Prescription Drugs Market Size, Share & Industry Analysis, By Product Type (Generics, Orphan, and Other Prescription Drugs), By Therapy (Oncology, Central Nervous System, Vaccines, Immunosuppressants, and Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies & Drug Stores, and Online Pharmacies), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

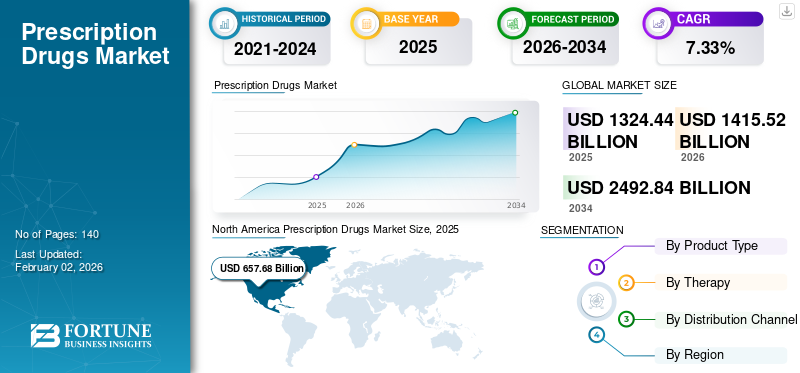

The global prescription drugs market size was valued at USD 1,324.44 billion in 2025. The market is projected to grow from USD 1,415.52 billion in 2026 to USD 2,492.84 billion by 2034, exhibiting a CAGR of 7.33% during the forecast period. North America dominated the prescription drugs market with a market share of 49.66% in 2025. Moreover, the U.S. prescription drugs market size is projected to grow significantly, reaching an estimated value of USD 931.1 million by 2032, driven by rising approval of orphan drugs by regulatory agencies.

Prescription drugs comprise various types of vaccines and therapies for the treatment and management of chronic and acute diseases. These disorders include types of cancer, cardiovascular diseases, diabetes, and also orphan disease. In a modern clinical scenario, the administration of appropriate prescription drugs is critical for better clinical outcomes for almost every patient suffering from serious disorders. Many market players are engaged in clinical trials for the development of new products for a wide range of diseases, but the prescription drugs scenario itself has undergone profound changes with an increasing influx of generic equivalents.

The impact of the COVID-19 pandemic resulted in a decline in market growth in 2020. Several regions across the globe faced challenges in accessing medical care and treatment due to the escalation of country restrictions or lockdowns. These factors also limited the number of patient visits to hospitals, and the dispersion of prescriptions by healthcare professionals, further moderately limiting the demand and adoption of prescription drugs. Also, the disruption caused by the COVID-19 pandemic to international supply chains led to high-profile shortages of critical medications and decline in drug expenditures across the globe.

- As per the American Society of Health-System Pharmacists statistics in 2022, prescription drug expenditures in nonfederal hospitals declined by 4.6% in 2020.

However, the resurgence of routine healthcare services after the initial COVID-19 shutdown and patient visits to healthcare centers increased globally. Moreover, rising R&D initiatives for the development and launch of COVID-19 treatment drugs by major players surged the demand for vaccines and orphan drugs among the population. Moreover, the high emphasis on shifts to homecare settings by patients, along with uptake in the use of biosimilar, a large pipeline of new increased approvals of specialty medications by regulatory authorities, further propelled the drug's adoption.

Thus, the rebound in the number of hospital visits by patients’ post-pandemic, coupled with the high consumption of prescription drugs in homecare settings, boosted the global prescription drugs market growth.

Download Free sample to learn more about this report.

Global Prescription Drugs Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 1,324.44 billion

- 2026 Market Size: USD 1,415.52 billion

- 2034 Forecast Market Size: USD 2,492.84 billion

- CAGR: 7.33% from 2026–2034

Market Share:

- North America dominated the prescription drugs market with a 49.66% share in 2025, driven by the increasing demand for advanced therapies, robust healthcare expenditure, and the presence of major pharmaceutical companies focusing on generic drug launches and specialty medicines.

- By product type, the other prescription drugs segment is expected to retain its largest market share owing to the rising number of critical drugs prescribed by healthcare professionals, including oncology and anti-diabetic medications, which lack immediate generic equivalents.

Key Country Highlights:

- United States: Surge in orphan drug approvals and increasing focus on specialty medications to address unmet clinical needs.

- Europe: Strong demand for affordable prescription medicines supported by new product launches and expansion of generic drug offerings.

- China: Growing healthcare infrastructure investments and rising awareness of chronic diseases are accelerating prescription drug adoption.

- Japan: High prevalence of aging-related disorders is fostering demand for advanced prescription therapies and biosimilars.

Prescription Drugs Market Trends

Increasing Presence of Pipeline Candidates in Various Therapy Areas

In this market, the increasing R&D investments by prominent companies for the development of new drugs are one of the main key trends.

- As per the European Federation of Pharmaceutical Industries and Associations (EFPIA) estimates, in 2022, the research-based pharmaceutical industry in 2021 invested an estimated USD 43,684.2 million in R&D in Europe.

This is primarily attributed to the fact that in the global scenario, there has been an increasing prevalence of several chronic disorders. This has led to increasing demand from patients due to their unmet clinical needs and demand for positive clinical outcomes. A number of these chronic disorders are often refractory in nature and require the administration of aggressive prescribed therapies.

This has led major pharmaceutical companies to be constantly engaged in clinical trials for the development and, ultimately, the approvals of new products. An increasing number of key manufacturers are shifting their focus toward developing drugs to treat rare diseases. This is projected to propel the market growth during the forecast period.

Download Free sample to learn more about this report.

Prescription Drugs Market Growth Factors

Increasing Launch of Generic Equivalents of Key Prescription Drugs to Fuel Product Demand

One of the critical elements driving the global market growth is the increasing launches of the generic equivalents of several key drugs in strong markets such as the U.S. The increasing adoption of these generic equivalents is especially due to the fact that these generics are often as efficient as their original counterparts and can often be adopted by patients at a fraction of the costs. Patients without access to expensive prescription products due to financial hurdles can often adopt these drugs and experience better clinical outcomes. In October 2019, the U.S. FDA announced that they had given 1,171 generic drug approvals, of which 935 were full approvals and 236 were tentative approvals. The U.S. FDA particularly approved these generic equivalents to improve drug competition and to also encourage the increasing adoption of these low-cost drug equivalents. This is especially critical for patients in emerging markets and also patients in developed countries who do not have access to appropriate payment plans for prescription medicines.

In addition, the governments of different nations are introducing different schemes to provide generic drugs at a lower cost than their branded equivalents.

- For instance, as per data published in September 2023, the Indian government has introduced the Aushadhi Scheme, which provides generic medications at prices that are 50-90% lower than their branded equivalents. Therefore, generic drugs are increasingly popular among Indian patients, supported by government initiatives.

These factors are anticipated to drive the global market growth during the forecast period.

Increasing Developments of Orphan Drugs Drive Market Growth

One of the key market driving factors prevailing in the market is the increasing R&D investments by prominent companies for the development of drugs for orphan diseases. A prime example of such a strategic move by a market player includes BioMarin, a key pharmaceutical company involved in the development of rare diseases therapies. BioMarin’s product portfolio includes several orphan drugs, such as the mucopolysaccharidoses (MPS) group of disorders, and the company also has strong orphan drug pipeline candidates in various stages of clinical trials.

Additionally, some of the key industry players are focusing on the development of orphan drugs for the treatment of several rare disorders.

- For instance, in September 2023, Baudax Bio, Inc. announced that its primary clinical candidate, TI-168, received orphan drug designation by the U.S. FDA for the treatment of Hemophilia A with inhibitors. After receiving this approval, the company can initiate the Phase 1/2a clinical trial of TI-168 for the treatment of haemophilia A. In addition, the company can progress this therapy into additional research by early 2024.

This increasing initiatives into rare diseases therapies are attributable to the fact that the development of blockbuster drugs is possible in orphan diseases as compared to the already mature markets of other traditional diseases such as cardiovascular and diabetes. The above factors, combined with the need for efficient therapeutics for severely debilitating rare diseases, are further projected to fuel the demand for these types of prescription products and boost the global market growth.

RESTRAINING FACTORS

High Costs Associated with Certain Prescription Drugs to Limit Market Growth

Despite the increasing incidence of critical diseases, such as cancers and cardiovascular diseases, globally and the higher prevalence of these conditions in developing regions, such as Africa, Latin America, and Asia, there are certain factors that are restraining the adoption of products. One of the major factors restraining the growth of the market is the high costs associated with numerous prescription drugs.

- According to an article published by Policy & Medicine in 2019, a recent study by the Tufts Center for the Study of Drugs stated that developing a new prescription medicine that gains marketing approval is estimated to cost drug makers around USD 2.6 billion.

This has led to a small number of patients adopting these drugs, and a significant proportion of these patients face financial hurdles during the usage of these products. In many instances, these prescription drug costs can lie in the range of USD 100,000-500,000, and the conditions are not even curative. For instance, Abiraterone used in the treatment of prostate cancer can cost the patient USD 10,000 per month at its lowest and not even cure the disease. Thus, such restraining factors are anticipated to limit the market growth during the forecast period.

Prescription Drugs Market Segmentation Analysis

By Product Type Analysis

Rising Number of Drugs Prescribed in Healthcare Settings to Boost the Other Prescription Drugs Segment

Based on product type, the market is segmented into generics, orphan, and other prescription drugs. A number of new drugs launched every year fall under several categories, such as biologics, and often do not have generic equivalents of them launched in the near future. Hence, the other prescription drugs segment dominated the market share in 2023. Moreover, the rising number of drugs prescribed by healthcare professionals for the treatment of chronic conditions, such as cancer, diabetes, and others, across the globe further augments the segment share.contributing 71.71% globally in 2026

- As per the Prescription drug statistics 2023, more than 4.0 billion prescriptions are dispensed in the U.S. every year. As per a similar source, the therapeutic areas with the highest prescription drug spending in the U.S. were antidiabetics, oncology drugs, autoimmune, and respiratory diseases.

The other segment contains critical and life-saving drugs such as oncology, anti-diabetic and cardiovascular drugs and has been instrumental in the dominance of this segment in the global market.

To know how our report can help streamline your business, Speak to Analyst

The orphan segment is anticipated to grow at a comparatively higher CAGR over the forecast period. The increasing clinical trials for the development of orphan drugs and rising approval by regulatory agencies are anticipated to increase the uptake of these drugs during the forecast period and drive the market growth.

- According to the Food and Drug Administration estimates, in March 2021, in 2020, the agency approved 32 novel drugs and biologics with orphan drug designation. As per a similar source, in the Center for Drug Evaluation and Research (CDER), 31 of the 53 novel drug approvals, or 58%, were orphan-designated products.

By Therapy Analysis

Global Rising Prevalence of Cancer to Aid Dominance of the Oncology Segment

In terms of therapy, the market is segmented into oncology, central nervous system, vaccines, immunosuppressants, and others. The oncology segment is anticipated to dominate the therapy segment due to the increasing prevalence of cancer and the high costs attributed to the treatment of the various forms of cancer. Further, the rising number of regulatory approvals for targeted therapies in the treatment of cancer is another factor contributing to the segmental growth. contributing 67.55% globally in 2026

- For instance, in September 2023, the U.S. FDA approved ten new anticancer therapeutics providing targeted therapies. Some of the approved drugs include quizartinib (Vanflyta), pralsetinib (Gavreto), bosutinib (Bosulif), and others.

- According to an article published by the American Cancer Society in 2022, an estimated 1.9 million new cancer cases were diagnosed, and around 609,360 deaths were reported due to cancer in the U.S.

The increasing population is also expected to aid the growth of the vaccines segment due to the increasing need for timely vaccinations, especially in infants and children.

The increasing prevalence of cardiovascular diseases is also anticipated to drive the anticoagulants segment. Increasing organ transplant procedures is also anticipated to drive the growth of the immunosuppressants segments. Moreover, rising demand and sales of immunomodulatory drugs to treat high prevalence of immunological disorders further boost the segment share.

- According to annual report estimates published by AbbVie Inc., in 2022, immunology drugs such as Skyrizi and Rinvoq generated a sales revenue of USD 4,484 million and USD 1,794 million, respectively.

Moreover, the others segment held a dominant share of the market in 2023, owing to the increasing launch and sales of drugs by key players and the rising number of prescriptions of these drugs by healthcare professionals across the globe.

By Distribution Channel Analysis

Rising Prescription Drug Spending in Hospital Pharmacies Led to the Dominance of the Segment

In terms of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies & drug stores, and online pharmacies. Some of the key reasons for the dominance of the hospital pharmacies segment is that the therapeutics indicated under prescription drugs can often be only prescribed in hospital settings under the guidance of trained medical professionals. Also, a number of therapeutics used in the treatment of critical diseases, such as cancers and orphan diseases, can only be administered intravenously by trained medical professionals. Such effective administration of therapeutics often allows for the appropriate treatment and management of critical diseases, leading to improved clinical outcomes.

- According to statistics published by NCBI, in 2021, the overall prescription drug spending in clinics and hospitals was anticipated to increase by 7% to 9% in the U.S.

- As per Centers of Disease Control and Prevention (CDC) estimates, in 2019, the number of drugs given or prescribed in emergency departments or hospital settings was 353.8 million in the U.S.

The growing availability of prescription drugs and the rising need for daily medications, such as anti-diabetics, are some of the major factors responsible for the growth of this segment over the forecast period.

- As per data revealed by the Organization for Economic Cooperation and Development (OECD) in 2020, around four out of every five euros spent on retail pharmaceuticals goes on prescription medicines in Europe.

The online pharmacies segment is anticipated to grow at the highest CAGR over the forecast period, especially due to the ease provided to patients in the refilling of prescription medications and the ability to acquire drugs from the comfort of their homes.

REGIONAL INSIGHTS

North America Prescription Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, the North America market stood at USD 657.68 billion, representing 49.66% of global demand, and is projected to grow to USD 703.04 billion in 2026. Some of the prominent reasons for the dominance of the North America prescription drugs market share included the increasing demand for efficient and advanced products in the region, especially due to the high prevalence of several chronic diseases. These factors, along with high healthcare expenditure, robust R&D for drugs in the region, and the presence of prominent companies in the region involved in the product of generic equivalents of key drugs, are responsible for the dominant share of the region in the global market.The United States market is projected to reach USD 607.6 billion by 2026.

- According to the Food and Drug Administration estimates, in 2022, till date, more than 32,000 generic drugs have been approved by the FDA, owing to the adoption of the FDA’s generic drug program. Moreover, as per similar estimates, approximately 9 out of every 10 prescriptions filled in the U.S. are filled with generic drugs.

Europe

The Europe region captured 20.48% of the global market in 2025, generating USD 271.21 billion in revenue, and is projected to reach USD 288.77 billion in 2026. The market in Europe accounted for the second largest share in the global market, and reasons for the region’s strong market share include increased demand for advanced prescription products and the product launches of efficient prescription products, including orphan drugs. Furthermore, several market players are introducing generic drugs to provide affordable treatment across the region.The United Kingdom market is projected to reach USD 36.41 billion by 2026, and the Germany market is projected to reach USD 53.34 billion by 2026.

- For instance, in February 2022, Novartis AG launched Lenalidomide, a generic oncology medicine, in 19 countries in Europe.

- According to the EFPIA estimates, in 2022, 16.8% of sales of new drugs launched during the period 2016-2021 were in the Europe market.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 300.57 billion in 2025, accounting for 22.69% share, and is expected to reach USD 323.5 billion in 2026. Asia Pacific is projected to register a reasonably higher CAGR during the forecast period. New launches of key products in the region and strong demand for these drugs are anticipated to drive the market during 2026-2034. The presence of a large potential patient population and the growing awareness of chronic and serious disorders amongst individuals leading to increased healthcare expenditure are projected to drive the market growth in Asia Pacific during the forecast period.The Japan market is projected to reach USD 101.54 billion by 2026, the China market is projected to reach USD 136.49 billion by 2026, and the India market is projected to reach USD 24.68 billion by 2026.

- As per the Economic Survey in 2021-2022, the Central and State Governments’ budgeted expenditure on the health sector reached 2.1% of its GDP in 2021-2022, against 1.3% in 2019-2020 in India.

Latin America and the Middle East & Africa

In 2025, Latin America represented USD 61.64 billion, accounting for 4.65% of the worldwide market, and is projected to grow to USD 65.11 billion in 2026. The Middle East & Africa market accounted for USD 33.33 billion in 2025, representing 2.52% of the global industry, and is expected to reach USD 35.1 billion in 2026. The rest of the world market comprises Latin America and the Middle East & Africa and is currently in a stage of growth. Increasing use of advanced prescription products and increasing healthcare expenditure are projected to fuel the market growth during the forecast period.

List of Key Companies in Prescription Drugs Market

Strong and Diversified Product Portfolio of Novartis and Pfizer to Help these Companies Retain a Leading Position

The overall competitive landscape of this market depicts a competition structure where there is a presence of a large number of prominent market players. Two major companies, Novartis and Pfizer, with their strong and diverse product portfolio and presence in key therapeutic areas, such as oncology and vaccines, are prominent reasons responsible for their dominance.

Despite that, a number of other prominent players, such as Roche, Johnson & Johnson, and Sanofi, also have strong market revenue shares in the global market. A number of companies producing generic equivalents of many drugs, such as Dr Reddy’s Laboratories Ltd., and Lupin Pharmaceuticals, Inc., are also expected to launch a number of products in the forecast period. This is projected to positively impact the global market as these companies are expected to gain market share during the forecast period.

LIST OF KEY COMPANIES PROFILED:

- Novartis AG (Switzerland)

- Pfizer, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Sanofi (France)

- Johnson & Johnson Services, Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- AbbVie, Inc. (U.S.)

- GlaxoSmithKline plc. (U.K.)

- AstraZeneca (U.K.)

- CELGENE CORPORATION (BRISTOL-MYERS SQUIBB COMPANY) (U.S)

KEY INDUSTRY DEVELOPMENTS:

- October 2023 - Novartis AG announced the spin-off of Sandoz, its Generics and Biosimilars business, to transform it into an innovative medicine company.

- January 2023 - Amgen Inc. announced launch of AMJEVITA (adalimumab-atto), a biosimilar to Humira (adalimumab), in the U.S.

- March 2022 - UCB S.A., a global biopharmaceutical company, announced the approval of FINTEPLA (fenfluramine) oral solution CIV in the U.S. by the U.S. Food and Drug Administration (FDA) for the treatment of seizures associated with Lennox-Gastaut syndrome in patients two years of age and older.

- April 2020 – Lupin Pharmaceuticals, Inc. announced the launch of the generic drug, Mycophenolic acid delayed-release tablets used for the prevention of organ rejection in kidney transplant patients in the U.S.

- March 2020 – Dr Reddy’s Laboratories Ltd. announced the launch of the generic equivalent of Geodon (Ziprasidone Mesylate) injection, a drug used for schizophrenia patients in the U.S.

- February 2020 – Dr. Reddy’s Laboratories Ltd. announced the launch of the generic equivalent of Vimovo (naproxen and esomeprazole magnesium), a drug used for inflammation in the U.S.

REPORT COVERAGE

The research report provides a thorough analysis of the market. It focuses on key features such as the prevalence of key diseases - by key countries - pipeline analysis, key industry developments, new product approvals, and regulatory scenarios - by key regions. Also, the report offers insights into the market trends and highlights key industry developments. In addition to the above-mentioned factors, the report includes numerous factors that have contributed to the growth of the market in the recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.33% from 2026-2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Product Type

|

|

By Application

|

|

|

By Distribution Channel

|

|

|

By Geography

|

Frequently Asked Questions

The global prescription drugs market size is projected to grow from $1,324.44 billion in 2025 to $2,492.84 billion by 2034, at a CAGR of 7.33%

Growing at a CAGR of 7.33%, the market will exhibit steady growth over the forecast period (2026-2034).

Oncology leads due to high cancer prevalence and treatment costs. Other key areas include CNS disorders, immunosuppressants, vaccines, and autoimmune therapies.

The other prescription drugs segment is expected to be the leading segment in this market during the forecast period.

The anticipated introduction of innovative prescription drugs in the market due to the increased prevalence of chronic and serious diseases, coupled with significant unmet clinical needs, is fueling the product demand.

Novartis AG and Pfizer, Inc. are the leading players in the global market.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us