Branded Generics Market Size, Share & Industry Analysis, By Therapy Area (Anti-infectives, Cardiovascular, Gastrointestinal, Vitamins, Minerals & Nutritional, CNS, Respiratory, Anti-diabetic, Dermatology, Pain Management, and Others), By Route of Administration (Oral, Parenteral, Topical, Inhalation, and Others), By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, and Others) and Regional Forecast, 2026-2034

Branded Generics Market Size and Future Outlook

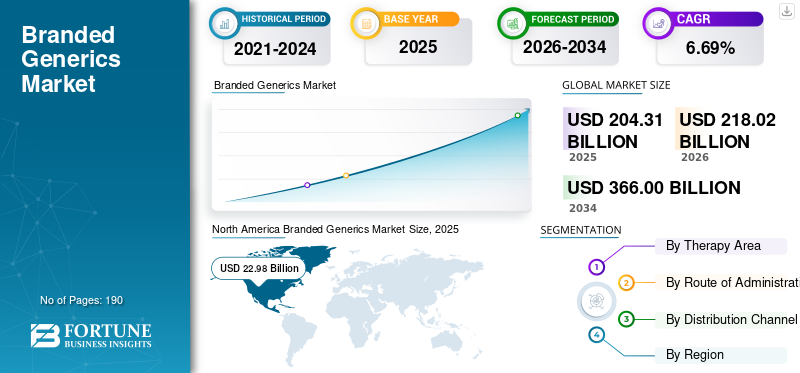

The global branded generics market size was valued at USD 204.31 billion in 2025. The market is projected to grow from USD 218.02 billion in 2026 to USD 366.00 billion by 2034, exhibiting a CAGR of 6.69% during the forecast period.

The global branded generic market is anticipated to grow steadily, driven by pharmaceutical companies introducing lower-cost versions of well-known molecules under their own brand names. Such initiatives help companies improve product recall, strengthen physician trust, and compete more effectively in highly price-sensitive markets. As a result, branded generics strike a balance between affordability and brand recognition, supporting wider patient access while helping manufacturers protect volume in crowded therapeutic categories. Key pharmaceutical companies are actively participating in product launches in the market, fueling growth.

- For instance, in March 2026, Sun Pharmaceutical Industries launched its semaglutide injection in India under the brand names Noveltreat and Sematrinity. The development reflects how companies in the market are using branded versions of widely demanded therapies to improve commercial visibility and expand access in high-growth chronic-care segments.

Furthermore, key players, such as Abbott, Sun Pharmaceutical Industries Limited, Dr. Reddy’s Laboratories Limited, and Cipla Limited, are expanding their branded generics offerings.

Download Free sample to learn more about this report.

BRANDED GENERICS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 204.31 billion

- 2026 Market Size: USD 218.02 billion

- 2034 Forecast Market Size: USD 366.00 billion

- CAGR: 6.69% from 2026–2034

- North America dominated the branded generics market in 2025, valued at USD 22.98 billion.

- The cardiovascular diseases segment accounted for the largest market share in 2025.

- The oral segment accounted for the largest market share in 2025.

North America

North America market valued at USD 22.98 billion in 2025.

Europe

Europe market is projected to reach USD 39.29 billion in 2026.

Asia Pacific

Asia Pacific market is projected to reach USD 98.14 billion in 2026.

U.S.

U.S. Market projected to reach USD 22.47 billion by 2026.

Japan

Japan Market projected to reach USD 8.91 billion by 2026.

Read More

BRANDED GENERICS MARKET TRENDS

Increasing Competition Driving Brand Differentiation in Generics is a Prominent Trend Observed

A global trend in the market that has been observed is a shift toward stronger brand differentiation as competition intensifies across off-patent molecules. As more companies enter the same therapeutic categories with similar generic products, manufacturers are increasingly using brand identity, physician engagement, broader distribution, and therapy-specific positioning to stand out in the market. This creates stronger product recall and helps companies protect prescription volumes in crowded segments. As a result, branded generics are no longer competing only on price but also on perceived reliability, familiarity, and market visibility, thereby strengthening their role in both chronic and specialty therapy areas.

- For instance, in December 2025, Cipla announced the launch of Yurpeak (tirzepatide) in India, the second tirzepatide brand under its agreement with Lilly. These developments show how rising competition is pushing companies to create differentiated branded offerings around the same high-demand molecule to expand reach and improve commercial positioning.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Affordable Branded Medicines Driving Market Growth

The global branded generics market growth is being driven by rising demand for affordable branded medicines. As patients, physicians, and healthcare systems are under increasing pressure to control treatment costs without compromising trust in therapy, demand for affordable medicines is on the rise. As the burden of chronic diseases continues to rise, demand is shifting toward lower-cost versions of established medicines that still carry a recognizable brand identity. These factors improve physician confidence, support better patient acceptance, and help companies scale volumes across large therapy areas. As a result, branded generics are gaining stronger traction. Moreover, key companies are focusing on regulatory approvals and new product launches to strengthen their market position.

- For instance, in March 2026, Dr. Reddy’s launched Obeda, India’s DCGI-approved generic semaglutide injection for type 2 diabetes. The development aimed at expanding access to advanced GLP-1 therapy in high-burden chronic care segments.

MARKET RESTRAINTS

Intense Price Competition from Low-Cost Unbranded Generics Restricts Market Growth

The global market is being restrained by intense price competition from low-cost unbranded generics. As more manufacturers enter the same off-patent molecule categories, pricing becomes increasingly aggressive. This reduces the commercial advantage of branded generics, especially in highly competitive therapy areas; systems focus more on the lowest available cost. As a result, companies face margin pressure, weaker differentiation, and lower incentive to invest in promotion and long-term portfolio expansion. This pricing pressure can ultimately limit sustainable growth for branded generic players, particularly in commoditized markets.

- For instance, in July 2024, Fierce Pharma reported that a pharmaceutical company published an article highlighting that sinking prices for generic medicines have become severe enough in some categories to contribute to broader supply chain and profitability problems. The article, citing a QYOBO white paper, noted that disproportionately low generic drug prices can make it difficult for manufacturers to maintain viable supply economics. This reinforces the same restraint in the market, where intense price competition from cheaper generics can erode margins and limit growth potential.

MARKET OPPORTUNITIES

Patent Expiry of High-Value Molecules Creating New Growth Opportunities for the Markets

The global market is gaining new growth opportunities as several high-value patented drugs approach loss of exclusivity in key markets. When patents expire, pharmaceutical companies can introduce branded versions of proven molecules at lower prices than the originator product. This helps expand patient access while also allowing manufacturers to enter established therapy areas with lower development risk. As a result, companies can use branded generics to build a strong market presence, improve product recall, and capture demand from physicians and patients seeking more affordable yet trusted brands. This opportunity is growing in chronic disease categories, where treatment demand is high and long-term.

- For instance, in January 2026, Sun Pharma received DCGI approval to manufacture and market generic semaglutide injection in India. It would launch the product under the brand name Noveltreat after the expiry of the semaglutide patent in India. Such development highlights the opportunity for branded generics companies to launch lower-cost versions of high-demand therapies and expand their market positions in large chronic-care segments.

MARKET CHALLENGES

Maintaining Regulatory Compliance and Manufacturing Quality Across Markets Poses a Challenge to Market Growth

The major challenge faced by the market is maintaining consistent regulatory compliance and manufacturing quality across different regions. As companies expand branded generic portfolios across multiple countries, they must meet strict approval, bioequivalence, labeling, and plant-quality requirements in each market. This makes operations more complex and increases the risk of delays, remediation costs, warning letters, or product recalls when quality systems fall short. These factors can result in supply disruptions, higher compliance spending, and reputational pressure, slowing portfolio expansion and reducing the commercial momentum of branded generics.

- For instance, in April 2025, Arab Times published an article titled ‘Dozens of life-saving drugs pulled for violating safety standards ‘, reporting that nearly 40 medicines made by Glenmark Pharmaceuticals were recalled in the U.S. because of manufacturing practice concerns at its India facility. Such instances can trigger regulatory action and create additional pressure on companies operating in the generics space.

Segmentation Analysis

By Therapy Area

High Disease Prevalence and Long-Term Care Burden to Lead the Segmental Growth of Cardiovascular Diseases

Based on therapy area, the market is categorized into anti-infectives, cardiovascular, gastrointestinal, vitamins, minerals & nutritional, CNS, respiratory, anti-diabetic, dermatology, pain management, and others.

Among these, the cardiovascular diseases segment dominated the market. The segment dominated because heart-related disorders such as hypertension, heart failure, dyslipidemia, and ischemic heart disease affect a very large patient population and usually require long-term treatment. Since these therapies are taken for extended periods, prescription volumes remain consistently high, creating strong demand for lower-cost branded alternatives.

- For instance, in August 2025, MSN Pharmaceuticals launched its generic Sacubitril + Valsartan Tablets in the U.S., indicated to reduce the risk of cardiovascular death and hospitalization in adults with chronic heart failure and reduced ejection fraction. This reflects how companies are actively expanding branded/generic cardiovascular portfolios in high-demand chronic-care categories.

The anti-diabetic segment is expected to grow at a CAGR of 8.10% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Route of Administration

Increasing Commercial Applications of Whole Body Twins to Boost Segmental Growth

Based on the route of administration, the market is segmented into oral, parenteral, topical, inhalation, and others.

In 2025, the oral segment accounted for the largest branded generics market share. Oral medicines are easier to manufacture, store, transport, prescribe, and administer than most other dosage forms. They also improve patient convenience and treatment adherence. These factors make them suitable for high-volume off-patent drugs for various indications. As a result, major pharmaceutical companies can scale oral branded generic products faster, reach wider retail distribution, and generate larger prescription volumes.

- For instance, in October 2025, Lupin Limited announced the launch of a branded generic version of Ravicti (Glycerol Phenylbutyrate) Oral Liquid, 1.1 g/mL, in the U.S. This highlights how oral formulations remain an attractive route for generic expansion, as they offer easier patient use and broader commercial reach.

The inhalation segment is projected to grow at a CAGR of 8.21% during the forecast period.

By Distribution Channel

Vast Distribution Network of Retail Pharmacies to Lead Growth in the Segment

Based on the distribution channel, the market is segmented into retail pharmacies, hospital pharmacies, online pharmacies, and others.

By distribution channel, the retail pharmacies accounted for the largest share of the market. These settings remain a major dispensing point for high-acuity treatments, complex therapies, and physician-supervised medicines. Many branded generics used in emergency care, intensive care, oncology support, perioperative settings, and other institutional use cases are stocked and purchased through hospital channels, supporting higher value concentration.

- For instance, in December 2025, Amneal Pharmaceuticals received approval from the U.S. FDA for epinephrine injection USP, 1 mg/mL, noting that the product expands its injectables portfolio and is an essential medicine used in U.S. hospitals for emergency and perioperative care. This shows how hospital-focused generic launches continue to support the dominance of the hospital pharmacy channel in the market.

The online pharmacies segment is projected to grow at a CAGR of 11.99% over the study period.

Branded Generics Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Branded Generics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 21.79 billion and maintained its leading position in 2025 at USD 22.98 billion. The market is growing in North America because regulators continue to support broader generic availability. Also, the region faces a significant chronic disease burden and high prescription volumes, which fuel market demand.

U.S. Branded Generics Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 22.47 billion in 2026, accounting for roughly 10.31% of the global market.

Europe

Europe is projected to grow at 5.68% over the coming years, the second-highest among all regions, and reach a valuation of USD 39.29 billion by 2026. The market is growing in Europe as health systems focus on expanding access to cost-effective off-patent medicines while managing reimbursement pressures and long-term care costs.

U.K. Branded Generics Market

The U.K. market is estimated at around USD 5.71 billion in 2026, representing roughly 2.62% of the global market.

Germany Branded Generics Market

Germany's market is projected to reach approximately USD 5.91 billion in 2026, equivalent to around 2.71% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 98.14 billion in 2026 and secure the position of the third-largest region in the market. The market is growing in the Asia Pacific because the region has a large population base, rising chronic disease incidence, expanding healthcare access, and strong physician preference for affordable branded medicines in several countries.

Japan Branded Generics Market

The Japanese market in 2026 is estimated at around USD 8.91 billion, accounting for approximately 4.09% of the global market.

China Branded Generics Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 21.02 billion, representing approximately 9.64% of global sales.

India Branded Generics Market

The Indian market in 2026 is estimated at around USD 31.18 billion, accounting for roughly 14.30% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The market in Latin America is estimated to reach a valuation of USD 28.35 billion. The market is growing in Latin America because the affordability of medicine remains a major concern, and governments and regional institutions are increasingly working to improve access, local production, and health system resilience. In the Middle East & Africa, the GCC is set to reach USD 5.24 billion in 2026.

South Africa Branded Generics Market

The South African market is projected to reach approximately USD 3.44 billion by 2026, accounting for roughly 1.58% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches by Key Players to Propel Market Progress

The global branded generics market is highly consolidated, with companies such as Abbott, Sun Pharmaceutical Industries Limited, Dr. Reddy’s Laboratories Limited, Cipla Limited, Lupin Limited, and Hikma Pharmaceuticals PLC holding significant market share. Strategic partnerships, new product launches, and increased investments in the sector drive these companies' market share gains.

- For instance, in March 2026, Lupin Limited collaborated with Zydus Lifesciences Limited to expand access to innovative Semaglutide Injection (15 mg/3 ml) with a patient-friendly reusable pen device in India. The partnership brought together Lupin Limited’s extensive reach in the Indian market and Zydus’ robust development capabilities, driven by the shared objective of bringing advanced therapies for metabolic disorders.

Other notable players in the global market include Amneal Pharmaceuticals, Inc., Padagis LLC, and GSK plc. These companies are expected to prioritize strategic collaborations and new product launches to strengthen their positions during the forecast period.

LIST OF KEY BRANDED GENERICS COMPANIES PROFILED

- Abbott (U.S.)

- Sun Pharmaceutical Industries Limited (India)

- Reddy’s Laboratories Limited (India)

- Cipla Limited (India)

- Lupin Limited (India)

- Viatris Inc.(U.S.)

- Sandoz AG (Switzerland)

- Hikma Pharmaceuticals PLC (U.K.)

- Alkem Laboratories Limited (India)

- Zydus Lifesciences Limited (India)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Accord Healthcare, Inc., re‑launched Hydrochlorothiazide Tablets, USP in 12.5 mg, 25 mg, and 50 mg strengths. Hydrochlorothiazide tablets are approved as adjunctive therapy in edema associated with congestive heart failure, hepatic cirrhosis, and corticosteroid and estrogen therapy, along with edema due to various forms of renal dysfunction such as nephrotic syndrome, acute glomerulonephritis, and chronic renal failure.

- February 2026: Cipla USA Inc. launched Liraglutide Injection, 18 mg/3 mL (6 mg/mL) single-patient-use prefilled pens, the generic equivalent of Saxenda (liraglutide injection).

- February 2026: Lupin Limited received approval from the U.S. FDA for its Abbreviated New Drug Application (ANDA) for Brivaracetam Oral Solution 10 mg/mL, indicated for the treatment of partial-onset seizures in patients 1 month of age and older.

- December 2025: Amneal Pharmaceuticals, Inc. received approval from the U.S. FDA for albuterol sulfate inhalation aerosol (90 mcg per actuation). The product is the generic equivalent of PROAIR HFA (albuterol sulfate inhalation aerosol), a registered trademark of Teva Respiratory LLC.

- February 2025: Hikma Pharmaceuticals PLC received U.S. FDA approval and launched Mercaptopurine Oral Suspension at 20mg/mL in the US. Hikma introduced the first generic of this product and was the first approved applicant to receive a Competitive Generic Therapy (CGT) designation from the US Food and Drug Administration.

- November 2022: Prasco Laboratories launched the Generic of ZIOPTAN (tafluprost ophthalmic solution) 0.0015%. This solution is the company’s first Generic launch in partnership with Théa Pharma, Inc.

REPORT COVERAGE

The report on the global branded generics market provides a detailed analysis of market size, historical performance, current trends, and future growth outlook across key regions. It examines the market by therapy area, route of administration, and distribution channel to highlight the major revenue-contributing segments and the factors supporting their growth. The study also evaluates key market drivers, restraints, opportunities, and challenges in a cause-and-effect manner to present a clear view of industry movement. In addition, it covers competitive developments, such as product launches, partnerships, acquisitions, and portfolio expansion strategies, adopted by leading companies in the market. The report also includes company profiling, regional insights, and an assessment of how pricing pressure, patent expirations, the chronic disease burden, and access to affordable medicines are shaping the future of the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.69% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Therapy Area, Route of Administration, Distribution Channel, and Region |

| By Therapy Area |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 204.31 billion in 2025 and is projected to reach USD 366.00 billion by 2034.

In 2025, the market value stood at USD 22.98 billion.

The market is expected to grow at a CAGR of 6.69% over the forecast period.

The cardiovascular Therapy Area segment is expected to lead the market.

The market is driven by growing demand for lower-cost prescription medicines.

Abbott, Sun Pharmaceutical Industries Limited, Dr. Reddy’s Laboratories Limited, Cipla Limited, and Lupin Limited are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us