Authorized Generics Market Size, Share & Industry Analysis, By Therapy Area (Cardiovascular, CNS, Anti-Infectives, Oncology & Supportive Care, Endocrine & Metabolic, Respiratory, and Others), By Route of Administration (Oral, Parenteral, Topical, Inhalation, and Others), By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, and Others) and Regional Forecast, 2026-2034

Authorized Generics Market Size and Future Outlook

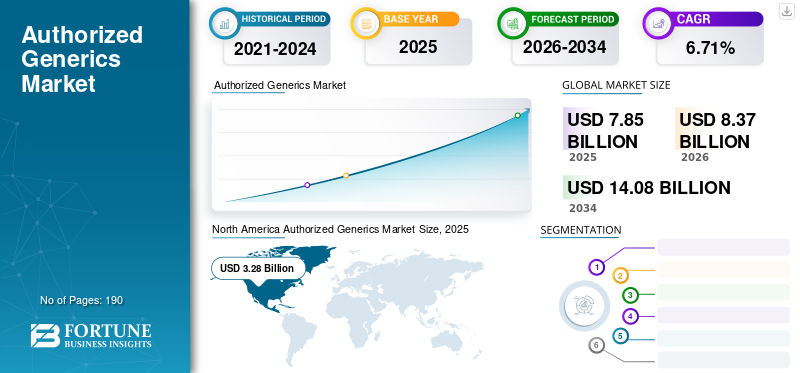

The authorized generics market size was valued at USD 7.85 billion in 2025. The market is projected to grow from USD 8.37 billion in 2026 to USD 14.08 billion by 2034, exhibiting a CAGR of 6.71% during the forecast period. North America dominated the authorized generics market with a market share of 41.78% in 2025.

The market is poised for steady growth as pharmaceutical companies increasingly adopt authorized generics as a pharmaceutical lifecycle management strategy after branded drugs lose exclusivity. This strategy aids companies protect part of their prescription volume while offering healthcare cost reduction. This results in improved patient access and offers more affordable treatment options. Additionally, rising price pressure in mature drug sectors is encouraging numerous originator companies and generic partners to expand these launches across high-value therapies. As a result, the market is developing as a commercially significant bridge between branded generics.

- For instance, in March 2026, Hikma Pharmaceuticals PLC, along with its wholly owned subsidiary Hikma Pharmaceuticals USA Inc., launched an authorized generic version of Nucynta ER (tapentadol) extended-release for their U.S. patients.

Furthermore, leading healthcare industry players, such as Prasco, LLC, Teva Pharmaceutical Industries Ltd., Sandoz AG, and Pfizer Inc, are expanding their offerings in the market.

Download Free sample to learn more about this report.

Authorized Generics Market Takeaways

- 2025 Market Size: USD 7.85 billion

- 2026 Market Size: USD 8.37 billion

- 2034 Forecast Market Size: USD 14.08 billion

- CAGR: 6.71% from 2026–2034

- North America dominated the authorized generics market with a 41.78% share in 2025.

- The cardiovascular segment held the largest market share in 2025.

- The oral segment dominated the market in 2025.

North America

North America maintained its leadership, reaching USD 3.28 billion in 2025, supported by strong demand for authorized generics across chronic disease therapies.

Europe

Europe is projected to grow at a 5.83% CAGR, reaching USD 1.98 billion by 2026, driven by increasing generic drug adoption.

Asia Pacific

Asia Pacific is expected to reach USD 1.60 billion in 2026, making it the third-largest regional market.

U.S.

The market is estimated at USD 3.24 billion in 2026, accounting for approximately 38.70% of the global market.

Japan

The market is estimated at USD 0.23 billion in 2026, representing approximately 2.77% of the global market.

Read More

AUTHORIZED GENERICS MARKET TRENDS

Rising Use of Authorized Generics as a Lifecycle Management Strategy is a Prominent Market Trend

A prominent global trend in the market is rising use of authorized generics as a lifecycle management strategy. As branded drug manufacturers seek different ways to protect revenue after loss of exclusivity, the alternative of authorized generics is on the rise. Companies introduce an authorized generic version of their own branded product. This can help to retain part of the market that would otherwise shift fully to independent generic competitors. Such development strategies help them defend prescription volumes, maintain relationships with payers and pharmacy channels, and respond more effectively to price-sensitive demand, making them an important commercial tool while improving affordability in mature drug categories. Emphasizing these advantages, many companies are focusing on numerous authorized generic launches followed by the loss of drug exclusivity period.

- For instance, in October 2025, Lupin Limited launched an authorized generic version of Ravicti (Glycerol Phenylbutyrate) Oral Liquid, 1.1g/mL, in the U.S. Glycerol Phenylbutyrate Oral Liquid, 1.1g/mL is indicated for chronic management of patients with Urea Cycle Disorders (UCDs) who cannot be managed by dietary protein restriction and/or amino acid supplementation alone.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Lower-Cost Prescription Medicines is Driving Market Growth

The growing demand for lower-cost prescription medicines is driving the authorized generics market growth. The healthcare systems are under continued pressure to reduce treatment spending, fueling demand. When branded drugs lose exclusivity, authorized generics allow companies to introduce the same approved medicine at a lower price, improving affordability. This creates a strong value proposition in mature therapy areas where cost sensitivity is high and long term treatment demand remains steady. As a result, rising preference for more affordable branded-equivalent medicines is supporting wider adoption of authorized generics across the market. Moreover, key companies are focusing on regulatory approvals and new product launches to strengthen their market position.

- For instance, in June 2024, Teva Pharmaceuticals, Inc., launched an authorized generic of Victoza1 (liraglutide injection 1.8mg) in the U.S. The development strengthened the company’s complex generics portfolio.

MARKET RESTRAINTS

Rapid Price Erosion in Off-Patent Drug Categories Limits Market Growth

A key restraint in the market is limited commercial attractiveness in price-eroded categories. When multiple lower-cost versions of a molecule enter the market, prices can decline rapidly, which reduces profitability for both the brand-linked authorized generic and other generic participants. As margins narrow, manufacturers may become more selective about which products they launch or continue to support, especially in mature categories with intense price competition. This can weaken supply incentives, reduce portfolio expansion, and ultimately restrain the overall growth pace of the market.

- For instance, in July 2024, Fierce Pharma reported that pharmaceutical tariffs disproportionately impacted generic drug makers, as the industry has very little pricing flexibility and limited supply-chain resilience. The article noted that generics operate on thin margins, so added cost pressure can weaken market sustainability and disrupt supply.

MARKET OPPORTUNITIES

Loss of Exclusivity of Branded Drugs Creates New Growth Opportunities for Market

The market is witnessing new growth opportunities as a rising number of branded drugs are reaching the end of their patent or exclusivity period. When this happens, originator companies look for ways to retain a share of their prescription volume and commercial presence rather than losing the market entirely to independent generic competitors. Authorized generics help them do this by allowing the same approved product to be sold at a lower price under a non-branded label, which improves affordability while extending the product’s commercial life. As a result, the upcoming loss of exclusivity across significant therapy areas is opening fresh opportunities for companies to expand authorized generic portfolios and strengthen post-exclusivity revenue strategies.

- For instance, in May 2022, GSK plc launched an authorized generic of Flovent HFA (fluticasone propionate), an inhaled asthma treatment. The AG is a product that is the same as the brand. It was made available to patients through another company (Prasco) as the branded product reached the end of its patent life. Such developments drive market growth.

MARKET CHALLENGES

Steep Post-Exclusivity Price Competition Challenging Long-Term Profitability of Market

A major market challenge is steep post-exclusivity price competition. An authorized generic competes not only with the original branded product but also with independent generic manufacturers and aggressive channel pricing. This reduces revenue per prescription, narrows profitability, and makes it harder for companies to keep expanding their authorized generic portfolios across all eligible molecules. As a result, manufacturers tend to remain selective, which limits the overall pace of market growth.

- For instance, in June 2025, A Health Affairs Forefront article titled ‘Financial Securitization As An Approach To Mitigating Generic Drug Shortages ’explained that pushing drug prices close to breakeven can push suppliers out of the market, leading to consolidation and loss of supply-chain robustness. Such factors reinforce how intense price pressure can weaken the long-term viability of low-margin off-patent markets.

Segmentation Analysis

By Therapy Area

High Disease Prevalence and Long-Term Care Burden Leads to Cardiovascular Segment Growth

Based on the therapy area, the market is categorized into cardiovascular, CNS, anti-infectives, oncology & supportive care, endocrine & metabolic, respiratory, and others.

Among these, the cardiovascular segment held highest authorized generics market share. They accounted for a large long-term treatment burden and require continuous medication use across broad patient populations. This leads to high prescription volumes for established molecules, which makes this therapy area suitable for authorized generic strategies after brand exclusivity ends. As a result, the combination of high disease prevalence, recurring refill demand, and strong affordability pressure helps cardiovascular therapies account for a leading share in the market.

- For instance, in May 2023, Prasco announced that the Authorized Generic of Farxiga (dapagliflozin) Tablets and Xigduo XR (dapagliflozin/metformin extended-release) Tablets were available from Prasco. Dapagliflozin has significant cardiovascular-metabolic relevance, especially in heart failure and related chronic cardiometabolic care. Such developments are expected to drive segmental growth.

The oncology & supportive care segment is expected to grow at a CAGR of 8.39% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Route of Administration

Ease of Consumption and Effectiveness for Long-Term Outpatient Therapy to Boost Oral Segmental Growth

Based on the route of administration, the market is segmented into oral, parenteral, topical, inhalation, and others.

In 2025, the oral segment dominated the market as oral medicines are easier for patients to take, more practical for long-term outpatient therapy, and generally better suited to high-volume generic distribution than more complex injectable or inhaled products. This improves adherence, simplifies dispensing, and supports wider substitution in routine chronic treatment settings. As many established branded medicines face loss of exclusivity in tablet, capsule, or oral liquid formulations, companies also find oral formats commercially attractive for authorized generic launches. As a result, the oral route benefits from stronger patient acceptance, greater familiarity among prescribers, and easier channel switching, which help it lead the market.

- For instance, in July 2023, Amneal launched its authorized generic for Xyrem (sodium oxybate) oral solution in the U.S. The development reflects how oral formulations remain a preferred route for authorized generic commercialization as they are well-suited to chronic outpatient use and broad patient access.

The inhalation segment is projected to grow at a CAGR of 8.01% during the forecast period.

By Distribution Channel

Vast Distribution Network of Retail Pharmacies Leads to Segment Dominance

Based on the distribution channel, the market is segmented into retail pharmacies, hospital pharmacies, online pharmacies, and others.

By distribution channel, retail pharmacies accounted for the largest share of the market. The segment dominated as authorized generics are designed to compete in mainstream generic trade channels where patients fill routine outpatient prescriptions. Chronic cardiovascular, CNS, endocrine, and anti-infective medicines are commonly dispensed outside hospital settings, resulting in retail pharmacies handling a large share of authorized generic volume. As a result, retail pharmacies capture the greatest demand as they are closest to everyday prescription fulfillment and have large, recurring patient traffic.

- For instance, in January 2023, Greenstone, a subsidiary of Pfizer Inc., and Roman announced a supply agreement to offer Roman members access to the approved authorized generic version of Viagra (sildenafil citrate). The development provided patients with access to a nationwide digital doctor’s office and online pharmacy for certain men’s health conditions, through an integrated platform that enhances the convenience and high quality of healthcare delivery.

The online pharmacies segment is projected to grow at a CAGR of 8.23% over the study period.

Authorized Generics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Authorized Generics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 3.10 billion and maintained its leading position in 2025 at USD 3.28 billion. The market is growing strongly as the U.S. and Canada have large, mature, branded-drug markets, frequent loss-of-exclusivity events, and a very strong payer focus on cost savings. Also, a favorable environment across the region drives market growth.

U.S. Authorized Generics Market

Given North America's substantial contribution, the U.S. market is estimated at around USD 3.24 billion in 2026, accounting for roughly 38.70% of the global market.

Europe

Europe is projected to grow at 5.83% over the coming years, the second-highest among all regions, and reach a valuation of USD 1.98 billion by 2026. The market is growing as generic medicines are already embedded in healthcare systems, and governments continue to use pricing, tendering, and substitution frameworks to expand the use of affordable medicines.

U.K Authorized Generics Market

The U.K. market is estimated at around USD 0.38 billion in 2026, representing roughly 4.53% of the global market.

Germany Authorized Generics Market

Germany's market is projected to reach approximately USD 0.42 billion in 2026, equivalent to around 4.96% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 1.60 billion in 2026 and secure the position of the third-largest region in the market. The market is growing as governments are actively promoting access to cheaper medicines and broader generic uptake, especially in high-population countries with a rising chronic disease burden.

Japan Authorized Generics Market

The Japanese market in 2026 is estimated at around USD 0.23 billion, accounting for approximately 2.77% of the global market.

China Authorized Generics Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.38 billion, representing approximately 4.59% of global sales.

India Authorized Generics Market

The Indian market in 2026 is estimated at around USD 0.47 billion, accounting for roughly 5.63% of global revenue.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The market in Latin America is estimated to reach a valuation of USD 0.63 billion in 2026. The growth in the region is driven by governments and regional health bodies placing greater emphasis on improving access to essential medicines, strengthening procurement, and supporting cost-efficient drug supply. In the Middle East & Africa, the GCC is set to reach USD 0.25 billion in 2026.

South Africa Authorized Generics Market

The South African market is projected to reach approximately USD 0.11 billion by 2026, accounting for roughly 1.33% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches by Key Players to Propel Market Competition

The global authorized generics market is highly consolidated, with companies such as Prasco, LLC, Teva Pharmaceutical Industries Ltd., Sandoz AG, Pfizer Inc, Lupin Limited, and Hikma Pharmaceuticals PLC holding significant market share. Strategic partnerships, new product launches, and increased investments in the sector drive these companies' market share gains.

- For instance, in December 2025, Amneal Pharmaceuticals, Inc. received approval from the U.S. FDA for albuterol sulfate inhalation aerosol (90 mcg per actuation). The product is the generic equivalent of PROAIR HFA (albuterol sulfate inhalation aerosol), a registered trademark of Teva Respiratory LLC.

Other notable players in the global market include Amneal Pharmaceuticals, Inc., Padagis LLC, and GSK plc. These companies are expected to prioritize strategic collaborations, and new product launches to strengthen their positions during the global forecast period.

LIST OF KEY AUTHORIZED GENERICS COMPANIES PROFILED

- Prasco, LLC (U.S.)

- Teva Pharmaceutical Industries Ltd.(Israel)

- Sandoz AG (Switzerland)

- Pfizer Inc. (U.S.)

- Lupin Limited (India)

- Hikma Pharmaceuticals PLC (U.K.)

- Amneal Pharmaceuticals, Inc. (U.S.)

- Padagis LLC (U.S.)

- GSK plc (U.K.)

- Viatris Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Accord Healthcare, Inc., a leading generic pharmaceutical company committed to improving access to affordable medicines, re‑launched Hydrochlorothiazide Tablets, USP in 12.5 mg, 25 mg, and 50 mg strengths.

- February 2026: Lupin announced the launch of the authorized generic version of Bausch Health’s Apriso (Mesalamine Extended-Release Capsules 0.375 g) in the U.S.

- December 2025: Amneal Pharmaceuticals, Inc.., received approval from the U.S. FDA for albuterol sulfate inhalation aerosol (90 mcg per actuation). The product is the generic equivalent of PROAIR HFA (albuterol sulfate inhalation aerosol), a registered trademark of Teva Respiratory LLC.

- November 2022: Prasco Laboratories launched the Authorized Generic of ZIOPTAN (tafluprost ophthalmic solution) 0.0015%. This solution is the company’s first Authorized Generic launch in partnership with Théa Pharma, Inc.

- March 2021: Sandoz Inc. announced the in-licensing of commercial distribution rights for the brand and authorized generic of the respiratory inhalation medicine Proventil HFA (albuterol sulfate) Inhalation Aerosol from Kindeva Drug Delivery, a global contract development and manufacturing organization that supplies the product.

REPORT COVERAGE

The report provides a detailed assessment of the global authorized generics market, covering evolving trends across major therapy areas, product access channels, and post-exclusivity commercialization strategies. It analyses how pharmaceutical companies are using authorized generics to protect branded product value, expand lower-cost access, and respond to pricing pressure after patent expiry. The study also examines market performance across therapy areas, route of administration, and distribution channel to show where demand is strongest and how companies are positioning their portfolios. In addition, it reviews the competitive landscape, highlighting the role of originator companies, licensing partners, and generic-focused distributors operating in this market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.71% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Therapy Area, Route of Administration, Distribution Channel, and Region |

| By Therapy Area |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 7.85 billion in 2025 and is projected to reach USD 14.08 billion by 2034.

In 2025, the North America market value stood at USD 3.28 billion.

The market is expected to grow at a CAGR of 6.71% over the forecast period of 2026-2034.

The cardiovascular therapy area segment is expected to lead the market.

The market is driven by growing demand for lower-cost prescription medicines.

Prasco, LLC, Teva Pharmaceutical Industries Ltd., Sandoz AG, Inc., Pfizer Inc., and Lupin Limited are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us