Active Protection System Market Size, Share & Industry Analysis, By Platform (L&-based, Airborne, & Marine), By L&-based (Main Battle Tank (MBT), Light Protected Vehicles (LPV), Amphibious Armored Vehicles (AAV), Mine-Resistant Ambush-Protected (MRAP), Infantry Fighting Vehicles (IFV), Armored Personnel Carriers (APC)), By Airborne (Fighter Aircraft, Helicopters, Special Mission Aircraft, & Others), By Marine (Submarine, Frigates, Destroyers, Aircraft Carriers), By Kill System Type, and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

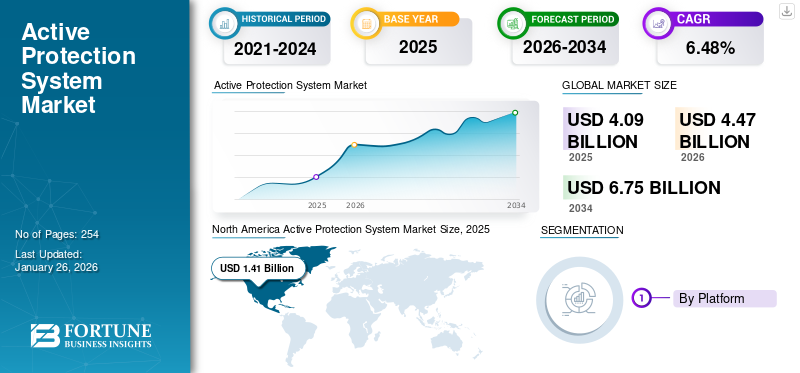

The global active protection system market size was valued at USD 4.09 billion in 2025. The market is projected to grow from USD 4.47 billion in 2026 to USD 6.75 billion by 2034, exhibiting a CAGR of 6.48% during the forecast period. North America dominated the active protection system market with a market share of 34.44% in 2025.

According to the Congressional Research Service (CRS) Report, Department of Defense (DOD) Directed Energy Weapons (DEW), directed energy weapons can destroy a vast array of electronic systems, which may include both commercial and military systems. They can disable, incapacitate, or destroy any electronic system that falls under their electromagnetic cone. This factor is expected to drive market growth owing to the demand for weapon systems based on high-energy lasers and high particle beams on naval, airborne, and land platforms. All these aspects are driving the demand for Active Protection Systems (APS).

The global COVID-19 pandemic was unprecedented and staggering, with active protection systems experiencing higher-than-anticipated demand across all regions compared to pre-pandemic levels. Based on our analysis, the global market share exhibited a growth of 5.38% in 2024 as compared to 2023.

Download Free sample to learn more about this report.

Active Protection System MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 4.09 billion

- 2026 Market Size: USD 4.47 billion

- 2034 Forecast Market Size: USD 6.75 billion

- CAGR: 6.48% from 2026–2034

- North America dominated the active protection system market with a 34.44% share in 2025.

- The land-based segment accounted for 57.43% of the market share in 2026.

- The Main Battle Tank (MBT) segment held an 18.22% market share in 2026.

North American

North America reached USD 1.54 billion in 2026, driven by rising investments in next-generation platform protection systems.

Europe

Europe is projected to reach USD 1.16 billion in 2026, supported by increased defense modernization and military procurement programs.

Asia Pacific

Asia Pacific is projected to reach USD 0.85 billion in 2026, driven by growing investments in advanced land, naval, and airborne defense platforms.

U.S.

The market is projected to reach USD 1.30 billion in 2026, supported by continued deployment of advanced active protection systems.

Japan

The market is projected to reach USD 0.09 billion in 2026, driven by increasing investments in defense modernization.

Read More

IMPACT OF COVID-19

Rising Global Conflicts Owing to Interrupted Peace Negotiations and Deployment Reduction of Forces Boosted Market During the Pandemic

New security alliances by countries were formed during the pandemic. For instance, Australia, the U.K., and the U.S. announced a new tri-lateral security partnership, AUKUS, for the Indo-Pacific region. They will work together to produce hypersonic missiles. To consider another example, France reorganized its strategic involvement in the Sahel in Africa and focused on the Takuba counter-terrorism mission.

The pandemic interrupted peace negotiations and reduced the footprint of international forces. However, the market for APS was not much affected since countries did not decrease their defense spending. Further, with the second and third waves of the pandemic and continued regional disturbances, most nations resorted to modernization programs for their militaries. In the defense industry, a significant impact was felt from the inability to procure critical components due to the disrupted supply chains.

IMPACT OF RUSSIA-UKRAINE WAR

Operational Implications and Losses Incurred to Surge Demand for Deployment of APS on Future Military Platforms

The Russia-Ukraine war has renewed the debate regarding the deployment of APSs by armed forces on their military platforms for armored vehicles. The war initiated a domino effect in the increase in defense spending worldwide, especially in the European continent. The conflict has severely impacted military budgets and also changed the procurement priorities of the European Armed Forces.

In the war, Ukrainian troops challenged the Russian armored vehicles and destroyed several tanks with javelins and Next Generation Light Armored Vehicles (NLAW). Several tanks had old APS and could not counter modern guided missile systems. Due to this, several countries renewed their modernization programs for their infantry fighting vehicles. The lack of DIRCM (Directional Infrared Countermeasures) installation on helicopters served as a lesson for NATO and other European Non-NATO Armed Forces. The development has increased the demand for APS and its subsystems in the NATO region.

For instance, in July 2022, General Dynamics Land Systems was awarded an Indefinite-Delivery, Indefinite-Quantity (IDIQ) contract worth USD 280.1 by the U.S. Army. The move was intended to provide Trophy Modular Ready Kits as a self-protection system for the U.S. Army M1A2 SEPv2 & SEPv3 Abram main battle tanks.

ACTIVE PROTECTION SYSTEM MARKET TRENDS

Growing Adoption of Next-generation Modular Countermeasure Kits and Missile Countermeasure Devices to Bolster Demand

The base modular kits combine sensors and countermeasures in an open, common framework to detect, follow, organize, and defeat emerging and existing threats surge rocket-propelled projectiles and anti-tank guided munitions. North America witnessed active protection system market growth from USD 1.16 Billion in 2023 to USD 1.21 Billion in 2024.

The scalable and open MAPS base kit is prepared to succeed with existing combat vehicles and sustain the capabilities of next-generation armored vehicle protection systems. The open-architecture controller features open standard interfaces and readily incorporates sensors and countermeasures that are compliant with the integrated MAPS architecture framework. It provides fast and secure processing power to drive multiple applications and future vehicle protection system capabilities. Further, Modular Active Protection Systems (MAPS) protect armored vehicles and crews from rockets and missiles, which is a major factor impelling industry growth.

For instance, in February 2024, Hanwha Defense Australia (HDA) granted a contract valued at USD 600 million to Israeli military tech firm Elbit Systems to provide defensive and combat capabilities, as well as sensors for the Australian Redback infantry fighting vehicles (IFVs). In December 2023, the Australian Department of Defence (DoD) finalized a USD 2.4 billion agreement with HDA for the delivery of 129 Redback IFVs to the Australian Army as part of the service's Land 400 Phase 3 initiative. HDA collaborated with multiple defense manufacturers, including Elbit Land Systems, to manufacture the Australian Redbacks.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Deployment of Next-generation Countermeasures and Decoys to Drive Market Growth

Armed forces globally are moving toward a modular framework for their next-generation self-protection system requirements. The next-generation modular APS kits will enhance the capability to provide future solutions tailored to address a wide range of platforms and can be easily upgraded. The forces emphasize maximizing vehicle survivability by integrating advanced and next-generation multi-layered protection systems.

Innovations in APS technologies, including enhanced sensor systems, artificial intelligence, and countermeasure capabilities, are improving the effectiveness of these systems. Many countries are modernizing their armed forces by upgrading existing military vehicles with advanced protection systems. This trend is particularly strong in regions such as North America and Europe, where military modernization programs are being prioritized, catalyzing market growth.

With the increased prominence of APSs, market players and military operators are currently focusing on multiple coordinated layers of active and passive sensors and countermeasures. APS has been the most demanded technology for addressing modern situational awareness and survivability challenges. This is in light of threats from projectiles such as Rocket Propelled Grenades (RPGs), loitering munitions, and Anti-tank Guided Missiles (ATGMs).

For instance, in November 2024, BAE Systems received a subsequent contract from the U.S. Army to enhance its Multi-Class Soft Kill System (MCSKS) countermeasures, which aim to safeguard ground combat vehicles from guided missiles and related threats, thereby increasing vehicle survival rates and mission effectiveness. As part of the MCSKS agreement, BAE Systems will continue to develop its laser-based Stormcrow™ and TERRA RAVEN™ countermeasure systems, contributing to the Army’s work on electronic warfare (EW)-based APS. These advanced systems effectively mitigate threats while enabling crews to conserve kinetic countermeasures.

Surging Advancement in Electronic Warfare Countermeasures and Missile-based Hard Kill Systems to Bolster Market Growth

Electronic countermeasures are adopted on account of the escalated demand for threat detection, threat suppression, and threat neutralization on various military platforms such as land-based, airborne, and marine. Therefore, several regulatory bodies and industry players are launching a series of projects that are focused on product development.

For instance, the Precision Electronic Warfare (PREW) project by DARPA emphasizes the development of a low-cost EW countermeasures system with several airborne jamming pods synchronization to replicate AESA, avoiding collateral jamming of non-targeted receivers.

To consider a few other instances:

- In January 2024, The Defence Science and Technology Laboratory (Dstl) was awarded a new contract via the Aurora Engineering Delivery Partnership (EDP) for a project aimed at enhancing the survivability and protection of Land Armoured Vehicles used by the British Army.

- In January 2024, The Defence Science and Technology Laboratory (Dstl) was awarded a new contract via the Aurora Engineering Delivery Partnership (EDP) for a project aimed at enhancing the survivability and protection of Land Armoured Vehicles used by the British Army.

MARKET RESTRAINTS

High Complexity and Overbearing Cost for Implementation and Installation to Hamper Market Growth

In the defense sector, the protection system is significant for protecting from air defense systems, situational radars, and platform detection. The high cost associated with implementing and installing an APS is a prime factor hampering the market growth. This active protection system consists of highly expensive systems owing to complex installation and integration with existing military assets.

A high maintenance cost is required to upgrade the APS to improve the main battle tanks’ defending capacity, light-protected vehicles, and an amphibious armored vehicle. Therefore, the necessity to upgrade APS is expected to hamper the active protection system market growth during the forecast period.

SEGMENTATION ANALYSIS

By Platform

Land-based Systems to Record Surging Demand Due to Burgeoning Product Requirement on Armored Vehicles

By platform, the global market is divided into land-based, airborne, and marine.

The land-based segment is expected to hold a 57.43% share in 2026. The growth is attributed to the high demand for APS on land-based platforms and rising technological advancements in soft-kill systems. A few instances include electronic and laser-based jamming coupled with smoke dispensers.

The marine segment recorded the second-largest share in 2024 and is set to register commendable growth from 2025 to 2032. The growing need for advanced and next-generation countermeasures against infrared detection, laser ranging, visual observation, UAV swarm attacks, and laser weapons is driving this growth.

The airborne segment is estimated to be the fastest-growing segment during the forecast period. The growth can be credited to the high adoption rate of electronic warfare strategies and technologies to electronically jam the enemy situational awareness system and weaponry from detection and attack.

To know how our report can help streamline your business, Speak to Analyst

By Land-based

High Adoption of APS amid Increased Procurement and Modernization of Main Battle Tank (MBT) Bolstered Segment Growth

Based on land-based, the market is segmented into main battle tank (MBT), light protected vehicles (LPV), amphibious armored vehicles (AAV), mine-resistant ambush-protected (MRAP), infantry fighting vehicles (IFV), armored personnel carriers (APC), and others.

The Main Battle Tank (MBT) segment will account for 18.22% market share in 2026. Main Battle Tank (MBT) was the largest segment by market share, owing to the high adoption rate of hard-kill and soft-kill APS amid the rise in the procurement and modernization of main battle tanks. For instance, in July 2022, the U.S. Armed Forces awarded General Dynamics Land Systems an Indefinite Delivery, Indefinite Quantity (IDIQ) contract worth USD 280 million to procure Trophy Active Protection System for its M1A2 SEPv2 and SEPv3 Abrams Tanks.

The Mine-Resistant Ambush-Protected (MRAP) segment is estimated to be the fastest-growing segment during the forecast period. According to SIPRI publications and the DefenseiQ Report, the armed forces globally are heavily investing in the procurement of mine-resistant ambush-protected vehicles and modernizing their existing MRAPs. The increased procurement of MRAPs is driving the installation and procurement of APS on these platforms amid rising IED attacks on armored columns by enemy armed forces, terrorists, or non-state actors.

By Airborne

Heightened Procurement of Soft- and Hard-kill APSs Onboard Fighter Aircraft Globally by Air Forces Propelled Segment Growth

On the basis of airborne, this market is classified into fighter aircraft, helicopters, special mission aircraft, and others.

The fighter aircraft segment is expected to account for 7.47% of the market in 2026. The growth is attributed to the rise in procurement of soft- and hard-kill APSs onboard this airborne platform, which is anticipated to bolster the segmental growth during the projection period. For instance, in April 2022, the Indian Air Force tied up with India’s Defense Research Development Organization to induct CHAFF technology to protect fighter aircraft from enemy radar-guided missiles during war scenarios.

The special mission aircraft segment is estimated to be the fastest-growing during the projection period. The growth is due to the increased hard-kill APS, such as Directed IR Countermeasures (DIRCM) and other hard-kill APSs on these platforms, which are propelling the segmental growth during the forecast period. For instance, in July 2022, Elbit Systems Ltd was awarded a contract worth USD 80 million by an undisclosed Asia Pacific Country to supply airborne EW (Electronic Warfare) systems and direct infrared countermeasures (DIRCM) for airborne platforms such as special mission aircraft.

By Marine

Modernization of Destroyers Amid Rise in Naval Skirmishes and Anti-Piracy Operations to Drive the Adoption of APS in the Market

Based on marine, the market is divided into submarine, frigates, destroyers, aircraft carriers, and others.

The Destroyers segment is anticipated to hold a dominant market share of 7.83% in 2026. The growth is attributed to the growing market penetration of the key global players into the Asia Pacific and North America markets amid the heightened adoption rate of APS by regional naval forces. For instance, in May 2022, Raytheon Missile & Defense, a subsidiary of Raytheon Technologies Corporation, was awarded a contract worth USD 423 million to produce SPY-6 radars for U.S. Navy Vessels such as Destroyers and Aircraft Carriers.

Frigates is anticipated to be the fastest-growing segment during the projection period. Asian Naval Forces such as the Indian Navy, PLA Navy, Malaysia, the Philippines, Japan, and South Korea are heavily investing in the naval shipbuilding of Frigates owing to the operational requirements of their naval forces. This development will drive the segmental growth in the global market.

By Kill System Type

Soft Kill Systems Segment to Record Considerable Growth

Based on the kill system type, the market is classified into soft kill system, hard kill system, and reactive armor.

The soft kill system segment held the largest share in 2024 and is estimated to record commendable growth during the projected period. The growth is attributed to the high demand for soft-kill self-protection systems owing to heightened investment in RDT&E of electronic warfare countermeasures and C-UAS (Counter-Unmanned Aerial System) systems.

The hard kill system segment held the second-largest share in 2024 and is poised to register appreciable expansion during the forecast period. The segmental growth is driven by the high demand and investment increment in developing the next-generation hard kill system. These include Directed Energy Weapons as Counter-Hypersonic Air Defense or Short Range Air Defense (SHORAD).

The reactive armor segment is anticipated to be the fastest-growing segment during the 2026-2034 period. This can be credited to the rising threats from anti-tank guided missiles, Molotov cocktails used in the Russia-Ukraine war, and loitering munitions.

By Solution

High Demand for APS Hardware Boosted Segment Growth

By solution, the global market is classified into hardware and software.

The hardware segment accounted for the largest share in 2024 and will record a substantial surge during the forecast period. The growth is attributed to the high demand for APS hardware and the increment in RDT&E investment in hardware required for APSs. For instance, in July 2020, Leonardo UK announced that it had completed the ICARUS Technology Demonstrator Programme (TDP) contract to field automatic agile APSs on its current and future armored fighting vehicle platform. The development will enhance their survivability from a wide range of incoming threats.

The software segment is estimated to be the fastest-growing during the projected period owing to the high adoption rate of the self-protection system software suite to support its hardware systems. For instance, in May 2022, BAE Systems Australia was awarded an export contract worth USD 50 million to provide software and hardware sub-assemblies for the NATO Evolved Sea Sparrow Missile (ESSM) program.

ACTIVE PROTECTION SYSTEM MARKET REGIONAL OUTLOOK

Based on region, the global market is segmented into North America, Europe, Asia Pacific, the Middle East, and the Rest of the World.

North America

North America Active Protection System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 1.41 billion, contributing 34.44% to global market revenue, and is projected to grow to USD 1.54 billion in 2026. The rising threat of anti-tank guided missiles and loitering munitions has driven the U.S. Armed Forces to develop platform self-protection systems such as MAPS, Quick Kill, Iron Curtain, and Directed Energy Weapons to safeguard its platforms, personnel and heighten its situational awareness from existing and emerging threats. The U.S. market is projected to reach USD 1.3 billion by 2026.

Europe

The Europe market accounted for USD 1.05 billion in 2025, representing 25.78% of the global industry, and is expected to reach USD 1.16 billion in 2026. European Union members have increased their investment in next-generation self-protection systems for their armed forces platforms owing to their traditional procurement programs and the ongoing Russia-Ukraine war. The rest of Europe, especially Eastern European countries, is anticipated to adopt self-protection systems for their armed forces and homeland security forces during the forecast period. This development is expected to positively influence the market growth of the meteorological device market in the region during 2026-2034. The UK market is projected to reach USD 0.38 billion by 2026, while the Germany market is projected to reach USD 0.19 billion by 2026.

Asia Pacific

Asia Pacific recorded a market size of USD 0.79 billion in 2025, capturing 19.22% of the global market share, and is projected to reach USD 0.85 billion in 2026. Several countries in Asia Pacific have increased their investments in armed forces platforms such as airborne, naval, and land. The burgeoning demand for hard kill systems such as directed energy weapons fuels regional growth. The Japan market is projected to reach USD 0.09 billion by 2026, the China market is projected to reach USD 0.24 billion by 2026, and the India market is projected to reach USD 0.19 billion by 2026.

Rest of the World

The Rest of the World market was valued at USD 0.33 billion in 2025, capturing 8.17% of global revenue, and is estimated to reach USD 0.36 billion in 2026.

The Middle East & Africa market generated USD 0.51 billion in 2025, representing 12.39% of the global market landscape, and is expected to reach USD 0.55 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Major Key Players Focus on Development in APS Systems to Propel Market Growth

The active protection system market is highly fragmented among various regional players. The top five players in the market are SAAB AB, Rheinmetall AG, Raytheon Technologies Corporation, Rafael Advanced Defense Systems Ltd., and Hensoldt AG, which comprise 54.2% of the total market. Various key players, such as major players in defense technologies, are making developments. RTX develops advanced APS solutions that integrate sensors, tracking systems, and countermeasures. In addition, the Italian company specializes in aerospace and defense technologies, including APS, which enhance vehicle protection through innovative sensor integration. Furthermore, it is a global defense, security, and aerospace company that offers a range of APS products designed to protect armored vehicles from modern threats.

LIST OF KEY ACTIVE PROTECTION SYSTEM COMPANIES PROFILED

- Artis LLC (U.S.)

- Aselsan A.S. (Turkey)

- Hensoldt AG (Germany)

- JSC Konstruktorskoye Byuro Mashinostroyeniya (Russia)

- Krauss-Maffei Wegmann GmbH & Co. KG (Germany)

- Lockheed Martin Corporation (U.S.)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Raytheon Technologies Corporation (U.S.)

- Rheinmetall AG (Germany)

- SAAB AB (Sweden)

- Israel Military Industries Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS

- December 2024 – EuroTrophy secured a significant contract with KNDS Deutschland to provide 123 Trophy Active Protection Systems for the latest Leopard 2 A8 main battle tank fleet of the German Army.

- November 2024 – Elbit Systems revealed this week that it has received a subsequent contract valued at around USD 127 million to provide Iron Fist APS to General Dynamics Ordnance and Tactical Systems (GD-OTS) for enhancements to the U.S. Army's Bradley M2A4E1 Infantry Fighting Vehicles (IFVs). The execution of the contract will span over 34 months.

- November 2024 - The BAE Systems Multi-Class Soft Kill System (MCSKS) is a countermeasure system designed to protect without relying on kinetic force. This innovative approach will streamline the logistics required for defense. Recently, the U.S. Army awarded BAE Systems a follow-up contract to develop further the MCSKS countermeasures system, which aims to safeguard vehicles against guided missiles and similar threats.

- October 2024 – ELTA North America secured a USD 7.5 million contract from the U.S. Army to assist with the Trophy APS used on M1 Abrams tanks. As part of this agreement, the company will create a more effective testing and repair facility in the U.S. for the Israeli-made tank defense system. This facility will enhance the operational readiness of the Trophy system, minimizing downtime and boosting its availability for deployment.

- September 2024 – A subsidiary of General Dynamics secured a firm-fixed-price contract from the Defense Logistics Agency to supply APS kits for the U.S. Army and federal civilian entities. The Department of Defense announced that General Dynamics Ordnance and Tactical Systems, located in Williston, Vermont, received a one-time purchase contract valued at no less than USD 191.2 million for the acquisition of Iron Fist Active Protection System B-kits.

REPORT COVERAGE

The market research report provides a detailed analysis of various aspects, such as key players, their product offerings, and end-users of active protection systems. Moreover, it offers insights on market trends, competitive landscape, market competition, product pricing, and market status and highlights key industry developments. In addition to the aspects mentioned above, it encompasses several direct and indirect factors that have contributed to the sizing of the global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

6.48% CAGR from 2026 to 2034 |

|

Segmentation |

By Platform

|

|

By Land-based

|

|

|

By Airborne

|

|

|

By Marine

|

|

|

By Kill System Type

|

|

|

By Solution

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 4.47 billion in 2026 and is projected to record a valuation of USD 6.75 billion by 2034.

Registering a CAGR of 6.48%, the market will exhibit steady growth during the forecast period of 2026-2034.

Based on the kill system type, the soft kill system segment led the market in 2026.

Rafael Advanced Defense System Ltd., Raytheon Technologies Corporation, and Aselsan A.S. are the leading players in the global market.

North America dominated the active protection system market with a market share of 34.44% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 254

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us