Autoinjectors Market Size, Share & Industry Analysis, By Type (Disposable and Reusable), By Application (Autoimmune Disorders, Diabetes, Emergency Care, and Others), By Route of Administration (Intramuscular and Subcutaneous), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Regional Forecasts, 2026-2034

(Offer valid till 30th Jun 2026)

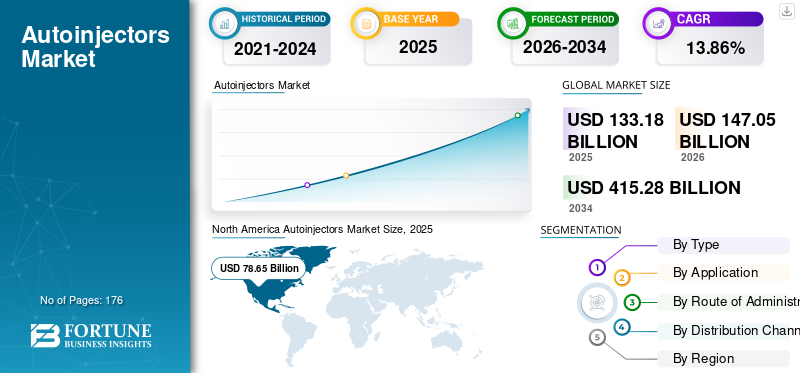

Autoinjectors Market Size and Future Outlook

The global autoinjectors market size was valued at USD 155.52 billion in 2025. The market is projected to grow from USD 182.67 billion in 2026 to USD 414.93 billion by 2034, exhibiting a CAGR of 10.8% during the forecast period. North America dominated the autoinjectors market with a market share of 60.58% in 2025.

Autoinjectors are spring-loaded devices equipped with a pre-filled syringe to self-administer a fixed dose of parental medicines to patients. These devices treat selected chronic diseases, such as rheumatoid arthritis and multiple sclerosis, and emergency treatments, including anaphylactic shock and migraine attacks. The incidence of emergency conditions such as anaphylactic shock and migraine attacks is increasing due to several causative agents, such as food allergens, insect bites, or drug insensitivity, across the globe. Owing to this rising incidence, demand for biological therapies used to treat these chronic diseases is also high, which is anticipated to drive market growth.

- According to an article published in the World Allergy Organization Journal in June 2024, the global lifetime prevalence of anaphylaxis is estimated to range between 0.3% and 5.1%, with an annual incidence of 50-112 cases per 100,000 people.

Viatris Inc., Bristol-Myers Squibb Company, and Teva Pharmaceutical Industries Ltd. held the major market share in 2025 due to strong brand reputation and a wide portfolio of autoinjector products.

Download Free sample to learn more about this report.

Autoinjectors Market Key Takeaways

- 2025 Market Size: USD 155.52 billion

- 2026 Market Size: USD 182.67 billion

- 2034 Forecast Market Size: USD 414.93 billion

- CAGR: 10.8% from 2026–2034

- North America dominated the autoinjectors market with a 60.58% share in 2025.

- The diabetes segment is projected to hold a 33.7% market share in 2026.

- The reusable segment is anticipated to grow at the fastest CAGR of 11.3% during the forecast period.

North America

North America led the global market in 2025, driven by high adoption of self-injection devices, advanced healthcare infrastructure, and strong presence of major pharmaceutical companies.

Europe

Europe secured the second-largest market position, supported by rising approvals of injectable devices and increasing collaborations among manufacturing players.

Asia Pacific

Asia Pacific is projected to emerge as the fastest-growing regional market due to the increasing prevalence of chronic diseases and rising demand for home-based emergency care solutions.

U.S.

The U.S. autoinjectors market is projected to reach USD 106.26 billion by 2026, supported by strong demand for diabetes management and self-administration therapies.

Japan

Japan is expected to generate approximately USD 6.86 billion in revenue by 2026, driven by growing adoption of advanced injectable drug delivery systems and rising chronic disease burden.

Read More

AUTOINJECTORS MARKET TRENDS

Rising Adoption of Disposable Autoinjectors among Patients to Boost Market Growth

Healthcare professionals have long relied on injection systems as convenient drug delivery devices for administering subcutaneous injections. However, challenges associated with conventional injection devices, such as needle stick injury, multiple low-dose injections, and the high costs associated with recurrent hospital visits, limited their preference among patients.

Thus, several market players are focused on developing and launching self-injection and wearable devices with high efficacy, patient compliance, and low cost globally. These products comprise accurate dosage volumes and already reconstituted drugs, with minimized chances of needle stick injuries. Such advantages of the product over other conventional devices drive higher patient adoption and adherence.

- According to an article published by ONdrugDelivery in May 2022, the annual volume of sales of disposable autoinjectors reached above 100.0 million.

Moreover, the number of prescriptions issued by healthcare professionals for self-injection therapies in acute care settings has increased awareness among patients suffering from chronic diseases. This led to increased awareness of drug delivery systems and a high preference for self-injection devices at home among patients. Moreover, the availability of more user-friendly, efficient, and patient-compliant products developed by injectable device industry players has further supported the adoption of these devices.

In addition, supportive regulatory authorities have enabled several industry players to receive approvals for disposable autoinjectors used in the treatment of various types of medical conditions.

- For instance, in October 2025, BD introduced a novel disposable autoinjector designed for patient self-administration of biologics, prioritizing safety and user-friendliness.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Incidence of Chronic Diseases to Boost Industry Growth

The demand for the product is rising across the globe owing to increasing incidence of chronic diseases such as Diabetes and Rheumatoid Arthritis. In response to this growing disease burden, several market players are shifting their focus toward the development of platform device technologies to support faster development and lessen device costs. Moreover, the rising focus by key players on enabling high-volume delivery of biosimilar and biologics in home-care settings will drive market growth.

- For instance, in March 2026, Portal Instruments signed a multi-million dollar development agreement to advance PRIME NEXUS, its large volume reusable autoinjector platform, toward clinical readiness.

Moreover, the production and introduction of reusable and technologically advanced platforms are increasing in response to the growing prioritization of sustainable drug delivery within the pharmaceutical industry. Similarly, key players are now emphasizing adding new devices to their existing product portfolio to enable self-administration by patients for larger-volume medications. The increasing number of autoinjectors launches across a wide range of applications including conditions, such as cancers and autoimmune disorders, will further strengthen the presence of these devices across developed nations, thereby boosting the global autoinjectors market growth.

- In May 2022, Jabil Healthcare, a division of Jabil Inc., announced the launch of the Qfinity autoinjector platform, a simple, reusable, and modular solution for subcutaneous drug self-administration at a lower cost than market alternatives.

- In October 2022, Ypsomed announced the launch of a new autoinjector platform, YpsoMate 5.5 autoinjector, for liquid medications with volumes between 1.5 mL and 5.5 mL. This latest addition to the YpsoMate portfolio enables self-administration for larger-volume medications.

MARKET RESTRAINTS

Product Recalls and Law Infringements for Autoinjectors May Hamper Market Growth

Although product launches of autoinjectors are increasing due to rising use among patients with autoimmune disorders and diabetes, product recalls related to potential manufacturing defects and inaccurate dosage delivery remain a key concern.

- For instance, in May 2025, Kitt Medical Limited stated that all Emerade adrenaline auto-injector pens are under recall due to potential malfunctions that could prevent effective anaphylaxis treatment.

Such issues may lead to increased regulatory scrutiny and stringent oversight, creating barriers to new product approvals and slowing overall market expansion. Moreover, product recalls result in financial losses for companies due to product withdrawal, replacements, and potential legal liabilities, which can adversely affect profitability and limit investment in future innovations.

MARKET OPPORTUNITIES

Increasing Patient Awareness to Offer Lucrative Growth Opportunities

The rising prevalence of anaphylaxis, cardiac arrest, and respiratory disorders, along with increasing patient awareness, is creating demand for improved treatment options for the management of these conditions. In response, key market players are focusing on R&D to develop new therapeutics for allergy management.

- For instance, in February 2024, ALK-Abelló A/S and researchers from McMaster University discovered a new cell that remembers allergies. The discovery provides scientists and researchers with a new target in treating allergies and facilitates the development of new therapeutics.

Traditionally used for administering drugs such as insulin and epinephrine, the product is now being developed for a variety of new therapeutic areas, including oncology, autoimmune diseases, and neurological disorders. This diversification is largely driven by the growing adoption of biologics and biosimilars, which require precise and regular dosing, making autoinjectors an effective drug delivery solution.

In oncology, several cancer therapies that were traditionally administered in hospitals are being adapted for self-injection formats, allowing patients to manage their treatment more conveniently at home. Similarly, the product is gaining traction in the administration of biologics for conditions such as rheumatoid arthritis and psoriasis, offering patients a less invasive, more convenient alternative to traditional injection methods.

Additionally, various key players are adopting growth strategies such as acquisition and collaborations to introduce advanced product to the market, aiming to address the unmet needs of people at high risk of anaphylaxis shocks.

MARKET CHALLENGES

Limited Availability of Adrenaline Autoinjectors across Developing Countries to Hamper Market

Adrenaline (epinephrine) is considered the first-line treatment for Anaphylaxis by healthcare professionals. However, despite its pivotal role, autoinjectable formulation are not readily available in most countries, which prevents optimal management of patients with anaphylaxis. Similarly, the lack of immediate access to this emergency medication during an anaphylaxis reaction increases the risk of progression to severe episode and death.

- According to an article published by UpToDate in February 2023, deaths reported due to anaphylaxis had annual rates of 0.21 to 0.76 per million population in the U.S.

- For instance, as per data published by the National Center for Biotechnology Information in November 2025, even in regions where adrenaline auto-injectors are available, only 44.0% of patients have a standardized action plan for their use in treating anaphylaxis.

These devices also suffer from limited availability via official channels such as retail or pharmacy networks worldwide. In many developing countries, access is restricted to special licensing programs or named-patient distribution channels.

Thus, the scarcity of epinephrine injection devices across distribution channels at retail pharmacies, leading to less adoption of the product among patients, may hamper market growth.

Segmentation Analysis

By Type

Rising Prevalence of Chronic Diseases Boosted Disposable Segment Growth

By type, the market is segmented into disposable and reusable.

The disposable segment accounted for the largest share in 2025. This growth is driven by the rising prevalence of chronic diseases across the globe, the rising recommendation of disposable devices by healthcare professionals, and the high preference for single-use devices by patients.

- According to an article published by Sciencedirect in October 2021, among 80 autoinjector devices launched by several manufacturers, 62.0% were disposable devices.

In addition, industry players' rising focus on launching innovative disposable devices and rising product approval by regulatory agencies further propel the segment’s share.

- For instance, in August 2022, Rafa Laboratories, Ltd., announced that it had received FDA approval for its 10mg Midazolam autoinjector for treating status epilepticus or prolonged seizures.

To know how our report can help streamline your business, Speak to Analyst

The reusable segment is expected to register a comparatively higher CAGR of 11.3% over the project period. The segment growth is driven by high potential advantages over disposable devices, such as ease of use, cost-effectiveness, and high safety. Moreover, rising emphasis by several key players on the introduction of devices to facilitate the growing market for subcutaneous injections used to treat chronic diseases such as rheumatoid arthritis, Crohn’s disease, and multiple sclerosis is primarily contributing to segment growth.

Several market players are focusing on the development of reusable auto-injectors as a low-waste alternative.

- For instance, in October 2024, Nemera unveiled its new reusable auto-injector platform at CPHI Milan, aligning with sustainability goals by reducing carbon footprints through reusable designs, bio-resins, and minimal parts.

By Application

Increasing Demand for Injectable Insulin Led to Diabetes Segment Growth

Based on application, the market is segmented into autoimmune disorders, diabetes, emergency care, and others.

The diabetes segment accounted for the highest global autoinjectors market share in 2025, owing to the increasing demand for injectable insulin among the rising diabetes population and initiatives by leading players to develop novel products to cater to the demand for diabetes management among patients. Moreover, the segment is projected to hold a 33.7% share in 2026.

The emergency care segment is projected to register a significant CAGR of 9.6% during the forecast period. The growth is attributable to a high incidence rate of anaphylactic episodes among the population due to specific causative agents such as food allergens, insect bites, and drug hypersensitivity, and rising demand for self-injection devices for the treatment of anaphylaxis.

- As per Allergy & Asthma Network statistics, the prevalence rate of anaphylaxis in the U.S. population is between 1.6% and 5.1%. Among the causative agents, medication allergy to non-steroidal anti-inflammatories (NSAIDs) constituted the most common factor for anaphylaxis (34.0%), followed by food allergy (31.0%).

Furthermore, some of the government authorities are funding autoinjectors for emergency treatment of anaphylaxis.

- For instance, as per data provided by pharmac.govt.nz in December 2022, the government of New Zealand decided to fund adrenaline auto-injectors from February 2023 for the emergency treatment of anaphylaxis.

By Route of Administration

Subcutaneous Segment Led the Market due to Increasing Demand for Self-Administration Devices

On the basis of the route of administration, the global market is segmented into intramuscular and subcutaneous.

The subcutaneous segment held the largest market share in 2025, owing to increasing demand for self-administration devices among home-use patients. Similarly, the rising production of subcutaneous devices by key players and increasing regulatory approvals of autoinjectors owing to high demand further propel segment growth. Furthermore, the segment is set to hold 81.6% share by 2026.

- For instance, in February 2024, Eisai Co., Ltd. and Nippon Medac Co., Ltd. unveiled that its Metoject Subcutaneous Injection Pen received manufacturing and marketing approval in Japan by its regulatory authority.

- In February 2025, AstraZeneca and Amgen announced the launch of Tezspire (tezepelumab) subcutaneous autoinjector in the U.S. for self-administration in patients aged 12 years and older with severe asthma.

The intramuscular segment is expected to grow at a CAGR of 10.2% over the forecast period. The growth is due to the high potential advantages of intramuscular products, such as rapid onset of action, convenience, and minimal pain among patients. Similarly, the high adoption of intramuscular injections among healthcare professionals for pediatric patients further boosts the segment’s share in the global market. Furthermore, the segment is set to hold 70.5% share by 2026.

- According to a study article published by NCBI in 2021, the intramuscular injection of adrenaline autoinjectors could achieve greater results owing to their rapid action compared to the subcutaneous route among patients.

By Distribution Channel

Key Players' Rising Focus On Enhancing Sales Boosted Retail Pharmacies Growth

Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies.

The retail pharmacies segment accounted for the highest market share in 2025. The growth is attributable to key players' rising focus on enhancing sales and distribution networks of these devices across developing countries. Furthermore, the segment is set to hold 67.7% share by 2026.

Hospital pharmacies are expected to grow at a significant CAGR of 10.0% during the forecast period. The growth is attributable to key players' rising focus on enhancing sales and distribution networks of these devices across developing countries.

Autoinjectors Market Regional Outlook

Based on region, the market can be divided into Europe, Latin America, North America, Asia Pacific, and the Middle East & Africa.

North America

North America Autoinjectors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 75.49 billion, and reached USD 94.21 billion in 2025. An increase in R&D and the introduction of new technologies in self-injection devices by key players to support inpatient treatment is likely to drive market growth in the region. Moreover, healthcare professionals' rising emphasis and recommendation of autoinjector prescriptions against anaphylactic episodes is further expected to boost regional market growth.

U.S. Autoinjectors Market

The U.S. is anticipated to reach USD 106.26 billion by 2026, accounting for approximately 58.2% of the global market.

Europe

Europe is projected to record a CAGR of 9.7% during the forecast period, the second-highest globally, reaching USD 39.84 billion by 2026. The market in Europe held a significant share due to increasing collaborations among manufacturing players to boost production, and rising approvals of new injectable devices across the region further boosted the European market.

- For instance, in January 2024, FUJIFILM Diosynth Biotechnologies signed a strategic partnership agreement with SHL Medical to enhance its autoinjector services.

- In May 2022, Stevanato Group S.p.A., a global drug delivery and diagnostic solutions provider, signed an exclusive agreement with leading medical device manufacturer Owen Mumford Ltd. for its Aidaptus autoinjector.

U.K. Autoinjectors Market

The U.K. market is projected to reach USD 6.47 billion by 2026, representing approximately 3.5% of global revenues.

Germany Autoinjectors Market

Germany's market is predicted to reach around USD 10.53 billion by 2026, representing around 5.8% of global revenue.

Asia Pacific

By 2026, Asia Pacific is projected to reach approximately USD 25.28 billion, making it the third-largest market worldwide. The market growth is driven by the growing prevalence of chronic disorders amongst the population. Huge demand for emergency care at home settings among patients is anticipated for the region's growth at the highest CAGR.

- For instance, according to the data published by Arthritis India in March 2026, rheumatoid arthritis (RA) affects around 0.92% of the adult population in India.

Japan Autoinjectors Market

Japan is projected to generate approximately USD 6.86 billion in revenue by 2026, representing nearly 3.8% of the global market.

China Autoinjectors Market

China’s market is anticipated to reach around USD 6.72 billion by 2026, accounting for nearly 3.7% of global revenues.

India Autoinjectors Market

India’s market is expected to reach approximately USD 2.04 billion by 2026, accounting for around 1.1% of global market revenue.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to witness moderate growth during the study period, with the Latin America market is estimated to reach approximately USD 3.58 billion by 2026. The region's growth is due to rising chronic disease prevalence amongst the population and the high adoption of these devices by patients in homecare settings. The market in the Middle East & Africa region is projected to grow at a moderate CAGR during the forecast period, owing to the rising diagnosis and treatment rate of anaphylaxis, creating demand for these devices.

GCC Autoinjectors Market

By 2026, the GCC market is estimated to reach approximately USD 1.05 billion, representing around 0.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus on the Adoption of Various Organic and Inorganic Growth Strategies to Maintain Their Positions

The global market is majorly led by producers such as Viatris, Bristol-Myers Squibb, Teva Pharmaceutical Industries Ltd., and other prominent players. Prominent market participants are concentrating on increasing investments in device production centers and rising collaborations & acquisitions owing to the huge demand for these devices globally.

- In July 2023, Viatris Inc. and Kindeva Drug Delivery L.P., a manufacturer of complex drug-delivery formats, including autoinjectors and other injectables, announced the launch of Breyna inhalation aerosol, the first generic version of AstraZeneca's Symbicort. Breyna, a drug-device combination product, is indicated for certain patients with asthma or chronic obstructive pulmonary disease (COPD).

Similarly, other major market players, including Recipharm AB, ALK-Abelló A/S, and Phillips-Medisize, are constantly focused on inorganic developments, such as strengthening distribution networks through strategic partnerships and securing product approvals across global markets.

- For instance, in July 2021, ALK-Abelló A/S, a Danish allergy immunotherapy company, announced a licensing agreement with China Grand Pharmaceutical and Healthcare Holdings (Grandpharma) to register and launch ALK’s adrenaline auto-injector (AAI) Jext in China, thereby expanding its regional presence.

Thus, continuous production advancements and rising efforts by key players to expand distribution channels through inorganic strategies, particularly in emerging nations, are expected to propel market expansion over the forecast period.

LIST OF KEY AUTOINJECTORS COMPANIES PROFILED

- Viatris Inc. (U.S.)

- Teva Pharmaceuticals, Inc. (Netherlands)

- Ypsomed AG (Switzerland)

- Recipharm AB (Sweden)

- Becton Dickinson and Company (U.S.)

- Halozyme, Inc. (U.S.)

- AstraZeneca (U.K.)

- Bristol-Myers Squibb (U.S.)

- Phillips-Medisize (U.S.)

- SHL Medical AG (Switzerland)

- Xeris Pharmaceuticals, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: MGS launched the A.i.r. Platform, a customizable auto-injector system with a patent-pending core engine supporting 0.3-2.25 mL fill volumes across multiple formats and therapies.

- September 2025: Sharp Services announced the investment of USD 20.0 million to expand autoinjector and pen assembly, labeling, and packaging lines at its Macungie, Pennsylvania, facility.

- April 2025: SHL Medical opened a new USD 220 million, state-of-the-art manufacturing facility in North Charleston, South Carolina, to meet surging global demand for its leading autoinjectors.

- June 2024: Instron launched its next-generation Autoinjector Testing System, enabling full functionality tests on pens, autoinjectors, safety syringes, and button-activated devices to ISO 11608 standards.

- May 2023: Boehringer Ingelheim International GmbH announced that the U.S. FDA approved the Cyltezo Pen, an autoinjector option for Cyltezo (adalimumab), an FDA-approved interchangeable biosimilar to Humira.

- May 2022: The FDA approved Eli Lilly and Company's Mounjaro (tirzepatide) injection, indicated as an adjunct to diet and exercise to improve glycemic control in adults with type 2 diabetes. The drug is available in six dose forms and will come in a well-established autoinjector.

- April 2022: Halozyme Therapeutics, Inc., entered into a definitive agreement to acquire Antares Pharma, Inc. The acquisition created a leading drug delivery and specialty product company in the business of autoinjector platforms.

REPORT COVERAGE

The global market report provides detailed market analysis and focuses on crucial aspects such as leading players, product types, and major applications of the product. Additionally, it offers insights into market trends and key industry developments such as mergers, partnerships, & acquisitions. In addition to the factors mentioned above, the report includes the factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.8% over 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Application, By Route of Administration, Distribution Channel, and Region |

| By Type |

|

| By Application |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 155.52 billion in 2025 and is projected to reach USD 414.93 billion by 2034.

Registering a CAGR of 10.8%, the market will exhibit steady growth over the forecast period (2026-2034).

By type, the disposable segment led the market in 2025.

The rising prevalence of chronic diseases is a key factor driving market growth.

Viatris Inc., Teva Pharmaceuticals Inc., and AstraZeneca are major companies in the global market.

The growing patient awareness is expected to drive the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 150

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us