Automotive Advanced Manufacturing Bodies Market Size, Share & Industry Analysis, By Manufacturing Technology (Advanced Robotics & Automation, Laser Welding & Advanced Joining Technologies, Hot Stamping & Press Hardening, & Others), By Vehicle Type (Hatchback & Sedans, SUVs, LCVs, and HCVs), By Propulsion Type (ICE and Electric), By Material Type (Advanced High-Strength Steel, Aluminum & Aluminum Alloys, Composites, & Others), By Body Structure Type (Body-in-White, Closures, Structural Frames & Underbody Systems, Crash Management Structures, & Others), and Regional Forecast, 2026-2034

Automotive Advanced Manufacturing Bodies Market Size and Future Outlook

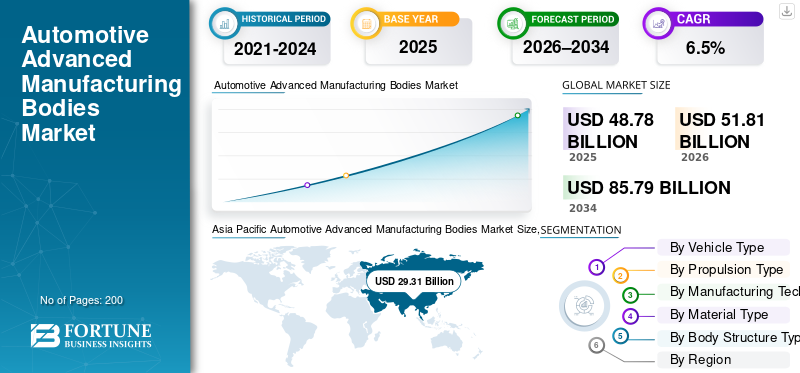

The global automotive advanced manufacturing bodies market size was valued at USD 48.78 billion in 2025. The market is projected to grow from USD 51.81 billion in 2026 to USD 85.79 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period. Asia Pacific dominated the automotive advanced manufacturing bodies market with a market share of 60.08% in 2025.

Automotive advanced manufacturing bodies refer to vehicle body structures produced using advanced materials, automation, robotics, and precision forming technologies to enhance strength, safety, light weighting, and production efficiency. Market drivers include demand for lightweight vehicles, stricter safety and emissions regulations, electric vehicle adoption, the use of advanced materials, automation investments, and OEMs’ focus on cost efficiency and scalable manufacturing.

Major players in the market include Magna International, Gestamp, Benteler, Martinrea, Magna Steyr, Flex-N-Gate, thyssenkrupp Automotive Body Solutions, and voestalpine, competing through lightweight structures, advanced materials, automation, and high-precision body manufacturing technologies.

Download Free sample to learn more about this report.

Automotive Advanced Manufacturing Bodies Market Key Takeaways

- 2025 Market Size: USD 48.78 billion

- 2026 Market Size: USD 51.81 billion

- 2034 Forecast Market Size: USD 85.79 billion

- CAGR: 6.50% from 2026–2034

- Asia Pacific dominated the market with a 60.08% share in 2025.

- The Digital Manufacturing & Industry 4.0 segment is the fastest-growing, registering a 7.90% CAGR during the forecast period.

- The Electric segment is the fastest-growing, expanding at a 10.60% CAGR during the forecast period.

Asia Pacific

Asia Pacific dominates the global market and remains the fastest-growing region, driven by expanding EV production

North America

North America market is projected to reach USD 13.09 billion by 2034.

Europe

Europe holds the second-largest market and is projected to grow at a 6.20% CAGR during the forecast period.

U.S.

U.S. market is estimated to reach USD 5.67 billion in 2026.

Japan

Japan market is projected to reach USD 4.61 billion in 2026.

Read More

AUTOMOTIVE ADVANCED MANUFACTURING BODIES MARKET TRENDS

Shift Toward Multi-Material Body Structures and Modular Platforms is a Key Market Trend

One of the major automotive advanced manufacturing bodies market trends is the transition toward multi-material body structures and modular vehicle platforms. Automakers increasingly combine steel, aluminum, composites, and magnesium to optimize weight, crash performance, and cost. Modular platforms enable faster model launches and shared components across ICE and EV portfolios. This trend accelerates the adoption of advanced joining technologies, simulation-driven design, and flexible manufacturing systems capable of handling diverse materials within a single production line.

- In August 2022, STRUCTeam explored advances in multimaterial EV battery enclosures, highlighting multi-material composite design to meet safety, weight, thermal, and structural integration needs, influencing future battery enclosure manufacturing and complex body assembly in electric vehicles.

MARKET DYNAMICS

MARKET DRIVERS

Light Weighting and EV Architecture Complexity to Drive Advanced Body Manufacturing Demand

Rising demand for lightweight vehicles and the rapid shift toward electric mobility are key drivers for automotive advanced manufacturing bodies. Automakers are increasingly adopting aluminum, AHSS, composites, and multi-material structures to improve range, safety, and structural integrity. Complex EV architectures, including battery enclosures and structural floor assemblies, require high-precision manufacturing technologies such as hot stamping, laser welding, and technologically advanced robotics, driving sustained investment across global OEM and Tier-1 facilities.

- In January 2025, GM expanded its additive manufacturing strategy, deploying 3D printing for body fixtures, tooling, and select structural components, improving production flexibility and supporting lightweight, next-generation automotive body manufacturing.

MARKET RESTRAINTS

High Capital Investment and Technology Integration to Restrain Market Expansion

The adoption of advanced manufacturing technologies for automotive advanced manufacturing bodies requires substantial upfront capital expenditure. High costs associated with robotics, automation systems, laser-based joining, and specialized tooling limit adoption, particularly among smaller manufacturers. Additionally, integrating new technologies into existing production lines can disrupt operations and increase downtime. Skill gaps in operating and maintaining advanced equipment further complicate operations, hindering rapid, uniform automotive advanced manufacturing bodies market growth.

MARKET OPPORTUNITIES

Localization of EV Production to Create New Manufacturing Opportunities

Growing localization of electric vehicle production presents significant opportunities for automotive advanced body manufacturing. Governments are encouraging domestic manufacturing through incentives, while vehicle manufacturers are establishing regional EV plants to reduce supply-chain risks. This drives demand for localized body-in-white, battery enclosure, and structural component manufacturing. Suppliers offering flexible, scalable, and multi-material body solutions can capitalize on new Greenfield projects and long-term supply contracts across emerging and mature automotive sector markets.

- In December 2025, Maruti Suzuki announced plans to localize EV battery production and critical components ahead of the e-VITARA launch, expanding charging infrastructure and EV-enabled workshops to strengthen India’s EV ecosystem and support localized structural and body part manufacturing.

MARKET CHALLENGES

Process Complexity and Quality Consistency to Challenge Advanced Body Manufacturing

Maintaining consistent quality across complex, multi-material automotive bodies remains a critical challenge. Advanced forming and joining processes demand precise control, real time monitoring, and rigorous validation to avoid defects. Variations in material behavior, thermal expansion, and joining compatibility increase the risk of rework and scrap. Ensuring repeatability at high volumes, while meeting stringent safety standards, places continuous pressure on manufacturers to invest in process optimization and skilled workforce development.

Download Free sample to learn more about this report.

Segmentation Analysis

By Manufacturing Technology

Automation-Driven Productivity and Precision to Strengthen Advanced Robotics & Automation Segment Growth

By manufacturing technology, the market is divided into advanced robotics & automation, laser welding & advanced joining technologies, hot stamping & press hardening, additive manufacturing, digital manufacturing & industry 4.0.

The advanced robotics & automation segment dominates the market. This demand stems from its critical role in delivering high-volume, high-precision automotive body production. OEMs and Tier-1 suppliers rely on robotic welding, material handling, and automated assembly to ensure consistency, reduce defects, and improve throughput. Increasing model complexity, multi-material body structures, and stringent safety requirements reinforce sustained investment in robotics, making automation the backbone of modern body manufacturing operations globally.

- In December 2025, Hyundai announced major investments in humanoid robots for logistics and industrial work, aiming to integrate autonomous machines into manufacturing and material handling operations, boosting automation, body assembly throughput, and flexible intralogistics in future automotive production.

Digital manufacturing & industry 4.0 is the fastest-growing segment, expanding at a CAGR of 7.9% during the forecast period. Rising adoption of digital twins, predictive maintenance, and real-time production monitoring helps manufacturers improve efficiency, reduce downtime, and optimize costs across advanced automotive body manufacturing lines.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

High Passenger Car Production Volumes and Standardized Body Architectures to Sustain Hatchback & Sedans Dominance

Based on vehicle type, the market segmentation is divided into hatchback & sedans, SUVs, LCVs, and HCVs.

The hatchback & sedans segment dominates the market due to their high global production volumes and standardized body structures. These vehicles rely heavily on mature, high-throughput body-in-white processes using robotics, laser welding, and press hardening. Large-scale manufacturing programs, especially in the Asia Pacific and Europe, ensure steady demand for advanced body manufacturing technologies, tooling upgrades, and process automation across OEM and Tier-1 production facilities.

- In February 2025, Kia unveiled its EV4 and Concept EV2 at Kia EV Day, expanding its core EV lineup with a new electric sedan and B-segment SUV concept, reinforcing future body and structural design evolution for electrified platforms.

The SUVs segment is the fastest-growing, expected to grow at a CAGR of 7.6% during the forecast period. Rising consumer preference for larger vehicles and electrified SUVs is driving increasing demand for complex, lightweight body structures, leading to higher adoption of advanced materials, modular platforms, and flexible manufacturing technologies.

By Propulsion Type

Established ICE Production Scale and Mature Body Platforms to Strengthen ICE Segment Growth

Based on propulsion type, the market is segmented into ICE and electric.

The ICE segment dominates the market due to its extensive global production base and well-established body manufacturing platforms. High volumes of passenger cars and commercial vehicles powered by ICE continue to rely on proven body-in-white processes, robotics, and forming technologies. Ongoing model refreshes, safety upgrades, and lightweighting initiatives sustain steady investments in advanced manufacturing equipment and process optimization across ICE vehicle body production lines worldwide.

The electric segment is the fastest-growing, with a 10.6% CAGR during the forecast period. Rapid EV adoption drives demand for battery enclosures, structural floor assemblies, and lightweight body architectures, accelerating the use of advanced materials, automation, and next-generation manufacturing technologies.

- In January 2026, Volvo revealed details of its upcoming EX60 EV SUV, featuring megacasting and structural battery integration to reduce body component complexity, lower costs, and improve production efficiency for electric vehicle body structures on its new SPA3 platform.

By Material Type

Cost-Effective Light Weighting and Proven Formability to Drive Advanced High-Strength Steel Requirements

By material type, the market is categorized into advanced high-strength steel, aluminum & aluminum alloys, composites, magnesium alloys, and multi-material body structures.

Advanced high-strength steel dominates the market, due to its optimal balance of strength, weight reduction, and cost efficiency. Automakers widely adopt AHSS for body-in-white and structural components to meet crash safety and emission regulations without major process overhauls. Its compatibility with existing stamping, welding, and automation infrastructure ensures high-volume scalability, sustaining strong demand across ICE and electric vehicle body manufacturing programs.

- In November 2022, Honda deployed advanced manufacturing technologies for the Civic family, incorporating automation, high-strength materials, and optimized body structures to improve productivity, enhance production efficiency, and vehicle safety performance.

Multi-material body structures are the fastest-growing segment, expanding at a CAGR of 8.5% during the forecast period. Increasing use of aluminum, composites, and magnesium alongside steel supports aggressive lightweighting targets and complex EV architectures, driving adoption of advanced joining and flexible manufacturing technologies.

By Body Structure Type

Core Structural Role and High-Volume Production to Sustain Body-in-White Segmental Dominance

By body structure type, the market is categorized into body-in-white, closures, structural frames & underbody systems, crash management structures, battery enclosures & structural floor assemblies.

The body-in-white segment dominates the market, as it serves as the fundamental structural framework for all vehicle types. High production volumes across passenger cars and commercial vehicles drive continuous demand for advanced stamping, welding, press hardening, and robotic assembly technologies. Ongoing safety upgrades, platform renewals, and lightweighting initiatives ensure steady investments in BIW manufacturing capabilities across global OEM and Tier-1 facilities.

Battery enclosures & structural floor assemblies are the fastest-growing segment, expanding at a CAGR of 8.4% over the forecast period. Rapid electric vehicle adoption increases demand for crash-resistant, lightweight battery structures, accelerating the use of advanced materials, precision joining, and highly automated manufacturing processes.

Automotive Advanced Manufacturing Bodies Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Advanced Manufacturing Bodies Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global market and is the fastest-growing region. The region’s growth is attributed to its massive vehicle production base and expanding electric vehicle manufacturing. China, Japan, South Korea, and India host large OEM and Tier-1 facilities investing heavily in robotics, automation, and advanced body technologies. Rapid EV adoption, cost-competitive manufacturing, government incentives, and continuous capacity expansions for body-in-white and battery structures collectively drive strong, sustained market growth across the region.

- In December 2025, Singapore launched its first 5G-enabled smart automotive factory, enabling real-time robotics coordination, digital quality monitoring, and connected manufacturing systems that enhance productivity and precision in advanced body and structural component production.

China Automotive Advanced Manufacturing Bodies Market

The China automotive advanced manufacturing bodies market in 2026 is projected to reach a valuation of USD 17.89 billion, accounting for roughly 34.5% of global market revenues. The dominance is driven by large-scale vehicle production, rapid automation adoption, lightweight material integration, strong EV manufacturing, and continuous investments in smart factories and advanced body-in-white technologies.

Japan Automotive Advanced Manufacturing Bodies Market

The Japan automotive advanced manufacturing bodies market in 2026 is set to be valued at USD 4.61 billion, accounting for roughly 8.9% of global market revenues. Market growth in Japan is supported by precision engineering leadership, high automation intensity, advanced robotics usage, focus on quality manufacturing, and steady demand from hybrid and next-generation vehicle platforms.

India Automotive Advanced Manufacturing Bodies Market

The India automotive advanced manufacturing bodies market is likely to reach USD 3.50 billion in 2026, accounting for roughly 6.8% of global market revenues. India’s rapid growth stems from expanding vehicle production, localization of body manufacturing, rising EV investments, government manufacturing incentives, and increasing adoption of automated welding and forming technologies.

Europe

Europe holds the second-largest automotive advanced manufacturing bodies market share, growing at a CAGR of 6.2% during the forecast period, supported by stringent emission and safety regulations. Automakers increasingly adopt lightweight materials, multi-material body structures, and advanced joining technologies. Strong EV penetration, premium vehicle manufacturing, and early adoption of Industry 4.0 technologies across Germany, France, and the U.K. sustain steady investments in advanced automotive body manufacturing infrastructure.

- In November 2025, the U.K. government launched the GBP 2.5 billion (USD 3.35 billion) DRIVE35 initiative to scale automotive manufacturing innovation, supporting automation, advanced materials, and digital body manufacturing technologies across OEMs and Tier-1 suppliers.

Germany Automotive Advanced Manufacturing Bodies Market

The Germany automotive advanced manufacturing bodies market in 2026 is expected to reach a valuation of USD 2.24 billion, accounting for roughly 4.3% of global market revenues. The market growth in Germany is driven by premium vehicle production, Industry 4.0 adoption, advanced lightweight structures, strong OEM Tier 1 collaboration, and continuous innovation in body manufacturing processes.

U.K. Automotive Advanced Manufacturing Bodies Market

The U.K. automotive advanced manufacturing bodies market in 2026 is estimated at around USD 0.50 billion, accounting for roughly 1.0% of global market revenues. The market in U.K. is supported by niche vehicle manufacturing, EV-focused body platforms, investments in flexible manufacturing systems, and increasing adoption of advanced materials and automation technologies.

North America

North America market is projected to reach USD 13.09 billion by 2034. The regional market in automotive advanced manufacturing bodies is driven by steady vehicle production and growing electrification initiatives. OEMs and Tier-1 suppliers continue to modernize body manufacturing lines with automation, digital manufacturing, and flexible tooling. Increasing focus on investments in EV plants, battery assembly, and localized supply chains supports demand for advanced body-in-white and structural component manufacturing technologies across the region.

- In September 2024, Toyota partnered with a U.S. firm to pilot a custom manufacturing breakthrough, leveraging advanced forming and digital processes to enable flexible body production and faster adaptation to evolving vehicle platform requirements.

U.S. Automotive Advanced Manufacturing Bodies Market

The U.S. automotive advanced manufacturing bodies market in 2026 is estimated at around USD 5.67 billion, accounting for roughly 10.9% of global market revenues. The demand stems from its large-scale automotive manufacturing footprint and accelerating EV investments. Major OEMs are upgrading body shops with advanced robotics, laser welding, and press hardening technologies. Federal incentives for domestic EV production and battery manufacturing further drive demand for advanced body structures, particularly for electric SUVs and pickup trucks.

Rest of the World

The rest of the world is experiencing gradual market growth driven by emerging automotive manufacturing hubs in South America, the Middle East, and parts of Africa. Increasing vehicle assembly localization, expanding EV adoption, and investments in modern manufacturing facilities are boosting demand for advanced body manufacturing technologies. However, adoption remains selective due to cost sensitivity and infrastructure limitations.

COMPETITIVE LANDSCAPE

Key Industry Players

Automation, Advanced Materials, and Platform Engineering Define Competitive Intensity

The automotive advanced manufacturing bodies market is moderately consolidated, dominated by global Tier-1 suppliers and specialized body engineering firms with strong OEM relationships. Key players such as Magna International, Gestamp, Benteler, Martinrea, Magna Steyr, Flex-N-Gate, thyssenkrupp Automotive Body Solutions, and voestalpine compete through advanced robotics, multi-material expertise, and scalable body-in-white platforms. Competitive differentiation centers on lightweighting capabilities, digital manufacturing, and EV-ready structural solutions. Companies strengthen positions through capacity expansions, automation upgrades, strategic partnerships, and localized production to support regional OEM platforms and evolving electric vehicle architectures.

LIST OF KEY AUTOMOTIVE ADVANCED MANUFACTURING BODIES COMPANIES PROFILED

- Magna International Inc. (Canada)

- Gestamp Automoción S.A. (Spain)

- Benteler International AG (Austria)

- Martinrea International Inc. (Canada)

- Kirchhoff Automotive GmbH (Germany)

- Thyssenkrupp Automotive Technology (Germany)

- ArcelorMittal Automotive (Luxembourg)

- Voestalpine AG (Austria)

- POSCO Automotive Steel Solutions (South Korea)

- Nippon Steel Corporation (Japan)

- Hyundai Steel Company (South Korea)

- Novelis Inc. (U.S.)

- Constellium SE (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Sony Honda Mobility announced advancements to the AFEELA platform, emphasizing software-defined vehicle integration that increases demand for adaptable body structures and digitally engineered manufacturing processes to support future mobility architectures.

- January 2026: Magna announced DRIVE Hyperion-compatible ECUs and Tier-1 integration services, reinforcing its role in platform-level integration that increasingly links vehicle electronics architecture with advanced body and structural system design.

- September 2025: DXC Technology advanced AI innovation in automotive manufacturing through startup collaborations, enabling digital engineering, smart factory optimization, and AI-driven production planning for advanced automotive body manufacturing operations.

- September 2025: Hennessey Special Vehicles broke ground on an advanced manufacturing facility featuring automation-driven body fabrication and precision assembly, supporting growing demand for high-performance vehicles and reinforcing investments in flexible, low-volume advanced automotive body manufacturing.

- September 2025: Machina Labs advanced custom automotive manufacturing using AI-driven robotics and metal forming, enabling rapid production of complex body panels and structural components without traditional tooling, supporting flexible, next-generation automotive body manufacturing models.

- November 2024: Inteva Products expanded its Pune manufacturing plant to support rising production demand, strengthening localized manufacturing of automotive structural and body components while enhancing automation, capacity scalability, and supply-chain resilience in the Asia Pacific.

- June 2024: BMW expanded additive manufacturing capabilities by opening a USD 26.84 million Additive Manufacturing Campus in Munich, scaling industrial 3D printing for body-related tooling, structural components, and production aids, enabling flexible, high-precision manufacturing and reduced development lead times.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, By Propulsion Type, By Manufacturing Technology, By Material Type, By Body Structure Type, and By Region |

|

By Vehicle Type |

· Hatchback & Sedans · SUVs · LCVs · HCVs |

|

By Propulsion Type |

· ICE · Electric |

|

By Manufacturing Technology |

· Advanced Robotics & Automation · Laser Welding & Advanced Joining Technologies · Hot Stamping & Press Hardening · Additive Manufacturing · Digital Manufacturing & Industry 4.0 |

|

By Material Type |

· Advanced High-Strength Steel · Aluminum & Aluminum Alloys · Composites · Magnesium Alloys · Multi-material Body Structures |

|

By Body Structure Type |

· Body-in-White · Closures · Structural Frames & Underbody Systems · Crash Management Structures · Battery Enclosures & Structural Floor Assemblies |

|

By Geography |

· North America (By Vehicle Type, By Propulsion Type, By Manufacturing Technology, By Material Type, By Body Structure Type, and By Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, By Propulsion Type, By Manufacturing Technology, By Material Type, By Body Structure Type, and By Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, By Propulsion Type, By Manufacturing Technology, By Material Type, By Body Structure Type, and By Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World (By Vehicle Type, By Propulsion Type, By Manufacturing Technology, By Material Type, By Body Structure Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 48.78 billion in 2025 and is projected to reach USD 85.79 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 29.31 billion.

The market is expected to exhibit a CAGR of 6.5% during the forecast period of 2026-2034.

The hatchback & sedans segment leads the market in terms of vehicle type.

Stricter safety and crashworthiness regulations are the key factors driving the market.

Key players in the market include Magna International, Gestamp, Benteler, Martinrea, Magna Steyr, Flex-N-Gate, thyssenkrupp Automotive Body Solutions, and voestalpine, among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us