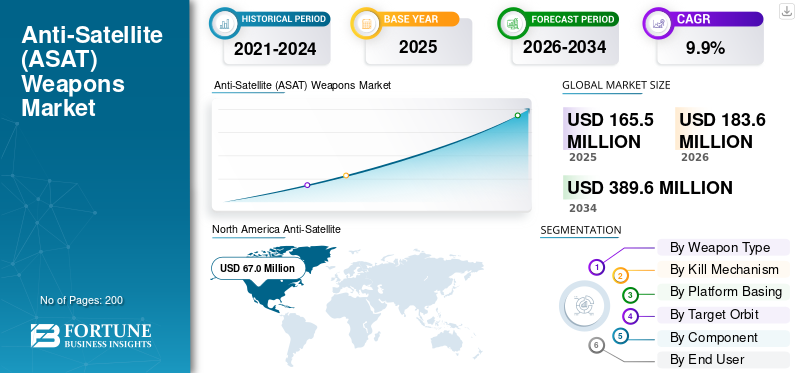

The global Anti-Satellite (ASAT) weapons market size was valued at USD 165.5 million in 2025. The market is projected to grow from USD 183.6 million in 2026 to USD 389.6 million by 2034, exhibiting a CAGR of 9.9% during the forecast period. North America dominated the anti-satellite (asat) weapons market with a market share of 40.48% in 2025.

The Anti-satellite (ASAT) weapons market includes systems built to disrupt, disable, or destroy satellites and the support architecture required to detect, target, and execute those missions. It covers kinetic ASAT systems as well as electronic, cyber, co-orbital, and selected energy weapons within a wider space defense capabilities framework. The market is being driven by growing national security dependence on satellite constellations, rising concern over space debris after destructive ASAT tests, and the need for stronger space situational awareness as competition in earth orbit intensifies, especially around China and Russia.

The competitive landscape is still led by the government, but a few defense primes are changing it through real military-space programs. The U.S. Space Force will use L3Harris Meadowlands as an offensive space-control system in 2025. Companies including Lockheed Martin, Northrop Grumman, and Boeing continue to shape the market with missile warning, tracking, orbital systems, and other military-space infrastructure.

Download Free sample to learn more about this report.

Anti-Satellite (ASAT) Weapons MARKET TRENDS

Shift Toward Non-Destructive and Reversible Counterpace Systems to be a Significant Market Trend

Shift from debris-generating, high-escalation intercept systems toward non-destructive and more operationally usable counterspace tools such as electronic warfare, cyber-enabled disruption, and reversible space-control effects, is a noticeable trend in market. This shift is being driven by the need to protect satellite constellations, limit space debris, and maintain freedom of action in earth orbit without crossing the political and military threshold associated with destructive ASAT tests. Moreover, it is also making space situational awareness, command layers, and non-kinetic mission systems more central to future procurement and program development.

In May 2025, the U.S. Space Force received fielding approval for CCS Meadowlands, an upgraded Counter Communications System designed to detect, identify, and disrupt adversary communications systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Military Dependence on Satellite-Based Services is a Primary Driver of ASAT Market

The key driver in the global Anti-satellite (ASAT) weapons market growth is the military’s rising dependence on space-based services for satellite communications, positioning, navigation and timing, missile warning, missile tracking, and ISR. As this functions become central to warfighting, satellites stop being support assets and become strategic targets as well as protected infrastructure. As a result, governments are investing more in offensive and defensive counterspace systems, resilient architectures, and faster space situational awareness and attribution capability.

In March 2024, the Department of the Air Force released its FY2025 budget proposal, which included USD 4.7 billion to proliferate a multi-orbit missile warning architecture and USD 4.4 billion for integrating satellite communications to increase space superiority.

MARKET RESTRAINTS

Rising International Pressure Against Debris-Generating ASAT Activity is Restraining Market Growth

The growing diplomatic, regulatory, and operational pushback against destructive, debris-generating ASAT systems is restraining the market growth. Governments are investing in counterspace capability, but the market for overt kinetic ASAT development is being constrained by the risk of long-lived space debris, higher political costs, and the increasing preference for reversible or non-destructive space-control options. Overall, the more the industry is tied to debris-creating tests, the harder it becomes to justify procurement, testing, and deployment in a rules-sensitive national security environment.

In December 2022, the UN General Assembly adopted the resolution on destructive direct-ascent anti-satellite missile testing by a vote of 155-9-9, strengthening international pressure against debris-generating ASAT behavior.

MARKET OPPORTUNITIES

Expansion of Increased Military Satellite Constellations is Creating a Major Opportunity for Advanced Counterspace and Space-Control Systems

Main opportunity in the global market is the rapid expansion of proliferated and multi-orbit military space architectures. As governments deploy larger numbers of satellites for communications, missile warning, tracking, and ISR, the demand side of the market broadens beyond traditional kinetic ASAT systems and opens more room for non-kinetic space-control tools, electronic warfare, cyber-enabled disruption, and stronger space situational awareness layers. Overall, the more militaries depend on dense satellite constellations, the larger the opportunity for suppliers offering detection, disruption, targeting, protection, and mission-control capability across challenged earth orbit environments.

MARKET CHALLENGES

Dense and Dual-Use Program Structures are Making ASAT Market Difficult to Scale

A major challenge in the global market is that most counterspace capability is not procured as a clean, standalone weapon line. It is usually embedded inside broader missile, cyber, electronic warfare, intelligence, or military-space programs, making demand harder to isolate, supplier opportunity harder to quantify, and procurement visibility much weaker than in conventional defense markets.

In December 2024, the U.S. Department of Defense said China’s counterspace portfolio spans direct-ascent anti-satellite missiles, co-orbital satellites, electronic warfare, directed-energy systems, mobile jammers, and offensive cyberspace capabilities.

Impact of Current War

Current Conflicts are Accelerating Demand for Non-Destructive Counterspace Systems and Faster Space-Domain Resilience

The impact of ongoing conflicts on the global market is becoming more visible through the growing military use of jamming, spoofing, SATCOM disruption, and other non-destructive counterspace effects rather than through repeated debris-generating intercepts. The wars and confrontations linked to Ukraine and the Middle East have shown how heavily modern forces depend on satellites for communications, navigation, ISR, and targeting, also showing how vulnerable those services are to reversible disruption. That is pushing the market toward soft-kill, stronger space situational awareness, quicker attribution, and more resilient military-space architectures instead of relying only on classic kinetic ASAT pathways.

In March 2025, the ITU, ICAO, and IMO issued a joint warning urging states to protect radio-navigation satellite services from harmful interference after growing cases of jamming and spoofing disrupted GNSS signals used for civilian and humanitarian operations.

Segmentation Analysis

By Weapon Type

Due to Growing Preference for Reversible, Deployable, and Operationally Usable Space-Control Effects, Electronic Warfare ASAT Segment Dominated

In terms of weapon type, the market is categorized into direct-ascent ASAT, co-orbital ASAT, directed-energy ASAT, electronic warfare ASAT, and cyber ASAT.

Electronic Warfare ASAT segment held the largest Anti-satellite (ASAT) weapons market share in 2025, as they offer a clean, reversible way to disable enemy satellites. Unlike kinetic weapons, which create dangerous debris, EW tools use jamming, spoofing, and lasers to disrupt communications and surveillance without physically destroying the target. Additionally, this systems are easier to integrate to bigger space defense systems and fit better with the trend toward non-destructive counterspace options. Moreover, armed forces are using satellite constellations more and more for communications, ISR, and navigation support, in turn driving the segment growth.

Co-orbital ASAT segment is expected to grow at a CAGR of 12.0% over the forecast period.

By Kill Mechanism

Growing Preference for Reversible and Operationally Usable Counterspace Effects, Soft-Kill Segment Dominated Market

On the basis of kill mechanism, the market is classified into hard-kill and soft-kill.

Soft-kill segment dominated the global market in 2025, since it allows militaries to disrupt or damage satellite services without creating the long-term effect related with debris-generating destruction. As defense forces become more dependent on communications, navigation, ISR, and missile warning from space, governments are prioritizing non-destructive options such as electronic warfare, cyber-enabled disruption, and other reversible space-control effects that are more usable in live operations and easier to integrate into wider space defense capabilities.

For Instance, in April 2025, SWF’s 2025 assessment reinforces this shift by mentioning that, despite ongoing counterspace R&D, only non-destructive counterspace capabilities are being used in active military conflicts.

Hard-kill segment is expected to show the second fastest growth, registering a CAGR of 8.6% over the forecast period.

By Platform Basing

Due to Proven Terrestrial Deployment, Easier System Integration, and Stronger Operational Readiness, Ground-Based Segment Dominated

By platform basing, the market is segmented into ground-based, space-based, air-launched, and sea-based.

Ground-based systems held the largest global market share in 2025, as the most counterspace capabilities still rely on terrestrial launch, tracking, command, and electronic attack infrastructure. Compared with space-based systems, ground-based platforms are easier to deploy, upgrade, and integrate with wider military networks, while also supporting both kinetic ASAT intercept concepts and non-kinetic space-control missions. This gives them a practical advantage in a market due to governments wanting operationally usable systems without waiting for more complex on-orbit architectures to mature.

Space-based segment is the fastest growing segment and is expected to grow at a CAGR of 12.7% across the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Target Orbit

LEO Segment Dominated Market Due to its High Concentration of Military Satellites and History of ASAT Activity

Based on target orbit, the market is segmented into LEO, MEO, GEO, and multi-orbit.

LEO segment led the global market in 2025, since it is the most operationally dense orbital layer for modern military and strategic space activity. A growing share of missile warning, tracking, communications, ISR, and proliferated defense architecture is being deployed into low Earth orbit, which makes LEO the most exposed and most contested orbital band in the market. Additionally, it also remains the major orbit for publicly demonstrated kinetic ASAT activity, strengthening its dominance over MEO, GEO, and multi-orbit categories.

In March 2019, India’s Ministry of Defence announced that Mission Shakti had successfully engaged an Indian target satellite in Low Earth Orbit (LEO) in a “Hit to Kill” mode using a DRDO-developed interceptor missile.

Multi-orbit segment is the fastest growing segment in market and is expected to grow at a CAGR of 13.1% during the forecast period.

By Component

Due to Central Role of Mission Effectors in Kinetic and Non-Kinetic Counterspace Operations, Weapons & Payload Dominated Market

Based on component, the market is segmented into weapon & payload, launcher, guidance, navigation & control, sensors & tracking, command, control & battle management, and others.

Weapon & payload dominated the global market in 2025, as it represents the core mission-delivery layer of the system, whether the capability is built around a hit-to-kill interceptor, an electronic attack package, or other non-kinetic space-control hardware. In this market, the payload are main component that creates the operational effect, so it captures a larger share of value than supporting elements such as launch, guidance, or integration alone. That advantage grows as governments invest in more specialized counterspace systems designed to disrupt, degrade, or destroy targets across contested earth orbit environments.

The others segment is expected to grow at a CAGR of 11.6% during the forecast period.

By End User

Military & Defense Forces Segment Dominated Market Due to Their Central Role in Operating, Protecting, and Contesting Space-Based Services

Based on end user, the market is segmented into military & defense forces, strategic & missile forces, space commands, and intelligence-linked national security agencies.

The military & defense forces segment led the global market in 2025, as they are the primary users of satellite communications, missile warning, tracking, ISR, navigation, and wider space-enabled warfighting support. As these functions become important to military effectiveness, the same forces also become the main buyers of systems that can disrupt, deny, or defend against hostile space activity. As a result, ASAT demand remains focused within defense organizations rather than in narrower specialist users, especially as space is now treated as a priority military domain supporting joint and combined operations.

The space commands segment is expected to show the fastest market growth, registering a CAGR of 11.2% over the forecast period.

Anti-Satellite (ASAT) Weapons Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and rest of the world.

North America

North America Anti-Satellite (ASAT) Weapons Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America led the global Anti-satellite (ASAT) weapons market in 2025, since it leads in operational counterspace systems, defense-space funding, and military space architecture development. The region benefits from the U.S. Space Force’s active role in offensive and defensive space control, stronger integration of space situational awareness with warfighting needs, and faster movement from program development to fielded capability. Compared with other regions, North America has the most mature institutional structure for translating national security requirements into deployable ASAT capabilities, which keeps it at the front of the market.

U.S. Anti-Satellite (ASAT) Weapons Market

Based on the strong contribution of North America to the market and the dominance of U.S. within the region, the U.S. market stood at around USD 65.8 million in 2025, growing at a CAGR of 8.5% over the forecast period.

Europe

Europe held around 20.16% share of global Anti-Satellite (ASAT) Weapons market in 2025. Europe is not only a Western European space-security market built around resilience, surveillance, and active-defense concepts, it also includes Russia’s legacy in destructive ASAT testing, co-orbital behavior, and wider counterspace activity, driving the region growth. Additionally, the regional analysis focus is gradually shifting toward more structured military-space organizations, stronger space situational awareness, and non-destructive counterspace tools. The U.K.’s 2025 Strategic Defence Review reinforces the importance of space as an operational military domain, while France and Germany are also deepening early-warning and military-space cooperation.

France Anti-Satellite (ASAT) Weapons Market

France market reached approximately USD 4.2 million in 2025, equivalent to around 12.50% of Europe revenues.

Russia Anti-Satellite (ASAT) Weapons Market

Russia is actively developing a diverse, multi-layered anti-satellite (ASAT) arsenal, focusing on both kinetic (physical destruction) and non-kinetic (jamming, lasers, nuclear) technologies, as a result Russia’s market stood at around USD 15.8 million in 2025, representing roughly 47.42% of Europe revenues.

Asia Pacific

Asia Pacific is one of the most important growth regions in the market, and is anticipated to grow at a highest CAGR of 11.3% over the forecast period, the region is growing as it combines the strongest mix of hard-kill legacy and expanding non-kinetic counterspace development. China and India give the region real ASAT weight through past destructive testing, while Japan, Australia, and South Korea are steadily strengthening military-space doctrine, command structures, and broader counterspace-support capabilities. This gives Asia Pacific a more balanced profile than Europe or Rest of the World. Moreover, the region is also moving deeper into jamming, cyber-linked disruption, tracking, and operational space-domain control. In turn, Asia Pacific is becoming more important not only owing to weapons development, but also due to its wider military-space architecture is maturing quickly.

China Anti-Satellite (ASAT) Weapons Market

China has developed the world's most comprehensive Anti-Satellite (ASAT) program, encompassing kinetic missiles, co-orbital technologies, directed energy, and cyber warfare capabilities, accelerating investment to achieve strategic superiority, with 2025 revenues stood at around USD 24.5 million, representing roughly 47.62% of the global sales.

Japan Anti-Satellite (ASAT) Weapons Market

The Japanese market stood at around USD 5.2 million in 2025, accounting for roughly 10.12% of Asia Pacific revenues.

Rest of the World

Rest of the World (Middle East & Africa and Latin America) holds a comparatively smaller market share but is expected to grow at a CAGR of 9.5% during the forecast period. The strongest momentum in this segment comes from Middle East, where current threat patterns include persistent GPS jamming and spoofing and Iran and Israel are part of the broader counterspace-development conversation. Apart from this, Latin America remains comparatively limited and more focused on civil space and support infrastructure than on offensive ASAT capability.

Latin America Anti-Satellite (ASAT) Weapons Market

The market in Latin America reached around USD 1.7 million in 2025, accounting for roughly 12.26% of revenues.

Middle East & Africa Anti-Satellite (ASAT) Weapons Market

Driven by regional geopolitical tensions, increased reliance on space assets, and the need for defense against surveillance, the Middle East & Africa market stood at around USD 12.1 million in 2025 and is expected to reach USD 28.5 million in 2034, representing roughly 87.74% in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Expanding their Market Share through Deployable Electronic Warfare Systems Orbital Mission Experimentation

The competitive landscape of the global Anti-satellite (ASAT) weapons market remains highly concentrated and strongly tied to government-led space and defense programs rather than broad commercial demand. L3Harris is a major leader as it delivered the Meadowlands offensive space-control system to the U.S. Space Force in 2025, giving it a direct role in operational counterspace capability. Lockheed Martin is influencing the market from a broader military-space angle through work on proliferated missile warning and tracking architectures, while Northrop Grumman remains important through space-domain-awareness and surveillance capability such as GSSAP, supporting tracking and characterization of objects in near-geosynchronous orbit.

Boeing also holds an important position through the X-37B program, keeping the company tied to advanced orbital experimentation and future military-space operating concepts. Overall, these key players are driving the market less through mass production and more through deployable electronic warfare systems, sensing layers, command architecture, and orbital mission experimentation. Inclusive, the market is still state-led, but the firms best positioned in it are the ones converting military space requirements into fielded systems and resilient space-defense infrastructure.

LIST OF KEY ANTI-SATELLITE (ASAT) WEAPONS COMPANIES PROFILED IN REPORT

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- The Boeing Company (U.S.)

- RTX Corporation (U.S.)

- Kratos Defense & Security Solutions, Inc. (U.S.)

- BAE Systems plc. (U.K.)

- Airbus SE (Netherlands)

- Thales S.A. (France)

- Leonardo S.p.A. (Italy)

- OHB SE (Germany)

- Israel Aerospace Industries Ltd. (Israel)

- China Aerospace Science and Technology Corporation (China)

- China Aerospace Science and Industry Corporation (China)

KEY INDUSTRY DEVELOPMENTS

- May 2025: SSC awarded Phase 2 contracts under the USD 100.00 million Enterprise Space Terminal (EST) program to CACI, General Atomics, and Viasat to develop space laser communication terminal prototypes that enable on-orbit crosslink compatibility for future DoD space systems and support a more resilient military space data network.

- May 2025: SSC awarded SciTec, Inc. a USD 259.00 million contract for the FORGE Enterprise OPIR Solution (EOS) effort, expanding the cyber-secure ground processing backbone for missile warning and tracking across LEO, MEO, GEO, and polar constellations and improving resilience against emerging threats.

- February 2025: SSC awarded Firefly Aerospace a USD 21.81 million launch service contract for VICTUS SOL, the U.S. Space Force’s newest Tactically Responsive Space mission, intended to deliver a faster and more agile on-orbit response capability to warfighters in the face of evolving orbital threats.

- January 2025: SSC awarded L3Harris a USD 90.00 million sole-source contract to continue the Advanced Tracking and Launch Analysis System (ATLAS) program, integrating SDA, C2, intelligence, and operational data to help warfighters respond faster to emerging anti-satellite threats.

- October 2024: SSC awarded Omitron a USD 46.30 million MASCCOT contract for continued R&D and deployment of modern, resilient Space Command and Control (C2) technologies, including upgrades to operational space domain awareness data transport and processing.

- May 2024: The U.S. Space Force Space Systems Command (SSC) awarded Starfish Space a USD 37.50 million STRATFI contract to build, launch, and operate an Otter satellite vehicle for a first-of-its-kind docking mission designed to provide two years of augmented maneuver for national security space assets, strengthening on-orbit mobility, and counterspace support options.

- April 2024: L3Harris received option year five of the MOSSAIC program worth up to USD 187.00 million from the U.S. Space Force to continue modernization and sustainment of critical space infrastructure for space domain awareness, including systems that detect, track, and identify deep-space objects.

REPORT COVERAGE

The global Anti-Satellite (ASAT) weapons market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advances, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.9% from 2026 to 2034 |

| Unit | Value (USD Million) |

|

Segmentation |

By Weapon Type

|

|

By Kill Mechanism

|

|

|

By Platform Basing

|

|

|

By Target Orbit

|

|

|

By Component

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value will achieve USD 183.6 million in 2026 and is projected to reach USD 389.6 million by 2034.

In 2025, the North America’s market value stood at USD 67.0 million.

The market is expected to exhibit a CAGR of 9.9% during the forecast period.

The soft-kill segment led the market by kill mechanism.

Growing military dependence on satellite-based services is a primary driver of ASAT market.

Key players in the market include Northrop Grumman, Lockheed Martin, RTX, L3Harris, The Boeing Company, and BAE Systems.

North America held the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us