Anti-Submarine Warfare (ASW) Market, Size, Share & Industry Analysis, By Offering (Hardware, Software & Services), By Component (Sonar Systems, Underwater Sensors, Torpedoes, & Others), By Deployment Mode (Shipborne, Airborne, & Submarine-Launched Systems, & Others), By Range (Short-Range, Medium-Range & Long-Range ASW Systems), By Installation Type (Line Fit & OEMs, and Upgrades & Retrofitting), By Technology (Active Sonar Technology, Passive Sonar Technology, & Others), By Platform (Naval Surface Ships, Submarines, Aircrafts, UAVs, UUVs & Others), By End User, & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

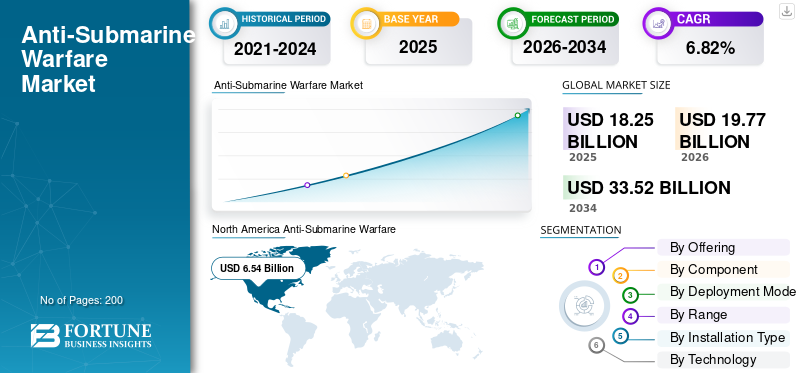

The global anti-submarine warfare (ASW) market size was valued at USD 18.25 billion in 2025. The market is projected to grow from USD 19.77 billion in 2026 to USD 33.52 billion by 2034, exhibiting a CAGR of 6.82% during the forecast period.

Capabilities range across several types and modes, including surface ships (frigates, destroyers, and corvettes), rotorcraft (helicopters), fixed-wing planes (maritime reconnaissance planes), submarines and more recently, unmanned underwater vehicles. The industry is known to cover the entire technology gamut, ranging from sonar systems (both passive and active modes), towed detection schemes, lightweight anti-submarines torpedoes and acoustic processing with artificial intelligence systems, more advanced command and control systems which facilitate coordination and prompt action against threats in the oceanic domains.

ASW capabilities are strategically focused on areas where high-density maritime trading routes exist, territorial waters are contested, and the submarine proliferation ratio is witnessing an increase. The ASW industry is witnessing rapid growth owing to overriding macroeconomic/geopolitical stimulators. Advances being made in the field of artificial intelligence-based acoustic signal processing and autonomous underwater vehicle integration are paving way for a radical improvement in capabilities at dramatically lower operating expenses.

The market for ASW is moderately consolidated, and is dominated by the presence of major contractors such as Raytheon Technologies, Lockheed Martin, BAE Systems, Thales Group, General Dynamics and so on.

Download Free sample to learn more about this report.

Anti-Submarine Warfare Market Trend

Quantum Computing Integration and Emerging Quantum Sensor Development is Emerging Market Trend

Quantum computing advancement as per military applications involves fundamental improvements in sonar data processing, navigation accuracy and sensor sensitivity by means of quantum mechanical phenomena. Research institutions working on naval submarines study the optimization of quantum algorithms for vast acoustic datasets, enhancing target detection and classification through parallel processing capabilities of quantum mechanics that enable exploring multiple acoustic signature patterns that are incompatible with classical computing architectures.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Driver

Critical Maritime Infrastructure Protection and Strategic Chokepoint Vulnerability Drives Market Growth

The Anti-Submarine Warfare (ASW) market growth comes from operational requirements regarding the need to defend vital sea routes and energy assets using sophisticated underwater threat detection systems. The Energy Information Agency of the U.S. reported that a total of 20 percent of world oil output about 20 million barrels a day is carried through the Strait of Hormuz, thus requiring this route to be a high priority concern in global energy security. Furthermore, there are estimated to be only 30 submarines in operation in the Indo-Pacific currently, but there are plans to have 250 in operation in Asian waters by 2030, thereby producing exponentially increasing demands related to detection and neutralization in maritime domain awareness.

Market Restraint

Acquisition Cost Escalation and Extended Procurement Timelines Hamper Market Growth

Market expansion is deterred due to constraint that exist in the current processes of acquisition in the defense sector. The cost analysis program on acquisition conducted by the Institute for Defense Analyses identified the cost growth phenomenon in major defense acquisition was above the 30 percent threshold. It also identified cases that spiked up to 70 percent increases in the cost of acquisition during the execution of the program. The Congressional Research Service analysis on the field of defense procurement identified the tendency toward contract extension of 5 years or more.

Market Opportunities

Unmanned Undersea Vehicle Proliferation and AI-Integrated Autonomous Operations Catalyze the Market Opportunities

The landscape of strategic opportunities is primarily driven by autonomous platform integration, which is increasingly becoming the reality with transition of naval forces' ASW systems of manned asset dependence to autonomous underwater vehicle networks. The success of the complete in-water test of the DARPA Manta Ray extra-large UUV carried out by Northrop Grumman in February-March 2024 showed the reality of gliding propulsion based on buoyancy, low-power hibernation modes with anchoring at the bottom of the sea, and mission management systems, allowing for autonomous underwater performance without the presence of human logistics. Contracts for the development of large underwater drones were award to Anduril Industries, Oceaneering International, and Kongsberg Discovery by the U.S. Defense Innovation Unit in the year 2025.

Market Challenges

Escalating Submarine Acoustic Stealth and Technological Arms Race in Acoustic Superiority Hinder Market Growth

The ASW market is facing challenge of competing against designs that have been developed to counter existing means of detection as a result of new submarine designs and operation concepts that specifically aim to counter existing means of detection by using innovative means of acoustic stealth. The Director of U.S. Navy Undersea Warfare and the Program Executive Officer of Submarines has vowed to retain an acoustic superiority advantage but has accepted that existing submarine nations are attaining acoustic stealth parity using electric propulsion systems and sound-reducing paint.

Segmentation Analysis

By Offering

Exponential Expansion of Artificial Intelligence and Machine Learning Integration Propels software Segmental Growth

Based on the offering, the market is divided into Hardware, Software, and Services

The software segment is estimated to be fastest growing during the forecast period. The growth is driven by an unprecedented level of growth with the advent of revolutionary artificial intelligence and machine learning models in acoustic signal processing, threat classification, and unmanned platform control. The use of attention-based deep neural networks within sonar processing systems has achieved a 98% level of precision and recall in the detection and classification of vessels, which was unachievable with the help of traditional signal processing techniques.

The hardware segment is accounted for the largest Anti-Submarine Warfare market share of 55.55% in year 2025 and estimated to grow at a 5.92% CAGR.

By Component

Autonomous Underwater Vehicle Proliferation and Distributed Sensor Network Expansion Boosts Underwater Sensors Segmental Growth

Based on the component, the market is divided into Sonar Systems, Underwater Sensors, Torpedoes, Depth Charges & ASW Rockets, Decoys and Countermeasure Systems, Underwater Communication Systems, and Others

The underwater sensors segment is experiencing fastest growing during the forecast period due to paradigm shifts to and a focus on autonomous platform architectures requiring the use of advanced sensor technology that is inapplicable to traditional centralized sonar architectures. The unprecedented adoption rate and growth of Autonomous Underwater Vehicles (AUVs), and Remotely Operated Vehicle (ROV) technology, as adapted by the Military, Oceanographic, and Renewable Energy sectors, has also contributed to the unprecedented growth rate for sensor technology platforms requiring the capability to function independently without constant power and communication connectivity, impractical for traditional sonar systems architectures.

The sonar system sub-segment is accounted for the largest market share of 30.23% in 2025 with a CAGR of 7.76%.

By Deployment Mode

Growing Requirements for Extended Deep-Ocean Surveillance and Submarine Threat Detection Leads to Unmanned/Autonomous Systems Segment Growth

Based on the deployment mode, the market is divided into Shipborne Systems, Airborne Systems, Submarine-Launched Systems, Unmanned/Autonomous Systems, and Fixed Coastal/Seabed Installations.

The unmanned/autonomous system segment is estimated to be the fastest growing during the forecast period. This rapid acceleration represents a fundamental realization by naval authorities of the operational benefits of autonomous platforms to achieve asymmetric operations in terms of eliminating risks to personnel and extensive mission duration beyond the limitations imposed by crewed platforms, rapid introduction of technology to autonomous platforms with the aid of module payloads and cost-effectiveness of operating multiple autonomous platforms in replacement of valuable crewed vessels.

Shipborne systems segment is accounted for the largest market share of 34.79% in year 2025 and grow at a CAGR of 6.45% during the forecast period.

By Range

Strategic Ocean-Wide Surveillance Infrastructure Expansion Drives Long-Range ASW Systems Segment Growth

Based on the range, the market is divided into Short-Range ASW Systems, Medium-Range ASW Systems, and Long-Range ASW Systems.

The long-range anti-submarine warfare systems segment is projected to be the fastest growing during the forecast period of 2026-2034. The growth is driven by extended range detection capability of submarines is vital to the assumed undersea domain awareness over vast distances that are not feasible by platform-centric ranges. This growth pattern corresponds to the strategic requirement for the detection of an ever more technically sophisticated foreign submarine presence operating within extended ranges and deep sea environments that the traditional medium frequency capability cannot maintain.

The medium-range ASW systems accounted for the largest market share 41.81% and grow at a CAGR of 6.92%.

By Installation Type

Cost-Effective Platform Modernization Economics Drives Upgrades and Retrofitting Segment Growth

Based on the installation type, the market is divided into Line Fit & OEMs and Upgrades & Retrofitting

The upgrades and retrofitting segment is estimated to be the fastest growing during the forecast period. This growth reflects strategic defence establishment prioritization of extending the service life of aging platforms through systematic modernization, which is incompatible with sustained new-build procurement at constrained defence budgets. Instead, economic advantage is proving compelling for navies facing budget constraints to move toward extending the operational life of their existing platform inventories through advanced technology insertion rather than accelerating new-build acquisition programs.

The Line Fit & OEMs segment is accounted for the largest market share of 59.53% and grow at a CAGR of 6.33%

By Technology

Exponential Acoustic Data Volume Expansion and Real-Time Processing Requirement Leads of AU & ML Analytics Segmental Growth

Based on the technology, the market is divided into Active Sonar Technology, Passive Sonar Technology, Acoustic Signal Processing, Electronic Warfare for ASW, AI & ML Analytics, Data Fusion and Sensor Integration and Others

The AI & ML analytics sub-segment is projected to be the fastest growing during the forecast period. Passive sonar systems produce more acoustic data than humans can analyze, combining environmental noise, machinery sounds, and biological signals across multiple naval platforms which creates the multiple growth opportunity for the segmental growth.

The passive sonar technology accounted for the largest market share of 20.66% and grow at a CAGR of 5.74%.

By End User

To know how our report can help streamline your business, Speak to Analyst

Strategic Submarine Proliferation and Existential Threat Requirement Catalyze Naval Forces (navies) Segmental Demand

Based on the End User, the market is divided into Naval Forces (Navies), Coast Guards, Defense Contractors, and Allied Military Forces

Naval forces (navies) segment is estimated to be the fastest growing during the forecast period with a highest CAGR of 7.26% and also accounted for the largest Anti-Submarine Warfare (ASW) market share of 75.70% in year 2025. The growth is recognized as existential risks for naval operations, maritime trade, and strategic deterrence that demand specific detection and engagement infrastructure that cannot be characterized by other end use categories (coast guard organizations, research organizations, and private maritime organizations).

Coast guards segment is accounted for the 9.61% market share and grow at a 5.90% CAGR during the forecast period.

Anti-Submarine Warfare Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Middle East & Africa and Latin America.

Asia Pacific

North America Anti-Submarine Warfare (ASW) Market Size, 2025 USD Billion

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market is estimated to be the fastest growing with a CAGR of 8.15%. This is driven by unprecedented submarine proliferation and strategic naval competition in the Asia Pacific, establishing existential imperatives for advanced ASW capability incompatible with stationary defense postures or incremental modernization approaches. Quantifiable submarine expansion underpins the strategic drivers underlying ASW acceleration in the region.

China Anti-Submarine Warfare Market

The China market in 2025 was valued at USD 1.87 billion, representing the growth at a CAGR of 7.47% during the forecast period.

India Anti-Submarine Warfare Market

The India’s market in 2025 was valued at around USD 0.89 billion, representing the growth at a CAGR of 10.19% during the forecast period.

Japan Anti-Submarine Warfare Market

The Japan’s market in 2025 was valued at USD 0.82 billion, representing the growth at a CAGR of 6.88% during the forecast period.

North America

North America held the largest market share in 2025, valuing at USD 6.53 billion, and also will maintain the leading share in 2026, with USD 7.04 billion. North America maintains its leadership position due to the United States' unmatched naval procurement scale, advanced technology investments, and long-term submarine modernization strategies.

U.S. Anti-Submarine Warfare Market

Based on North America’s strong contribution the U.S. market was valued at around USD 6.05 billion in 2025, and estimated to be the grow at a CAGR of 6.44% during the forecast period.

Europe

Europe is projected to record a growth rate of 7.34% in the coming years, which is the second highest among all regions, and reached a valuation of USD 4.05 billion in 2025. NATO commitment to an unprecedented escalation in defense spending establishing the framework for sustained naval modernization incompatible with the previous post-Cold War budget constraints.

U.K. Anti-Submarine Warfare Market

The U.K. market in 2025 was at around USD 0.74 billion, representing the growth at a CAGR of 7.22% during the forecast period.

Germany Anti-Submarine Warfare Market

The Germany market in 2025 was valued at around USD 0.56 billion, representing the growth at a CAGR of 8.16% during the forecast period.

Nordic Countries Anti-Submarine Warfare Market

The Nordic Countries market in 2025 was at around USD 0.50 billion, representing the growth at a CAGR of 9.32% during the forecast period.

Middle East & Africa & Latin America

The Middle East& Africa region demonstrates significant growth through record defense spending allocation specifically emphasizing the modernization of naval capability and maritime domain awareness. The Latin American region demonstrates moderate growth through concentrated naval modernization emphasis in Brazil, establishing regional maritime power aspirations and domestic defense industrial capability developments.

Saudi Arabia Anti-Submarine Warfare Market

The Saudi Arabia market in 2025 was at USD 0.34 billion, representing the growth at a CAGR of 6.17% during the forecast period.

Brazil Anti-Submarine Warfare Market

The Brazil market in 2025 was valued at USD 0.37 billion, representing the growth at a CAGR of 3.99% during the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry Consolidation Status and Competitive Concentration Propel Market Competition

The global key players operating in the ASW market demonstrates moderate consolidation characterized by dominant incumbent players with the largest market share through extensive vertical integration, established government relationships, and comprehensive technology portfolios incompatible with fragmented competitive structures where major players maintain equivalent market positions.

In the consolidated market structure, it identifies global Tier 1 incumbent players such as Thales Group, Raytheon Technologies, L3Harris Technologies, Lockheed Martin, General Dynamics, Northrop Grumman Corporation, which control the majority of the market value through platform-integrated sonar systems, combat management architecture and tactical engagement weapons commanding premium pricing across allied navies, focusing on tried reliability above cost-sensitive procurement behavior.

List of Key Anti-Submarine Warfare Companies Profiles

- Lockheed Martin Corporation (U.S.)

- RTX Corporation (U.S.)

- Thales S.A. (France)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- BAE Systems plc (U.K.)

- Naval Group (France)

- Fincantieri S.p.A. (Italy)

- Navantia S.A. (Spain)

- Bharat Electronics Limited (India)

- TKMS Hagenuk Marinekommunikation GmbH (Germany)

- Exail SAS (France)

- L3Harris Technologies, Inc. (U.S.)

- The Boeing Company (U.S.)

- ATLAS ELEKTRONIK GmbH (Germany)

KEY INDUSTRY DEVELOPMENT

- November 2025: - The Hunter class frigates of the Royal Australian Navy will feature cutting-edge defence systems due to BAE Systems Maritime Australia granting Ultra Maritime a contract for its Surface Ship Torpedo Defence (SSTD) system. Each frigate in the Hunter class will have sophisticated acoustic detection and tracking capabilities and integrated countermeasures, boosting the fleet's anti-submarine warfare potential and protecting Australia's maritime interests.

- October 2025:- Thales marks the delivery of its 100th CAPTAS variable immersion towed sonar system, reaching an important milestone in naval defense. Thales reinforces its position as a global leader in ASW technologies.

- September 2025:- The Royal Australian Navy (RAN) has engaged Swedish defense firm Saab to provide an extra AUV62-AT, an autonomous training target designed for ASW.

- June 2025:- The U.S. Department of Defense has granted a contract worth USD 12.88 million to the American firm RTX BBN Technologies Inc. for the design, development, integration, and testing of a novel engineering tool called the Ground Replay System (GRS), which is intended to improve the U.S. Navy's anti-submarine warfare (ASW) abilities.

- April 2025: - The Defence Equipment & Support (DE&S) in the U.K. has secured a contract extension valued at USD 213.08 million for the Integrated Merlin Operational Support (IMOS) to sustain the Royal Navy's Merlin helicopters designed for submarine hunting. The Merlin Mk2 helicopters, which are armed with Sting-Ray torpedoes and M3M .50 caliber machine guns, play a crucial role in the Royal Navy's operations for anti-submarine and anti-surface warfare.

REPORT COVERAGE

The global ASW market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and global ASW market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating major players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.82% 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Offering · Hardware · Software · Services By Component · Sonar Systems · Underwater Sensors · Torpedoes · Depth Charges & ASW Rockets · Decoys and Countermeasure Systems · Underwater Communication Systems · Others By Deployment Mode · Shipborne Systems · Airborne Systems · Submarine-Launched Systems · Unmanned/Autonomous Systems · Fixed Coastal/Seabed Installations By Range · Short-Range ASW Systems · Medium-Range ASW Systems · Long-Range ASW Systems By Installation Type · Line Fit & OEMs · Upgrades & Retrofitting By Technology · Active Sonar Technology · Passive Sonar Technology · Acoustic Signal Processing · Electronic Warfare for ASW · AI & ML Analytics · Data Fusion and Sensor Integration · Others By End User · Naval Forces (Navies) · Coast Guards · Defense Contractors · Allied Military Forces By Region North America (By Offering, By Component, By Deployment Mode, By Range, By Installation Type, By Technology, By End User, by Country) · U.S. (By Deployment Mode) · Canada (By Deployment Mode) Europe (By Offering, By Component, By Deployment Mode, By Range, By Installation Type, By Technology, By End User, by Country) · U.K. (By Deployment Mode) · Germany (By Deployment Mode) · France (By Deployment Mode) · Nordic Countries (By Deployment Mode) · Eastern Europe (By Deployment Mode) · Rest of Europe (By Deployment Mode) Asia Pacific (By Offering, By Component, By Deployment Mode, By Range, By Installation Type, By Technology, By End User, by Country) · China (By Deployment Mode) · India (By Deployment Mode) · Japan (By Deployment Mode) · South Korea (By Deployment Mode) · Australia (By Deployment Mode) · Rest of Asia Pacific (By Deployment Mode) Middle East & Africa (By Offering, By Component, By Deployment Mode, By Range, By Installation Type, By Technology, By End User, by Country) · Israel (By Deployment Mode) · Turkey (By Deployment Mode) · Saudi Arabia (By Deployment Mode) · Iran (By Deployment Mode) · South Africa (By Deployment Mode) · Rest of Middle East & Africa (By Deployment Mode) Latin America (By Offering, By Component, By Deployment Mode, By Range, By Installation Type, By Technology, By End User, by Country) · Brazil (By Deployment Mode) · Argentina (By Deployment Mode) Rest of Latin America (By Deployment Mode) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 18.25 billion in 2025 and is projected to reach USD 33.52 billion by in 2034.

In 2025, the market value stood at USD 4.05 billion.

The market is expected to exhibit a CAGR of 6.82% during the forecast period of 2026-2034.

Naval Forces (Navies) sub-segment in end user segment is expected to lead the market

Critical maritime infrastructure protection and strategic chokepoint vulnerability drives the market growth.

Raytheon Technologies, Lockheed Martin, BAE Systems, Thales Group, General Dynamics and so on.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us