Automotive Brake Fluid Market Size, Share, Industry Analysis, By Brake Fluid Type (DOT 3, DOT 4, DOT 5, and DOT 5.1), By Product Type (Petroleum Based and Non-petroleum Based), By Vehicle Type (Passenger Vehicles (Sedan & Hatchback and SUVs) and Commercial Vehicles (Light Duty Trucks, Medium Duty Trucks, Heavy Duty Trucks, Mini Buses, Buses & Coaches, Pickup Trucks, and Minivans), By Propulsion Type (ICE, Electric, and Hybrid), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

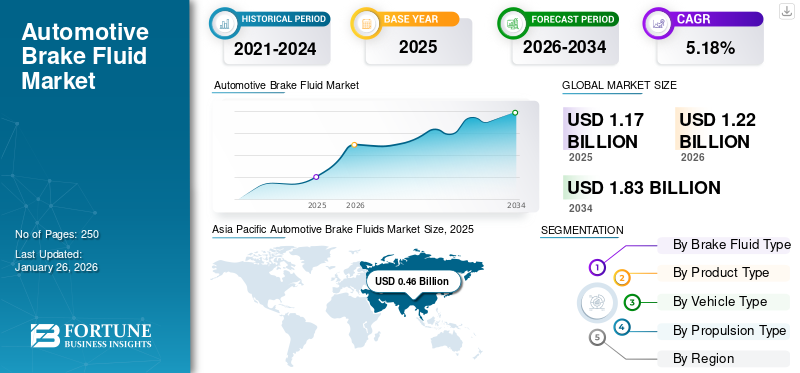

The global automotive brake fluid market size was valued at USD 1.17 billion in 2025 and is projected to grow from USD 1.22 billion in 2026 to USD 1.83 billion by 2034, exhibiting a CAGR of 5.18% during the forecast period. Asia Pacific dominated the automotive brake fluid market with a market share of 38.90% in 2025.

Automotive brake fluid plays an essential role in the automotive braking system because it transmits force from the brake pedal to the brake pad in the hydraulic system, helping the vehicle come to a halt. As modern vehicles advance toward widespread adoption of Anti Lock Braking System (ABS) and Electronic Stability Control (ESC), brake fluids have become an essential commodity for these systems. As the world transitions from conventional mechanical braking systems to advanced hydraulic braking systems, a demand for temperature-resistant, high-quality, corrosion-resistant brake fluids will rise.

Additionally, a boom in electric vehicle sales worldwide has created an opportunity since the vehicles require formulated brake fluids for regenerative braking systems.

With a growth in fluid chemistry and growing awareness among customers about effective regular vehicle maintenance, the market is expected to maintain its growth in the forecast period. Robert Bosch, Castrol Limited, etc., are some of the key players in the market. Major players in this market are capitalizing on trends by developing innovative brake fluid formulations and expanding their reach through OEM and aftermarket channels.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Global Increase in Vehicle Production to Fuel Demand for Automotive Brake Fluids

Increased global vehicle production, particularly across China, Brazil, and India, is expected to be a major driving force of the market growth. As automotive manufacturing sales grow, the demand for automotive consumables and components is also growing, which is enabling the rise in the demand for advanced brake fluids. Growing consumer awareness about regular maintenance, vehicle safety, and performance encourages timely replacement and maintenance of system components in the vehicle also supports the market growth.

Implementing strict security regulations by regulatory authorities further accentuates the market growth, such as government mandating ESC and ABS features in new vehicle models. This, in turn, has led to a high demand for high-performing brake fluids to withstand moisture absorption and high temperatures.

Additionally, the growing popularity of electric and hybrid vehicles is expected to expand the market prospects. These vehicles require specialized brake fluid to meet performance standards and drive market demand. Moreover, a robust growth of the automotive maintenance market, increased vehicle ownership, and longer vehicle lifespans are driving market growth. Advancements in fluid technology, high temperature resistance, corrosion resistance, and reduced maintenance frequency ensure a high demand for brake fluids across OEMs and aftermarket channels.

Market Restraints

Emergence of Brake-By-Wire System Limits the Market Growth

A brake-by-wire system substantially restrains the market by replacing the traditional hydraulic mechanism with electronic controls. The new system uses sensors to detect pedal inputs and sends signals to the actuator to initiate braking force. Currently, the adoption of the brake-by-wire system is limited to high-end vehicles, but the system poses a long-term threat to fluid manufacturers.

As the system gains traction, particularly in electric vehicles (EVs) and advanced driver-assistance systems (ADAS) equipped cars, the system is expected to diminish the usage of brake fluid. The demand for this system is increasing due to its advantages in weight reduction, safety, ease of operation, and system responsiveness. Major OEMs are visualizing the brake-by-wire system as an evolutionary step in electronic system integration and vehicle control because autonomous and electric vehicles are now widely adopted.

Download Free sample to learn more about this report.

Market Opportunities

Increased Focus On Environmental Sustainability Fuels the Growth Opportunities

Increased focus on environmental sustainability and increased consumer awareness are expected to be major opportunities for the automotive brake fluid market growth. Traditional glycol-ether formulation-based brake fluids are slightly on the chemically aggressive and non-biodegradable side and pose a significant environmental hazard if not disposed of properly. The disposed fluids can contaminate water sources or soil if leaked, posing a major risk and affecting the ecosystem.

In response to this problem, the manufacturers are now heavily focusing on developing eco-friendly, non-toxic, biodegradable brake fluids. From production to disposal, the consumable manufacturers are aiming to minimize their ecological footprint while maintaining quality and performance standards. Certain regulations in regions of Europe and the U.S. are accelerating the shift by imposing strict regulations on fluid disposal and harmful chemical usage.

Numerous fleet operators and ORMs are increasingly prioritizing the use of sustainable fluids to meet their ESG (Environmental, Social, and Governance) needs. This opportunity offers an advantage and widespread adoption to new entrants and early adopters, and supports a global outlook toward reducing carbon footprint and the maintenance of a circular economy.

Automotive Brake Fluid Market Trends

Advancements in Formulation and the Emergence of Synthetic Brake Fluids to Amplify Product Demand

Advancements in brake fluid formulations, particularly with the emergence of nanotechnology-enhanced fluids and subsequent synthetic fluids alternatives, are poised to impact market trends significantly. As vehicle components and technology become advanced, the traditional petroleum or glycol-based fluids are not sufficient to meet the standard, thermal, evolving safety, and longevity requirements. This, in turn, has led OEMs to invest in the demand for brake fluids and next-generation fluid formulation and design that would offer superior reliability, thermal protection, and protection under extreme operational conditions.

Nanotechnology-enhanced formula in brake fluid is being seen as a breakthrough in the automotive industry because the fluid consists of microscopic nano-particles that significantly improve the lubricity, thermal stability, and anti-corrosion properties due to the presence of metal oxides and carbon derivatives. The fluid also forms a protective layer on the braking system, reducing wear & corrosion, and enabling increasing demand for high performance in risky or heavy-duty operations. These advantages make nanofluids and synthetic brake fluids an effective option for commercial fleets, performance vehicles, EVs, and vehicles with regenerative braking systems with critical components.

SEGMENTATION ANALYSIS

By Brake Fluid Type

DOT 3 Brake Fluid Dominated the Market, Propelled By High Usage In Conventional Braking Systems

By brake fluid type, the market is divided into DOT 3, DOT 4, DOT 5, and DOT 5.1.

The DOT 3 segment is expected to lead by brake fluid type, contributing 43.14% globally in 2026 and is expected to grow significantly in the forthcoming years due to its widespread compatibility, prevalence, and affordability in the global vehicle fleet. DOT 3 fluid is the oldest and most recognized, predominantly glycol-based, extensively used brake fluid, primarily used in passenger vehicle applications. The chemical formulation offers significantly higher boiling points, effective moisture, and corrosion resistance for day-to-day driving, making it an effective choice for automotive manufacturers. One of the major growth factors is that the DOT 3 brake fluid is compatible with conventional braking systems, with and without ABS systems. Many vehicles in Asia Pacific and Latin America remain compatible with DOT 3 brake fluid, thereby fueling the market demand.

The DOT 5.1 segment is expected to grow at the highest CAGR in the forecast period. The proliferation of advanced safety features, the growing popularity of performance vehicles and EVs, and increasing demand for high-performance braking are expected to boost the growth of the DOT 5.1 segment in the forecast period. DOT 5.1 brake fluid maintains compatibility with conventional braking systems due to its glycol-based compatibility while being equally supportive to new braking systems, delivering a high boiling point compared to DOT 5 fluid. Low viscosity is a prime advantage for DOT 5.1 type of brake fluid. Low viscosity ensures quick fluid response in advanced systems including ABS, ESC, and autonomous braking systems. As global regulatory bodies are mandating these advanced systems in new vehicles, the demand for DOT 5.1 automotive brake fluid will grow in the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Product Type

Advancements in Propulsion Systems Support the Dominance of Petroleum-Based Segment Growth

By product type, the market is divided into petroleum-based and non-petroleum-based.

The petroleum-based segment is projected to reach 74.72% of the global market share in 2026. Petroleum-based brake fluid dominates the market due to specific performance benefits and compatibility with conventional braking systems. A major driver for demand for petroleum-based automotive brake fluids is their non-hygroscopic nature, which causes moisture absorption from the environment to be less than that of other brake fluids. This makes them ideal for long-term fluid stability and applications in heavy vehicles, specialty vehicles, vintage cars, etc.

High lubricity, high temperature tolerance, and low compressibility further contribute to longer life retention, anti-corrosion, and reduced wear and tear in the braking system components, making it a preferred choice for most manufacturers and fleet operators.

The non-petroleum-based segment is expected to grow at the highest CAGR in the forecast period. Non-petroleum brake fluids are usually with a glycol-ether silicone based formulation and helps absorb moisture over time and helps prevent localized water pooling in the system, which is a key safety benefit because it reduces a major risk of brake failure due to vapor lock.

The chemical properties of non-petroleum-based automotive brake fluid make it suitable for multiple vehicle types. It is also compatible with autonomous braking, ABS, and ESC, which are newly introduced braking technologies. Additionally, the market is now focusing on low-toxic formulations and sustainability in brake fluid, and low-emission, bio-derived variants are readily used to reduce carbon footprints. This, in turn, is expected to boost market growth in the forecast period.

By Vehicle Type

Passenger Vehicles Segment Led By Growing Production For Evs And Increase In Volume For Modern Passenger Vehicles

Based on vehicle type, the market is divided into passenger and commercial vehicles.

The passenger vehicle segment is projected to dominate the automotive brake fluid market by vehicle type, accounting for 78.96% of the global market share in 2026. The growth in purchasing power of individuals leads to a rise in the number of passenger vehicle deliveries, which further enables subsequent recovery of economies and stabilization of emerging markets such as Brazil, China, India, and parts of Africa, resulting in high vehicle ownership. In addition to increasing volumes, modern passenger vehicles are readily equipped with advanced safety technologies such as ADAS, ESC, and ABS that place more stringent requirements on apt brake fluid usage, thereby fueling the market demand.

A rise in EVs in passenger cars is also expected to boost market demand significantly. Electric vehicles (EVs) comprise sophisticated components and advanced braking systems that necessarily require effective braking fluid in the braking system to maintain performance and safety.

The commercial vehicles segment is expected to grow significantly in the forthcoming years. Increased demand for logistics services, last-mile delivery, goods transportation, and a major surge in e-commerce applications is expected to boost market growth. Commercial vehicles, particularly heavy-duty buses and trucks, operate under extreme conditions, involving heavy loads, long driving hours, and frequent braking. Therefore, their braking systems experience a lot more heat, stress, and high performance, making it important for them to use effective automotive brake fluids.

By Propulsion Type

ICE Segment Dominated Due to Use of Brake Fuels in Conventional Braking Systems

Based on propulsion type, the market is divided into ICE, electric, and hybrid.

The ICE segment dominated the global automotive brake fluid market in 2024. One of the major reasons for the growth in internal combustion engine (ICE) vehicles is the affordability and accessibility of these vehicles, especially in emerging markets in Asia Pacific and Africa, where EV infrastructure is still developing. ICE vehicles heavily rely on a hydraulic braking system, require regular maintenance, and therefore require periodic replacement of brake fluid as well.

Since ICE vehicles undergo challenging terrains and longer routes, a routine checkup or top-up of brake fluid is also mandatory by regulatory authorities. A large aging vehicle fleet in various parts of the world further boosts the automotive brake fluid market.

The electric segment is projected to remain significant, accounting for 44.18% of the global market share in 2026. The rapid global adoption of EVs in regions such asEurope and North America, combined with mandates to reduce vehicle emissions, is accelerating the market demand. The need for extended service intervals is a major driving factor of the electric segment. Since EVs use friction brakes comparatively less, fluids must resist moisture buildup, stagnation, and corrosion for long periods of low or minimal use. This requires high-quality DOT 4 or DOT 5.1 fluid with thermal stability and chemical compositions.

Automotive Brake Fluid Market Regional Outlook

The market is studied by region across North America, Asia Pacific, Europe, and the Rest of the World.

North America

Asia Pacific Automotive Brake Fluids Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America held 19.99% of the global market share, reaching a valuation of USD 0.23 billion, and is projected to grow to USD 0.24 billion in 2026. North America, particularly the U.S., accounts for a major part of the global fleet, leading to market growth. Safety regulations such as the FMVSS 116 and a widespread adoption of ECS/ABS systems fuel demand for advanced and high-quality automotive brake fluid. North American consumers favor performance-oriented and eco-friendly formulations, including nanotech-enhanced synthetic fluids, aligning with EVs and ADAS-based system requirements. Particularly in the U.S., the presence of major market players such as Castrol and Valvoline is a major driver. Additionally, high growth in volume of passenger car deliveries is a major reason behind the dominance of the region. It is also expected to drive market growth in the forthcoming years. The U.S. market is valued at USD 0.22 billion by 2026.

Europe

The market in Europe reached USD 0.32 billion in 2025, representing 27.27% of total market revenue, and is projected to reach USD 0.33 billion in 2026. The growth in this region is attributed to government collaboration and the need to adopt enhanced EV/hybrid vehicles to align with EU emission goals and safety standards. Automotive innovations from major regional OEMs, such as Volkswagen, BMW, and Renault, and their demand for high-quality, high-grade automotive brake fluid manufacturing. Meanwhile, Europe’s aftermarket thrives on replacement cycles with high consumer awareness, performance maintenance, and availability of regional service centers. The UK market is valued at USD 0.03 billion by 2026. The Germany market is valued at USD 0.04 billion by 2026.

Asia Pacific

The market in Europe reached USD 0.32 billion in 2025, representing 27.27% of total market revenue, and is projected to reach USD 0.33 billion in 2026. During the forecast period, the Asia Pacific region will witness the highest CAGR in the market. The market growth is dominated by China, the region's largest producer of passenger and commercial vehicles. India is also set to grow with exponential growth and production capacity in the forthcoming years. Increasing vehicle ownership in the region, high spending on consumables, and consumer awareness about regular vehicle maintenance are expected to propel the market growth further. The Japan market is valued at USD 0.06 billion by 2026. The China market is valued at USD 0.26 billion by 2026. The India market is valued at USD 0.04 billion by 2026.

Rest of the World

The Rest of the World market accounted for USD 0.16 billion in 2025, representing 13.85% of the global industry, and is expected to reach USD 0.17 billion in 2026. The rest of the world is anticipated to witness moderate growth during the forecast period. Latin American governments are implementing regulatory regimes to improve vehicle safety and control emissions. Expansion of support and accessible maintenance is expected to grow the market for automotive brake fluid in the region. GCC countries such as the UAE and Saudi Arabia are major supporters and exporters of luxury vehicles that demand high-end automotive brake fluid, thereby growing market demand.

Competitive Landscape

Key Market Players

Leading Players are Focusing on High Regional Penetration and Distribution to Sustain Market Share

The automotive brake fluid market is highly competitive, comprising a mix of global chemical conglomerates, regional manufacturers, and automotive OEM suppliers. Consumers choose automotive brake fluid companies based on product innovation, regulatory compliance, brand reliability, and distribution reach. Leading players in the market are expected to maintain dominance over the forecast period owing to innovation, mergers, acquisitions, strategic partnerships, and eco-certifications. Local and regional market players may compete via affordability and effective regional distribution.

LIST OF KEY AUTOMOTIVE BRAKE FLUID COMPANIES PROFILED

- Castrol Limited (U.K.)

- Valvoline Inc. (U.S.)

- Hindustan Petroleum (India)

- Robert Bosch GmbH (Germany)

- DuPoint (U.S.)

- Gars Lubricants (India)

- Pakelo Lubricants S.p.a (Italy)

- Prestone Products Corporation (U.S.)

- Motul S.A. (France)

- Champion Oil (U.S.)

- Motorcraft (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025- AO Racing, a major IMSA WeatherTech SportsCar Championship team, unveiled a partnership with Halo-Orthene, a prominent brake fluid OEM. This partnership has already proven its mettle, since AO Racing bagged a historic win at the GTD PRO category at the Twelve Hours of Sebring, utilizing Halo’s advanced Halo P1 brake fluid.

- April 2025-Third Coast Chemicals, a leading global manufacturer and supplier of aftermarket automotive brake fluids, unveiled an addition of DOT 5.1 brake fluid to their expanding product line. DOT 5.1 is launched with an advanced formulation, engineered to meet the demands of high-performance with advanced braking systems, providing higher reliability for modern passenger and commercial vehicles.

- February 2025- PREMA Racing partnered with Halo By Orthene for the 2025 racing season. This partnership is expected to see the company’s prominent brake fluid technology integrated into PREMA’s high-performance fleet in motorsport.

- March 2024- BASF unveiled a new facility on a methyl glycol (MG) plant in China. The new facility is designed with a high annual capacity of over 45,000 metric tons. It aims to meet the rapidly rising demand for brake fluids in the region and is scheduled to start operations by the end of 2025.

- December 2022- A Hinduja Group company, Gulf Oil Lubricants India Ltd., announced an extensive partnership with Altigreen to provide them with EV Fluids such as brake and gear oils. Gulf can manufacture customized EV fluids through this partnership for commercial electric vehicle maker Altigreen.

REPORT COVERAGE

The report provides a detailed market analysis and focuses on important aspects across various countries, such as key players, products, applications, and platforms. Moreover, it offers deep insights into the market trends, competitive landscape, market competition, pricing of automotive brake fluids, and market status, highlighting key industry developments. In addition, it encompasses several direct and indirect factors that have contributed to the expansion of the global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.18% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

By Segmentation

|

By Brake Fluid Type

|

|

By Product Type

|

|

|

By Vehicle Type

|

|

|

By Propulsion Type

|

|

|

By Region

|

Frequently Asked Questions

According to the Fortune Business Insights study, the global market size is projected to grow from USD 1.22 billion in 2026 to USD 1.83 billion by 2034

The market will likely grow at a CAGR of 5.18% during the forecast period (2026-2034).

The top players in the industry are Castrol Limited (U.K.), Valvoline Inc. (U.S.), Hindustan Petroleum (India), and Robert Bosch GmbH (Germany).

Asia Pacific dominated the global automotive brake fluid market.

The growth in purchasing power of individuals and the rise in the number of passenger vehicle deliveries are key factors driving segment growth.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us