Air Defense Systems Market Size, Share & Industry Analysis, By Component (Command & Control Systems, Weapon Systems, Fire Control Systems, Radar Systems, and Support Equipment), By System Type (Threat Detection Systems and Countermeasure Systems), By Platform (Airborne, Naval, and Land-Based), By Range (Short Range (Below 10 km), Medium Range (10-100 km), and Long Range (Above 100 km)), By Technology (Radar & Tracking, Guidance Systems, and Directed Energy Weapons), By Deployment Mode (Containerized, Portable, and Fixed Installations), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

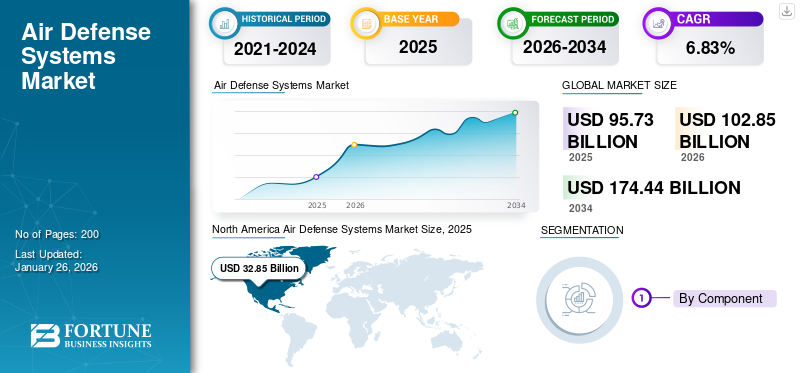

The air defense systems market size was valued at USD 95.73 billion in 2025. It is projected to grow from USD 102.85 billion in 2026 to USD 174.44 billion by 2034, exhibiting a CAGR of 6.83% during the forecast period. North America dominated the air defense systems market with a market share of 34.31% in 2025.

Air defense systems comprises of combine radar, missile interceptors, and command-and-control technologies to counter evolving aerial threats, including drones, cruise missiles, and hypersonic weapons.

Technological advancements in air defense tactical control radar technology, missile defense systems, and command & control systems are other factors driving the market growth. Integrating new technologies, including AI and ML in air defense systems, is also important to enhance the defense capabilities.

Major market players include Raytheon Technologies Corp., General Dynamics Corp, BAE Systems Plc., ASELSAN AS, Elbit Systems Ltd., and others. These companies continuously investigate effective air defense technologies, including threat detection capabilities and countermeasure systems. Key programs include growing manufacturing capacity, premeditated alliances, and enabling large-scale projects. These companies are also investing heavily in research and development to enhance existing systems, aiming to meet the demand of the defense and space industries. This includes developing quick-response air and missile defense systems and advanced radar systems to detect threats from miles away.

Download Free sample to learn more about this report.

AIR DEFENSE SYSTEMS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 95.73 billion

- 2026 Market Size: USD 102.85 billion

- 2034 Forecast Market Size: USD 174.44 billion

- CAGR: 6.83% from 2026–2034

- North America dominated the air defense systems market with a market share of 34.31% in 2025.

- The weapon systems segment is projected to dominate the market with a share of 39.39% in 2026.

- The countermeasure systems segment is expected to lead the market, contributing 65.29% globally in 2026.

North America

North America maintained a strong presence in the global market, reaching USD 32.85 billion in 2025, accounting for 34.31% share, and is expected to reach USD 35.34 billion in 2026.

Asia Pacific

Asia Pacific accounted for USD 28.89 billion in 2025, representing 30.18% of the global industry, and is expected to reach USD 31.32 billion in 2026.

Europe

Europe generated USD 19.9 billion in 2025, contributing 20.78% to global market revenue, and is projected to grow to USD 21.28 billion in 2026.

U.S.

The U.S. market is projected to reach USD 33.18 billion by 2026, supported by continued investments in missile defense programs and air defense capabilities.

Japan

The Japan market is projected to reach USD 5.19 billion by 2026, driven by continued defense modernization and strengthening air defense capabilities.

Read More

MARKET DYNAMICS

Market Drivers

Increasing Geopolitical Tension Drives Market Growth

The rising geopolitical tensions in different regions have driven governments to strengthen their military capabilities, especially in ADS. Countries emphasize national security in response to threats from state and non-state factors, substantially increasing defense expenditures. This increased attention on safeguarding airspace has stimulated manufacturing and procuring cutting-edge air defense technologies, including threat detection capabilities and countermeasure systems.

For instance, it is the third year of the Russian-Ukrainian war, and the country's air defense system protects both military and civilian sites from aircraft and missiles. Ukrainian President Volodymyr Zelenskyy stated in 2024 that the air defense system will emerge as an effective solution. Western nations have enhanced Ukraine's air defenses with a mix of various systems, including the Aspide, Aster-30, Crotale, Gepard, IRIS-T, MIM-23 HAWK, Mistral, NASAMS, Patriot PAC-2, Piorun, RBS 70, Skynex, Starstreak, and Stinger.

Advancements in Technology Boost Market Growth

Technological advancements have improved the efficiency of ADS. Developments including enhanced synthetic aperture radar systems, better missile precision, and incorporation of artificial intelligence have made these systems more efficient and dependable. This has also resulted in a growing demand for modernized air defense with extended range capabilities and improved air defense tactical control radar systems. As military forces strive to safeguard against advancing aerial dangers such as drones and loitering munitions, the adoption of state-of-the-art air and missile defense technologies has become prominent.

For example, in November 2024, the Indian Army reached a significant milestone with the development and gradual implementation of Project Akashteer. This project presents a completely automated and cohesive air defense system, providing unmatched responsiveness and dependability. The phased induction of Akashteer is currently in progress. Out of the total need for 455 systems, 107 are delivered, and another 105 are anticipated to be delivered by 2025 end.

Market Restraints

High Cost of Development and Maintenance Restrains Market Expansion

A significant challenge to the market is the substantial investments linked to these systems' development, deployment, and continuous maintenance. This financial strain can pressure military budgets, particularly for smaller countries or those with economic difficulties. As a result, this financial aspect restricts the number of systems that can be acquired, hindering the overall air defense system market growth.

Political and Regulatory Frameworks Pose Challenges to Market Growth

The air defense industry frequently faces complex political and regulatory landscapes that can hinder market progress. Export restrictions and global treaties may hinder nations seeking cutting-edge defense technologies. Moreover, changes in government policies related to defense budgets can influence long-term agreements and collaborations in the aerospace and defense industries.

Market Opportunities

Developing Nations are Investing Heavily in Air Defense Capabilities, Providing Growth Opportunity

Developing nations are enhancing their military capabilities due to the critical role of ADS in contemporary warfare. These rising markets offer substantial growth opportunities for air defense system manufacturers and vendors. For instance, in January 2025, the Serbian Defense Agency announced that the FK-3, manufactured in China, is officially operational with the Serbian Air Force. This development represents a significant achievement for Beijing, which has been aiming to increase its influence in the Balkan nation in recent years. The 250th Air Defense Missile Brigade is equipped with an anti-aircraft missile system that includes vehicles featuring a command center, missile launchers, and synthetic aperture radar equipment. As geopolitical circumstances evolve and nations seek to bolster their military strength, the need for sophisticated air defense solutions in these areas is expected to increase.

Air Defense Systems Market Trends

Shift toward Modular Air Defense Systems Drives Market Growth

The shift toward modular ADS is becoming a standard choice by nations' defense organizations. Modular systems enable military forces to tailor and adjust their capabilities to particular threats. They provide configuration flexibility, making upgrades and integration with various platforms straightforward. This adaptability guarantees countries can respond more efficiently to new challenges in the defense environment.

For instance, in May 2025, Swedish Defence Materiel Administration (FMV) awarded Saab a contract worth USD 166 million to provide the Sea Ceptor air defence system from MBDA for the five Visby-class corvettes of the Swedish Navy.

Focus on Counter-UAV Systems is a Notable Trend Aiding in Market Expansion

As Unmanned Aerial Vehicles (UAVs) become more dominant in military operations, air defense systems are increasingly tailored to address these emerging threats. The importance of creating systems that can detect, track, and neutralize UAVs highlights the necessity for cutting-edge technology in air defense. This shift shows the evolving warfare landscape, emphasizing the importance of proactively integrating counter-UAV features into current air defense structures.

Download Free sample to learn more about this report.

For instance, in January 2025, Elbit Systems Ltd. secured a contract valued at around USD 60 million to provide its multi-layered Counter Unmanned Aerial Systems (C-UAS) to a European NATO member. This contract is set to be executed over a period of three years. Additionally, in May 2024, BEL entered into a contract with the Army for an indigenous counter-drone system, securing orders totaling approximately USD 66.89 million. The contract is for the Integrated Drone Detection and Interdiction System (IDDIS). This system, which was developed collaboratively by the Defence Research and Development Organisation (DRDO) and BEL, represents a major achievement under the Government of India's Make in India initiative.

Impact of Wars

Impact of Russia-Ukraine War

The Russia-Ukraine war has significantly influenced the global air defense strategies, exposing the problems of traditional systems against low-cost, mass drone attacks and highlighting the need for adaptive, multi-layered defense systems. Ukraine’s innovative use of affordable drones to attack deep into Russia's territory has demonstrated how asymmetric tactics have neutralized high-value military assets. In contrast, Russia's drone capacity movements have overwhelmed costly Ukrainian interceptors. This conflict has driven both nations to explore cost-effective solutions, including electronic scanning and AI-based systems, signaling a broader global shift toward modernized, resilient, and tech-integrated air defense.

Impact of India-Pakistan War

In May 2025, tension between India and Pakistan flared after a devastating terror attack in Pahalgam claimed 26 innocent lives. India responded swiftly with Operation Sindoor, launching precision missile strikes deep into Pakistan and displaying the growing reliance on indigenous air defense technologies such as the Akshteer System, which intercepted every incoming drone. The skies over both nations rose with the activity of fighter jets, drones, and missiles.

During these conflicts, in May 2025, India’s Ministry of Information & Broadcasting reported that the Akashteer air defense system achieved a remarkable interception rate, neutralizing over 600 Pakistani drones and missiles. The S-400 system also made headlines by downing a Pakistani AWACS aircraft at 314 km, while BrahMos missiles were used in combat for the first time. Pakistan deployed Bayraktar TB2 drones, all intercepted by India's defenses. It also claimed strikes on Indian S-400 units using JF-17 Block 3 jets, though India denied any damage.

Moreover, in May 2025, India’s Ministry of Information & Broadcasting reported,

- India targets approximately USD 35.04 billion in defense production by 2029, strengthening its place as a global defense manufacturing hub.

- The private sector contributes 21% to total defense manufacturing, increasing innovation and efficiency.

- A robust defense industrial base includes 16 DPSUs, over 430 licensed companies, and approximately 16,000 MSMEs, strengthening indigenous production capabilities.

- 65% of defense equipment is now manufactured domestically, a significant shift from the earlier 65-70% import dependency, showcasing India's self-reliance in defense.

These conflicts highlighted the importance and reliance of nations on ADS.

Impact of Israel-Hamas-Houthi War

The Ukraine war and the Israel-Hamas-Hizbullah conflicts have dramatically accelerated global investment in ADS. Israel’s reliance on Iron Dome and Iron Beam lasers has showcased how modern threats demand layered, tech-driven responses. Nations worldwide are now prioritizing cost-effective interception systems against drones and missiles, reshaping the defense landscape.

Israel reported the first successful use of laser defense in combat. At the same time, Ukraine continues to receive and test NATO-supplied systems such as IRIS-T and NASAMS, validating their effectiveness in live conflict zones.

Major arms manufacturers have observed revenue spikes since 2024 and in the first quarters of 2025.

SEGMENTATION ANALYSIS

By Component

Weapon Systems Dominates with Frequent Technological Advancement and Defense Modernization Programs

The market is segmented by component into command & control systems, weapon systems, fire control systems, radar systems, and support equipment.

Weapon systems dominate the component segment. Swift progress and breakthroughs in missile technology, combined with the incorporation of artificial intelligence and automation into weapon systems, fuel the segment’s expansion. Moreover, countries invest in sophisticated weapon systems to bolster their defense capabilities. The weapon systems segment is projected to dominate the market with a share of 39.39% in 2026.

For instance, in January 2025, Taiwan's Ministry of National Defense (MND) finalized three agreements to procure the Kongsberg/Raytheon National Advanced Surface-to-Air Missile System (NASAMS) along with two mobile radars from the U.S. These agreements, totaling over USD 724.8 million, are set to bolster the air defense and surveillance capabilities of the Republic of China (ROC) armed forces.

Radar systems are anticipated to show the fastest growth with the highest CAGR during the forecast period. These systems are vital in detecting, tracking, and identifying possible aerial threats, enabling quick responses and engagements. The need for advanced radar systems is on the rise, fueled by a growing demand for situational awareness and the incorporation of cutting-edge technologies, including 3D radar and phased array systems.

For instance, in December 2024, the Presidency of the Republic of Türkiye awarded Aselsan a contract worth USD 170 million to provide air defense radar systems, with deliveries scheduled from 2026 to 2031.

By System Type

Threat Detection Systems to Witness Fastest-Growth with Nations Focusing on enhancing their Air Defense Radar Capabilities

The market is divided by system type into threat detection systems and countermeasure systems.

The threat detection systems segment is projected to grow with the highest CAGR from 2025 to 2032. These systems consist of radar and EO/IR systems, critical in detecting and evaluating airborne threats, enabling prompt counteractions, and improving overall safety. Rising fear of terrorism, the spread of advanced aerial weaponry, and the demand for better situational awareness in military and civilian environments drive the expansion of threat detection systems. Advancements in sensor technology, artificial intelligence, and data analytics are also propelling innovations and boosting the segmental growth, making it an important part of thorough air defense strategies.

Countermeasure systems dominated the segment in 2024. This segment includes missile defense systems, anti-aircraft systems, and counter-UAS/C-RAM systems. Missile defense systems intercept and neutralize incoming projectiles, anti-aircraft systems focus on safeguarding airspace from enemy aircraft, and Counter-Unmanned Aerial Systems (C-UAS), along with Counter-Rockets, Artillery, and Mortar (C-RAM) systems, all of which are important components of modern-day defense strategies. Increasing geopolitical tensions and the growing need for sophisticated military capabilities mainly fuel the expansion of the countermeasure systems sector. Nations are investing substantially in cutting-edge defense technologies to protect their airspace from emerging threats, especially ballistic missiles and Unmanned Aerial Vehicles (UAVs). The countermeasure systems segment is expected to lead the market, contributing 65.29% globally in 2026.

For instance, in March 2025, Zen Technologies Limited announced that it had secured a contract worth around USD 17.73 million from the Indian Defence Ministry. This contract provides Integrated Air Defence Combat Simulators (IADCS) for the Army’s L70 air defence guns.

By Platform

Land-Based ADS Dominates by Providing a Reliable Solution for Airborne Threats

Based on platform, the market is sub-divided into airborne, naval, and land-based.

The land-based segment holds the largest market share and is anticipated to show the fastest growth during the forecast period. This dominance is attributed to the growing requirement for countries to safeguard their borders and defend essential infrastructure against a range of aerial dangers, including drones, missiles, and other airborne attacks. For instance, in May 2025, the conflict between India and Pakistan showed the importance of ADS in countering aerial threats. Land-based systems provide strategic benefits, including mobility, cost efficiency, and the ability to cover extensive geographical regions, making them important for nations prioritizing national security. Technological progress has enhanced the performance and effectiveness of land-based platforms, boosting their adoption rates. The land-based segment is expected to account for 59.05% of the market in 2026.

For instance, in January 2025, Raytheon, a business under RTX, secured a contract worth USD 946 million to provide Romania with more Patriot air and missile defense systems. This contract includes fire units, including radars, control stations, and missiles.

Airborne systems are anticipated to show significant growth during the forecast period. This development is primarily driven by a growing focus on multi-domain operations and the need for adaptable platforms to tackle threats and offer reconnaissance and surveillance functions. Airborne systems, typically equipped with airborne radar systems and missile technologies, facilitate quick reactions to new threats in ever-changing environments, rendering them crucial for contemporary military strategies. As nations aim to upgrade their ADS and enhance overall operational preparedness, the demand for sophisticated airborne systems is projected to increase.

For instance, in March 2025, BIRD Aerosystems, recognized as a global leader in defense technology, successfully obtained a contract to provide its Airborne Missile Protection System (AMPS), which includes the SPREOS (Self-Protection Radar Electro-Optic System) DIRCM, to another African Air Force. This contract provides a complete self-protection suite for Mi-17/8 and Mi-35 helicopters, ensuring better survivability against missile threats.

To know how our report can help streamline your business, Speak to Analyst

By Range

Long Range (Above 100 km) ADS Leads as Countries want to Eliminate Threat Before it Enters a Nation’s Airspace

By range, the market is sub-segmented into short range (below 10 km), medium range (10-100 km), and long range (above 100 km).

Long-range systems dominate the market. This segment features S-300, S-400, and THAAD (Terminal High Altitude Area Defense), all of which significantly protect nations from various airborne threats, including ballistic missiles and Unmanned Aerial Vehicles (UAVs). The long range (above 100 km) segments is anticipated to hold a dominant market share of 51.71% in 2026.

Their modern capabilities, encompassing target detection, tracking, and interception, contribute to their high price tag. However, countries are willing to invest in these systems to maintain a strong national defense and deterrence strategy. The strategic importance of these systems reinforces their market leadership and drives ongoing technological advancements to address emerging threats. For instance, in May 2025, the S-400 was part of Operation Sindoor and is known in India as “Sudarshan Chakra,” and played a crucial role for India in defending its territory against Pakistan's drone and missile attacks.

For instance, in February 2024, the Missile Defense Agency (MDA) awarded Lockheed Martin Corporation a follow-up development contract worth USD 2.8 billion for the Terminal High Altitude Area Defense (THAAD) Weapon System. This indefinite-delivery/indefinite quantity (IDIQ) contract aims to enhance the THAAD Weapon System's capabilities over the next five years, with the possibility of two extensions, allowing for a total performance period of up to 10 years.

The medium-range segment is anticipated to be the fastest-growing segment during the forecast period. The rise in demand can be linked to the growing utilization of medium-range systems in the fight against Unmanned Aerial Systems (UAS) and their proven effectiveness in mobile warfare situations.

Prominent examples of these medium-range systems are the Iron Dome, Barak-8, and HQ-22. The Iron Dome, in particular, has achieved worldwide commendation for its exceptional capability to intercept incoming rockets, particularly in conflict areas, accurately. As countries focus on adaptable defense strategies to tackle asymmetric warfare, the attractiveness of medium-range defense systems is rising, resulting in heightened investments in research and development within this field.

For instance, in January 2025, Rafael Advanced Defense Systems announced that it had signed a major contract with the Israeli Ministry of Defense (IMOD) to increase the production of Iron Dome interceptors. This expansion is supported by the U.S. aid package established after the recent conflict. In April 2024, the U.S. Congress approved an aid package totaling USD 8.7 billion. USD 5.2 billion is designated for improving Israel’s air and missile defense systems, including Iron Dome, David’s Sling, and the cutting-edge Laser Defense System.

By Technology

Guidance Systems is Gaining Traction due to Rapid Technological Advancements in AI and ML

By technology, the market is classified into radar & tracking, guidance systems, and directed energy weapons.

Guidance systems is anticipated to be the fastest-growing segment from 2025 to 2032. This anticipated growth is associated with rapid development in precision engagement technologies, improving targeting precision and operational efficiency. Important technologies propelling this sector include infrared and radio-frequency band systems that improve target acquisition, laser-guided systems that provide precise strike capabilities, and GPS/INS (Global Positioning System/Inertial Navigation System) technologies that guarantee dependable navigational guidance. Additionally, the advancement of active and semi-active radar homing systems is boosting the effectiveness of munitions, increasing their adaptability in various military applications.

The radar and tracking segment dominates as these systems help in target detection, fire control, and battle management. Advanced systems employ cutting-edge signal processing and data fusion methods to effectively detect and monitor potential threats in real time, thereby improving situational awareness on the battlefield, resulting in successful target detection and neutralization. Moreover, every air defense system (SHORD, MRAD, LRAD) requires radar integrations, driving the segment's growth and dominance in the market.

For instance, in March 2025, the Ministry of Defense, India, awarded Bharat Electronics Ltd. a contract worth USD 333.40 million to procure Low-level Transportable Radar, LLTR (Ashwini). LLTR (Ashwini) is an active electronically scanned phased array radar based on state-of-the-art solid-state technology. The radar can track aerial targets from high-speed fighter aircraft to slow-moving targets such as UAVs and helicopters.

By Deployment Mode

Fixed-Installation Dominates as they are Installed at Strategic Locations, Providing a Reliable Solution with a Wide Coverage Area

Based on deployment mode, the market is categorized into containerized, portable, and fixed installations.

The fixed-installation segment dominates the market owing to the reliability and wide coverage offered by fixed systems, which make them an important part of national defense strategies. These installations are usually positioned in key locations, enabling improved surveillance and interception abilities against aerial threats. Moreover, high-cost and long-range systems such as S-400 and THAAD are generally fixed-installation systems.

For instance, in June 2024, the Norwegian government ordered new NASAMS from Kongsberg Defence & Aerospace (KONGSBERG) to enhance the nation’s defense capabilities against aerial threats. This contract is valued at around USD 448.76 million, including options, with deliveries anticipated to begin in 2027.

The portable segment is anticipated to showcase the fastest growth during the forecast period. These systems are mainly MANPADS, or mounted on light tactical vehicles. Its growth is fueled by the rising need for multipurpose and flexible air defense solutions that can rapidly deploy in different operational environments. Moreover, these systems are helpful for military operations in changing environments where quick responses are important. Their mobility enables deployment across various terrains and circumstances, making them attractive to defense forces globally.

Air Defense Systems Market Regional Outlook

Geographically, the market is segmented into Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa.

North America

North America Air Defense Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America maintained a strong presence in the global market, reaching USD 32.85 billion in 2025, accounting for 34.31% share, and is expected to reach USD 35.34 billion in 2026. North America is the second-largest player in the market due to its strong defense industrial base, ongoing investments in missile modernization, and presence of leading defense companies such as Northrop Grumman, L3Harris Technologies Inc., General Dynamics Corp., Lockheed Martin, and others. For instance, in May 2025, the U.S. announced that it had selected a design for the USD 175 billion Golden Dome missile defense shield and named a Space Force general to head the program to block threats from China and Russia. The U.S. market is projected to reach USD 33.18 billion by 2026.

Additionally, each year the U.S. spends about 4.4% of its military budget on its ADS capabilities, For instance, in 2023 and 2024, Program Acquisition Cost by Weapon System Missile Defense Programs in the Annual Budget was about 12.3 billion and 14.8 billion, respectively, and in 2025, it is about 13.5 billion.

Europe

In 2025, Europe generated USD 19.9 billion, contributing 20.78% to global market revenue, and is projected to grow to USD 21.28 billion in 2026. Europe holds a significant air defense systems market share, with France, Germany, and the U.K. prioritizing their air defense capabilities to address changing security threats. NATO's commitment to collective defense has resulted in heightened investments in air defense systems among its member nations. Additionally, initiatives, including the European Sky Shield Initiative, are being developed to enhance regional air defense networks, promoting market expansion. The UK market is projected to reach USD 3.18 billion by 2026, while the Germany market is projected to reach USD 4.28 billion by 2026.

For instance, in March 2025, the Defense Equipment & Support department of the British Ministry of Defense placed an order valued at as much as USD 2 billion with Thales to supply more than 5,000 Lightweight Multirole Missiles defense systems on behalf of the Ukrainian government.

Asia Pacific

Asia Pacific Segment Dominates with Ongoing Regional Tensions and Presence of Developing Nations

The Asia Pacific market accounted for USD 28.89 billion in 2025, representing 30.18% of the global industry, and is expected to reach USD 31.32 billion in 2026. The Asia Pacific holds the largest ADS market, fueled by substantial investments in military upgrades and ongoing regional conflicts. China, India, Australia, and Japan are strongly improving their defense capabilities, resulting in a heightened demand for sophisticated air defense technologies. The strategic importance of protecting airspace and addressing possible threats from adjacent nations has encouraged the regional growth in this industry. Moreover, collaborations and alliances with well-established defense manufacturers are improving local production capabilities. The Japan market is projected to reach USD 5.19 billion by 2026, the China market is projected to reach USD 10.33 billion by 2026, and the India market is projected to reach USD 6.41 billion by 2026.

For instance, in February 2025, Thales and Bharat Dynamics Limited (BDL) signed an agreement to supply Laser Beam Riding Man Portable ADS (LBRM). This initiative is in direct response to a request from the Indian Government to enhance India’s air defense capabilities.

Latin America and the Middle East & Africa

The Middle East air defense market is showcasing substantial growth. Nations including Saudi Arabia, the UAE, and Israel are investing in cutting-edge defense technologies to address regional threats and enhance national security. The current geopolitical situation and persistent conflicts between Israel-Gaza and the Hamas Group have increased the focus on ADS, such as missile defense and surveillance technologies, driving the market's growth. In 2025, Middle East & Africa represented USD 10.39 billion, accounting for 10.86% of the worldwide market, and is projected to grow to USD 11.07 billion in 2026.

For instance, in January 2025, Saudi Arabia announced the acquisition of 39 Pantsir-S1M air defense systems manufactured in Russia through a discreet transaction valued at approximately USD 2.3 billion.

The Latin American air defense systems market is growing slowly, with Brazil and Colombia starting to increase their defense investments. Although military budgets in this area are typically lower than in other regions, there is an increasing awareness about the significance of air defense capabilities. Collaborations with international defense firms and a heightened emphasis on modernization are expected to propel growth. Latin America contributed 3.86% to the global market in 2025, with a valuation of USD 3.7 billion, and is projected to reach USD 3.85 billion in 2026.

Africa’s air defense systems market is growing gradually, characterized by limited yet increasing investments in defense capabilities. South Africa and Nigeria are investigating avenues to improve their air defense systems in light of new security challenges. Despite ongoing budget limitations, regional collaborations and the pursuit of joint defense initiatives may offer prospects for future growth.

Competitive Landscape

Key Industry Players

Major Players are Driving Growth through Advanced Technology Integration and Strategic Defense Contracts

The air defense systems market combines established companies and innovative newcomers. Prominent firms, including Northrop Grumman, L3Harris Technologies, and Rafael Advanced Defense Systems, are dedicated to creating advanced technologies to secure their positions in the market. These companies actively pursue strategic partnerships and collaborations to boost their capabilities and broaden their product lines. Furthermore, continuous investments in research and development are essential for fostering innovation and enhancing system performance in response to changing defense requirements.

The market is dominated by several key players, each emphasizing innovation, strategic alliances, and capacity growth to consolidate their market positions. Key players are Northrop Grumman (U.S.), L3Harris Technologies Inc. (U.S.), BAE Systems (U.K.), Rafael Advanced Defense Systems Ltd. (France), Lockheed Martin Corporation (U.S.), Israel Aerospace Industries Ltd. (Israel), and others. The focus on environmental sustainability is gaining traction, compelling competitors to create propulsion systems that are efficient and eco-friendly. As the demand in defense and commercial space sectors continues to grow, the competitive landscape is anticipated to shift, resulting in further consolidation and advancements in air defense technologies.

LIST OF KEY AIR DEFENSE SYSTEMS COMPANIES PROFILED

- BAE Systems Plc. (U.K.)

- Elbit Systems Ltd. (Israel)

- General Dynamics Corp. (U.S.)

- Hanwha Aerospace Co., Ltd. (South Korea)

- Israel Aerospace Industries Ltd. (Israel)

- Kongsberg Gruppen ASA (Norway)

- L3Harris Technologies Inc. (U.S.)

- Leonardo S.P.A. (Italy)

- Lockheed Martin Corp. (U.S.)

- Northrop Grumman Corp. (U.S.)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Raytheon Technologies Corp. (U.S.)

- Rheinmetall AG (Germany)

- Saab AB (Saab AB)

- Thales Group (France)

- The Boeing Co. (U.S.)

- MBDA (France)

- ASELSAN AS (Türkiye)

- Bharat Dynamics (India)

KEY INDUSTRY DEVELOPMENTS

- November 2024: Anduril received a USD 200 million, five-year Indefinite Delivery/Indefinite Quantity (IDIQ) contract from the U.S. Marine Corps to create and supply a Counter Unmanned Aerial System (CUAS) Engagement System (CES) for the Marine Air Defense Integrated System (MADIS). The MADIS CES Program of Record aims to deliver advanced, expeditionary CUAS capabilities to safeguard the Marine Air Ground Task Force (MAGTF) against emerging aerial threats.

- November 2024: Japan’s Ministry of Defense awarded a contract worth approx. USD 368 million to Mitsubishi Heavy Industries to develop the Glide Phase Interceptor (GPI), a next-generation missile defense system, specifically designed to shoot down hypersonic missiles.

- September 2024: Saab AB received a contract by the Swedish Defence Materiel Administration (FMV), which operates under the Swedish defense department, to provide the Giraffe 1X radar for one of Sweden's Ground-Based Air Defense (GBAD) systems. This contract with the FMV is set to last until 2027 and is valued at around USD 68 million.

- August 2024: Anduril Industries secured a contract worth USD 249.9 million to provide enhanced air defense capabilities across various services for the Department of Defense. This agreement includes delivering over 500 Roadrunner-M systems and extra Pulsar electronic warfare features to counter the increasing risk posed by Unmanned Aerial Systems (UAS) attacks on U.S. forces. Deliveries are set to commence in the fourth quarter of 2024 and will extend through the end of 2025.

- June 2024: The U.S. Army entered into a contract worth USD 4.5 billion with Lockheed Martin to manufacture 870 Patriot Advanced Capability-3 Missile Segment Enhancement (PAC-3 MSE) missiles, as reported on the U.S. Army's official website.

- January 2024: L3Harris Technologies received a contract worth approx. USD 919 million to design and build 18 infrared space vehicles for the Space Development Agency’s (SDA) Tranche 2 (T2) Tracking Layer program that will provide near-global missile warning and tracking coverage.

REPORT COVERAGE

The research report delivers a detailed analysis of the market and emphasizes key aspects such as key players, offerings, objects, and end-users of air defense systems. Moreover, the report deals with insights into market trends, competitive landscape, market competition, product pricing, regional analysis, market players, competition landscape, and the market status, and highlights key industry growth. In addition to the factors stated above, the report encompasses several direct and indirect influences that have subsidized the sizing of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.83% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

|

|

By System Type

|

|

|

By Platform

|

|

|

By Range

|

|

|

By Technology

|

|

|

By Deployment Mode

|

|

|

By Region

|

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 95.73 billion in 2025 and is anticipated to reach USD 174.44 billion by 2034.

The market will likely grow at a CAGR of 6.83% over the forecast period (2026-2034).

The top players in the market are ASELSAN AS, BAE Systems Plc., Elbit Systems Ltd., General Dynamics Corp., Hanwha Aerospace Co. Ltd., Israel Aerospace Industries Ltd., Kongsberg Gruppen ASA, L3Harris Technologies Inc., Leonardo S.P.A., Lockheed Martin Corp., Northrop Grumman Corp., Rafael Advanced Defense Systems Ltd., Raytheon Technologies Corp., Rheinmetall AG, Saab AB, Thales Group, The Boeing Co., MBDA, and Bharat Dynamics.

Asia Pacific dominates the market by holding the largest share of 30.18% in 2025

Increasing geopolitical tension and advancements in technology are driving the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us