Automotive Air Fuel Module Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, Light Commercial Vehicles, and Heavy Commercial Vehicles), By Module Type (Fuel Injection Modules and Air Management Modules), By Fuel Type (Gasoline, Diesel, and Alternative Fuels), By Technology Type (Port Fuel Injection, Gasoline Direct Injection, Diesel Common Rail Direct Injection, and Electronic Throttle Control Modules), By Propulsion Type (ICE and Hybrid), By Sales Channel (OEM and Aftermarket) and Regional Forecasts, 2026-2034

Automotive Air Fuel Module Market Size and Future Outlook

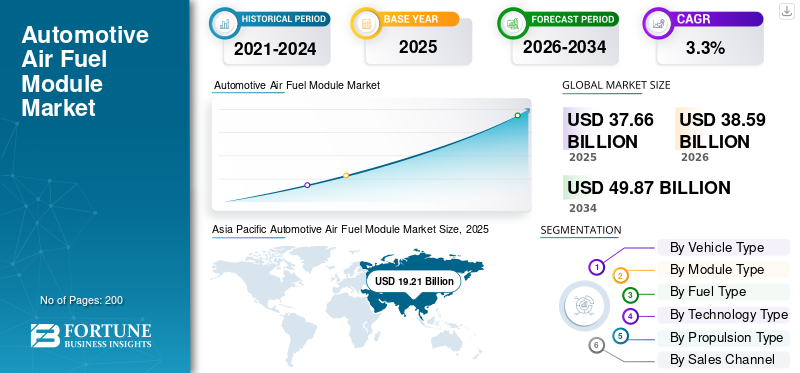

The global automotive air fuel module market size was valued at USD 37.66 billion in 2025. The market is projected to grow from USD 38.59 billion in 2026 to USD 49.87 billion by 2034, exhibiting a CAGR of 3.3% during the forecast period. Asia Pacific dominated the automotive air fuel module market with a market share of 51.1% in 2025.

The automotive air fuel module market covers the integrated parts and electronics that measure, meter, and deliver air and fuel to an engine to maintain stable, clean, and efficient combustion. In simple terms, these modules help an engine breathe the right amount of air and drink the right amount of fuel at the right moment, often using sensors, actuators, and control logic that react in real time. This market includes assemblies such as fuel delivery and injection-related modules, air intake/throttle-related modules, and supporting management systems (engine control strategies and interfaces) that maintain the target air–fuel ratio across different loads and temperatures.

Over the forecast period, market dynamics will be shaped by stricter emissions regulations and the need for improved fuel economy without sacrificing drivability. Automakers and suppliers are investing in technological advancements such as higher-pressure injection, improved atomization, tighter airflow control, and more accurate sensing to meet stringent emission targets while keeping solutions cost effective for mass-market vehicles. At the same time, the industry must manage supply chain volatility, including exposure to raw materials price swings and electronic component availability, which can influence module cost and lead times. These forces act as core growth drivers and sustain market growth even as electrification expands.

Key applications include passenger cars and light commercial vehicles, where precise mixture formation improves performance and reduces tailpipe emissions. The market report typically evaluates market share shifts by vehicle type, module type, fuel type, and technology, as adoption patterns differ by regulatory intensity, driving cycles, and consumer preferences.

Key players such as Bosch, Schaeffler, and Denso are strengthening product portfolios, expanding R&D, and forming partnerships to improve performance, compliance readiness, and manufacturing resilience across global platforms.

Download Free sample to learn more about this report.

AUTOMOTIVE AIR FUEL MODULE MARKET TRENDS

Migration Toward Precise Direct-Injection and Smarter Airflow Control is a Key Market Trend

A key market trend is continued migration toward gasoline direct injection and more advanced throttle/airflow solutions, supported by better sensing and control algorithms. As GDI adoption expands, suppliers focus on cleaner combustion and reduced particulates through improved atomization, tighter pressure control, and more responsive airflow management. This trend elevates the role of software-calibrated management systems and increases electronic content that operates in real time.

For instance, in February 2024, the U.S. DOE reported that GDI reached 73% adoption in 2023 model-year light-duty production, demonstrating the sustained shift toward higher-precision injection architectures.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Tightening Emissions and Efficiency Targets Accelerate Advanced Air-Fuel Modules

Stronger emission regulations and rising expectations for fuel economy are major growth drivers for the air–fuel module ecosystem. To comply with stringent emission limits, automakers need more accurate mixture formation, improved injection timing, and tighter airflow control, which is driving demand for higher-performance modules and smarter management systems that respond in real time. This driver supports steady automotive air fuel module market growth even when vehicle programs shift across regions.

- For instance, in April 2024, the EU Council adopted Euro 7 rules, reinforcing stricter lifetime emissions requirements pushing OEMs to improve air and fuel control hardware and calibration.

MARKET RESTRAINTS

Accelerating EV Adoption and Reduced ICE Investments Hampers Market Growth

While hybrids still use air–fuel modules, accelerating EV adoption gradually constrains the core ICE-only opportunity. As battery-electric volumes rise, some OEMs reduce investment in new combustion platforms, which can dampen incremental demand for advanced fuel and air hardware in certain segments. This restraint affects market dynamic planning, especially for suppliers with high ICE exposure, and can pressure pricing and market share in mature markets.

- For instance, in April 2024, IEA’s Global EV Outlook highlighted rapid EV expansion and policy momentum, signaling a structural shift that can limit future ICE platform growth in key markets.

MARKET OPPORTUNITIES

Hydrogen and Alternative-Fuel ICE Advancements in Air-Fuel Systems Offers Growth Opportunities

Hydrogen and other alternative-fuel ICE programs create an eco-friendly pathway that requires specialized injectors, rails, sensors, and control logic to manage new combustion behaviors safely and efficiently. This opportunity supports innovation in air–fuel metering and control, potentially adding premium content per vehicle and diversifying supplier revenue. It also encourages partnerships that strengthen supply chain readiness for new component specifications and validation requirements.

- For instance, in June 2024, Voith and Weifu signed a strategic cooperation agreement to develop hydrogen storage systems, reflecting accelerating hydrogen mobility programs that can stimulate adjacent injection and control-module innovation.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Price Fluctuations Creates Market Challenge

Air–fuel modules increasingly rely on sensors, ECUs, and power electronics, so disruptions in the supply chain can delay builds or raise costs. Suppliers also face raw materials price swings, which can pressure margins and complicate long-term contracts. Maintaining quality and delivery performance under volatile input conditions is a persistent challenge, especially when OEM launch schedules are fixed, and compliance deadlines are non-negotiable.

- For instance, in October 2025, ACEA warned that a shortage of simple chips used in vehicle control units was hitting automakers, underscoring ongoing electronics-related supply risks for module-heavy systems.

Segmentation Analysis

By Vehicle Type

Higher Torque Needs and Efficiency Optimization Drives SUVs Segment Growth

On the basis of vehicle type, the market is segmented into hatchback/sedan, SUVs, light commercial vehicles, and heavy commercial vehicles.

SUVs segment dominates the market as they typically require strong low-end torque and consistent drivability across varied loads, increasing the value of precise air and fuel control for combustion stability and efficiency. Their heavier mass and higher frontal area can worsen consumption, so OEMs increasingly rely on advanced mixture control and optimized injection/airflow strategies to protect fuel economy and compliance. This supports higher module content intensity and reinforces the SUVs segment growth.

- For instance, in May 2024, IEA reported that SUVs accounted for 48% of global car sales in 2023, reinforcing why SUV platforms drive higher demand for robust air–fuel control solutions.

To know how our report can help streamline your business, Speak to Analyst

SUVs segment is expected to grow at a CAGR of 4.3% over the forecast period.

By Module Type

Rising Precision and Emission Compliance Requirements Drives Fuel Injection Modules Segment Growth

On the basis of module type, the market is segmented into fuel injection modules and air management modules.

Fuel injection modules segment dominates the market as they directly govern atomization, timing, and delivered quantity, making them central to meeting emission regulations and drivability targets. As injection pressure and precision requirements rise, OEMs adopt higher-performance injectors, pumps, rails, and control strategies to reduce particulates and stabilize combustion. This makes fuel injection modules a dominant value contributor in the air–fuel stack and a key lever for market share wins.

- For instance, in September 2024, PHINIA launched an electronically controlled, low-pressure common-rail injection system with Kohler, highlighting continued investment in advanced injection architectures for efficiency and emissions compliance.

Fuel injection module segment is expected to grow at a CAGR of 3.6% over the forecast period.

By Fuel Type

Large Installed Base and Ongoing Combustion Optimization Boosts Gasoline Segment Growth

On the basis of fuel type, the market is segmented into gasoline, diesel and alternative fuels.

Gasoline segment dominates with the largest automotive air fuel module market share, owing to the largest installed base across many passenger-car markets, sustaining high volumes for gasoline-specific air–fuel modules. Even where hybridization grows, gasoline engines still require precise air metering and injection control to meet emissions and efficiency targets. As suppliers optimize combustion and reduce particulates, gasoline-focused module platforms continue to anchor scale, pricing leverage, and long-running OEM programs.

- For instance, in February 2024, DOE highlighted broad efficiency technology adoption in light-duty production, with GDI becoming mainstream, indirectly reflecting the continued centrality of gasoline powertrains to module demand.

Alternative fuels segment is expected to grow at a CAGR of 4.7% over the forecast period.

By Technology Type

Enhanced Combustion Control and Emission Compliance Drives Gasoline Direct Injection Segment Expansion

On the basis of technology type, the market is segmented into port fuel injection, gasoline direct injection, diesel common rail direct injection, and electronic throttle control modules.

Gasoline direct injection segment dominates the market as it improves control over mixture formation, supporting better combustion stability and enabling efficiency gains across many operating modes. As emission regulations tighten and particulate control becomes more important, GDI hardware and calibration sophistication increase, raising content per vehicle. Suppliers compete on injector precision, pressure stability, and integrated controls to deliver compliance and performance, reinforcing GDI leadership.

- For instance, in February 2024, DOE stated that GDI reached 73% adoption in 2023 model-year vehicles, underscoring why GDI remains the dominant technology focus for air–fuel module suppliers.

Electronic throttle control modules segment is expected to grow at a CAGR of 5.2% over the forecast period.

By Propulsion Type

Large Global Production Base and Ongoing Efficiency Upgrades Fuels ICE Segment Growth

On the basis of propulsion type, the market is segmented into ICE and hybrid.

Despite electrification, the ICE segment dominates the market and continues to represent a substantial global production and parc, sustaining strong demand for air–fuel metering hardware and controls. Many markets also favor affordable combustion and hybrid solutions, keeping ICE platforms active through the forecast period. Continuous improvement programs, targeting efficiency, durability, and emissions, support steady demand for upgraded injection and airflow modules.

- For instance, in April 2024, IEA’s Global EV Outlook tracked rapid EV growth but also highlighted the scale of the existing combustion fleet, supporting continued demand for ICE air–fuel control solutions.

Hybrid segment is expected to grow at a CAGR of 4.2% over the forecast period.

By Sales Channel

OEM Segment Dominates the Market Due to Integrated Engine Design and Certification Requirements

On the basis of sales channel, the market is segmented into OEM and Aftermarket.

OEM segment dominates the market as air–fuel modules are designed, validated, and calibrated as part of the original engine and emissions certification package. This requires tight integration across hardware and software, which favors direct OEM sourcing and long-term supply agreements. While the aftermarket is meaningful for replacement, OEM programs drive scale, technology upgrades, and the highest-value launches.

- For instance, in November 2024, Magneti Marelli Parts & Services expanded its LPG injector range, illustrating aftermarket growth, but OEM-integrated systems still dominate new-vehicle module volumes.

Aftermarket segment is expected to grow at a CAGR of 4.3% over the forecast period.

Automotive Air Fuel Module Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Air Fuel Module Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant market share in 2025, valued at USD 19.21 billion, and also maintained the leading share in 2024, with USD 18.64 billion. Asia Pacific dominates due to high vehicle production volumes, strong ICE/hybrid penetration, and a broad model lineup across price points. Large domestic supply ecosystems in China, Japan, South Korea, and India support localized manufacturing, shorter lead times, and competitive pricing for injection and airflow components. In addition, rising middle-class mobility and stricter local emissions enforcement in key cities sustain upgrades in mixture control technology. These factors collectively strengthen regional demand and encourage suppliers to invest in capacity and localized engineering.

- For instance, as per OICA’s 2023 production statistics show Asia’s top producers (notably China, Japan, and India) are leading global output, supporting high regional demand for air–fuel modules.

China Automotive Air Fuel Module Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at USD 10.37 billion, representing roughly 27.5% of global revenues.

India Automotive Air Fuel Module Market

The Indian market in 2025 was valued at USD 3.26 billion, accounting for roughly 8.7% of global revenues.

Europe

Europe is estimated to reach USD 8.43 billion in 2026 and secure the position of the second-largest region in the market. Europe’s market grows through compliance-driven upgrades as tighter standards drive improvements in injection precision, particulate control, and calibration robustness. Suppliers prioritize efficiency improvements, durability testing, and integration support to meet evolving rules and lifetime requirements. In the U.S., demand stays supported by a large gasoline fleet and SUV-heavy mix, sustaining module volumes even as electrification expands unevenly across states.

Germany Automotive Air Fuel Module Market

Germany’s market in 2025 was valued at USD 2.40 billion, accounting for roughly 6.4% of global revenues.

U.K. Automotive Air Fuel Module Market

U.K. market in 2025 was valued at USD 1.16 billion, accounting for roughly 3.1% of global revenues.

North America

North America is projected to record a growth rate of 3.0% over the coming years, and reach a valuation of USD 7.33 billion by 2026. North America benefits from an SUV-leaning fleet and continuous efficiency and emissions optimization in gasoline platforms. OEMs and suppliers focus on improving mixture control, reducing particulates, and enhancing drivability, which supports ongoing adoption of more precise injectors, pumps, sensors, and airflow control components across high-volume vehicle lines.

U.S. Automotive Air Fuel Module Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 6.01 billion, representing roughly 16.0% of global revenues.

Rest of the World

The rest of the world grows through expanding vehicle parc, longer service life, and gradual emissions tightening in major urban centers. As fleets modernize, demand for reliable, serviceable injection and airflow components that improve fuel efficiency and reduce visible emissions is growing, with a meaningful pull from commercial and value-focused passenger segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Companies are Implementing Various Strategies to Gain Leadership Position

The competitive landscape of the global automotive air fuel module market is led by large Tier-1 suppliers with deep calibration know-how, global manufacturing footprints, and strong OEM program access. Competitive advantage often comes from delivering modules that improve combustion stability, reduce particulates, and integrate seamlessly with the vehicle’s engine control architecture. As OEMs value reliability and repeatable emissions compliance, suppliers differentiate through durability validation, integration support, and software-enabled performance consistency, especially as emission regulations tighten.

A major strategy is platform modularity; suppliers design families of injectors, pumps, throttles, sensors, and control elements that can be scaled across engines and regions while keeping costs under control. This helps maintain cost effective sourcing and improves responsiveness to growing demand swings. Another strategy is co-development with automakers to tailor airflow and injection hardware to specific combustion concepts, improving calibration speed and achieving robust emissions performance in varied driving conditions. Increasingly, suppliers also compete on manufacturing resilience, multi-sourcing electronics, improving traceability, and reducing exposure to supply chain shocks and raw materials inflation. Many suppliers position their solution roadmaps around content market trends such as alternative fuels, hybridization, and hydrogen-capable injection architectures, framing them as a bridge between today’s ICE fleet and future propulsion mixes.

Competitive intensity is high as product cycles are long, switching costs are significant, and OEM quality gates are strict. As a result, key players pursue targeted partnerships and selective acquisitions to broaden portfolios, add software capability, or strengthen regional production footprints.

- For instance, in December 2023, Marelli introduced a hydrogen fuel system with dedicated injectors and an advanced ECU, highlighting suppliers’ push into cleaner combustion solutions.

LIST OF KEY AUTOMOTIVE AIR FUEL MODULE COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- DENSO Corporation (Japan)

- Continental AG (Germany)

- Hitachi Astemo, Ltd. (Japan)

- Marelli (Italy)

- MAHLE GmbH (Germany)

- BorgWarner Inc. (U.S.)

- Schaeffler AG (Germany)

- Aisin Corporation (Japan)

- Hyundai Mobis (South Korea)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Stanadyne introduced its GX Series, high-performance fuel pumps designed to deliver improved durability, optimized fuel flow characteristics, and enhanced pressure stability. The launch reflects ongoing demand for advanced fuel delivery solutions across both performance and specialized engine applications. The new series strengthens Stanadyne’s product portfolio in precision fuel system components amid tightening efficiency and emissions expectations.

- January 2025: American Honda Motor Co. announced a recall of approximately 295,000 vehicles in the U.S. to update the fuel injection Electronic Control Unit (ECU) software. The update aimed to correct improper fuel injection programming that could cause engine hesitation or stalling. This development highlights the critical role of precise air–fuel calibration and robust control logic in modern engine management systems.

- November 2024: Magneti Marelli Parts & Services launched a new LPG injector range focused on performance and extended lifespan, expanding injector options for alternative-fuel service markets.

- September 2024: MAHLE Powertrain supported hydrogen combustion development (Project Cavendish), aimed at fuel-injection systems ready for high-volume production aligned to future regulations.

- September 2024: PHINIA launched an electronically controlled, low-pressure common-rail injection system with Kohler, aiming to improve efficiency and meet emissions compliance requirements.

- April 2024: Bosch emphasized work on specialized injection systems for hydrogen engines, underscoring its R&D investment in next-generation fuel delivery architectures.

- December 2023: Stanadyne unveiled a high-pressure port-fuel injection enhancement kit for performance applications, expanding advanced injection offerings in the aftermarket.

REPORT COVERAGE

The global automotive air fuel module market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, Module Type, Fuel Type, Technology Type, Propulsion Type, Sales Channel and Region |

| By Vehicle Type |

|

| By Module Type |

|

| By Fuel Type |

|

| By Technology Type |

|

| By Propulsion Type |

|

| By Sales Channel |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 37.66 billion in 2025 and is projected to reach USD 49.87 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 19.21 Billion.

The market is expected to exhibit a CAGR of 3.3% during the forecast period.

SUVs segment is leading the market by vehicle type.

Tightening emissions and efficiency targets are the key factors driving the market.

Bosch, Denso, Schaeffler and Marelli are some of the top players in the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us