Artificial Intelligence in Military Market Size, Share, and Industry Analysis By Offering (Hardware, Software, and Services), By Application (Warfare Platform, Cyber Security, Logistics & Transportation, Surveillance & Situational Awareness, Command & Control, Battlefield Healthcare, Threat Detection, By Technology (Machine Learning, Context-Aware Computing, Computer Vision, Intelligent Virtual Agent (IVA) /Virtual Agents & Others), By Platform (Land, Naval, Airborne, & Space), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

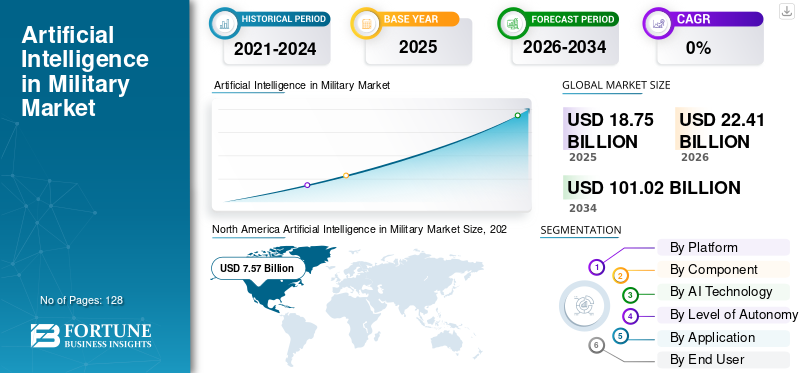

The global artificial intelligence in military market size was valued at USD 18.75 billion in 2025. The market is projected to grow from USD 22.41 billion in 2026 to USD 101.02 billion by 2034, exhibiting a CAGR during the forecast period of 20.7%. North America dominated the global artificial intelligence in military market with a market share of 40.37% in 2025.

Artificial intelligence in the military involves using algorithms, machine learning models, autonomous systems, and data-driven software to improve how armed forces gather information, make decisions, and take action on the battlefield. It marks a move from manual processes to systems that can quickly analyze large amounts of data, predict threats, automate tasks, and support faster, more accurate decisions. Nations are investing heavily in AI to enhance intelligence, surveillance, and reconnaissance (ISR), counter new unmanned threats, secure their networks, reduce decision-making time, improve training realism, and modernize logistics. Increasing geopolitical tensions, the rise of autonomous platforms, and the demand for AI-enabled command and control are driving this market forward quickly.

The AI in military applications consist of traditional defense companies and newer software-driven firms. On the hardware and mission systems side, companies such as Lockheed Martin, Northrop Grumman, RTX (Raytheon), BAE Systems, Thales, Leonardo, Airbus Defence & Space, IAI, Rafael, and Elbit Systems are integrating AI into radars, ISR pods, EW suites, command systems, and autonomous platforms. Whereas, Palantir, Anduril, Microsoft, Google, Amazon, IBM, and a growing number of defense-focused AI startups are providing data platforms, model pipelines, battle management tools, and autonomy stacks.

Download Free sample to learn more about this report.

ARTIFICIAL INTELLIGENCE IN MILITARY MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 18.75 Billion

- 2026 Market Size: USD 22.41 Billion

- 2034 Forecast Market Size: USD 101.02 Billion

- CAGR: 20.7% from 2026–2034

- North America dominated the artificial intelligence in military market with a 40.37% share in 2025.

- The Air platform segment held the largest share of the global market.

- Hardware emerged as the leading component segment in 2025.

North America

North America generated USD 7.57 billion in 2025 and accounted for 40.37% of the global market.

Europe

Europe reached USD 4.71 billion in 2025 and is projected to grow at a CAGR of 21.8% during the forecast period.

Asia Pacific

Asia Pacific is projected to be the fastest-growing region with a CAGR of 23.0% during the forecast period.

U.S.

The country contributed over 94.06% of North America's market share in 2025.

Japan

The market is expanding steadily as regional AI defense investments increase.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Post-Ukraine Modernization Wave Accelerates AI Adoption in Defense

The war in Ukraine has turned AI from a future idea into a current operational priority. Militaries have witnessed how drones, loitering munitions, counter-UAS systems, and digital command-and-control can determine the outcome of battles. As a result, budgets are shifting from traditional hardware to C4ISR, autonomy, and data-driven systems. This change is moving AI projects from research labs to funded programs that are central to force modernization plans, particularly in Europe and North America.

In March 2024, the U.S. Department of Defense requested about USD 1.8 billion specifically for AI and autonomy in its FY2025 budget. This request includes the rapid development of autonomous systems and decision-support tools under the Replicator initiative and the Chief Digital and AI Office.

MARKET RESTRAINTS

Growing Technological Complexity and Talent Gaps Slow AI Adoption in Military Systems

Defense forces are pushing to adopt machine learning, autonomous platforms, and AI driven decision tools. However, the rapid rise in technology demands has made modern military systems more complex to manage for defense organizations. Even countries that are heavily investing in AI technology, such as South Korea, South Africa, and several nations in Latin America, struggle with a lack of data engineers, algorithm specialists, and autonomy testers. This shortage of talent delays program timelines, raises integration costs, and limits how quickly AI can be integrated into next-generation defense systems.

MARKET OPPORTUNITIES:

Expanding Demand for Autonomous and AI-Driven Defense Systems Creates New Growth Pathways

A major opportunity in the artificial intelligence military market comes from the global push toward autonomous platforms and smarter military systems that require less human input. Countries want AI driven capabilities that improve surveillance, targeting, decision-making, and border security. This interest grows as defense forces aim to enhance their military capabilities without significantly increasing manpower. This shift allows for advance integration of AI into defense, from machine learning powered threat prediction to autonomous mission planning. This creates a growing market for AI-enabled defense systems, data-fusion solutions, and semi-autonomous mission platforms.

ARTIFICIAL INTELLIGENCE IN MILITARY MARKET TRENDS:

Shift toward AI-Driven, Multi-Domain Military Applications Reshapes Global Defense Strategies

The military use of artificial intelligence (AI) is shifting toward AI-driven, multi-domain systems that combine autonomy, machine learning, and advanced data analysis into mission. Militaries are no longer viewing AI as a niche addition; it is becoming the main software layer in modern defense systems. This includes autonomous drones, unmanned ground vehicles, predictive maintenance tools, and AI-supported command centers. The larger defense sector is heavily investing in machine learning-enabled targeting, battlefield automation, digital twins for training, and joint operations across all domains. The trend showcase AI is becoming the foundation of future military platform and capabilities developed, managed, and improvements.

MARKET CHALLENGES:

Fragmented Data, Legacy Systems, and Trust Issues Slow AI-Driven Adoption

Major challenge in artificial intelligence in military market growth is that most forces try to add new AI technology to outdated defense systems and isolated data. Real integration of AI into defense requires linking sensors, command tools, logistics, and weapons across different areas. However, many military systems still operate on legacy structures that weren't designed for machine learning or real-time data integration. This leads to complicated integration projects, cybersecurity concerns, and trust issues among military forces results in hesitation to allow AI-driven tools to integrate into old platforms or systems.

Russia Ukraine War Impact

The Russia-Ukraine conflict has become a key driver for militaries to modernize with AI. The war has demonstrated how autonomous platforms, digital targeting, counter-UAS tools, machine-learning-based ISR, and rapid battlefield data fusion can change the dynamics of modern combat. Countries now knows traditional military systems are not effective against drones, electronic warfare, long-range fires, and cyber operations and at the pace they are evolving rapidly. Countries are focusing on faster decision-making, multi-domain integration, and more resilient command networks. Defense contractors including Lockheed Martin, Northrop Grumman, and BAE Systems are speeding up the development of autonomous systems and AI-enabled defense tools, considering data from Ukraine in AI-assisted targeting, automated threat recognition, and predictive logistics. The war has confirmed the importance of artificial intelligence (AI) in military operations, prompting governments to accelerate the integration of AI into defense planning, purchasing, and frontline uses.

In June 2023, Ukraine's Ministry of Digital Transformation confirmed the rapid growth of AI-enabled battlefield tools. These include machine-learning-based drone detection and AI-assisted imagery analysis, driven by frontline units reporting that automated analysis was cutting down targeting and response times during intense combat.

Download Free sample to learn more about this report.

Segmentation Analysis

By Platform

Rising Demand for Technological Superiority and AI-Driven Air Power, Air Segment Dominates the Platform Market

In terms of by platform, the market is categorized into land, air, naval, space, and joint/multi domain.

Air platforms lead the military market for artificial intelligence (AI), the dominance is attributed to air forces technological superiority over other platform. This is especially true for high-end military systems such as fighter jets, ISR aircraft, and advanced drones. These platforms are capable for machine learning, computer vision, and data-fusion tools that convert raw sensor data into useful intelligence. As a result, integrating AI into defense aviation is a top priority for many countries. They aim to include autonomy, decision support, and targeting intelligence in airborne defense systems. Resulting in air segment lead the market followed by land, naval, and other platforms in AI funding respectively.

Space segment in market expected to show fastest grow at a CAGR of 23.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Growing Demand for AI-Capable Defense Systems, Hardware Segment Dominates Component Market

On the basis of by component, the market is classified into hardware, software, and services.

The hardware segment leads the artificial intelligence (AI) in military market due to every advancement in AI capability must fit into physical defense systems, including sensors, processors, radios, and weapon platforms. To achieve real technological edge, defense ministries are investing heavily in rugged compute modules, machine learning accelerators, next-generation radars, electro-optical/infrared suites, and onboard electronics that can run sophisticated algorithms and support the development of autonomous vehicles. As a result, hardware remains the primary investment in many AI-enabled military applications, creating the base of better military capabilities while software and services continue to grow more quickly.

Software segment is expected to show fastest growth at a CAGR of 22.4% over the forecast period.

By AI Technology

Central Role in Enabling AI-Driven Military Applications, Machine Learning and Deep Learning Segment Dominates AI Technology Market

Based on by AI technology, the market is segmented into, machine learning & deep learning, computer vision, data fusion & predictive analytics, autonomous navigation & guidance, generative ai & large models, swarm intelligence & multi-agent systems, and others.

The machine learning and deep learning segment leads the artificial intelligence (AI) market in the military sector because nearly every significant AI-driven feature in modern military systems relies on these algorithms. This includes computer vision for ISR, predictive maintenance for engines, targeting support, cyber defense analytics, and the development of autonomous drones and vehicles. Machine learning is the driving reason behind these capabilities. They aim for deeper AI integration into defense. As ML and DL are key to improving military roles such as threat detection, sensor fusion, electronic warfare, and autonomous navigation, they hold a significant share of the AI technology in the global defense sector.

Generative AI & Large Models segment is fastest growing segment in market at a CAGR of 24.6% growth across the forecast period.

By Level of Autonomy

Operational Trust, Safety Requirements, and Compliance Needs, Human-In-the-Loop Segment Dominates Autonomy Market

Based on by level of autonomy, the market is segmented into human-in-the-loop, human-on-the-loop, and high-autonomy systems.

The human-in-the-loop segment leads the artificial intelligence (AI) market in the military. Militaries remain alert about giving full control to autonomous platforms, especially in lethal or high-risk situations. Militaries want the speed of AI-driven analytics and machine learning, but they also want human judgment supervision critical decisions in complex military systems. Until countries gain more confidence in fully autonomous operations, human-in-the-loop systems will remain the main way of integrating AI into defense, prompting new military applications and autonomous platforms develop.

High-Autonomy Systems segment is expected to show fastest growth at a CAGR of 27.0% growth across the forecast period.

By Application

Need for Faster, Deeper Battlefield Visibility; ISR and Situational Awareness Segment Dominates Application Market

On the basis of by application, the market is segmented into ISR & situational awareness, autonomous & remotely operated platforms, command, control & battle management, cyber defence & information operations, logistics, maintenance & support, training, simulation & wargaming, and others.

ISR and situational awareness dominate the use of artificial intelligence (AI) in the military market. Technological dominance starts with seeing and understanding the battlespace better than the opponent. Only AI-driven analytics and machine learning can quickly turn that data into useful insights. Enhancing detection, tracking, and threat classification immediately increases overall military capabilities and supports the development of autonomous platforms that depend on situational awareness. As a result, ISR-focused military applications holds the largest share of AI spending across modern military systems in the global defense sector.

Autonomous & Remotely Operated Platforms segment is expected to show fastest growth at a CAGR of 24.8% growth across the forecast period.

By End User

Air forces Play a Central Role in High-end Air Power and Technology, as a result, they Dominate End User Market

Further the market is segmented by end user, into land forces, air forces, navies, and others.

Air Forces lead the artificial intelligence (AI) market in the military because they are at the forefront of technological power. They operate the most advanced military systems, such as fighters, ISR aircraft, tankers, and high-end drones. These assets are ideal for AI-driven avionics, machine learning-based sensor fusion, and autonomous mission aids. As a result, air forces are often the first to benefit when governments invest in AI and next-generation technology. Additionally, the creation of autonomous loyal wingmen and unmanned combat aircraft keeps Air Forces at the forefront of AI-focused military applications worldwide.

Others segment is expected to show fastest growth at a CAGR of 23.2% growth across the forecast period.

Artificial Intelligence in Military Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World (Middle East & Africa, and Latin America).

North America Artificial Intelligence in Military Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America held the dominant artificial intelligence in military market share in 2024 valuing at USD 6.39 billion and also took the leading share in 2025 with USD 7.57 billion, led primarily by the U.S., which alone contributes over 94.06% share in 2025 of the regional share. The U.S. have large defense budgets and a strong network of prime contractors, software companies, and laboratories, all competing for technological leadership. Resulting this region boasts some of the world’s most advanced military systems. It is also focused on developing autonomous aircraft, unmanned systems, and AI-driven command and control. This makes it the central hub for AI technology in the global defense industry.

Europe

Europe is expected to see significant growth in artificial intelligence in military market in the coming years. During the forecast period, the Europe region is projected to have a growth rate of 21.8%. The market in Europe is estimated to be USD 4.71 billion in 2025, driven directly by the Russia-Ukraine war. In this region, both the U.K. and France are expected to reach USD 1.22 billion and USD 1.02 billion, respectively, in 2026. Governments are focusing to integrate AI technology into ISR, air defense, electronic warfare, and digital command and control. Russia is working to modernize its old defense systems with more automation. NATO countries are investing in AI not only for pilots and analysts but also for various military applications.

Asia Pacific

Asia Pacific is anticipated to fastest growing segment in the global artificial intelligence in military market growing at a CAGR of 23.0%. China, India, Japan, and South Korea are making significant progress in developing autonomous drones, loyal wingmen, and smart ISR networks, driving the growth of this market in Asia pacific region. Based on these factors, countries such as China expect to reach a valuation of USD 2.39 billion, and India is set to reach USD 0.90 billion by 2026.

Rest of the World

Meanwhile, Rest of the world (Middle East & Africa and Latin America) contributes 10.15% in 2025. Middle East & Africa and Latin America, has comparatively smaller in share but is growing at a CAGR of 20.5%. In the Middle East and Africa, Israel, and South Africa are investing in AI technology and upgrades to their existing defense systems. Latin America, budgets are tighter, but there is growing interest in specific military applications such as AI-assisted border security, coastal surveillance, and tracking organized crime.

COMPETITIVE LANDSCAPE

Key Industry Players:

Intense Focus on Technological Superiority Means AI in Military Market is Highly Concentrated and Quickly Changing

The military artificial intelligence (AI) market is still largely dominated by a few major defense companies, but their competition is changing quickly. Lockheed Martin Corporation, Northrop Grumman Corporation, and BAE Systems plc. are incorporating AI technology and machine learning into advanced military systems, such as fighters, ISR platforms, integrated air and missile defense, and command networks. They aim to maintain a technological edge. Their strategies focus on providing AI-ready defense systems and upgrade options. This allows customers to start with partial automation and eventually move toward more AI-driven and semi-autonomous capabilities. This approach has become a key selling point for ministries that want to integrate AI into defense without replacing entire fleets.

Meanwhile, specialist software companies, cloud service providers, and autonomy startups are supplying the intelligence needed for these platforms, such as battle-management algorithms, autonomous swarms, and edge analytics. Countries including South Korea, South Africa, and several in Latin America are encouraging local industries to collaborate with global leaders to maintain control over sensitive data and develop AI skills within their defense sectors. As a result, the market has become layered. A few major original equipment manufacturers (OEMs) manage complex hardware and system integration, while a growing number of AI firms provide specialized military applications and services.

LIST OF KEY ARTIFICIAL INTELLIGENCE IN MILITARY COMPANIES PROFILED:

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Raytheon / RTX Corporation (U.S.)

- BAE Systems plc. (U.K.)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

- Airbus Defence and Space (Netherlands)

- Israel Aerospace Industries Ltd (Israel)

- Rafael Advanced Defense Systems Ltd (Israel)

- Elbit Systems Ltd (Israel)

- Saab AB (Sweden)

- L3Harris Technologies, Inc. (U.S.)

- General Dynamics Corporation (U.S.)

- Anduril Industries, Inc. (U.S.)

- Palantir Technologies Inc. (U.S.)

- IBM Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Google LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In July 2025: Palantir Technologies signed an enterprise agreement with the U.S. Army valued at up to USD 10 billion over ten years, consolidating dozens of existing software deals into a single framework to provide AI-enabled data integration, analytics and targeting tools as the backbone of the Army’s long-term data and AI strategy.

- In July 2023: South Korea’s Defense Acquisition Program Administration (DAPA) announced new investments in AI-powered air defense analytics and autonomous drone swarms. This move supports Seoul’s effort to build domestic AI-driven military capabilities.

- In November 2023: Northrop Grumman Corporation completed a successful test of an AI-enabled multi-domain battle management prototype that autonomously recommended threat responses. This was one of the most notable demonstrations of AI-driven C2 to date.

- In February 2024: BAE Systems plc received a contract from the U.K. Ministry of Defence to integrate machine-learning-based targeting and sensor-fusion software into next-generation land and air platforms. This contract helps the U.K.’s effort toward AI-ready military systems.

- In January 2024: The U.S. Navy awarded a contract to L3Harris Technologies to integrate AI-powered sensor fusion and autonomous navigation algorithms into unmanned surface vessels (USVs). This expands naval autonomy initiatives.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 20.7% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform

|

|

By Component

|

|

|

By AI Technology

|

|

|

By Level of Autonomy

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region |

North America (By Platform, By Component, By AI Technology, By Level of Autonomy, By Application, By End User, and By Country)

Europe (By Platform, By Component, By AI Technology, By Level of Autonomy, By Application, By End User, and By Country)

Asia-Pacific (By Platform, By Component, By AI Technology, By Level of Autonomy, By Application, By End User, and By Country)

Rest of the World (By Platform, By Component, By AI Technology, By Level of Autonomy, By Application, By End User, and By Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 22.41 billion in 2026 and is projected to reach USD 101.02 billion by 2034.

In 2025, the market value stood at USD 7.57 billion.

The market is expected to exhibit a CAGR of 20.7% during the forecast period of 2026-2034.

The Hardware segment led the market By Component.

Post-Ukraine Modernization Wave Accelerates AI Adoption in Defense

Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon / RTX Corporation, BAE Systems plc., Thales Group, Leonardo S.p.A., Airbus Defence and Space, Israel Aerospace Industries Ltd, Rafael Advanced Defense Systems Ltd, and among others are the top companies in the Artificial Intelligence in Military market.

North America dominated the market in 2024

- 2021-2034

- 2025

- 2021-2024

- 128

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us