Artificial Intelligence In Manufacturing Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Services), By Technology (Computer Vision, Machine Learning, Natural Language Processing, and Context Awareness), By Application (Predictive Maintenance & Inspection (PMI), Production Planning, Supply Chain Management, Energy Management, Quality Management, Industrial Robotics, and Others), By Industry (Automotive, Healthcare, Semiconductor & Electronics, Energy & Power, Metals & Machinery, FMCG, and Others ), and Regional Forecast Report, 2026 – 2034

KEY MARKET INSIGHTS

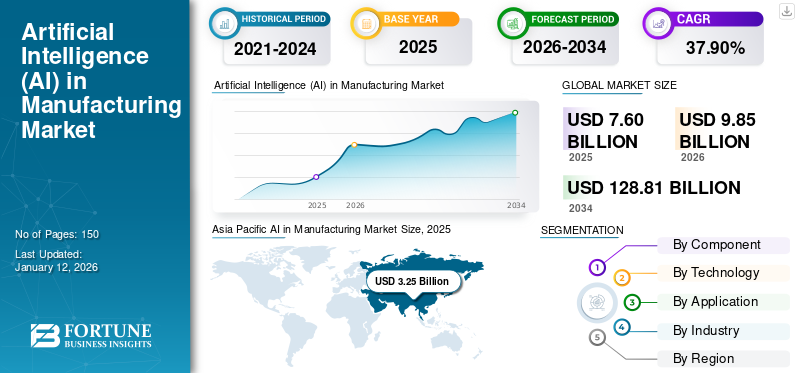

The global artificial intelligence in manufacturing market size was valued at USD 7.6 billion in 2025 and is projected to grow from USD 9.85 billion in 2026 to USD 128.81 billion by 2034, exhibiting a CAGR of 37.90% during the forecast period. The Asia Pacific dominated global market with a share of 42.80% in 2025.

Market Trends and Strategic Insights

- Asia Pacific artificial intelligence in manufacturing market held the largest share of 42.80% of the global market in 2025.

- By component, Hardware segment dominated the market in 2024 due to the growing use of AI infrastructure chipsets and IoT sensors.

- Based on technology, Machine learning segment held the highest market share in 2024 and is projected to remain dominant during the forecast period.

- By application, Production planning segment led the market in 2024 owing to the rising adoption of AI-driven optimization solutions.

- Based on industry, Semiconductor & electronics segment held the highest market share in 2024.

Market Size and Growth Forecast

- 2025 Market Size: USD 7.6 Billion

- 2026 Market Size: USD 9.85 Billion

- 2034 Projected Market Size: USD 128.81 Billion

- CAGR (2026–2034): 37.90%

- Asia Pacific: Largest market in 2025

- North America: Second-largest market with strong AI infrastructure investment

Artificial intelligence (AI) is a critical set of technologies used in machine processes to enhance production efficiency, reduce downtime, and achieve optimal results through massive data generation and transmission. Machine learning and deep learning are among the modern trends of AI in manufacturing, shaping a resilient future and addressing real-world challenges. Innovative technologies such as computer vision, machine learning, natural language processing, and context awareness are further strengthening the AI industry. Expanded availability of AI solutions and integration of AI-driven systems by key players such as Microsoft, Siemens, and others are driving data-driven process optimization and supporting smart factory strategy. According to a Microsoft Corporation report in 2019, 15% of businesses are currently leveraging AI, and 31% of businesses are planning to implement an intelligent system over the next few years. Many industries are heavily investing in building smart factories to improve production and leverage the benefits of AI in manufacturing.

The COVID-19 pandemic laid a strong foundation for the growth of the AI market, driven by high demand for data-driven decision-making to navigate volatile market dynamics. Besides, the rising adoption of Industry 4.0 by manufacturers is expected to boost demand for AI in factory optimization, accelerating the integration of AI in the manufacturing sector.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Growing Use of AI to Streamline Production Boosts Market Growth

Modern AI techniques, such as image synthesis and machine learning, are gaining popularity in the tool & manufacturing industry. These modern techniques help create innovative designs, improve production techniques, and provide solutions to optimize processes in manufacturing. Machine learning, in particular, enables industry to generate new ideas and refine production workflows by minimizing repetitive tasks and streamlining operations to achieve desired results. For example, Airbus adopted Industry 4.0 for its new aircraft product development. Leveraging AI technology, the company validated that no extra costs were required for the new aircraft project.

- For instance, in April 2023, Siemens and Microsoft harnessed the collaborative power of generative AI to help industrial companies boost innovation and efficiency across the entire product operational lifecycle. As part of this initiative, Siemens integrated Teamcenter with Microsoft Teams and Azure-based large language models to enhance cross-functional collaboration.

IMPACT OF TARIFFS

Rising Cost Pressures and Supply Chain Disruption Pose Challenge to Market Growth

Recently announced U.S. tariffs have introduced major challenges for the AI infrastructure. Tariffs on imports from countries such as China, Mexico, Taiwan, Vietnam, and Canada have impacted the AI semiconductor sector, which heavily relies on global supply chains. These tariffs, around 10%, aimed to revitalize domestic manufacturing but have also increased cost pressure on U.S. manufacturers. As a result, the added financial pressure could hamper cost structures, increase operational costs, and delay the timely deployment of AI technologies due to elevated implementation costs.

ARTIFICIAL INTELLIGENCE IN MANUFACTURING MARKET TRENDS

Adoption of Digital Twin Technology to Fuel Market Growth

AI is making precise manufacturing processes more feasible through enhanced simulated designs and high-resolution modeling using digital twin technology. This supports innovative applications such as product design and performance analysis, contributing to the long-term adoption of AI in the manufacturing sector. In manufacturing, AI development is often directed by human experts who encode their expertise into intelligent systems. Over time, modern solutions such as autonomous AI systems, built on this expert knowledge, are streamlining processes such as preventive maintenance, quality control, and resilient production planning. These technological advancements are shaping emerging industry trends and are expected to boost the artificial intelligence in manufacturing market share during the forecast period.

- For instance, in October 2024, Siemens and Microsoft collaborated to scale up the Industrial Co-pilot to the next level, enhancing its ability to operate in demanding industrial environments. The solution has already been deployed by 100 customers across Europe to cut downtime, improve operational efficiency, and address labor shortages, benefiting more than 1,20,000 engineers.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Investments in Industry 4.0 to Drive Product Demand

Artificial intelligence in manufacturing is being driven by the expanding applications of innovative technologies, including digital twins, machine learning, and AR/VR. The global push toward Industry 4.0 is accompanied by substantial investments aimed at implementing AI-powered, trained predictive maintenance and automated processes across manufacturing lines. Over the past two decades, automation has played a pivotal role in various industries by performing predefined tasks. The industry is evolving with the use of intelligent robots capable of learning from repetitive tasks, simulating scenarios, mitigating risks, minimizing the number of steps, and improving productivity on the production floor. The use of AI brings a wide range of innovations in manufacturing that improve the availability and quality of goods, impacting the proliferation of AI. It enables manufacturers to detect even the smallest imperfections and improve them proactively, further driving the adoption of AI in manufacturing.

- For instance, according to the Manufacturing Leadership Council, Investment in AI for manufacturing is expected to reach USD 16.7 billion by 2026. The survey reports that only 28% of the manufacturers have cleared the pilot project, and 56% are still using AI in small-scale projects.

Market Challenges

Data Privacy Concerns and Lack of Technical Knowledge to Hinder Market Growth

Despite the market's vast potential, AI continues to face short-term challenges, owing to the rising upfront costs associated with infrastructure development. Implementing AI solutions in manufacturing environments carries potential risks, particularly in integrating new systems, which raises concerns about data privacy. While the integration of digital twins and Industrial IoT offers major benefits, the shortage of technologically skilled individuals capable of managing and safeguarding data further complicates AI deployment.

Market Opportunities

Evolution toward Industry 5.0 Present Significant Growth Opportunities

The increasing demand for modern technologies in production lines began with the emergence of smart factories and has been further proliferated by Industry 4.0 initiatives. The implementation of artificial intelligence in manufacturing enables manufacturers to process vast amounts of data for real-time analysis, while also optimizing production processes through applications such as digital twin technology, predictive maintenance, and AI-assisted visual inspection. Furthermore, conversational AI, powered by natural language processing, enhances production efficiency and technical proficiency. These advancements collectively empower businesses to maximize throughput, retain critical knowledge, and bridge technical skill gaps, laying the foundation for Industry 5.0 and contributing to the progressive expansion of artificial intelligence in manufacturing over the long term.

- For instance, in April 2024, Cognizant and Microsoft announced a partnership aimed at boosting the adoption of generative AI. The collaboration is designed to help employees and enterprises operationalize AI. It helps businesses transform business operations and accelerate cross-industry innovation.

SEGMENTATION ANALYSIS

By Component

Hardware Segment Leads Due to Growing Use of Modern AI Infrastructure Chipsets

By component, the market is divided into hardware, software, and services.

The hardware segment will account for 45.89% market share in 2026, owing to the growing adoption of modern AI infrastructure chipsets, IoT sensors, AR/VR devices, and edge computing systems. Significant investments are being made to build AI infrastructure capable of mimicking human intelligence and automating complex industrial tasks.

The software segment is experiencing rapid growth, particularly among manufacturers that already have the necessary infrastructure in place. These companies are increasingly leveraging AI software to address complex challenges such as predictive testing, quality assurance shortfall, and program optimization.

The services segment is showcasing steady growth, driven by demand for post-deployment support services to maintain servers, manage computing workloads, and ensure consistent Service Level Agreements (SLA) compliance.

By Technology

Machine Learning Leads, Owing to Its Cruciality in Automating Industrial Tasks

By technology, the market is categorized into computer vision, machine learning, natural language processing, and context awareness.

The Machine learning segment is expected to account for 40.10% of the market in 2026, owing to its critical role in automating complex industrial tasks more efficiently. Machine learning implementation can help AI-trained robots interpret commands more effectively and develop new methods by analyzing data from multiple data sources. In smart manufacturing, these intelligent machines help detect faults and identify repetitive steps. The technology mimics human intelligence and optimizes the production processes, which saves a lot of time and capital.

Natural language processing is the next highly implemented technology in manufacturing. It enables real-time analysis on the factory floor, facilitating proactive decision-making and helping bridge gaps in knowledge sharing using natural language interfaces.

Computer vision and context awareness are revolutionizing the quality control process. These technologies improve vision capabilities through AI-integrated cameras and vision systems that can conduct AI-based automated inspections and identify defects that are not easy for human eyes to catch.

By Application

Production Planning Segment Leads due to Growing Adoption of AI Technologies

By application, the market is divided into predictive maintenance & inspection (PMI), production planning, supply chain management, energy management, quality management, industrial robotics, and others (field services).

The production planning segment is dominating the artificial intelligence in the manufacturing market, driven by the increasing use of AI technologies to deliver optimized production plans based on past data and API-sourced inputs. These data-driven strategies help mitigate demand patterns and lower the risks of bottlenecks, ensuring smoother operations without hampering cash flow and inventory levels. The Production Planning segment is anticipated to hold a dominant market share of 23.96% in 2026.

The predictive maintenance and inspection of machines and equipment are rising as businesses leverage benefits such as minimized downtime, optimized inventory, and proactively maintaining machines. ML plays a key role in enabling preventive maintenance, which is gaining popularity for its ability to prevent operational losses.

The increasing adoption of industrial robotics is extending AI applications into quality management, supply chain management, and field services. The rise in robotics also intensifies competition in achieving successful automation across global markets. AI has a substantial impact on quality management and enables early detection of product defects during the early stages of production. Manufacturers are optimizing energy management by using real-time data analytics to plan distribution and net loss in transmissions. Thus, the implementation of artificial intelligence in manufacturing improves key functions such as product quality, production planning, supply chain operations, customer service, and energy management.

To know how our report can help streamline your business, Speak to Analyst

By Industry

Semiconductor & Electronics Segment Dominates Due to Rising Product Usage in Manufacturing Processes

By industry, the market is categorized into automotive, healthcare, semiconductor & electronics, energy & power, metals & machinery, FMCG, and others (aerospace & defence).

The semiconductor & electronics segment is dominating the adoption of AI within their manufacturing processes. By implementing AI, manufacturers can optimize production workflows, enhance product quality, reduce costs, and improve inventory management. The Semiconductor & Electronics segment is expected to account for 25.28% of the market in 2026.

In the automotive industry, AI adoption is accelerating due to its multiple advantages, including AI-driven production planning, preventive maintenance, machine inspection, yield optimization, and quality control.

The healthcare industry utilizes AI across various applications, such as quality testing, telematics, healthcare software, and machine predictive maintenance from generated data. Quality assurance and rising investment are boosting the adoption of AI in the medical device industry.

AI is playing a transformative role in energy & power, industrial machinery, FMCG, and other sectors. These industries are benefiting from advanced AI applications, including predictive maintenance, fault identification, energy management, and process optimization.

ARTIFICIAL INTELLIGENCE IN MANUFACTURING MARKET REGIONAL OUTLOOK

Asia Pacific

Asia Pacific AI in Manufacturing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 42.80% to the global market in 2025, with a valuation of USD 3.25 billion, and is projected to reach USD 4.3 billion in 2026. Asia Pacific is dominating the global artificial intelligence in manufacturing market, driven by the growing usage of AI across diverse manufacturing activities. The region’s dynamic use cases and increasing investment in AI development, particularly in key markets such as China, India, Japan, and South Korea, are accelerating the proliferation of AI technologies operations in the manufacturing industry. The Japan market is projected to reach USD 0.8 billion by 2026 and the India market is projected to reach USD 0.76 billion by 2026.

China is the leading country in the Asia Pacific region with the largest market share, owing to the tech-savvy youth population skilled in machine learning and AI advancements. China market is projected to reach USD 1.8 billion by 2026. The country is heavily investing in AI developments to replace and automate production lines with humanoid robots, contributing significantly to the global AI momentum. On the other hand, countries such as India are witnessing strong growth through government-led initiatives, such as Make in India and the promotion of Industry 4.0. The schemes incentivize manufacturers to integrate AI technologies, such as AI and IoT, to enhance productivity. Additionally, many companies, such as Japan and Southeast Asia, are exploring the emerging market for testing AI technologies.

North America

In 2025, North America represented USD 2.18 billion, accounting for 28.70% of the worldwide market, and is projected to grow to USD 2.82 billion in 2026. North America's market for AI in manufacturing is shaped by persistent semiconductor shortages and the ongoing chip war, which slows down the development of AI infrastructure. Furthermore, the complex tariff situation and sourcing problems caused by geopolitical tensions are slowing growth, although the region still holds a second position in the market.

The U.S., in particular, faces market uncertainty due to unclear tariff policies and a shift in manufacturing activities toward emerging markets such as India, China, and Taiwan. Despite these hurdles, the growing software industry and expanding AI-driven services sector continue to support the U.S. market’s resilience in the near term. The U.S. market is projected to reach USD 1.99 billion by 2026

Latin America

The market in Latin America reached USD 0.34 billion in 2025, representing 4.40% of total market revenue, and is projected to reach USD 0.41 billion in 2026. The Latin America region is witnessing significant growth, driven by the expansion of semiconductor facilities and shifting industrial demands. However, U.S. nearshoring strategies and tariff-related geopolitical issues present ongoing challenges to regional sustained growth.

Europe

The Europe market generated USD 1.58 billion in 2025, representing 20.70% of the global market landscape, and is expected to reach USD 2.01 billion in 2026. Europe's market is likely to grow at a moderate pace during the study period. This is supported by significant investments, estimated at USD 1.3 billion in artificial intelligence technology. Furthermore, growing applications of AI in modern manufacturing processes to minimize defects in production lines and automate tasks are driving the market. Germany, Italy, and the U.K. are the top countries in the region, witnessing progressive growth. The UK market is projected to reach USD 0.54 billion by 2026, while the Germany market is projected to reach USD 0.63 billion by 2026.

Middle East & Africa

The Middle East & Africa market was valued at USD 0.26 billion in 2025, capturing 3.40% of global revenue, and is estimated to reach USD 0.32 billion in 2026. The Middle East & Africa region holds significant long-term potential for artificial intelligence in manufacturing. The government of UAE launched the UAE Strategy for AI, promoting smart transformation through initiatives such as Smart Dubai and dedicated AI labs.

Meanwhile, in Africa, a young, tech-savvy population is driving interest in emerging technologies such as blockchain and crypto, which further strengthen the artificial intelligence in manufacturing market growth.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Deploying Automated Solutions to Reduce Defects

AI advancements and deployment are largely shaped by key players focusing on integrating automated solutions capable of handling the complexities of modern production lines while ensuring high product quality. Through AI integration, businesses are increasingly leveraging past data to minimize faults, reduce defects, and lower operational costs. Additionally, government incentives and strategic capital allocations aimed at supporting AI-led manufacturing are further driving the demand for AI solutions across various industries, strengthening the market in the long term.

- For instance, in April 2024, Microsoft announced a partnership with G42 to deliver advanced AI solutions via Microsoft Azure across various industries. For the project, Microsoft would invest USD 1.5 billion for a minority stake in G42. Companies would support a USD 1 billion fund for developers to boost AI skills in UAE.

List of Key Artificial Intelligence in Manufacturing Companies Profiled

- Microsoft Corporation (U.S.)

- Siemens AG (Germany)

- General Electric Company (GE) (U.S.)

- IBM Corporation (U.S.)

- SAP SE (Germany)

- Rockwell Automation Inc. (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Schneider Electric SE (France)

- ABB Ltd. (Switzerland)

- Honeywell International Inc. (U.S.)

- Dassault Systèmes SE (France)

- PTC Inc. (U.S.)

- Autodesk Inc. (U.S.)

- Cisco Systems Inc. (U.S.)

- Intel Corporation (U.S.)

- NVIDIA Corporation (U.S.)

- Robert Bosch GmbH (Germany)

- Huawei Technologies Co., Ltd. (China)

- Oracle Corporation (U.S.)

- Accenture plc (Ireland)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Siemens Industries announced its intent to acquire Wevolver, a move aimed at expanding Siemens's audience reach and enhancing its Supplyframe product portfolio. This acquisition would bolster Siemens’s capabilities in digital marketing and integrated campaign management, including go-to-market support and content creation.

- March 2025: Siemens and Accenture announced the formation of a new business group comprising 7,000 professionals with proven manufacturing and IT experience globally. The collaboration focuses on co-developing and jointly marketing AI-powered solutions to clients that combine automation, industrial AI, and software.

- March 2025: Siemens announced the acquisition of Altair Engineering Inc., a leading provider of industrial simulation and analysis software, for a valuation of USD 10 billion. The acquisition aims to extend Siemens's leadership in simulation and industrial Artificial Intelligence (AI) by adding new capabilities in mechanical and electromagnetic simulation, high-performance computing (HPC), data science, and AI.

- February 2025: Microsoft Corporation and Andruil Industries, a defense technology group, expanded their partnership to support the U.S. Army’s Integrated Visual Augmented System (IVAS) program. This partnership positions Microsoft Azure as the preferred hyperscale cloud for all IVAS workloads and Andruil AI technologies.

- November 2024: Siemens Digital Industries announced the latest advancement in its electronics system design software, combining the capabilities of Xpedition, Hyperlynx, and PADS Professional into a next-generation platform. These tools deliver cloud connectivity and AI capabilities to drive innovation.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Global players are leveraging their market presence as an advantage to expand their product portfolio with modern product and service offerings. Thus, players diversify their investments in new trends, innovations, and technology advancements to lead the market and expand their reach.

- March 2025: Siemens planned to invest USD 108 million over a five-year tenure to establish a global AI manufacturing technology Research and Development (R&D) center for battery production in Canada. The R&D center is initially located in Oakville, Canada. The facility will leverage Siemens’ expertise in AI, edge computing, machine vision, cybersecurity, and digital twins.

REPORT COVERAGE

The artificial intelligence in manufacturing market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, components, technology, and product applications. It also offers insights into market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 37.90% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

By Technology

By Application

By Industry

By Region

|

|

Companies Profiled in the Report |

Microsoft Corporation (U.S.), Siemens AG (Germany), General Electric Company (GE) (U.S.), IBM Corporation (USA), SAP SE (Germany), Rockwell Automation Inc. (U.S.), Mitsubishi Electric Corporation (Japan), Schneider Electric SE (France), ABB Ltd. (Switzerland), and Honeywell International Inc. (U.S.). |

Frequently Asked Questions

The market is projected to reach USD 128.81 billion by 2034.

In 2026, the market was valued at USD 9.85 billion.

The market is projected to grow at a CAGR of 37.90% during the forecast period.

By component, the hardware segment leads the market.

Rising Investments in Industry 4.0 is a key factor driving market growth.

The top players in the market are Microsoft Corporation, Siemens AG, General Electric Company, IBM Corporation, SAP SE, Rockwell Automation Inc., Mitsubishi Electric Corporation, Schneider Electric SE, ABB Ltd, and Honeywell International Inc.

he Asia Pacific dominated global market with a share of 42.80% in 2025.

By application, production planning segment dominates the market.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us