Anti-Tank Guided Missiles (ATGM) Market Size, Share, Industry Analysis & Russia-Ukraine War Impact Analysis, By Platform (Man-Portable, Vehicle-Mounted, and Airborne Platforms), By Warhead Mode (Single Mode and Multi-Purpose Switchable), By Range (Short Range (Below 2 km), Medium Range (2 - 4 km), Long Range (4 - 8 km), and Extended Range (Above 8 km)), By Propulsion Type (Solid Rocket Motors, Ducted Rockets, and Hybrid (Rocket-Ramjet)), By Missile Guidance System (Wire-Guided, Laser-Guided, Infrared-Guided, Millimeter Wave Radar-Guided, and GPS/INS-Guided), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

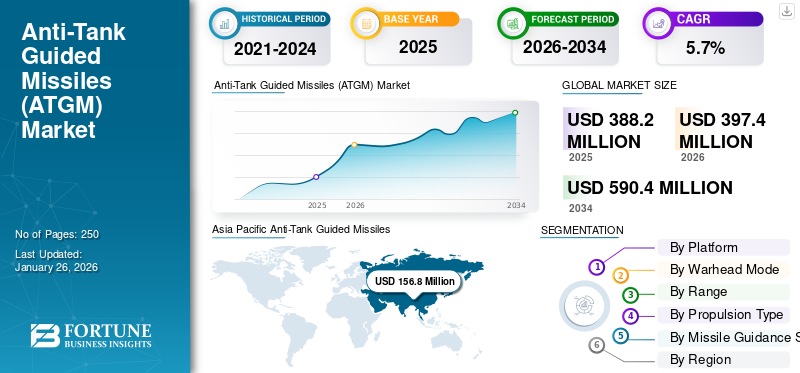

The global anti-tank guided missiles (ATGM) market size was valued at USD 388.20 million in 2025 and is projected to grow from USD 397.40 million in 2026 to USD 590.40 million by 2034, exhibiting a CAGR of 5.7% during the forecast period. Asia Pacific dominated the anti-tank guided missiles (ATGM) market with a market share of 40.39% in 2025.

The Anti-Tank Guided Missiles (ATGM) market encompasses the global industry involved in developing, producing, and deploying missile systems designed to target and destroy armored vehicles, such as tanks and other fortified anti-tank guided missiles. These guided missile systems utilize advanced targeting technologies, including laser guidance, infrared homing, and wire-guidance, to provide precise, long-range firepower in modern warfare. The market serves military and defense agencies worldwide, supporting efforts to enhance battlefield effectiveness and counter armored threats. Ongoing military modernization, regional security concerns, and technological advancements are driving growth in the market. These factors reflect the critical role of ATGMs in contemporary defense strategies.

The COVID-19 pandemic initially disrupted supply chains, delayed military procurement processes, and prompted budget reallocations as governments prioritized healthcare and economic recovery. However, the impact was relatively short-lived, and the market demonstrated resilience due to the strategic importance of ATGMs in modern warfare. In the post-pandemic period, defense agencies accelerated their modernization programs, driving demand for lightweight, highly accurate missile systems surged, fueling market growth.

Key players such as MBDA, Rafael Advanced Defense Systems, Lockheed Martin, Kongsberg Defense & Aerospace, and Northrop Grumman dominate the industry. These companies focus on developing innovative, multi-platform compatible missile systems with enhanced range, accuracy, and countermeasure resistance. The competitive landscape emphasizes technological innovation, integration with existing military platforms, and cost-effective solutions to meet diverse regional security needs.

Download Free sample to learn more about this report.

Anti-Tank Guided Missiles (ATGM) Market

- 2025 Market Size: USD 388.20 million

- 2026 Market Size: USD 397.40 million

- 2034 Forecast Market Size: USD 590.40 million

- CAGR: 5.7% from 2026–2034

- Asia Pacific dominated the anti-tank guided missiles (ATGM) market with a 40.39% share in 2025.

- The man-portable segment is projected to lead the market with a 46.86% share in 2026.

- The single mode segment is projected to account for a 62.26% share in 2026.

Asia Pacific

Asia Pacific generated USD 156.8 million in 2025 and is projected to reach USD 161.9 million in 2026.

Europe

Europe accounted for USD 103.1 million in 2025 and is expected to reach USD 105.7 million in 2026.

North America

North America held USD 93.6 million in 2025 and is projected to grow to USD 94.9 million in 2026.

U.S

The U.S. anti-tank guided missiles market is projected to reach USD 87.3 billion by 2026.

Japan

The Japan anti-tank guided missiles market is projected to reach USD 22.3 billion by 2026.

Read More

RUSSIA-UKRAINE WAR IMPACT

Rising Investments in Developing Next-generation ATGMs in Russia-Ukraine War

The Russia-Ukraine conflict has significantly reshaped the ATGM market, highlighting their critical role in modern warfare. The war has underscored the strategic importance of advanced anti-armor weaponry, prompting countries to accelerate the procurement and development of more sophisticated ATGMs. Ukraine’s effective use of Western-supplied systems, such as Javelin and NLAW missiles, has demonstrated the strategic value of portable, high-precision missile systems in countering heavily armored Russian tanks. This has increased global demand for similar systems, prompting defense agencies worldwide to prioritize ATGM acquisitions and upgrades.

Furthermore, the conflict has exposed vulnerabilities in traditional armored platforms, highlighting the need for versatile, multi-platform missile systems that engage targets in complex battlefield environments. As a result, manufacturers are investing heavily in developing next-generation ATGMs with improved range, accuracy, and countermeasure resistance. The war has also accelerated international collaboration, with Western nations providing military aid and ATGMs to Ukraine, boosting the global market.

The conflict has emphasized the importance of portable, easy-to-use missile systems for infantry units, leading to increased focus on lightweight, man-portable ATGMs. Additionally, the war has demonstrated the necessity for ATGMs to be integrated with modern battlefield management systems, fostering innovation in missile guidance and targeting technologies.

However, the war has also prompted countries to re-evaluate their defense strategies, leading to increased budgets and a focus on asymmetric warfare capabilities. This shift is expected to sustain demand for ATGMs in the coming years. Conversely, geopolitical tensions and arms export restrictions may pose risks to the global supply chain, hindering market growth.

ANTI-TANK GUIDED MISSILES (ATGM) MARKET TRENDS

Rising Investment in Indigenous ATGM Programs to Boost Market Growth

The ATGM market is experiencing dynamic growth driven by rapid technological advancements, evolving warfare tactics, and increasing global defense budgets. One prominent trend is the shift toward lightweight, portable systems that enable infantry units to effectively engage armored threats from a distance, enhancing battlefield flexibility. These man-portable systems, such as Javelin and NLAW, are increasingly favored for their ease of use and high precision, reflecting a move toward more decentralized and mobile combat strategies.

Another key trend is the integration of advanced guidance and targeting technologies. Modern ATGMs now incorporate infrared homing, laser guidance, and multi-target engagement capabilities, improving their accuracy and effectiveness against modern, heavily armored vehicles. Incorporating artificial intelligence and sensor fusion is expected to enhance missile targeting further, enabling faster and more reliable target acquisition.

Additionally, there is growing interest in multi-purpose missile systems that engage various targets beyond tanks, such as fortified positions and low-flying aircraft. This diversification aims to maximize the utility of ATGMs on the battlefield, making them more versatile and cost-effective.

- North America witnessed anti-tank guided missiles (ATGM) market growth from USD 145 Million in 2023 to USD 151.5 Million in 2024.

Geopolitical tensions and regional conflicts also prompt countries to modernize their armored warfare capabilities, fueling demand for advanced ATGMs. Countries increasingly invest in indigenous missile programs to reduce reliance on foreign suppliers and enhance national defense autonomy.

Download Free sample to learn more about this report.

MARKET OPPORTUNITIES

Rising Defense Budgets to Present Opportunities for Market Players

The anti-tank guided missiles (ATGM) market presents significant growth opportunities, driven by increasing global defense spending, technological innovation, and evolving warfare strategies. As nations prioritize the modernization of their armed forces, there is a rising demand for lightweight, portable, and highly accurate missile systems that can effectively counter advanced armored threats. Developing multi-purpose ATGMs, designed to engage various targets, including tanks, fortified positions, and low-flying aircraft, further broadens the market potential.

Additionally, geopolitical tensions and regional conflicts are compelling countries to invest in indigenous missile programs to reduce reliance on foreign suppliers. This shift is fostering local innovation and expanding opportunities for domestic production. The integration of advanced guidance systems, artificial intelligence, and sensor fusion enhances the effectiveness of ATGMs, making them more attractive to military buyers seeking cutting-edge solutions.

Moreover, the trend toward network-centric warfare, where ATGMs are integrated with battlefield management systems and drones, offers avenues for collaborative and multi-layered defense strategies. As defense budgets grow and technological capabilities advance, the ATGM market is poised for sustained expansion, presenting lucrative opportunities for defense contractors, technology developers, and regional manufacturers aiming to strengthen their military arsenals.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Defense Spending and Military Modernization to Boost Market Growth

Countries globally increasingly prioritize enhancing their armored and ground forces to counter evolving threats, especially in regions marked by geopolitical tensions and conflicts. The need for advanced, lightweight, and highly accurate missile systems has led militaries to invest heavily in ATGMs capable of effectively neutralizing modern armored vehicles and fortified positions.

Modernization programs often include the integration of ATGMs with existing battlefield management systems and drones, enabling more comprehensive and responsive defense networks. As nations allocate more funds toward defense, procuring cutting-edge missile systems becomes a strategic priority, fueling market growth. This trend is expected to continue as countries recognize the importance of maintaining technological superiority and battlefield readiness. As a result, rising defense spending will remain a key driver of expansion in the ATGM market.

Technological Advancements and Integration of AI to Drive Market Growth

Technological innovation is crucial to propelling the anti-tank guided missiles (ATGM) market growth. Integrating advanced guidance systems, such as fire-and-forget, lock-on before launch, and sensor fusion, has significantly improved missile accuracy and operational effectiveness. Adopting artificial intelligence (AI) and machine learning algorithms further enhances target recognition, tracking, and engagement capabilities, making ATGMs more reliable and versatile.

These advancements have enabled the development of multi-purpose missiles capable of engaging various targets, including tanks, aircraft, and fortified structures, broadening their application scope. Additionally, incorporating network-centric warfare capabilities allows ATGMs to work seamlessly with other battlefield assets such as drones and command systems, creating a more interconnected and responsive defense environment. Continuous innovation in guidance, propulsion, and warhead technology ensures that ATGMs remain effective against evolving armored threats. This continuous advancement drives product demand and fosters new growth opportunities for defense manufacturers and technology developers.

MARKET RESTRAINTS

Rapid Evolution of Countermeasure Technologies to Hamper Market Growth

The key restraint is the rapid evolution of countermeasure technologies, such as active protection systems (APS) installed on modern tanks. These systems can detect and neutralize incoming missiles, reducing the effectiveness of existing ATGMs. This necessitates continuous innovation and increased R&D expenditure by manufacturers, which can be a significant financial strain and slow down the pace of new system deployment. Developing new missile technologies that can overcome these defenses requires substantial investment in research, testing, and validation, further escalating costs.

Additionally, the technological arms race between missile developers and tank manufacturers fosters a cycle of constant upgrades, making it challenging for ATGM producers to maintain a competitive edge. This ongoing technological arms race can delay the deployment of new systems and limit the market's overall growth, as military organizations may hesitate to invest heavily in systems that could quickly become obsolete.

MARKET CHALLENGES

Geopolitical Tensions and Regional Conflicts to Challenge Market Growth

One of the significant challenges facing the ATGM market is the high cost associated with developing, procuring, and maintaining advanced missile systems. Cutting-edge ATGMs equipped with sophisticated guidance systems, sensors, and AI integration tend to be expensive, limiting accessibility for countries with constrained defense budgets. This financial barrier can hinder widespread adoption and slow market growth, particularly in emerging economies.

Another major challenge is the rapid pace of technological advancements in armored vehicle design and countermeasure systems. Modern tanks and armored vehicles are increasingly equipped with active protection systems (APS) that can detect and neutralize incoming missiles, making ATGM developers need to continuously innovate. This arms race between missile technology and countermeasures increases R&D costs and complicates the development process.

Furthermore, geopolitical tensions and regional conflicts pose risks to the stability of the supply chain disruptions, and political restrictions on missile exports. Countries may face challenges in acquiring or maintaining reliable supply chains for critical components, which can delay production and deployment. Additionally, international arms control regulations and export restrictions may limit the proliferation of certain missile technologies, posing legal and diplomatic hurdles for manufacturers and buyers alike.

SEGMENTATION ANALYSIS

By Platform

Man-Portable Segment Led Due to Its Cost-Effectiveness and Ease of Use

By platform, the market is classified into man-portable, vehicle-mounted, and airborne platforms.

In 2026, the man-portable segment is projected to lead the market with a 46.86% share. These systems are cost-effective, easy to operate, and highly mobile, allowing infantry units to engage armored targets effectively in various terrains without the need for heavy equipment. Their simplicity and affordability make them accessible to many armed forces globally.

The airborne platforms segment is expected to experience the highest compound annual growth rate (CAGR) of 5.2% during the forecast period due to their strategic advantages, including rapid deployment, flexibility, and the ability to engage targets from a safe distance. As modern warfare emphasizes mobility and precision, the demand for airborne ATGMs is increasing, driving significant growth in this segment to meet evolving battlefield requirements.

By Warhead Mode

Single-Mode Segment Dominated Due to Its Reliability and Cost-Effectiveness

By warhead mode, the market is classified into single mode, and multi-purpose switchable.

In 2026, the single mode segment is projected to lead the market with a 62.26% share. The single-mode warhead segment offers specialized, optimized performance for specific target types, making it reliable and cost-effective for most military applications. These warheads are simpler to design and produce, ensuring widespread adoption.

The multi-purpose switchable segment is expected to experience the highest compound annual growth rate (CAGR) of 5.0% during the forecast period due to its versatility, allowing operators to switch between different modes (such as anti-armor and anti-structure) based on mission requirements. This adaptability reduces the need for multiple missile types, enhancing operational flexibility and cost-efficiency. As modern combat scenarios demand versatile weapon systems, the demand for switchable warheads is expected to grow rapidly.

By Range

Long-Range (4-8 km) Segment Led Market Due to Optimal Engagement Distance and Compatibility

By range, the market is classified into short range (below 2 km), medium range (2 - 4 km), long range (4 - 8 km), and extended range (above 8 km).

In 2026, the long range (4 - 8 km) segment is projected to lead the market with a 37.41% share. It balances effective engagement distances with manageable missile size and launch platform compatibility, making it suitable for various military operations. It provides sufficient stand-off distance to minimize risk to operators while maintaining high accuracy.

The extended range (above 8 km) segment is projected to experience the highest compound annual growth rate (CAGR) of 5.1% throughout the forecast period due to advancements in missile technology, increased emphasis on standoff capabilities, and the need for forces to engage targets from safer distances. The growing demand for strategic, long-distance precision strikes in modern warfare is driving rapid growth in the segment.

By Propulsion Type

Solid Rocket Motors Segment Dominated Market Due to Its Simplicity, Reliability, and Cost-Effectiveness

Based on propulsion type, the market is classified into solid rocket motors, ducted rockets, and hybrid (Rocket-Ramjet).

In terms of revenue, the solid rocket motors segment is projected to lead the market with a 68.81% in 2026 share. Solid rocket motors are gaining traction due to their simplicity, reliability, quick response, and cost-effectiveness, making them the preferred choice for most ATGMs. They require less maintenance and have a proven track record, ensuring widespread adoption.

The hybrid (Rocket-Ramjet) segment is projected to experience the highest compound annual growth rate (CAGR) of 7.9% from 2025 to 2032. It combines the advantages of solid and liquid propulsion, enabling higher speeds, longer ranges, and better efficiency. As militaries seek advanced, high-performance missiles for extended reach and improved maneuverability, hybrid propulsion systems are increasingly favored, driving rapid growth in this segment. This innovation enhances missile capabilities to meet modern combat demands.

By Missile Guidance System

To know how our report can help streamline your business, Speak to Analyst

Wire-Guided Segment Led Market Share Due to Its Accuracy and Reliability

Based on missile guidance system, the market is divided into wire-guided, laser-guided, infrared-guided, millimeter wave radar-guided, and GPS/INS-guided.

In 2024, the wire-guided segment is projected to lead the market with a 22.61% share, as it offers high accuracy, reliability, and resistance to jamming, making it ideal for close-to-mid-range engagements. Its proven technology and cost-effectiveness have led to widespread adoption by armed forces.

The millimeter wave radar-guided segment is projected to experience a compound annual growth rate (CAGR) of 5.8% during the forecast period due to its advanced targeting capabilities, all-weather functionality, and resistance to countermeasures. Millimeter-wave radar-guided ATGMs are gaining popularity as militaries seek more sophisticated, long-range, and autonomous guidance systems. Their ability to operate effectively in complex environments and provide precise targeting drives rapid growth, making this guidance system a key focus for future missile development.

ANTI-TANK GUIDED MISSILES (ATGM) MARKET REGIONAL OUTLOOK

This market is segmented into North America, Europe, Asia Pacific, and the Rest of the World.

North America

Asia Pacific Anti-Tank Guided Missiles (ATGM) Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 24.12% to the global market in 2025, with a valuation of USD 93.6 million, and is projected to reach USD 94.9 million in 2026. North America, particularly the U.S., is expected to grow at significant growth rate in the global ATGM market due to its substantial defense budget, technological innovation, and extensive military operations. The U.S. government continuously invests in developing next-generation missile systems to maintain technological superiority. U.S. defense contractors such as Lockheed Martin and Raytheon are at the forefront, delivering advanced ATGM platforms such as the Javelin missile, which has seen widespread adoption across allied forces. The U.S. market is projected to reach USD 87.3 billion by 2026.

Europe

The anti-tank guided missiles (ATGM) market in Europe holds a significant share, driven by the region’s ongoing modernization of defense systems and increased military expenditure. European countries such as France, Germany, and the U.K. are investing heavily in advanced missile systems to enhance their armored and infantry capabilities. The presence of prominent defense manufacturers such as MBDA and Rheinmetall further propels the market, with a focus on integrating cutting-edge technologies such as fire-and-forget and top-attack systems. Additionally, regional security concerns and NATO’s strategic initiatives bolster the demand for sophisticated ATGM systems. The UK market is projected to reach USD 22.9 billion by 2026, and the Germany market is projected to reach USD 16.6 billion by 2026. Europe accounted for USD 103.1 million in 2025, representing 26.57% of the global market share, and is projected to reach USD 105.7 million in 2026.

Asia Pacific

The Asia Pacific region is largest and fastest growing region owing to rapid growth due to increasing defense budgets, regional conflicts, and modernization efforts by countries such as India, China, and South Korea. These nations are investing heavily in advanced ATGMs to bolster their military capabilities and address security challenges. The Japan market is projected to reach USD 22.3 billion by 2026, the China market is projected to reach USD 55.4 billion by 2026, and the India market is projected to reach USD 34 billion by 2026. The Asia Pacific market was valued at USD 156.8 million in 2025, capturing 40.39% of global revenue, and is estimated to reach USD 161.9 million in 2026.

Rest of the World

Emerging markets across the Middle East, Africa, and Latin America are increasingly expanding their ATGM procurement to enhance battlefield effectiveness amid ongoing conflicts and internal security threats. These regions are increasingly adopting cost-effective, reliable missile systems to modernize their armed forces. The Rest of the World region captured 8.92% of the global market in 2025, generating USD 34.6 million in revenue, and is projected to reach USD 35 million in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Technological Advancements to Propel Market Growth

The anti-tank guided missiles (ATGM) market share is dominated by key players such as MBDA, Rafael Advanced Defense Systems, and Lockheed Martin, who lead in innovation and technological advancements. Other significant companies include Kongsberg Defense & Aerospace, Northrop Grumman, and Denel Dynamics, each offering advanced missile systems to meet evolving defense needs. These industry leaders focus on developing lightweight, highly accurate, and versatile ATGMs capable of defeating modern armored threats. The competitive landscape is shaped by several factors, including increasing defense budgets, technological innovation, and the demand for enhanced battlefield survivability, positioning these key players at the forefront of the global ATGM market.

LIST OF KEY ANTI-TANK GUIDED MISSILE COMPANIES PROFILED

- Raytheon Technologies Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- MBDA (France)

- Rafael Advanced Defense Systems Ltd. (Israel)

- KBP Instrument Design Bureau (Russia)

- Norinco (China)

- Roketsan (Turkey)

- Saab AB (Sweden)

- LIG Nex 1 (South Korea)

- Bharat Dynamics Ltd. (India)

- NPO Mashinostroyeniya (Russia)

- Denel Dynamics (South Africa)

- Mesko (Poland)

- Aselsan (Turkey)

- BAE Systems plc (U.K.)

KEY INDUSTRY DEVELOPMENTS

- March 2025 - The Ministry of Defence (MoD) India entered into a contract with Armoured Vehicles Nigam Limited (AVNL) for the procurement of the tracked version of the Nag Missile System (NAMIS), a key anti-tank weapon platform. Additionally, the MoD entered into contracts with Force Motors Ltd and Mahindra & Mahindra Ltd for the supply of approximately 5,000 Light Vehicles intended for armed forces use.

- February 2025 - Brazilian missile expert SIATT – Engenharia, Indústria e Comércio received a contract from the Brazilian Army to commence serial production of the MAX 1.2 AC medium-range man-portable anti-tank guided missile (ATGM) system.

- November 2024 - Elbit Systems announced a follow-on contract of around USD 127 million with General Dynamics Ordnance and Tactical Systems (GD-OTS) for supplying Iron Fist Active Protection Systems (APS) for the Bradley M2A4E1 Infantry Fighting Vehicles (IFVs). This contract is set to be executed over a duration of 34 months.

- September 2023 - India’s Ministry of Defence (MoD) signed a contract worth USD 34.7 million with Kalyani Rafael Advanced Systems Pvt Ltd (KRAS) for the procurement of Spike anti-tank guided missiles (ATGMs) intended for the Indian Armed Forces.

- March 2021 - The German defense giant, Rheinmetall, secured a multi-million Euro contract to supply the MELLS anti-tank guided missile (ATGM) systems to the German Army. The Bundeswehr of Germany ordered the MELLS anti-tank guided missile system through EuroSpike GmbH, a collaborative venture involving Rheinmetall, Diehl Defence, and Israel's Rafael Advanced Defense Systems.

REPORT COVERAGE

This anti-tank guided missiles (ATGM) research report offers a comprehensive market analysis, identifying key players, product categories, and primary applications. It also details market trends and significant industry developments. Moreover, the report highlights various factors that have fueled the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.7% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Platform

|

|

By Warhead Mode

|

|

|

By Range

|

|

|

By Propulsion Type

|

|

|

By Missile Guidance System

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 397.40 million in 2026 and is estimated to reach USD 590.40 million by 2034.

The market will grow steadily at a CAGR of 5.7% during the projection period.

By platform, the man-portable segment led the market.

Raytheon Technologies Corporation (U.S.), Lockheed Martin Corporation (U.S.), MBDA (France), Rafael Advanced Defense Systems Ltd. (Israel), KBP Instrument Design Bureau (Russia), and Norinco (China) are some of the leading OEMs in the market.

Asia Pacific dominated the anti-tank guided missiles (ATGM) market with a market share of 40.39% in 2025.

By warhead mode, the multi-purpose switchable segment is expected to rise at the highest CAGR during the forecast period.

Next-Gen Guidance: AI, Dual & Multi-Mode Seekers and Portable & Modular Designs of ATGM are latest trends.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us