Automated Fiber Placement (AFP) Market Size, Share & Industry Analysis, By Machine Architecture (Gantry-Based AFP Machines, Robotic Arm-Based AFP Machines, and Hybrid Motion AFP Machines), By Fiber Type (Carbon Fiber, Glass Fiber, and Aramid Fiber), By End-Use Industry (Aerospace & Defense, Automotive, Wind Energy, Energy & Industrial Equipment, Marine, and Research & Technology Centers), and Regional Forecast, 2026 - 2034

Automated Fiber Placement (AFP) Market Size and Future Outlook

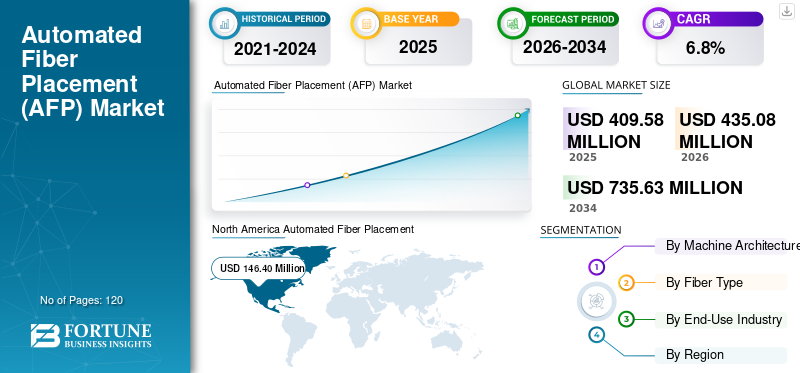

The global Automated Fiber Placement (AFP) market size was valued at USD 409.58 million in 2025. The market is projected to grow from USD 435.08 million in 2026 to USD 735.63 million by 2034, exhibiting a CAGR of 6.8% during the forecast period. North America dominated the automated fiber placement (afp) market with a market share of 35.74% in 2025.

Automated fiber placement refers to advanced composite manufacturing machinery used to lay down multiple narrow tows of resin-impregnated fibers with high precision for composites production of complex, load-bearing structures. These AFP systems are critical for manufacturing primary and secondary structural components in aerospace and defense, space, and select industrial applications, where fiber orientation control, repeatability, and material efficiency directly influence structural performance and production efficiency. Compared with traditional automated tape laying machines, AFP platforms enable high speed, multi-tow placement and enhanced process control for high performance composite materials. The market for automated fiber placement machines is witnessing structurally driven growth as aircraft OEMs and Tier-1 suppliers expand composite-intensive programs across aerospace automotive and wind energy applications, including advanced structures such as wind turbine blades, while increasing automation penetration across primary structures and transitioning toward digitally enabled manufacturing environments.

- For instance, in March 2025, Electroimpact continued deliveries of large-format gantry-based AFP systems for primary aerostructure manufacturing programs, while MTorres expanded the use of its AFP platforms within Airbus-linked composite production lines, reflecting sustained OEM investment in high-rate, automation-intensive composite manufacturing infrastructure.

Fives Group, Ingersoll Machine Tools, Electroimpact, MAG Industrial Automation, Broetje-Automation, MTorres, Coriolis Composites, Automated Dynamics, MIKROSAM, and Accudyne Systems are among the key players holding a significant share of the market. Their competitive positioning is supported by strong installed bases across major aerospace programs, broad portfolios spanning gantry, robotic, and hybrid AFP architectures, and the capability to deliver application-specific, turnkey composite manufacturing cells.

Download Free sample to learn more about this report.

AUTOMATED FIBER PLACEMENT (AFP) MARKET TRENDS

Shift from Fixed, Program-Specific AFP Systems to Modular and Reconfigurable Production Architectures is an Emerging Market Trend

Composite manufacturers are increasingly moving away from fixed, program-dedicated AFP installations toward modular and reconfigurable AFP systems to manage fluctuating production rates, multi-program manufacturing, and evolving material requirements. AFP suppliers are responding by offering robotic and hybrid architectures with flexible layouts, scalable tow capacities, and software-driven process control, enabling brownfield composite facilities to expand or reconfigure capacity incrementally while improving equipment utilization and reducing capital risk.

- For instance, in March 2025, Coriolis Composites emphasized the growing adoption of modular robotic AFP cells designed for reconfiguration across multiple composite part geometries, supporting flexible production planning and faster qualification cycles for aerospace and industrial customers.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Integrated Composite Manufacturing Portfolios Enabling End-to-End AFP Deployment

Strategic portfolio expansion by leading AFP equipment manufacturers is driving Automated Fiber Placement (AFP) market growth. Aerospace OEMs and composite Tier-1 suppliers increasingly favor vendors capable of delivering integrated solutions spanning fiber placement, tooling interfaces, inspection, and material handling, reducing system integration complexity and improving production reliability. This shift is encouraging AFP suppliers to strengthen complementary automation and software capabilities, supporting investments in both Greenfield composite facilities and phased upgrades at existing manufacturing sites.

- For instance, in June 2024, Fives Group advanced the integration of AFP systems with downstream inspection and handling technologies, strengthening its end-to-end composite manufacturing offering for high-rate aerospace production programs.

MARKET RESTRAINTS

High Capital Intensity and Program-Specific Qualification Requirements Limiting Flexible AFP Adoption

Unlike conventional machining or assembly equipment, automated fiber placement systems require high upfront capital investment and extensive process qualification tied to specific parts, materials, and production programs. Variations in component geometry, fiber architecture, and certification standards across aerospace and defense platforms often necessitate customized AFP configurations, increasing system cost and limiting redeployability. For manufacturers operating with uncertain production rates or short program lifecycles, the risk of underutilization and prolonged qualification timelines can delay AFP adoption, particularly where return on investment is highly sensitive to long-term program stability and production volume commitments.

MARKET OPPORTUNITIES

Expansion of AFP Adoption Beyond Large Aerospace OEMs Unlocking Demand from Tier-2 and Regional Composite Manufacturers

A growing opportunity for the market lies in the gradual adoption of AFP technology by Tier-2 suppliers and regional composite manufacturers beyond large aerospace OEM ecosystems. Increasing composite content in aircraft, space, defense, and industrial platforms is pushing smaller manufacturers to transition from manual layup and semi-automated processes toward compact and cost-optimized AFP solutions. This shift is driving demand for robotic and hybrid AFP systems that offer lower capital intensity, smaller footprints, and faster qualification pathways, enabling incremental automation upgrades without the scale, complexity, or investment requirements of large gantry-based installations.

- For instance, in July 2024, Coriolis Composites highlighted increased deployment of its robotic AFP systems among Tier-2 aerospace and industrial composite manufacturers seeking flexible, space-efficient automation solutions to support growing composite part production.

MARKET CHALLENGES

Fragmented Certification Standards and Program-Specific Qualification Requirements Challenging Market Scalability

Automated fiber placement manufacturers and end users face challenges arising from fragmented certification, qualification, and program-specific approval requirements across aerospace, defense, space, and industrial end markets. AFP systems often need to be customized and requalified to meet varying OEM standards, material specifications, and regulatory compliance frameworks, particularly for flight-critical composite structures. This lack of harmonization increases engineering complexity, extends qualification timelines, and limits standardization of AFP platforms. For manufacturers supporting multiple programs or customers, repeated validation cycles and configuration changes can slow deployment, elevate project risk, and discourage investment in highly specialized or single-program AFP installations.

Segmentation Analysis

By Machine Architecture

Gantry-Based AFP Machines Dominate Market Share Due to Primary Structure Manufacturing Requirements

The market, based on machine architecture, is segmented into gantry-based AFP machines, robotic arm-based AFP machines, and hybrid motion AFP machines.

The gantry-based AFP machines hold the highest Automated Fiber Placement (AFP) market share as they remain the preferred solution for manufacturing large, load-bearing composite structures such as wings, fuselage sections, pressure vessels, and space launch components. These systems provide superior positional accuracy, high tow placement capacity, and stable deposition over large surface areas, making them essential for high-rate aerospace and defense programs where dimensional consistency, repeatability, and certification compliance are critical. Their dominance is further reinforced by deep integration into long-running commercial aircraft and defense production lines, where replacement cycles and incremental upgrades sustain ongoing demand.

- For instance, in September 2024, MTorres advanced the use of its gantry-based automated fiber placement systems within aerospace composite manufacturing lines, supporting high-precision layup of large structural components and reinforcing the continued dominance of gantry architectures in primary aerostructure production.

The robotic arm-based AFP machines are witnessing the highest growth, registering a CAGR of 7.7% over the forecast period, driven by increasing demand for flexible, space-efficient, and reconfigurable composite manufacturing solutions. These systems are gaining traction among Tier-2 suppliers, regional composite manufacturers, and industrial users producing complex-geometry parts with lower volume variability. Their ability to support multi-part production, faster redeployment, and lower upfront investment compared to gantry systems is accelerating adoption, particularly in brownfield facilities and emerging composite applications. Growing use in thermoplastic AFP processing and non-aerospace structural components is further strengthening the growth outlook for robotic AFP architectures.

To know how our report can help streamline your business, Speak to Analyst

By Fiber Type

Carbon Fiber Dominates Market Share Due to Structural Performance and Certification Requirements

Based on fiber type, the market is segmented into carbon fiber, glass fiber, and aramid fiber.

The carbon fiber segment accounts for the largest share of the market due to its widespread use in primary and secondary aerospace, defense, and space structures where high strength-to-weight ratio, fatigue resistance, and stiffness are critical. AFP systems are predominantly configured for carbon fiber tow placement, as certification standards, long-running aircraft programs, and established material supply chains strongly favor carbon composites. The dominance of carbon fiber is further reinforced by its extensive qualification across wings, fuselage sections, pressure vessels, and space structures, making it the default material for high-value AFP applications.

- For instance, in May 2024, Ingersoll Machine Tools highlighted continued demand for carbon fiber-based AFP systems supporting large composite aerostructure manufacturing, reflecting sustained reliance on carbon composites in primary structural applications.

The glass fiber segment is expected to witness the highest growth, registering a CAGR of 7.5% over the forecast period, driven by expanding AFP adoption in cost-sensitive aerospace substructures, wind energy, and industrial composite applications. Compared to carbon fiber, glass fiber offers lower material cost and improved impact resistance, making it attractive for non-flight-critical structures and large industrial components.

By End-Use Industry

Aerospace & Defense Dominates Market Share Due to High Composite Intensity and Certification-Driven Automation

Based on end-use industry, the market is segmented into aerospace & defense, automotive, wind energy, energy & industrial equipment, marine, and research & technology centers.

The aerospace & defense segment accounts for the largest share of the market, driven by the extensive use of AFP systems in manufacturing primary and secondary composite structures such as wings, fuselage sections, empennage, pressure vessels, and space structures. These applications require precise fiber placement, repeatability, and certification-compliant processes, making AFP a critical production technology. Long aircraft program lifecycles, high composite content per platform, and stringent structural performance requirements continue to sustain strong demand for AFP systems across commercial aerospace, defense aircraft, and space launch programs.

The automotive segment is expected to witness the highest growth, registering a CAGR of 8.1% over the forecast period, driven by increasing adoption of lightweight composite structures in electric vehicles, performance vehicles, and structural battery enclosures. Automotive manufacturers are increasingly evaluating robotic and hybrid AFP systems to enable repeatable fiber placement for complex geometries while maintaining cycle-time efficiency and cost control. Growing emphasis on vehicle lightweighting, crash performance, and structural integration, combined with rising production volumes of electric and premium vehicles, is accelerating AFP adoption beyond prototyping toward low-to-medium volume serial production environments.

Automated Fiber Placement (AFP) Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Automated Fiber Placement (AFP) Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for over USD 146.40 million revenue in 2025, supported by the region’s large installed base of composite manufacturing facilities and strong concentration of aerospace, defense, and space production programs. The presence of major aircraft OEMs, Tier-1 aerostructure suppliers, and defense contractors continues to sustain demand for gantry-based and robotic AFP systems used in primary and secondary composite structures. Increasing aircraft production rates, rising composite content per platform, and ongoing replacement and upgrade of legacy automated tape laying and manual layup processes are driving steady investment in AFP equipment. In addition, labor constraints, certification requirements, and the need for repeatable, high-quality composite production are reinforcing automation adoption across the U.S., Canada, and Mexico.

U.S. Automated Fiber Placement (AFP) Market

The U.S. to dominate the North American market with an estimated revenue of about USD 131.24 million in 2026, supported by its extensive aerospace and defense manufacturing footprint and leadership in composite-intensive aircraft and space programs. The country hosts a large number of AFP installations across commercial aerospace, defense aviation, space launch vehicles, and advanced industrial applications. Strong integration between OEMs and composite Tier-1 suppliers, combined with sustained investment in production rate increases, tooling upgrades, and digital manufacturing, continues to drive demand for both large-format gantry AFP systems and flexible robotic architectures.

Europe

The European market holds a significant share of the market, supported by a strong concentration of aerospace, defense, and space composite manufacturing programs across the region. Demand is driven by long-established aircraft production ecosystems, stringent certification and quality requirements, and high composite penetration in both commercial and defense platforms. Germany, France, the U.K., Italy, and Spain lead AFP adoption, supported by Airbus-linked aerostructure manufacturing, space systems production, and advanced Tier-1 composite suppliers. Ongoing modernization of legacy composite facilities, replacement of older automated tape laying systems, and increasing focus on production rate scalability and digital manufacturing integration continue to underpin steady AFP equipment demand across Europe.

U.K. Automated Fiber Placement (AFP) Market

The U.K. market is estimated at around USD 19.22 million in 2026, representing roughly 4.4% of global revenues.

Germany Automated Fiber Placement (AFP) Market

Germany’s market is projected to reach approximately USD 24.90 million in 2026, equivalent to around 5.7% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing market, which generated revenue of USD 105.05 million in 2025 globally. Market growth is driven by increasing localization of aircraft structures, indigenous aerospace and space programs, and rising investment in advanced composite production infrastructure. China, Japan, South Korea, India, and ASEAN countries are key contributors, supported by new composite manufacturing facilities, growing Tier-1 and Tier-2 supplier bases, and government-backed aerospace and defense initiatives. The region is witnessing a structural shift from manual layup and basic automation toward robotic and hybrid AFP systems, particularly in China, India, and Southeast Asia, as manufacturers seek scalable, cost-efficient, and flexible composite production solutions.

China Automated Fiber Placement (AFP) Market

China’s market is projected to remain the dominant in the region, with 2026 revenues estimated at around USD 37.03 million, representing roughly 8.5% of global sales.

Japan Automated Fiber Placement (AFP) Market

The Japan market is estimated at around USD 19.93 million in 2026, accounting for roughly 4.6% of the global market.

India Automated Fiber Placement (AFP) Market

The Indian market is estimated at around USD 12.23 million in 2026, accounting for roughly 2.8% of global revenues.

Middle East & Africa

The Middle East & Africa market is driven by growing investment in aerospace, defense, and advanced industrial composite manufacturing, particularly across the GCC countries, Israel, and select parts of North Africa. Government-backed defense modernization programs, space initiatives, and industrial diversification strategies are supporting demand for automated fiber placement systems used in high-performance composite structures. The GCC benefits from high-capex, automation-intensive composite manufacturing projects, while Israel continues to invest in AFP-enabled production for defense and UAV applications.

GCC Automated Fiber Placement (AFP) Market

The GCC market is projected to reach around USD 4.71 million in 2026, representing roughly 1.1% of the global market.

South America

The South America market is supported by the region’s growing participation in aerospace, defense, and advanced industrial composite manufacturing, led primarily by Brazil and Argentina. Demand for automated fiber placement systems is driven by localized aerostructure production, defense modernization programs, and increasing use of composites in industrial and energy applications. Brazil represents the largest market, supported by established aerospace manufacturing capabilities and ongoing investment in composite structures, while Argentina contributes through defense and niche aerospace programs.

Brazil Automated Fiber Placement (AFP) Market

The Brazil market is projected to reach around USD 11.34 million in 2026, representing roughly 2.6% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Integrated Composite Automation Solutions and Program-Level Capability Intensifies Market Competition

The automated fiber placement market is moderately consolidated, characterized by a limited number of global manufacturers offering advanced composite automation systems spanning gantry-based, robotic, and hybrid AFP architectures. Leading players such as Fives Group, Ingersoll Machine Tools, Electroimpact, MTorres, Broetje-Automation, Coriolis Composites, Automated Dynamics, MIKROSAM, MAG Industrial Automation, and Accudyne Systems hold strong competitive positions, supported by established installed bases across major aerospace and defense programs and long-term relationships with OEMs and Tier-1 composite manufacturers.

Competitive differentiation is increasingly driven by program-level integration capability, placement head technology, thermoplastic processing compatibility, and digital manufacturing software integration rather than standalone machine hardware. Manufacturers are focusing on modular AFP platforms that enable scalable production rates, reconfigurable layouts, and integration with inspection, material handling, and tooling systems. This approach allows composite manufacturers to modernize brownfield facilities, support multi-program production, and improve process consistency while managing certification and qualification complexity.

- For instance, in June 2024, Coriolis Composites emphasized the expansion of its modular robotic AFP platforms with enhanced software-driven process control and reconfigurable cell layouts, supporting aerospace customers pursuing flexible, multi-part composite manufacturing environments.

LIST OF KEY AUTOMATED FIBER PLACEMENT COMPANIES PROFILED IN REPORT

- Fives Group (France)

- Ingersoll Machine Tools, Inc. (U.S.)

- Electroimpact, Inc. (U.S.)

- Trelleborg Group (Sweden)

- Broetje-Automation GmbH (Germany)

- Torres Industrial Designs (Spain)

- Coriolis Composites (France)

- Automated Dynamics, Corp. (U.S.)

- MIKROSAM (Macedonia)

- Accudyne Systems, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2024: Rocket Lab installed a large Electroimpact robotic AFP system for its Neutron rocket composite structures, automating high-volume carbon fiber component production and reducing manual labor.

- September 2024: MTorres announced advancements in its AFP technology portfolio, emphasizing enhanced gantry-based systems and integrated composite manufacturing solutions designed to support higher-rate aircraft production and complex structural layup applications.

- July 2024: Coriolis Composites showcased upgrades to its robotic AFP platforms, focusing on modular cell configurations, improved process monitoring software, and expanded thermoplastic composite placement capabilities for aerospace and industrial customers.

- June 2024: Fives Group strengthened its composite automation offering by advancing integration between AFP systems and downstream inspection and material handling solutions, supporting turnkey composite production line deployment.

- April 2024: Ingersoll Machine Tools continued deployment of its Mongoose™ AFP systems for large composite components, underscoring growing demand for high-precision, wide-format fiber placement solutions across aerospace and energy applications.

REPORT COVERAGE

The global Automated Fiber Placement (AFP) market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.8% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Machine Architecture, Fiber Type, End-Use Industry and Region |

| By Machine Architecture |

|

| By Fiber Type |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stands at USD 435.08 million in 2026 and is projected to reach USD 735.63 million by 2034.

In 2025, the market value in North America stood at USD 146.40 million.

The market is expected to exhibit a CAGR of 6.8% during the forecast period of 2026-2034.

By end-use industry segment, the aerospace & defense is expected to lead the market.

Rising composite complexity and automation intensity across aerospace and industrial sectors driving demand for advanced automated fiber placement systems.

Fives Group, Electroimpact, Ingersoll Machine Tools, MTorres, Broetje-Automation, and Accudyne Systems are the major players in the global market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us