Automotive Ball Joint Market Size, Share & Industry Analysis, By Type (Upper Ball Joints and Lower Ball Joints), By Vehicle Type (Hatchbacks/Sedans, Sports Utility Vehicles (SUVs), and Commercial Vehicles), By Material (Steel, Aluminum, and others), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

Automotive Ball Joint Market Size and Future Outlook

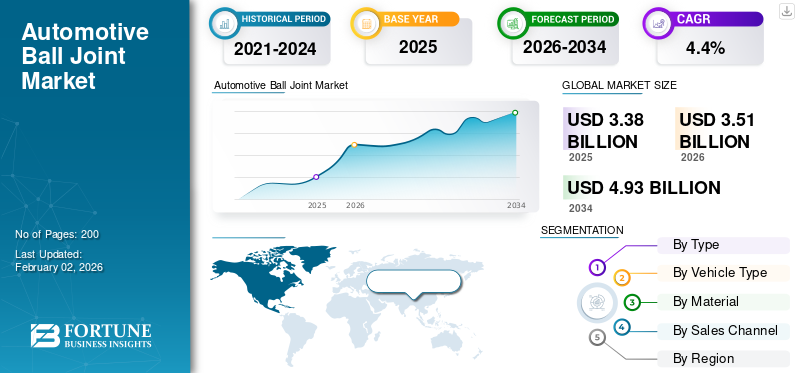

The global automotive ball joint market size was valued at USD 3.38 billion in 2025. The market is projected to grow from USD 3.51 billion in 2026 to USD 4.93 billion by 2034, exhibiting a CAGR of 4.4% during the forecast period. Asia Pacific dominated the global automotive ball joint market with a market share of 54.73% in 2025.

Automotive ball joints are spherical mechanical connectors used in a vehicle’s suspension system to link the control arms with the steering knuckles. Their design allows the wheels to move vertically over road irregularities while also turning left and right for steering. Most vehicles rely on at least one lower ball joint per front wheel, while multi-link and double-wishbone suspensions often use both upper and lower ball joints to improve stability and handling.

Ball joints are highly relevant because they directly influence steering precision, ride comfort, and overall vehicle safety. They carry significant loads during braking, cornering, and uneven-surface driving, making durability and reliability essential. A worn or damaged ball joint can cause poor handling, increased tire wear, noise, and even loss of control in severe cases. As a result, ball joints must meet strict performance and safety standards, and they require periodic inspection or replacement depending on road usage and vehicle type. Their importance grows as modern suspension systems become more complex and demand higher accuracy in wheel alignment and movement control.

The market is expanding due to several key factors. Rising global vehicle production, especially in regions with growing demand for passenger cars and light commercial vehicles, supports steady OEM (Original Equipment Manufacturers) consumption. The increasing popularity of SUVs and crossovers, vehicles that often use multi-link or heavy-duty suspension setups leads to a higher number of ball joints per vehicle. The demand from electric vehicles also contribute to market growth because their added battery weight and specialized suspension needs often require stronger, more advanced ball joint designs. Increasing average vehicle age globally is driving steady aftermarket demand, as older vehicles require more frequent suspension and ball joint replacements to maintain safety and stability. Additionally, regulations related to safety, ride comfort, and noise-vibration-harshness (NVH) are encouraging automotive manufacturers to adopt higher-quality, long-lasting components.

Key players in the market are focusing on innovation to meet new performance requirements. Manufacturers are using improved sealing systems, corrosion-resistant coatings, and high-strength materials to increase durability and fuel efficiency. Some companies are developing lightweight aluminum or hybrid-material ball joints for weight reduction. Other companies are designing ball joints specifically for EV platforms to handle higher loads and deliver smoother handling. These advancements reflect the industry’s movement toward safer, more durable, and more efficient suspension components.

Download Free sample to learn more about this report.

Automotive Ball Joint Market Key Takeaways

- 2025 Market Size: USD 3.38 billion

- 2026 Market Size: USD 3.51 billion

- 2034 Forecast Market Size: USD 4.93 billion

- CAGR: 4.4% from 2026–2034

- Asia Pacific dominated the automotive ball joint market with a 54.73% share in 2025.

- Lower Ball Joints accounted for the largest market share.

- The SUV segment held the dominant share due to growing global demand.

Asia Pacific

Strong vehicle production and expanding SUV and EV manufacturing support market growth.

North America

High SUV, pickup, and EV production continues to drive demand for ball joints.

Europe

Premium vehicle production and advanced suspension systems support steady market expansion.

U.S.

Rising EV production and robust automotive manufacturing strengthen OEM demand.

Japan

Advanced vehicle manufacturing and suspension innovation sustain steady market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Growing Adoption of Advanced Suspension Systems Increases the Ball Joint Usage

The shift toward multi-link, double-wishbone, and performance-oriented suspension systems in modern vehicles is increasing the number of ball joints needed per vehicle. These architectures are used to improve handling, stability, and ride comfort, especially in SUVs and premium models leading to higher OEM ball joint demand.

- For instance, Toyota’s TNGA platform uses multi-link rear suspension in models like the Camry and RAV4, increasing joint count for improved handling and stability.

MARKET RESTRAINTS:

Volatile Steel and Aluminum Prices Increase Manufacturing Pressures, Hampering the Demand for the Product

Ball joints rely heavily on steel and aluminum. These materials can experience frequent price fluctuations due to global supply changes, energy and production costs variations, and geopolitical conditions. This volatility directly impacts component manufacturing cost structures and squeezes margins for tier-1 and tier-2 suppliers.

- For example, the World Steel Association reports persistent fluctuations in global steel output and pricing due to shifting demand and geopolitical uncertainty.

MARKET OPPORTUNITIES:

Electrification and Hybrid SUVs Open New Market Segments Leading to Market Growth Opportunities

Electric vehicles require lightweight, low-friction suspension parts to compensate for battery mass and enhance driving efficiency. This shift enables new opportunities for specialized ball joint designs using aluminum housings, advanced coatings, and optimized geometries.

- For example, Tesla emphasizes lightweight suspension components in its Model 3 and Model Y to reduce weight and improve range efficiency.

MARKET CHALLENGES:

Global Supply Chain Risks and Regionalization to Hinder Market Growth

Although major pandemic related disruptions have eased, global supply chains still face challenges due to geopolitical tensions, shipping route shifts, and regional manufacturing diversification. These pressures complicate procurement stability and increase operational uncertainty for suspension component suppliers.

- For example, the U.S. Department of Transportation highlights continued freight delays and re-routing challenges driven by geopolitical and port-capacity constraints.

AUTOMOTIVE BALL JOINT MARKET TRENDS:

Adoption of Advanced Coatings and Long-Life Sealing Technologies

Manufacturers are increasingly developing ball joints with enhanced corrosion-resistant coatings, improved sealing systems, and longer maintenance intervals. These advancements aim to boost durability, reduce noise and vibration, and deliver longer service life across demanding road conditions.

- For instance, ZF Friedrichshafen AG’s Smart Chassis Sensor is integrated into the ball joint and monitors wheel movement, ride height, and surface irregularities in real time.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Lower Ball Joints Lead Due to Their Role as Essential Load-Bearing Components in Modern Suspension Systems

On the basis of type, the market is segmented into upper ball joints and lower ball joints.

Lower ball joints dominate because they are the primary load-bearing joints in most passenger vehicles, especially those using MacPherson strut suspensions that require only lower joints. Their critical role in carrying vehicle weight and maintaining wheel alignment makes them more commonly used across all vehicle categories.

- For instance, MOOG explains that the lower ball joint typically carries the vehicle’s load and experiences higher stress than the upper joint, making it essential in nearly all front-suspension architectures.

By Vehicle Type

SUVs Dominate Owing to Higher Adoption and Greater Ball-Joint Usage per Vehicle

On the basis of vehicle type, the market is segmented into hatchbacks/sedans, Sports Utility Vehicles (SUVs), and commercial vehicles.

The SUV segment dominates due to its higher global adoption, heavier suspension requirements, and its frequent use of multi-link or double-wishbone systems that increase ball-joint content per vehicle. The rising popularity of SUVs across regions further boosts the demand for high-strength suspension components.

- For instance, the Toyota RAV4 and Honda CR-V continued strong global momentum in 2024, reflecting sustained consumer preference for SUVs with robust suspension setups.

To know how our report can help streamline your business, Speak to Analyst

By Material

Steel Remains the Leading Material Due to Its Superior Strength and Durability

On the basis of material, the market is segmented into steel, aluminum, and others.

Steel dominates due to its superior load-bearing capacity, fatigue strength, durability, and cost-effectiveness, qualities required for critical joints operating under heavy mechanical stress. Steel remains the preferred choice for OEMs producing suspension components for both passenger and commercial vehicles.

- For example, the World Steel Association reports that high-strength steel grades continue to be widely used in automotive chassis components due to their performance under heavy load conditions.

By Sales Channel

OEM Segment Leads, Driven by Mandatory Installation of High-Precision Suspension Components

On the basis of sales channel, the market is segmented into OEM and aftermarket sales.

The OEM segment dominates because ball joints are safety-critical components installed during initial assembly, and automakers rely on certified, high-precision joints that meet strict durability and certification standards. Increasing global vehicle production also strengthens the demand for OEM sales channel.

- For instance, ZF supplies OEM-grade chassis joints including control-arm and suspension joints to automakers globally, emphasizing precision, durability, and compliance with strict manufacturing standards.

Automotive Ball Joint Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and Rest of the World.

Asia Pacific

The Asia Pacific region held the dominant automotive ball joint market share, supported by its large-scale vehicle production, expanding SUV and EV manufacturing, and strong presence of global and regional automakers. China, Japan, India, and South Korea remain central to the region’s leadership, backed by established supply chains, high-volume assembly plants, and continuous investments in chassis and suspension technologies. OEMs across Asia Pacific increasingly utilize multi-link, boosting the demand for advanced suspension systems including high-precision ball joints. For instance, Hyundai Motor Company reported sustained production growth across its Asia Pacific manufacturing hubs in 2024, including Korea and India, where models such as the Hyundai Tucson and Creta both using advanced suspension layouts drive strong demand for suspension components.

North America

The demand for automotive ball joints in North America followed by Asia Pacific is driven by high production of SUVs, pickup trucks, and commercial vehicles that require robust, load-bearing ball joints. Strong manufacturing activity in the U.S. and Mexico, along with rising EV output from companies like Tesla, Ford, and GM, boosts OEM demand for durable and optimized suspension joints.

Europe

Europe ranked third, supported by its advanced automotive engineering base and high adoption of premium vehicles featuring multi-link and double-wishbone suspension systems. Growing EV production in Germany, France, and the U.K. continues to push the need for lightweight, long-life ball joints.

Rest of the World

Rest of the World (RoW), including Latin America, the Middle East, and Africa, is projected to grow steadily. Rising vehicle ownership, expansion of local assembly plants, and increasing demand for SUVs and light commercial vehicles are gradually improving ball joint consumption, although overall volumes remain smaller compared to Asia Pacific, North America, and Europe.

COMPETITIVE LANDSCAPE

Key Industry Players:

Innovation-Driven Advancements by Leading Ball Joint Manufacturers is Sustaining a Robust Market Competitiveness

The global automotive ball joint market is moderately consolidated, with established chassis system suppliers, precision component manufacturers, and regional producers competing through advancements in durability, material engineering, and OEM partnerships. Companies are prioritizing long-life ball joint designs, improved sealing technologies, and lightweight materials to meet the evolving high performance needs of SUVs, commercial vehicles, and electric models.

Leading participants such as ZF Friedrichshafen AG, MOOG (Tenneco), CTR (Central Corporation), and TRW strongly influence market direction. ZF continues to invest in enhanced suspension technologies, focusing on higher load-bearing capacity and corrosion resistance. MOOG emphasizes extended-life ball joints featuring premium dust boots and heat-treated studs to enhance steering response and component longevity. CTR remains a major supplier for global automakers, known for precision-manufactured chassis parts optimized for multi-link and double-wishbone systems.

Additional key players include Delphi Technologies (BorgWarner), Acdelco, Sankei Industry (555), and Lemförder, all of whom are expanding their product portfolios with improved coatings, optimized geometries, and EV-ready ball joints capable of handling heavier battery platforms. Many manufacturers are also increasing automation in production to improve consistency and quality control.

LIST OF KEY AUTOMOTIVE BALL JOINT COMPANIES PROFILED:

- ZF Friedrichshafen AG (Germany)

- Delphi Technologies (U.S.)

- Somic Ishikawa Inc. (Japan)

- GKN Automotive (U.K.)

- GMB Corporation (Japan)

- FRAP S.p.A. (Italy)

- Dana Incorporated (U.S.)

- Federal-Mogul (U.S.)

- Mevotech (Canada)

- ACDelco (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: SH Auto Parts announced establishment of its smart factory in Taiwan producing OEM-grade ball joints under fully-automated manufacturing and sustainable practices.

- July 2025: Cadillac’s ultra-luxury Celestiq integrated advanced sensors directly into its ball joints to monitor wheel movement and chassis behavior, highlighting a growing trend toward intelligent, high-precision suspension components in the ball joint market.

- July 2025: ZF Group transferred full ownership of its Indian steering and suspension joint venture to Somic Ishikawa, strengthening the company’s focus on ball joints and chassis components in India, one of the fastest-growing automotive manufacturing markets.

- July 2024: KYB Europe expanded its lineup with a new range of steering parts, including ball joints, designed to meet OE specifications and subjected to extensive quality testing, strengthening its position in the European suspension aftermarket.

- June 2024: DRiV (Tenneco) announced a major expansion of its Monroe Steering and Suspension range, adding 750 new part numbers, including OE-quality ball joints with induction-hardened studs and advanced anti-corrosion coatings for improved durability.

REPORT COVERAGE

The global automotive ball joint market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.4% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Vehicle Type

By Material

By Sales Channel

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.38 billion in 2025 and is projected to reach USD 4.93 billion by 2034.

In 2025, the market value stood at USD 1.85 billion.

The market is expected to exhibit a CAGR of 4.4% during the forecast period.

The SUV segment led the market by vehicle type.

Growing adoption of advanced suspension systems driving the growth for the market.

ZF Friedrichshafen AG, MOOG (Tenneco), CTR (Central Corporation), and Delphi Technologies are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us