ASU Powered Ground Support Vehicles Market Size, Share, and Industry Analysis by Product Type (Aircraft Handling Vehicles, Passenger Handling Vehicles, Baggage & Cargo Handling Vehicles, Aircraft Servicing Vehicles, and Aircraft Maintenance & MRO Support Vehicles), By Capacity (Light-duty Units, Medium-duty Units, Heavy-duty Units, and Specialized Heavy-duty Units), By Powertrain (Diesel-powered Vehicles, Battery-Electric Vehicles (BEV), Hybrid-electric Vehicles (HEV/PHEV), Hydrogen Fuel Cell Vehicles (FCEV), and Gasoline/LPG/CNG Vehicles), By End-Use, and Regional Forecast, 2026-2034

ASU POWERED GROUND SUPPORT VEHICLES MARKET SIZE AND FUTURE OUTLOOK

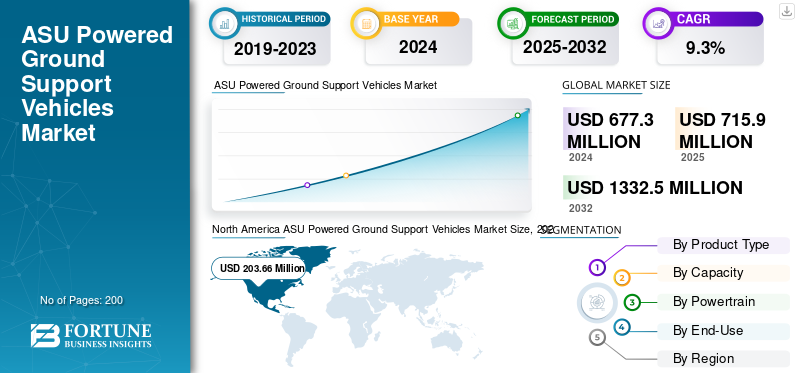

The global ASU powered ground support vehicles market size was valued at USD 716 Million in 2025. The market is projected to grow from USD 765 Million in 2026 to USD 1,507.70 Million by 2034, exhibiting a CAGR of 8.90% during the forecast period. North America dominated the ASU powered ground support vehicles market with a market share of 29.90% in 2025.

The ASU (air start unit) powered ground support vehicles market plays a crucial role in the aerospace industry by providing the compressed air required to start aircraft engines, particularly during maintenance, pre-flight checks, and ground operations. These vehicles are essential across commercial, military, and cargo aviation segments, enabling efficient turnaround times and operational reliability. The market is witnessing strong evolution with the introduction of battery-electric, hybrid, and hydrogen-powered ASUs, aligning with global sustainability and emission-reduction goals. Airports and airlines are progressively modernizing their fleets to meet regulatory pressures and reduce fuel costs, while defense airbases seek high-performance, ruggedized systems for multi-platform aircraft. The market growth is being supported by increasing air traffic, new airport developments, and rising demand for energy-efficient ground support equipment (GSE). Emerging trends such as telematics integration, smart fleet monitoring, and modular power systems are further reshaping the market’s technological landscape.

Key players in the market include Rheinmetall AG (Germany), Guinault S.A. (France), Textron GSE (U.S.), Air+MAK Industries (India), MAK Controls (India), Aviation Ground Equipment Corp. (U.S.), Ingersoll Rand (U.S.), Epsilon Systems Solutions (U.S.), Main New Energy (China), and Greenwood Aerospace (U.S.). These companies focus on developing innovative, energy-efficient ASUs with advanced control systems and modular power options to meet both commercial and defense requirements globally.

Download Free sample to learn more about this report.

ASU POWERED GROUND SUPPORT VEHICLES MARKET TRENDS

Shift toward Electrified and Sustainable Ground Operations to Accentuate Market Growth

The market is undergoing a significant transition driven by the aviation industry’s focus on decarbonization and operational efficiency. Airports and airlines are replacing traditional diesel-powered ASUs with battery-electric, hybrid, and hydrogen-fueled systems to align with global sustainability initiatives such as ICAO’s Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). Additionally, the integration of telematics, IoT, and smart monitoring systems into ASUs is enhancing fleet efficiency, predictive maintenance, and utilization analytics, propelling ASU powered ground support vehicles market growth. Defense airbases are increasingly adopting modular, multi-fuel ASUs to support diverse aircraft platforms and operational needs. The trend also leans toward fleet leasing and shared GSE ownership models, reducing the capital burden on airlines and airport authorities. This evolution is shaping a more connected, energy-efficient, and digitalized ground operation ecosystem across both commercial and defense aviation sectors.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET OPPORTUNITIES

Electrification, Hydrogen Adoption, and Fleet-as-a-Service Models to Accentuate Market Growth

The market presents strong growth opportunities through electrification, hydrogen-based innovation, and service-oriented business models. Airports worldwide are setting net-zero emission targets, creating a long-term market for battery-electric and hydrogen fuel cell ASUs. Manufacturers are focusing on developing modular, interchangeable power systems adaptable across multiple GSE platforms, improving asset utilization and sustainability. Defense modernization programs are also fueling opportunities for high-capacity, ruggedized ASUs designed for multi-aircraft compatibility. Furthermore, the rise of “Fleet-as-a-Service” and leasing models enables smaller operators to access advanced equipment without heavy capital investment. Partnerships among OEMs, airport authorities, and energy infrastructure providers will accelerate adoption. Collectively, these trends position the ASU powered ground support vehicles market for substantial technological and operational transformation over the next decade.

MARKET DRIVERS

Expansion in Global Air Traffic and Modernization of Ground Infrastructure to Boost Market Growth

Rising global air traffic and expanding airport infrastructure are major forces driving the market expansion. Post-pandemic air travel recovery, coupled with large-scale airport expansion projects across Asia Pacific, the Middle East, and Europe, has boosted the demand for reliable and efficient ground support fleets. Moreover, the push for modernization under “green airport” initiatives has encouraged the adoption of low-emission and high-efficiency ASUs. Defense modernization programs are also contributing significantly, as airbases seek high-capacity, ruggedized ASUs for next-generation military aircraft. Technological advancements in powertrains, including high-energy battery systems and modular powerpacks, are improving start-up reliability and reducing operational costs. Together, these drivers are reinforcing investment in next-gen ASUs that align with both environmental regulations and operational demands of growing air fleets.

MARKET RESTRAINTS

High Electrification Costs and Limited Charging Infrastructure to Hamper Market Growth

Despite the momentum toward electrification, high upfront costs and infrastructure gaps are key restraints for the ASU powered ground support vehicles market. Battery-electric and hydrogen-based ASUs require substantial investments in charging or refueling infrastructure, which many airports especially in developing regions are unable to justify economically. The transition from diesel fleets to zero-emission alternatives also poses compatibility and maintenance challenges, particularly where existing support systems are outdated. Moreover, fluctuations in aviation fuel prices and supply chain volatility for advanced batteries and semiconductors have increased procurement costs. Operational downtime during fleet conversion and limited technician training further slow adoption. These cost and infrastructure limitations are particularly evident at small and medium airports, where cost-per-operation remains the dominant purchasing criterion over sustainability.

MARKET CHALLENGES

Integration, Standardization, and Reliability Concerns to Create Major Challenges in the Market

The industry faces ongoing challenges related to the integration of new ASU technologies into existing airport systems and global standardization. Different airport authorities and defense agencies follow varied operational standards, making interoperability and certification complex. The integration of advanced electronic control systems and power management units into conventional ground vehicles often introduces reliability risks under harsh airfield conditions. Furthermore, temperature extremes, frequent duty cycles, and high power demand during aircraft start-up can strain batteries and hybrid systems, affecting performance. For defense applications, requirements for mobility, stealth, and resilience make design standardization even harder. The lack of skilled personnel for maintaining electric and hybrid ASUs further compounds reliability and lifecycle management challenges, slowing fleet transformation efforts globally.

SEGMENTATION ANALYSIS

By End-Use

High Aircraft Operations and Fleet Modernization to Drive Airlines Segment Expansion

By end-use, the market is segmented into airlines, airport authorities, ground handling companies, aircraft OEMs/MROs, defense forces/airbases, and leasing & fleet management firms.

The airlines segment captured the largest share of the market in 2025. In 2026, the segment leads with 30.94% share. The segment holds the dominant share, driven by continuous aircraft operations, high turnaround frequency, and fleet modernization. Growing air passenger traffic and sustainability goals are boosting the adoption of efficient, low-emission ASU-powered vehicles for ground handling and maintenance activities.

The leasing & fleet management firms segment is expected to grow at a CAGR of 11.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Powertrain

Reliability and Power Output to Fuel Diesel-powered Vehicles Demand

Based on powertrain, the market is classified into diesel-powered vehicles, battery-electric vehicles (BEV), hybrid-electric vehicles (HEV/PHEV), hydrogen fuel cell vehicles (FCEV), and gasoline/LPG/CNG vehicles.

The diesel-powered vehicles segment captured the largest share of the market in 2025. In 2026, the segment dominates with 46.14% share. The dominance is due to their proven reliability and high power output. However, while still widely used, demand growth is stabilizing as airports increasingly transition toward hybrid and electric alternatives to meet tightening emission regulations.

The battery-electric vehicles (BEV) segment is expected to grow at a CAGR of 10.1% over the forecast period.

By Capacity

Versatility and Cost-effectiveness to Boost Medium-duty Units Demand

By capacity, the market is classified into light-duty units (<5 tons/<50 kVA), medium-duty units (5–25 tons/50–150 kVA), heavy-duty units (>25 tons/>150 kVA), and specialized heavy-duty units (>50 tons/military).

The medium-duty units (5–25 tons/50–150 kVA) segment led the global ASU powered ground support vehicles market share in 2025. In 2026, the segment dominates with 38.15% share. Medium-duty ASUs are in strong demand owing to their versatility and compatibility with narrow- and wide-body aircraft. These units strike an optimal balance between performance, efficiency, and cost, making them the preferred choice for commercial airports and MRO operations worldwide.

The light-duty units (<5 tons/<50 kVA) segment is expected to grow at a CAGR of 9.1% over the forecast period.

By Product

Rising Air Cargo and Logistics Needs to Push Baggage & Cargo Vehicles Demand

By product, the market is classified into aircraft handling vehicles, passenger handling vehicles, baggage & cargo handling vehicles, aircraft servicing vehicles, and aircraft maintenance & MRO support vehicles.

The baggage & cargo handling vehicles segment captured the largest share of the market in 2024. In 2025, the segment leads with 27.85% share. Baggage and cargo handling vehicles see steady demand growth, supported by rising e-commerce logistics and global air freight traffic. Airports are investing in automated and electric solutions to enhance efficiency, reduce emissions, and improve cargo turnaround speed on the tarmac.

The aircraft servicing vehicles segment is expected to grow at a CAGR of 9.9% over the forecast period.

ASU POWERED GROUND SUPPORT VEHICLES MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and rest of the world.

North America ASU Powered Ground Support Vehicles Market Size, 2025 ( USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America region captured 29.90% of the global market in 2025, generating USD 213.76 million in revenue, and is projected to reach USD 226.8 million in 2026. The region is experiencing strong demand driven by large commercial fleets, major MRO hubs, and defense modernization programs. U.S. airports are actively replacing diesel-powered ASUs with battery-electric units, supported by sustainability initiatives and infrastructure upgrades. The U.S. market is projected to reach USD 141.17 million in 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 152.3 million in 2025 and accounting for a 21.30% share. The market is expected to reach USD 159.1 million in 2026. Demand for vehicles is driven by stringent environmental regulations, green airport initiatives, and a strong OEM presence. Countries such as Germany, France, and the U.K. are rapidly adopting hybrid and electric ASUs. The U.K. market is projected to reach USD 30.19 million in 2026, while the Germany market is projected to reach USD 24.47 million in 2026.

Asia Pacific

In 2025, Asia Pacific generated USD 196.4 million, contributing 27.40% of global market revenue, and is projected to grow to USD 215.4 million in 2026. The region's growth is fueled by rising air traffic, expanding airport infrastructure, and rapid fleet modernization across China, India, and Southeast Asia. Government-led airport expansion programs and increased defense spending are supporting market growth. The China market is projected to reach USD 71.42 million in 2026, while the Japan and India markets are projected to reach USD 36.26 million and USD 26.85 million, respectively, in 2026.

Rest of the World

The Rest of the World contributed 21.40% of the global market in 2025, with a valuation of USD 153.4 million, and is projected to reach USD 163.7 million in 2026. Demand across the Middle East, Africa, and Latin America is driven by airport expansion projects, tourism growth, and investments in military aviation. Major aviation hubs are increasingly focusing on advanced and energy-efficient ASUs to support commercial and cargo operations.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players to Adopt Fleet Electrification Programs and Partnerships to Expand Global Reach

The ASU powered ground support vehicles market is led by established aerospace and ground support equipment manufacturers focusing on innovation and sustainability. Major players include Rheinmetall AG (Germany), Guinault S.A. (France), Textron GSE (U.S.), Air+MAK Industries (India), MAK Controls (India), Ingersoll Rand (U.S.), Epsilon Systems Solutions (U.S.), Aviation Ground Equipment Corp. (U.S.), Main New Energy (China), and Greenwood Aerospace (U.S.). These companies are advancing hybrid, electric, and modular ASU systems, expanding global reach through collaborations, fleet electrification programs, and customized solutions for both commercial and defense aviation sectors.

LIST OF KEY ASU POWERED GROUND SUPPORT VEHICLE COMPANIES PROFILED:

- Rheinmetall AG (Germany)

- Air+MAK Industries (India)

- Guinault S.A. (France)

- Textron GSE (U.S.)

- Epsilon Systems Solutions (U.S.)

- Ingersoll Rand (U.S.)

- MAK Controls (India)

- Aviation Ground Equipment Corp. (U.S.)

- Main New Energy (China)

- Greenwood Aerospace (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- January 2025: Swissport International would deliver comprehensive ground handling services for Lufthansa Group airlines and their passengers at London Heathrow Airport. This five-year agreement emphasizes Swissport's worldwide expertise and proficiency in managing large base operations.

- November 2024: Blackhawk, recognized as a leader in IoT and real-time digital transformation for remote and mobile assets, in collaboration with AB Equipment, one of the largest and most established equipment suppliers and service centers in New Zealand, secured a 10-year contract to deliver maintenance services and connected IoT solutions for the ground support equipment (GSE) fleet of Air New Zealand.

- May 2024: dnata, a prominent global provider of air and travel services, entered into substantial agreements with top manufacturers, securing five-year global framework contracts for new Ground Support Equipment (GSE) during the Dubai Airport Show. The total estimated value of these contracts exceeds USD 210 million throughout their duration.

- December 2022: Babcock secured a multi-million dollar contract lasting 10 years for the worldwide support of air transit and aircraft operational equipment, awarded by the Aeronautical Maintenance Department of the French Ministry of Armed Forces. This marks Babcock's inaugural major contract in the Land Sector within France, which will benefit from the transfer of capabilities from U.K. operations. France is a key focus for Babcock and this new agreement enhances its support for the French Armed Forces.

- November 2021: Menzies Aviation struck a six-year global framework agreement with Rushlift GSE to supply ground support equipment to the cargo handling company. The specialized airport ground support equipment division of Doosan Industrial Vehicles UK would initially lease 650 new vehicles to the ground handling operations of Menzies Aviation at Gatwick and London Heathrow airports.

REPORT COVERAGE

The research report provides an in-depth analysis by identifying the key companies, product categories, and main applications within the industry. Additionally, the report highlights market trends and notable developments in this field. In conjunction with the aforementioned aspects, the report includes several factors that have contributed to the rapid market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.90% from 2026-2034 |

| Unit | Value (USD Million) |

|

Segmentation |

By Product Type

|

|

By Capacity

|

|

|

By Powertrain

|

|

|

By End-Use

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 716 Million in 2025 and is estimated to reach USD 1,507.70 Million by 2034.

The market is growing at a CAGR of 8.90% during the projection period (2026-2034).

By end-use, the airlines segment is the leading segment in the market during the forecast period.

The diesel-powered vehicles segment is the leading segment in this market during the forecast period.

Rheinmetall AG (Germany), Air+MAK Industries (India), Guinault S.A. (France), Textron GSE (U.S.), Epsilon Systems Solutions (U.S.), and Ingersoll Rand (U.S.) are some of the leading OEMs in the market.

North America accounts for the largest share in the global market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us