Anti-Sniper Detection Systems Market Size, Share, and Industry Analysis By Technology (Acoustic, Optronics, Infrared, AI and ML, & Others), By Platform (Fixed, Portable, & Vehicle-Mounted), By Range (Upto 500m, 500m to 1000m, & Above 1000m), By Application (Perimeter Intrusion & Camp Detection, Border Protection & Control, Critical Infrastructure Detection, VIP & Convoy Protection, ISR & Target Acquisition, Commercial & Office spaces, Hospital Emergency Entrances, Sport Venues, & Others), By End-User (Military, Law-Enforcement & Homeland Security, & Commercial), & Regional Forecast, 2026-2034

Anti Sniper Detection System Market Size and Industry overview

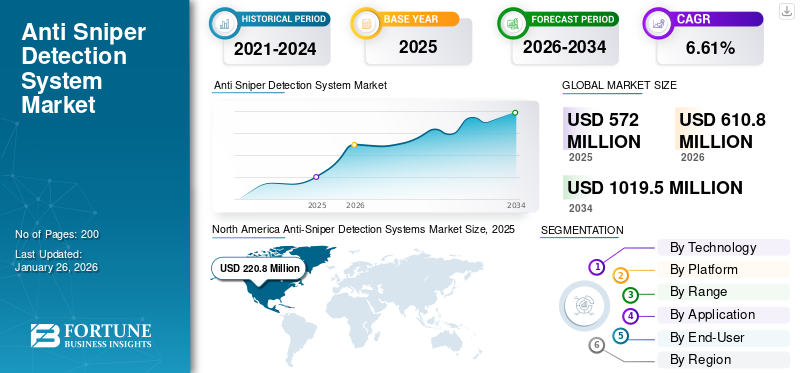

The global anti-sniper detection systems market size was valued at USD 572.00 million in 2025 and is projected to grow from USD 610.80 million in 2026 to USD 1,019.50 million by 2034, exhibiting a CAGR of 6.61% during the forecast period. North America dominated the global market with a share of 38.60% in 2025.

Anti-sniper detection systems are designed to rapidly detect, locate, and track the source of gunfire, particularly from sniper rifles, to protect personnel and assets from a distant range. These systems utilize a combination of sensors, such as acoustic sensors, optronics, and radar, and additional advanced analytics tools and software to identify the direction and distance of incoming fire, enabling a quick response to neutralize the threat. The market is witnessing notable growth fueled by increasing geopolitical tensions and ongoing conflicts between Russia and Ukraine, Israel-Gaza-Syria, and Hezbollah. Moreover, technological advancements in image processing and the integration of AI and ML with analytical tools enable the accurate detection and neutralization of threats.

Major players in the market include RTX Corp., Thales Group, Newcon Optik, WTDS Optics, and Rheinmetall AG, among others. These companies are driving the growth of the market by investing in next-generation detection systems with enhanced AI-assisted detection of the origin of the shot, and advancements in miniaturization. Rising defense sector, increasing spending, increasing geopolitical tension, and growing threats from sophisticated optics and targeting snipers are encouraging these players to innovate and collaborate with military forces globally.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Security Threats, Particularly Sniper Attacks, Fuel the Demand for Modernized Detection Systems

Recently, there has been a rise in terrorist activities and urban warfare scenarios have heightened the need for advanced security measures, including anti-sniper detection solutions. The frequency and harshness of sniper attacks, both on military and civilian populations, are driving the demand for systems that can detect and locate snipers quickly and accurately. Moreover, protecting critical infrastructure, such as power plants, transportation hubs, and government buildings, is crucial, making anti-sniper systems a priority.

Additionally, the ability of anti-sniper detection systems to integrate with existing C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) systems is crucial for operational effectiveness and market acceptance.

Integration of AI, Machine Learning, and Advanced Sensor Technologies in Detection Systems to Drive the Market

Advancements in technology, such as enhanced acoustic sensors, infrared and laser technology, and radar, along with real time data analytics and GPS-based localization systems. Moreover, anti-sniper detection systems are also becoming more adaptable to different environments and are being integrated with other surveillance technologies, making them a reliable and adaptable solution for possible long-range sniper threats.

Additionally, improved threat classification with AI and machine learning algorithms can be trained to differentiate between various types of gunfire, distinguish between sniper fire and other sounds, and identify the specific characteristics of a sniper threat. AI can help systems adapt to different environments, accounting for noise, clutter, and other factors that might interfere with detection. This drives the demand for AI-integrated detection systems for better accuracy and reliability.

Market Restraints

Technological Limitations, Integration Complexity, and Privacy Concerns May Hinder the Market Growth

While advancements are being made, some systems may still face limitations in terms of detection range, accuracy, and false positive/negative rates. For instance, some systems may struggle to accurately pinpoint the sniper's location in complex urban environments or when multiple shots are fired simultaneously. Integrating ASDS with existing security infrastructure can be challenging due to compatibility issues and the need for specialized personnel for installation and maintenance.

The use of surveillance technologies such as ASDS can raise concerns about privacy violations and data security, particularly in civilian applications. Furthermore, stringent regulations and data protection laws in certain regions may restrict the deployment of these systems. Some systems may produce false alarms (false positives) or fail to detect genuine threats (false negatives), which can erode user confidence and trust in the technology.

Limited Awareness and Competition from Alternative Solutions May Lead to a Lack of Demand

Some potential users may not be fully aware of the capabilities and benefits of ASDS, leading to a lack of demand. The absence of standardized protocols and interoperability between different ASDS technologies can create integration challenges and hinder market growth. Some users may opt for alternative, less expensive security solutions, such as manned patrols or CCTV systems, depending on their specific needs and budget.

Market Opportunities

Integration of AI and ML to Achieve Accuracy and Speed of Threat Detection and Analysis Provides Growth Opportunities

The integration of Artificial Intelligence (AI) and Machine Learning (ML) offers a significant opportunity to enhance anti-sniper detection systems by improving both accuracy and speed of threat analysis. This integration enables faster processing and analysis of vast amounts of data, allowing for quicker identification of potential threats, such as sniper fire, and reducing response times. The use of AI and ML in anti-sniper systems also enables better differentiation between actual sniper fire and background noise, thereby improving accuracy.

This, in turn, can lead to more effective and reliable threat detection in various environments, including densely populated areas or those with complex acoustics. This is anticipated to drive the anti-sniper detection systems market growth during the forecast period.

Developing More Affordable and Accessible Systems to Open Opportunities in Developing Countries and for Smaller Agencies

Lowering the cost and complexity of anti-sniper systems makes them more attainable for nations with limited resources and smaller law enforcement or security agencies. These systems can significantly improve security in urban environments, protect critical infrastructure, and safeguard personnel, especially in areas with high crime rates or terrorist threats.

Anti-Sniper Detection Systems Market Trends

Rise of Urban Warfare and Asymmetric Threats, Along with Targeted Attacks, to Fuel the Need for Proactive Security Measures

The increasing occurrence of urban warfare, asymmetric threats, and targeted attacks is driving the need for proactive security measures, which in turn is creating a high demand for anti-sniper detection systems. These systems are crucial for real time threat localization, enhancing situational awareness, and improving response times during active engagements. Moreover, features such as multi-sensor fusion, AI-powered analytics, and integration with network-centric warfare platforms enhance the effectiveness and versatility of anti-sniper systems.

Increasing ASDS Application beyond Traditional Military Use, including Homeland Security, VIP Protection, and Smart City Defense

Anti-sniper systems are finding escalating applications beyond traditional military use. They are being implemented in homeland security, VIP protection details, and even smart city defense frameworks, driven by advancements in technology and a growing need for enhanced security in various settings. As urban areas become more densely populated and technologically advanced, the need for smart city defense systems is growing. Anti-sniper technology can be integrated into existing surveillance networks to enhance overall security and protect citizens.

Additionally, the market is seeing a growing demand for tailored solutions, including deployment, maintenance, and managed anti-sniper detection services.

Download Free sample to learn more about this report.

Impact of Increasing Geopolitical Tensions, Ongoing, and Recent Conflicts in Europe, the Middle East, and the Asia Pacific

Growing geopolitical strains and regional struggles, predominantly in hotspots such as the South China Sea, Eastern Europe (Russia-Ukraine), and the Middle East (Israel-Iran & Hamas), are significantly accelerating the demand for anti-sniper detection systems.

For instance, global military expenditure reached a record USD 2.4 trillion in 2024, with a substantial portion dedicated to air and missile defense.

The conflicts in these regions, especially in Russia-Ukraine, demonstrate the ongoing relevance of sniper threats in both conventional and asymmetric warfare scenarios. Resulting military forces and law enforcement agencies involved in these conflicts are increasingly seeking technology to enhance situational awareness and protect personnel from sniper attacks, driving the demand for anti-sniper detection systems.

Countries such as these are investing in modernizing their defense capabilities, including advanced surveillance and detection systems such as anti-sniper systems in response to evolving security concerns. With increased geopolitical instability, there is a greater emphasis on safeguarding critical infrastructure from potential sniper attacks, further fueling the demand for these systems.

Improvements in sensor technology, AI integration, and data analytics are making anti-sniper systems more effective and reliable, making them more attractive to potential users

SEGMENTATION ANALYSIS

By Technology

By technology, the market is divided into acoustic, optronics, infrared, AI and ML, and others (laser range finder, radar, and LiDAR).

The acoustic segment anticipated to hold an dominant the largest share in the anti-sniper detection systems market with a share of 35.36% in 2026. This is primarily due to their cost-effectiveness, ease of deployment, and ability to provide real time location data of the shooter using sound wave analysis. Acoustic technology has a long history of use in both military and law enforcement applications, making it a trusted and reliable solution. While other technologies such as optoelectronics, lasers, and infrared systems also exist, acoustic systems dominate the market due to their combination of performance, cost, and ease of use.

The AI and ML segment is growing rapidly in the anti-sniper detection system market as AI and ML algorithms can significantly enhance the speed, accuracy, and adaptability of these systems, particularly in complex environments. AI can distinguish between actual sniper fire and background noise, which is crucial in crowded or noisy environments. The growing adoption of anti-sniper systems in urban environments, public spaces, and critical infrastructure protection is driving the demand for AI-powered solutions.

The combination of AI, ML, and advanced sensor technologies is revolutionizing anti-sniper detection, making systems more efficient, reliable, and adaptable to diverse threat scenarios.

For instance, in August 2024, ZeroEyes announced that it secured USD 23 million in funding following significant growth of over 300% in the past year. The company is known for developing the only AI-powered gun detection video analytics platform that has secured the SAFETY Act Designation from the U.S. Department of Homeland Security.

To know how our report can help streamline your business, Speak to Analyst

By Platform

By platform, the market is segmented into fixed, portable, and vehicle-mounted.

The portable segment dominates and is projected to anticipated to be the fastest-growing segment during the forecast period with a share of 61.40% in 2026. The dominance is attributed to their versatility, mobility, and ease of deployment, which makes them ideal for a wide range of applications, especially in dynamic environments such as urban warfare. Their ability to quickly transport and set up in various locations, coupled with advancements in sensor technology and data processing, contributed to their widespread adoption. Additionally, some variants of portable sniper detection systems are mounted on soldiers' shoulders, which provides a tactical advantage in accurately detecting and neutralizing threats. As a result, the demand for portable detection systems is high.

- For instance, according to the U.S. Department of Defense, 420 U.S. military units are equipped with anti-sniper detection systems.

The fixed segment accounts for the second-largest market share. These systems can provide continuous, wide-area surveillance and are suitable for protecting critical infrastructure and high-value assets. They offer a reliable and cost-effective solution for long-term security needs, especially in areas where continuous monitoring is important. Beyond military applications, fixed anti-sniper systems are increasingly being used by law enforcement agencies to protect public spaces, events, and high-risk areas.

By Range

By range, the market is segmented into up to 500m, 500m-1000m, and above 1000m.

The 500m to 1000m segment anticipated to hold a dominant the largest market share with a share of 39.30% in 2026, and is anticipated to show the fastest growth, registering the highest CAGR over 2026-2034. The demand for medium-range border security, enhanced accuracy, and detection speed, along with adaptability to various operational environments and a broad spectrum of applications, drives the growth and prominence of the 500m to 1000m segment. Additionally, this range segment offers a balance between the shorter detection ranges of close-range systems and the longer, sometimes lag-prone, ranges of long-range systems.

The below 500m segment holds the second-largest anti-sniper detection systems market share. The 1000-meter segment is designed for urban environments and enclosed spaces, providing quick responses and compact solutions for close-range threats. These systems play a vital role in safeguarding critical infrastructure, public events, and high-risk areas within cities. They are often integrated with other security technologies, such as surveillance cameras and alarm systems, to create a comprehensive security solution.

By Application

By application, the market is divided into perimeter intrusion & camp detection, border protection & control, critical infrastructure detection, VIP & convoy protection, ISR & target acquisition, commercial & office spaces, hospital emergency entrances, sport venues, and others.

The perimeter intrusion & camp detection segment anticipated to hold a dominant the largest market share with a share of 24.55% in 2026. The dominance of the segment is due to its widespread application and safeguarding of critical infrastructure and high-value assets. These systems are crucial for proactively detecting unauthorized intrusions, including potential sniper attacks, thereby enhancing perimeter security and preventing unauthorized access to sensitive areas. As a result, the Perimeter Intrusion & Camp Detection segment dominates the application segment.

The ISR and target acquisition segment is anticipated to be the fastest-growing segment during the forecast period. The growth of this segment is due to its crucial role in enhancing situational awareness and enabling rapid, accurate targeting in high-threat environments. Moreover, continuous development in sensor technology, data analytics, and integration capabilities is boosting the effectiveness and adoption of these systems, resulting in the segment's fastest growth during 2026-2034.

By End User

By end-user, the market is divided into military, law enforcement & homeland security, and commercial.

The military segment holds the largest market share due to anti-sniper detection systems' role in protecting troops, bases, and convoys in combat zones and in reconnaissance and perimeter defense. These systems play a vital role in enhancing situational awareness and mitigating risks in various military operations. Rising geopolitical tensions and the prevalence of asymmetric warfare scenarios, coupled with ongoing conflict between Russia, Ukraine, Israel and Hezbollah & Iran, have increased the demand for these systems.

For instance, in September 2023, TASS Russian News Agency reported that Russian commando units involved in the special operation in Ukraine have utilized the latest robotic sniper detector, known as Sosna-N. This remote-controlled device scans the environment for optical instruments, such as sniper rifle scopes, binoculars, or targeting systems for anti-tank missiles. Once it detects such equipment, it produces an acoustic signal and emits a specialized laser beam to damage the device.

The law enforcement & homeland security segment is anticipated to show the fastest growth by registering the highest CAGR during the forecast period. Increased threats from terrorism, organized crime, and public safety concerns are driving the demand for advanced anti-sniper detection systems, coupled with urbanization, critical infrastructure protection, and counter-terrorism initiatives. Improvements in acoustic, optical, and radar-based detection technologies, coupled with the integration of AI and machine learning with surveillance cameras, are making these systems more cost-effective, reliable, and easier to deploy.

Anti-Sniper Detection Systems Market Regional Outlook

Based on region, the ASDS market is studied across North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Anti-Sniper Detection Systems Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America segment holds the largest anti-sniper detection systems market share. The North America market was valued at USD 220.8 million in 2025, capturing 38.60% of global revenue, and is estimated to reach USD 235.6 million in 2026. The dominance is driven by substantial defense spending, early adoption of advanced technologies, and ongoing military modernization programs. The region's strong focus on homeland security and counter-terrorism initiatives further fuels market growth.

The U.S. holds a leading position in the North America anti-sniper detection system market, driven by its strong economy, technological advancements, and substantial defense spending. The dominance is also due to the presence of key players in the region, such as RTX Corporation, Databuoy Corporation, Textron Systems, and others. Moreover, the U.S. has been at the forefront of adopting and integrating technologies such as AI, machine learning, and data analytics into anti-sniper detection systems. The U.S. anti-sniper detection systems market is projected to valued at USD 206.70 million by 2026.

For Instance, in August 2024, the U.S. Army awarded Logos Technologies, Elbit Systems' segment, a USD 19.4 million contract for delivering, sustaining, and operating Serenity hostile fire detection systems. Serenity uses electro-optical and acoustic sensors to locate explosive detonations and heavy weapons fired up to 6.2 miles (10 kilometers) away in any direction.

Europe

In 2025, Europe held 28.92% of the global market, reaching a valuation of USD 164.8 million, and is projected to grow to USD 175.3 million in 2026. The anti-sniper detection system market in Europe is experiencing significant growth, driven by increasing security concerns and defense spending. The market is fueled by factors such as rising geopolitical tensions, NATO defense upgrades, and growing homeland security budgets. Moreover, NATO member countries are increasing defense spending, with a promise to allocate 2% of GDP toward defense, which will result in creating a strong demand for advanced security solutions such as air-defense systems, advanced threat detection systems, and anti-sniper detection systems. The UK anti-sniper detection systems market is valued at USD 34.8 million by 2026, while the Germany anti-sniper detection systems market is valued at USD 34.5 million by 2026.

Asia Pacific

The market in Asia Pacific reached USD 145.8 million in 2025, representing 25.49% of total market revenue, and is projected to reach USD 156.6 million in 2026. Asia Pacific region is anticipated to be the fastest-growing segment during the forecast period. The growth is driven by the increasing security concerns, rising regional tensions, and significant investments in advanced security technologies by governments in the region, especially in China, India, and Japan. The growing emphasis on VIP protection and the safety of government officials, particularly at high-profile events, is further driving the demand for these systems. The Japan anti-sniper detection systems market is valued at USD 24.4 million by 2026, the China anti-sniper detection systems market is valued at USD 49.8 million by 2026, and the India anti-sniper detection systems market is valued at USD 34 million by 2026.

Rest of the World

The rest of the world comprises the Middle East & Africa and Latin America. In 2025, Rest of the World generated USD 40.6 million, contributing 7.10% to global market revenue, and is projected to grow to USD 43.3 million in 2026.

Middle East & Africa and Latin America.

Compared to North America, Europe, and Asia Pacific, the Middle East & Africa and Latin America market share is small but expanding. These regions are experiencing increased demand due to heightened security concerns, geopolitical instability, and growing defense budgets.

For instance, in October 2020, Hezbollah was reported to consider ways to hit IDF soldiers, particularly along the Lebanese border, for retaliation after it was hit by the IDF. The Hamas in Gaza were supplied with high-power sniper rifles by Iranians. In response, Rafael Advanced Defense Systems, an Israeli company, reported that the solution for this critical scenario is the vehicle-mounted and ultra-smart Land Spotter, a passive electro-optical hostile location and fire detection solution.

Competitive Landscape

Key Industry Players

Defense OEM Manufacturers Place a Strong Emphasis on Technological Advancements and Strategic Partnerships

The competitive landscape of the anti-sniper detection system market comprises key players such as RTX Corporation, Newcon Optik, Rheinmetall, and others. Key players focus on growing investment in research and development, a diversified product portfolio of anti-sniper detection systems, and strategic acquisitions. The key market players focus on business expansion strategies such as agreements, mergers, and acquisitions, product portfolio growth, and long-term modernization contracts with multinational companies included in the market.

These companies are leveraging advanced technologies, including AI and ML integration, enhanced sensor technology, and improved acoustics systems to enhance the effectiveness of their detection, tracking, and identification of targets. Overall, the focus on technological integration with AI & ML, as well as advanced radar systems, will drive significant market growth over the coming years.

LIST OF KEY ANTI-SNIPER DETECTION SYSTEMS COMPANIES PROFILED

- RTX Corporation (U.S.)

- Newcon Optik (Canada)

- WTDS Optics (China)

- MH TECH (China)

- Databuoy Corporation (U.S.)

- Thales Group

- Shooter Detection Systems LLC (U.S.)

- Transvaro elektron aletleri (Turkey)

- ACOEM Group (France)

- ZeroEyes (U.S.)

- Rostec State Corporation (Russia)

- Rheinmetall AG (Germany)

- BAE Systems (U.K.)

- Textron System (U.S.)

- Saab AB (Sweden)

- QinetiQ (U.K.)

KEY INDUSTRY DEVELOPMENTS

- In September 2024, American tech firm Base Molecular Resonance Technologies (BMRT) launched an innovative solution to identify and neutralize sniper and bomb threats.

- In October 2023, QinetiQ US was awarded a contract worth USD 125.7 million by the Secretary of Defense Strategic Capabilities Office, U.S. The contract is intended to support the Secretary of Defense Strategic Capabilities Office in its mission to develop innovative solutions to shape and counter rising security threats across the domains, including the development of anti-sniper detection systems.

- In June 2021, Robotic Assistance Devices (RAD), a wholly owned subsidiary of Artificial Intelligence Technology Solutions, Inc., agreed with EAGL Technology, Inc., to offer EAGL's Anti-Sniper Detection System (GDS) in current and upcoming RAD devices.

- In July 2020, U.S. defense company Raytheon completed the integration of its mobile gunshot detection technology into the Pentagon’s main mobile battlefield network software, which handles all combat management operations for the U.S. armed forces.

- In May 2020, Lockheed Martin Corp won a contract a ceiling USD 485 million indefinite-delivery/indefinite-quantity contract for Department of Defense and Foreign Military Sales (FMS) Low Altitude Navigation and Targeting Infrared for Night (LANTIRN), Sniper, and Infrared Search and Track (IRST) navigation pod (fixed wing) hardware production.

REPORT COVERAGE

The research report delivers a detailed analysis of the market and emphasizes key aspects such as key players, offerings, objects, and end-users of anti-sniper detection solutions. Moreover, the report offers insights into market trends, competitive landscape, market competition, product pricing, regional analysis, market players, and the market status, and highlights key industry growth. In addition to the factors stated above, the report encompasses several direct and indirect influences that have influenced market expansion in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.61% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation

|

By Technology

|

|

By Platform

|

|

|

By Range

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

According to a study by Fortune Business Insights, the global market was valued at USD 610.80 million in 2026 and is anticipated to reach USD 1,019.50 million by 2034.

The market is likely to grow at a CAGR of 6.61% over the forecast period (2026-2034).

The top players in the industry are RTX Corporation, Breda and Oto Melara, Thales Naval, Tulamashzavod, Rheinmetall, General Dynamics Corporation, Norinco, Aselsan AS, Lockheed Martin, FABA Sistemas, BAE Systems, Leonardo S.p.A, L&T, and Northrop Grumman based on parameters such as services portfolio, regional presence, and industry experience.

North America dominates the global market.

Increasing security threats, particularly sniper attacks, is a key factor driving market growth.

Integration of AI and ML to achieve accuracy and speed of threat detection and analysis provide opportunities for market expansion.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us