Apheresis Market Size, Share & Industry Analysis By Product Type (Instruments and Consumables), By Procedure Type (Donor Apheresis and Therapeutic Apheresis), By Technology Platform (Centrifugation, Membrane Filtration, and Others), By Application (Plasmapheresis, Plateletpheresis, Leukapheresis, and Others), By End User (Hospitals, Specialty Clinics, Blood Collection Centers & Blood Banks, and Others), and Regional Forecast, 2026-2034

Apheresis Market Size and Future Outlook

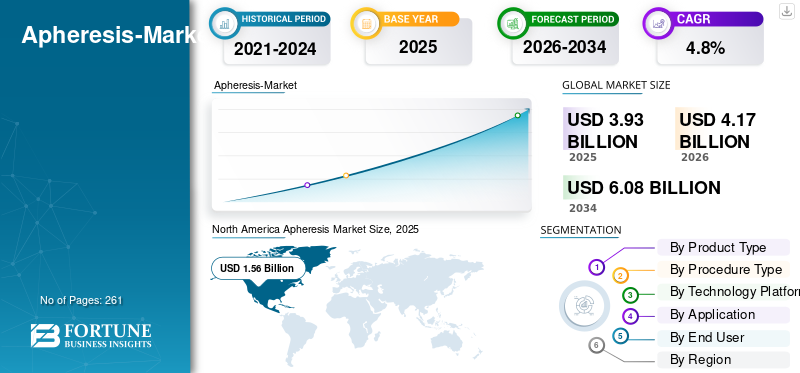

The global apheresis market size was valued at USD 3.93 billion in 2025 and is projected to grow from USD 4.17 billion in 2026 to USD 6.08 billion by 2034, exhibiting a CAGR of 4.8% during the forecast period. North America dominated the apheresis market with a market share of 39.69% in 2025.

Apheresis refers to an extracorporeal medical procedure used for therapeutic and life-saving treatments that uses specialized instruments to separate and remove specific blood components, such as red blood cells and platelets, among others, while returning the remaining components to the donor. The rising prevalence of chronic disorders, growing demand for plasma-derived therapies, and technological advancements in such devices are increasing the adoption rate of these products in the market. The increasing number of blood donation camps is further supporting the demand for these procedures in the market.

- In August 2022, as per the data published by News Medical, thalassemia affected approximately 4.4 out of every 10,000 live births throughout the world.

Furthermore, the growing R&D activities between the major market players, including Fresenius Medical Care AG and Haemonetics Corporation, among others, are further boosting the demand for these devices.

Download Free sample to learn more about this report.

APHERESIS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.93 billion

- 2026 Market Size: USD 4.17 billion

- 2034 Forecast Market Size: USD 6.08 billion

- CAGR: 4.80% from 2026–2034

- North America dominated the market with a 39.69% share in 2025.

- The Consumables segment dominated the market in 2025.

- The Hospitals segment is expected to hold the largest market share of 50.30% in 2026.

North America

The market reached USD 1.56 billion in 2025 and is projected to witness steady growth by 2026, driven by the rising prevalence of chronic diseases, increasing apheresis procedures, favorable reimbursement policies, and advanced healthcare infrastructure.

Europe

The market is projected to reach USD 1.15 billion by 2026, supported by technological advancements in apheresis systems and increasing adoption across healthcare facilities.

Asia Pacific

The market is projected to reach USD 1.01 billion by 2026, driven by expanding hospital infrastructure, improving reimbursement policies, and increasing adoption of advanced apheresis procedures.

U.S.

The market is projected to reach USD 1.47 billion by 2026.

Japan

The market is projected to reach USD 0.26 billion by 2026.

Read More

Apheresis Market Trends

Technological Advancements in these Products to Fuel Market Demand

A key global trend in the market is the preferential shift toward more advanced, software-driven platforms integrated with single-use disposable sets to enhance consistency, throughput, and safety across both donor apheresis and therapeutic apheresis, including leukapheresis, among others.

Additionally, advanced disposables such as redesigned bowls/sets, closed sterile pathways are being adopted to improve efficiency and reduce contamination risk in high-volume plasma centers and hospital apheresis units, thereby fueling the adoption rate for such products.

- For example, in December 2022, the Ghaziabad Unit of Navratna Defense PSU Bharat Electronics Limited (BEL) installed an Apheresis machine in the blood bank of MMG District Hospital, Ghaziabad, as part of its Corporate Social Responsibility (CSR) activities in India.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Occurrence of Chronic Conditions to Drive Market Growth

The increasing occurrence of chronic conditions such as hematologic conditions, renal conditions, and others that require blood component therapy is resulting in the rising demand for therapeutic apheresis procedures among the patient population, consequently triggering the product demand.

- As per the 2024 data published by the Center for Disease Control & Prevention (CDC), it was reported that about 1 in 20 adults has coronary artery disease in the U.S.

This, along with an aging population and improved access to specialty care, is further boosting the adoption rate of these devices in the market. Therefore, the factors above, along with the growing focus of key players on introducing research and development activities to launch novel products, are anticipated to boost the adoption rate of these systems.

Other Prominent Drivers

- Growth in plasma collection for fractionation is driven by demand for plasma-derived therapies.

Market Restraints

High Total Cost Per Apheresis Procedure to Hinder Market Growth

There is an increasing demand for innovative apheresis procedures among the patient population. Moreover, the high all-in cost per procedure is primarily driven by capital-intensive instruments, consumables used for each procedure, replacement fluids, particularly in therapeutic plasma exchange procedures, and others.

Additionally, this increasing cost is limiting adoption in small hospitals, reducing expansion in emerging nations, and creating reimbursement pressure even in developed countries, especially for therapeutic apheresis, where procedure economics depend heavily on payer rates and add-on payments for blood products/replacement solutions.

- For example, as per the 2026 data released by MediGence, the cost of plasmapheresis ranges between USD 2000 to USD 5000 in Jordan.

Market Opportunities

Expansion of Blood Banks and Blood Donation Infrastructure Create Lucrative Market Opportunity

A lucrative opportunity for the global market is the development and modernization of blood bank centers and donation infrastructure, such as new fixed-site collection centers, satellite/mobile drives, hospital-based blood banks, and integrated national blood networks.

This expands the addressable base for apheresis products and consumables and boosts utilization through better donor access, scheduling, and inventory management, particularly relevant in markets where donation rates and access to safe blood remain uneven.

- According to 2025 data published by the World Health Organization (WHO), about 118.5 million blood donations were collected globally.

Market Challenges

Limited Healthcare Access in Developing Nations to Hinder Market Growth

There are growing advancements in apheresis systems among the manufacturers globally. However, growth is constrained by reduced access to advanced hospital services and transfusion infrastructure. Therapeutic apheresis procedures require advanced equipment, consumables including anticoagulants, and replacement fluids, trained professionals, and ICU-level monitoring capabilities that are often limited in a few tertiary centers.

Additionally, fragmented blood collection networks, fewer collection sites, a less developed supply chain, and donor recruitment limitations hamper the scalability of plateletpheresis and plasmapheresis programs.

- For instance, according to 2025 statistics published by the World Health Organization (WHO), the blood donation rate is 5.0 donations per 1000 people in low-income countries.

Other Prominent Challenges

- Competition from alternative therapies and evolving treatment guidelines may hinder the market growth.

- Stringent regulatory guidelines for plasma collection are hampering the market growth.

SEGMENTATION ANALYSIS

By Product Type

Rising Collection of Platelet Units Led to Consumables Segment Dominance

Based on the product type, the market is bifurcated into instruments and consumables.

The consumables segment held the largest revenue share in 2025. The growth is owing to the growing number of platelet unit collections among the patient population, resulting in an increasing adoption of sterile disposable sets worldwide. This, coupled with the rising focus of major players on launching novel consumables, is further anticipated to support the global apheresis market growth.

- For instance, according to 2026 statistics published by America’s Blood Centers and ADRP, approximately 2,618,000 platelet units were distributed, such as single, double, and triple collections and whole blood-derived platelets in 2023 in the U.S.

The instruments segment is expected to grow at a CAGR of 4.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Procedure Type

Increasing Number of Eligible Donors Led to Dominance of Donor Apheresis Segment

Based on procedure type, the market is segmented into donor apheresis and therapeutic apheresis.

The donor apheresis segment reported to have dominated the global market in 2025. By procedure type, the donor apheresis segment accounted for 52.4% in 2025. The reported growth is owing to the rising cases of chronic conditions requiring blood component therapy and the growing number of eligible blood donors, supporting the rising demand in the market for donor apheresis procedures.

- According to the 2026 statistics published by America’s Blood Centers and ADRP, there are about 212 million eligible donors in the U.S.

The therapeutic apheresis segment is set to flourish with a growth rate of 5.0% across the forecast period.

By Technology Platform

Increasing Adoption of Centrifugation based Apheresis Products Led to Dominance of Segment

Based on the technology platform, the market is segmented into centrifugation, membrane filtration, and others.

The centrifugation segment dominated the global market in 2025. By technology platform, the centrifugation segment accounted for 78.4% in 2025. The growth is due to the increasing prevalence of chronic conditions, resulting in the rising adoption of centrifugation-based apheresis systems in the market.

- For instance, according to 2023 statistics published by Terumo Corporation, its Spectra Optia is used for 94% of white blood cell collections in the U.S. and 67% worldwide.

The segment of membrane filtration is set to flourish with a growth rate of 5.1% across the forecast period.

By Application

Growing Number of Plasma Centers Led to Dominance of Plasmapheresis Segment

Based on application, the market is segmented into plasmapheresis, plateletpheresis, leukapheresis, and others.

The plasmapheresis segment dominated the global market in 2025. By application, the plasmapheresis segment held the share of 52.9% in 2025. The growth is owing to the rising number of plasma centers, among others, resulting in a growing number of apheresis procedures globally, thereby contributing to the adoption rate of such devices in the market.

- For instance, according to the 2024 data published by the Plasma Protein Therapeutics Association (PPTA), it was reported that more than 1,200 plasma collection centers are in North America and Europe.

The segment of leukapheresis surgery is set to flourish with a growth rate of 6.0% across the forecast period.

By End User

Increasing Number of Hospitals Led to Segmental Dominance

Based on end user, the market is segmented into hospitals, specialty clinics, blood collection centers & blood banks, and others.

The hospitals segment dominated the market in 2025. The increasing prevalence of chronic conditions, rising number of apheresis procedures in hospitals, and rising number of hospitals, among others, are some of the key factors supporting the growth of the segment in the market. Furthermore, the segment is set to hold an 50.3% share in 2026.

- For instance, according to 2025 data published by Statistisches Bundesamt, there are about 1,874 hospitals in Germany.

In addition, specialty clinics’ end users are projected to grow at a 4.1% CAGR during the forecast period.

Apheresis Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Apheresis Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 1.47 billion, and also took the leading share in 2025 with USD 1.56 billion. The rising prevalence of chronic conditions such as autoimmune disorders, neurological disorders, and others, growing apheresis procedures, advanced reimbursement policies, and advanced hospital infrastructure, among others, are some of the factors supporting the growth of the segment in the market.

- For instance, according to 2024 statistics published by the Centers for Disease Control & Prevention (CDC), about 100,000 people are affected by sickle cell disease in the U.S.

U.S. Apheresis Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.47 billion in 2026, accounting for roughly 35.1% of global sales.

Europe

Europe is projected to record a growth rate of 4.1% in the coming years, which is the second highest among all regions, and reach a valuation of USD 1.15 billion by 2026. The growing technological advancements in such products are anticipated to support the market growth.

U.K. Apheresis Market

The U.K. market in 2026 is estimated at around USD 0.16 billion, representing roughly 5.1% of global revenues.

Germany Apheresis Market

Germany’s market is projected to reach approximately USD 0.26 billion in 2026, equivalent to around 6.3% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.01 billion in 2026 and secure the position of the third-largest region in the market. The fastest growth in these procedures, expanding hospital capacity, and improving reimbursement scenarios in Asia Pacific countries, including South Korea, China, and others, is supposed to support the growth of the market. In the region, India and China are both estimated to reach USD 0.12 billion and USD 0.31 billion, respectively, in 2026.

Japan Apheresis Market

The Japan market in 2026 is estimated at around USD 0.26 billion, accounting for roughly 6.2% of global revenues. Japan has historically reported a relatively high prevalence of chronic conditions, with growing technological advancements in these products.

China Apheresis Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.31 billion, representing roughly 7.4% of global sales.

India Apheresis Market

The Indian market size in 2026 is estimated at around USD 0.12 billion, accounting for roughly 2.8% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.19 billion in 2026. The growth is due to the gradual growth tied to increasing healthcare spending in these regions. The Middle East & Africa are also expected to grow due to the rising number of blood donations in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.07 billion in 2026.

South Africa Apheresis Market

The South Africa market is projected to reach around USD 0.03 billion in 2026, representing roughly 0.8% of global revenues.

Competitive Landscape

Key Industry Players

Rising Number of Product Approvals to Support Dominance of Key Market Players

A strong and varied product portfolio, combined with a major emphasis on global inorganic growth strategies, remains a key factor driving the leadership of these players in the market. In 2025, Fresenius Medical Care AG and Haemonetics Corporation were recorded as prominent companies in the market. Moreover, the increase in contribution of major companies on product approvals is expected to strengthen their presence, further supporting the global apheresis market share.

- For example, in June 2023, Haemonetics Corporation, a medical technology company focused on delivering innovative solutions to drive better patient outcomes, obtained clearance from the U.S. Food and Drug Administration (FDA) for advancements to its NexSys PCS plasma collection system.

Other key players, including Terumo Corporation and others, are also expanding their presence in the market. This is largely driven by their growing focus on acquisitions and collaborations among other players in order to strengthen brand visibility.

List of Key Apheresis Companies Profiled

- Fresenius Medical Care AG (Germany)

- Haemonetics Corporation (U.S.)

- Terumo Corporation (Japan)

- Braun SE (Germany)

- Asahi Kasei Medical Co., Ltd. (Japan)

- Cerus Corporation (U.S.)

- Baxter Corporation (U.S.)

- Nikkiso Co., Ltd. (Japan)

- KANEKA CORPORATION (Japan)

- Miltenyi Biotec (Germany)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Terumo Corporation partnered with Santersus AG to advance a novel technology to improve clinical outcomes for patients who become critically ill due to sepsis.

- September 2025: CSL Plasma and Terumo Corporation announced that the Rika Plasma Donation System has been deployed in all CSL Plasma centers across the U.S., a major milestone in donor care, operational efficiency, and access to lifesaving plasma-derived therapies for patients.

- August 2024: CSL Plasma, a player in plasma collection that creates life-saving medicines, introduced its Rika Plasma Donation System to the seven plasma centers in the Houston, Texas area. This helped the company in strengthening its presence.

- April 2023: Fresenius Kabi announces the availability of a single-needle venous access option for the Amicus Extracorporeal Photopheresis (ECP) System at the 49th annual meeting of the European Society for Blood and Marrow Transplantation (EBMT). This helped the company in strengthening its presence.

- August 2022: Terumo Corporation, a medical technology company, and Eliaz Therapeutics Inc. (ETI), a medical device company. The collaboration uses Terumo's Spectra Optia(R) Apheresis System with ETI's novel XGal-3(R) column, designed to remove Gal-3 from blood plasma selectively.

- October 2020: Haemonetics Corporation, a global medical technology company focused on delivering novel hematology solutions, received U.S. Food and Drug Administration (FDA) 510(k) clearance for its NexSys PCS system with Persona technology.

- February 2019: Fresenius Kabi received 510(k) clearance from the U.S. Food and Drug Administration for the Fenwal Amicus Red Blood Cell Exchange (RBCx) system.

REPORT COVERAGE

The report provides a detailed global apheresis market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, procedure type, technology platform, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Procedure Type, Technology Platform, Application, End User, and Region |

| By Product Type |

|

| By Procedure Type |

|

| By Technology Platform |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 3.93 billion in 2025 and is projected to reach USD 6.08 billion by 2034.

In 2025, the North America regional market value stood at USD 1.56 billion.

Growing at a CAGR of 4.8%, the market will exhibit steady growth over the forecast period.

By product type, the consumables segment is the leading segment in this market.

The introduction of novel apheresis systems is one of the major factors driving the markets growth.

Fresenius Medical Care AG and Haemonetics Corporation are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic conditions, the increasing number of apheresis procedures, among others, are some of the prominent factors anticipated to boost the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us