Automotive Hydraulic Brake Systems Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, LCV, and HCV), By Propulsion Type (IC Engine and Electric), By Technology (Anti-locking Braking System (ABS), Electronic Stability Control (ESC), Traction Control System (TCS), and Electronic Brakeforce Distribution (EBD)), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

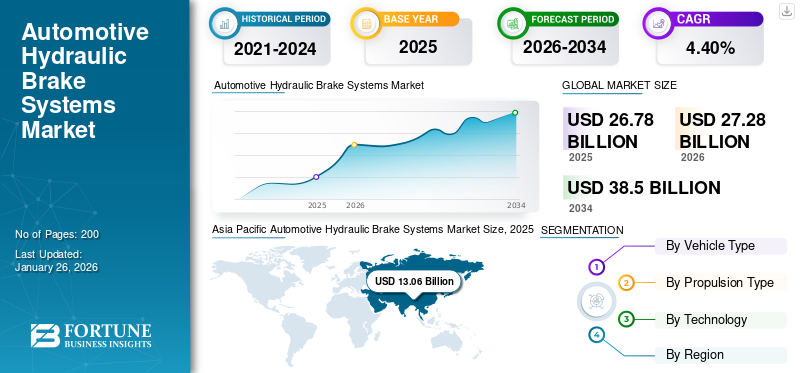

The global automotive hydraulic brake systems market size was valued at USD 26.78 billion in 2025. The market is projected to grow from USD 27.28 billion in 2026 to USD 38.50 billion by 2034, exhibiting a CAGR of 4.40% during the forecast period. Asia Pacific dominated the global market with a share of 48.76% in 2025.

Automotive hydraulic brake systems are braking mechanisms that use brake fluid to transmit force from the brake pedal to the braking components, such as calipers or drums. Based on Pascal's law, the system ensures equal pressure distribution through a closed hydraulic circuit, providing efficient and reliable braking. The system typically includes a master cylinder, brake lines, calipers, rotors (or drums), and brake pads or shoes. Hydraulic brakes are widely used in passenger cars, light commercial vehicles, and some heavy vehicles due to their responsiveness, ease of maintenance, and ability to generate high braking forces.

The automotive hydraulic brake systems market is driven by the increasing demand for advanced braking technologies in passenger and commercial vehicles. Hydraulic brakes are preferred for their efficiency, smooth operation, and compatibility with modern safety systems, anti-lock braking systems, and Electronic Stability Control (ESC). The market is witnessing growth due to advancements in brake materials, integration with electric and hybrid vehicles, and stringent safety regulations worldwide. Additionally, the rise of autonomous driving technologies has led to increased adoption of hydraulic systems compatible with Advanced Driver Assistance Systems (ADAS). Geographically, Asia Pacific dominates the market due to high vehicle production and sales in China and India.

The COVID-19 pandemic disrupted the global automotive supply chain, leading to production halts and reduced demand for vehicles. This significantly impacted the hydraulic brake systems market as OEMs scaled back manufacturing operations. However, the market has rebounded with the recovery of the automotive industry post-pandemic. The focus on Electric Vehicles (EVs) has accelerated innovation in hydraulic braking systems tailored for EV platforms. Current trends show increased adoption of regenerative braking integration with hydraulic systems in EVs and hybrids. Furthermore, rising consumer preference for safer vehicles and government mandates for advanced braking technologies have revitalized demand. Despite supply chain challenges, including semiconductor shortages, the market is stabilizing with a focus on sustainability and technological advancements.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Automotive Hydraulic Brake Systems Market Trends

Rapid Technological Advancements in the Product are Trending in the Market

One of the major ongoing trends in the automotive hydraulic brake systems market analysis is the integration of ADAS with hydraulic brakes. This trend is driven by stringent safety regulations and consumer demand for enhanced vehicle safety. For instance, the European Union has mandated that all new vehicles sold in the EU after 2024 must be equipped with collision-detection emergency global automotive braking systems and lane-keeping assist technologies, which require responsive hydraulic braking systems. Additionally, the growth of Electric Vehicles (EVs) is influencing the market. EVs often incorporate regenerative braking systems and brake-by-wire systems that work in conjunction with hydraulic brakes to improve energy efficiency.

The market is also witnessing a shift toward lightweight materials for brake components to enhance fuel efficiency and reduce emissions. This trend is supported by the increasing adoption of smart braking solutions like brake-by-wire technology and Autonomous Emergency Braking (AEB), which enhance vehicle safety and efficiency. Major players such as Bosch, Continental, and ZF Friedrichshafen are investing heavily in R&D to improve hydraulic brake systems, contributing to market growth significantly.

MARKET DYNAMICS

Market Drivers

Growing Demand for Enhanced Safety Vehicles Drive Market Growth

One major driving factor for the global automotive hydraulic brake systems market share is the increasing demand for enhanced vehicle safety, driven by stringent government regulations and consumer awareness. Governments worldwide are implementing stricter safety standards, mandating the use of advanced braking technologies such as Anti-lock Braking Systems (ABS), Electronic Stability Control (ESC), and Automatic Emergency Braking (AEB). This regulatory push is driving innovation in hydraulic brake systems, with manufacturers such as Bosch, Continental, and ZF Friedrichshafen investing heavily in R&D to meet these standards. Additionally, the growth of Electric Vehicles (EVs) is also influencing the market, as EVs often integrate regenerative brakes with hydraulic brakes to improve energy efficiency. As a result, the market is witnessing a significant shift toward advanced hydraulic brake systems that can seamlessly integrate with modern safety technologies.

Market Restraints

Regulatory Environment to Monitor Shift toward Electric Vehicles (EVs) is a Critical Factor that Affects Market Growth

One crucial restraining factor for the global automotive hydraulic brake systems market growth is the ongoing shift toward Electric Vehicles (EVs) and autonomous driving technologies, which are increasingly adopting alternative braking systems such as regenerative braking. While hydraulic brakes remain essential for many vehicle types, the integration of regenerative braking in EVs reduces the reliance on traditional hydraulic systems for braking. This shift is driven by the need for energy efficiency and reduced emissions in EVs, which can potentially decrease the demand for conventional hydraulic brake components over time.

Additionally, supply chain disruptions, including semiconductor shortages and localized production challenges, have affected the production and availability of hydraulic brake systems. These disruptions can lead to delays and increased costs, further restraining market growth. For instance, the automotive industry has faced significant challenges due to global supply chain issues, which have affected the production of vehicles and their components, including hydraulic brake systems. Moreover, the trend toward electrification and autonomous vehicles is driving innovation in braking technologies, which may gradually reduce the dominance of hydraulic systems in certain vehicle segments.

Market Opportunities

Rising Demand for Hybrid Braking Solutions and Regulatory Mandates for Advanced Safety Systems, Particularly in Commercial Vehicles

With increasing adoption of electric and hybrid vehicles, manufacturers are integrating hydraulic brakes with regenerative braking systems to enhance efficiency and meet emission norms. For instance, Bosch and Continental are developing electro-hydraulic brake-by-wire systems that combine hydraulic precision with electronic control, improving responsiveness and energy recovery. Technological advancements such as lightweight hydraulic components (e.g., aluminum master cylinders) reduce vehicle weight, boosting fuel efficiency. ZF Friedrichshafen has introduced modular hydraulic actuators for autonomous trucks, enabling precise braking in self-driving scenarios.

Additionally, regulatory mandates such as the EU’s Euro 7 norms and NHTSA’s FMVSS No. 127 (requiring automatic emergency braking by 2029) are driving demand for reliable hydraulic systems in conjunction with ADAS. Hybrid hydraulic-electric systems are gaining traction in buses and trucks, with companies like Knorr-Bremse launching next-gen ABS for commercial vehicles. Government policies, such as UNECE’s enhanced AEB standards for trucks (effective 2023), further solidify hydraulic brakes’ role in safety-critical applications. These trends position hydraulic systems as indispensable in the evolving automotive landscape.

Segmentation Analysis

By Vehicle Type

Rising Disposable Incomes and Urbanization to Contribute to Rising Adoption of SUVs

The global market is segmented by vehicle type into hatchback/sedan, SUVs, LCV (Light Commercial Vehicles), and HCV (Heavy Commercial Vehicles).

The dominance of the SUV segment is supported by rising disposable incomes and urbanization, particularly in Asia Pacific and Latin America. For instance, China's vehicle production increased by 12% in 2023, with a significant portion being SUVs. The SUV segment is rapidly gaining traction due to increased consumer preference for SUVs, driven by their versatility and comfort.

The hatchback/sedan segment traditionally holds a significant share due to the high volume of passenger vehicles produced globally.

The LCV and HCV segments are growing, especially in regions with expanding logistics and transportation sectors. Safety regulations and the need for efficient braking solutions in commercial vehicles drive the demand for advanced braking systems in these segments. LCVs and HCVs are crucial for commercial transportation, and their demand is rising due to economic activities and infrastructure development. The growth in these segments supports the overall market by increasing the demand for robust and reliable hydraulic brake systems. For example, in 2023, the U.K. witnessed an 18.5% increase in commercial vehicle production, highlighting the potential for brake system demand.

By Propulsion Type

IC Engine Segment to Dominate Due to Strong Established Fueling Infrastructure

The market is segmented by propulsion type into IC engine and electric.

The IC engine segment has dominated due to its widespread use in vehicles. IC engines remain prevalent in vehicles, but electronic systems such as ABS and ESC optimize hydraulic brake efficiency, ensuring compliance with safety standards and improving responsiveness. This synergy supports hydraulic brake relevance despite the rise of electro-mechanical alternatives.

The electric segment is rapidly growing as Electric Vehicles (EVs) become more popular, driven by environmental regulations and consumer preference for sustainable options. EVs often integrate advanced braking technologies such as regenerative braking, which enhances efficiency and safety. For instance, the global automotive brake system market is expected to expand significantly by 2035, partly due to the growth in EVs and autonomous driving technologies. The development of the electric segment contributes to the overall market by driving innovation in braking systems, such as brake-by-wire technology and Autonomous Emergency Braking (AEB), which improve vehicle safety and efficiency.

By Technology

Widely Adopted Anti-Lock Braking Systems (ABS), in Modern Vehicles Dominate Market

The market is segmented by technology into Anti-locking Braking System (ABS), Electronic Stability Control (ESC), Traction Control System (TCS), and Electronic Brakeforce Distribution (EBD).

ABS remains the dominant segment, widely adopted in modern vehicles to prevent wheel lockup during braking. Its prevalence is driven by mandatory safety regulations (e.g., EU’s General Safety Regulation, NHTSA standards) and high consumer demand for accident prevention. Recent advancements include integrated ABS modules with predictive algorithms for adaptive braking, as witnessed in Bosch’s ABS 10.3 for motorcycles and passenger vehicles. ABS accounts for around 30% of braking system revenue, per industry reports, with Asia Pacific leading in adoption due to rising vehicle production.

ESC is the fastest-growing segment, driven by regulations such as UN R140 mandating ESC in new vehicles. Innovations such as torque vectoring integration (e.g., ZF’s ReAX steering systems) enhance ESC’s role in autonomous and electric vehicles. ESC’s ability to prevent skidding through selective wheel braking makes it critical for SUVs and commercial vehicles.

TCS is gaining traction in off-road and luxury vehicles to manage wheel spin. Magna’s ActiveTC uses hydraulic pressure modulation for real-time slip control. Growth is bolstered by EV adoption, where TCS manages high torque delivery without traditional drivetrain components. EBD optimizes brake force between axles, improving safety in loaded vehicles.

Continental’s MK C2 brake-by-wire system integrates EBD with regenerative braking, reducing hydraulic reliance. EBD is increasingly paired with ADAS features such as automatic emergency braking.

AUTOMOTIVE HYDRAULIC BRAKE SYSTEMS MARKET REGIONAL OUTLOOK

Asia Pacific Automotive Hydraulic Brake Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Technological Advancements to Drive Asia Pacific Market Growth

The global automotive hydraulic brake systems market is segmented into North America, Europe, Asia Pacific, and the rest of the world. Each region contributes uniquely to the market's growth, driven by factors such as vehicle production, regulatory environments, and consumer demand.

Asia Pacific

The Asia Pacific region captured 48.76% of the global market in 2025, generating USD 13.06 billion in revenue, and is projected to reach USD 13.24 billion in 2026. Asia Pacific is the dominating and fastest-growing region in the global automotive hydraulic brake systems market. This dominance is attributed to the rapid growth in vehicle production and sales in China, India, and Indonesia. China alone accounted for over 50% of the revenue share in the Asia Pacific region in 2023, driven by a 12% increase in vehicle production compared to the previous year. The increasing disposable income and urbanization in these countries have fueled the demand for passenger and commercial vehicles, thereby boosting the demand for hydraulic brake systems. For instance, India's vehicle production grew by 7% in 2023, reaching 5.85 million vehicles.

Europe

In 2025, the Europe market stood at USD 3.45 billion, representing 12.87% of global demand, and is projected to grow to USD 3.55 billion in 2026. Europe is another significant market for automotive hydraulic brake systems, driven by stringent safety regulations and a strong focus on vehicle safety. European countries have implemented rigorous standards for vehicle safety, which has compelled manufacturers to adopt advanced hydraulic brake technologies such as ABS and EBD. This regulatory environment supports the growth of the market by ensuring that vehicles meet high safety standards, contributing to the overall global market growth.

North America

North America contributed approximately USD 8.07 billion to the global market in 2025, accounting for 30.12% share, and is expected to reach USD 8.26 billion in 2026. North America also plays a crucial role in the market, with the U.S. being a major contributor. The region benefits from a well-established automotive industry and a strong demand for both passenger and commercial vehicles. The growth in this region is supported by the Traffic Safety Administration NHTSA's ongoing advancements in braking technologies and the integration of Advanced Driver Assistance Systems (ADAS) into vehicles.

Latin America, Africa, and the Middle East

The rest of the world includes regions such as Latin America, Africa, and the Middle East. While these regions contribute less to the global market compared to others, they are experiencing growth due to increasing vehicle sales and infrastructure development. The rising demand for vehicles in these regions is expected to drive the adoption of hydraulic brake systems, contributing to the overall market expansion.

Rest of the World

In 2025, Rest of the World represented USD 2.21 billion, accounting for 8.25% of the worldwide market, and is projected to grow to USD 2.23 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Robert Bosch GmbH to Emerge as One of Leading Market Players Due to its Technological Advancements and Presence

Robert Bosch GmbH is the top leading major market player in the global market. The company dominates due to its extensive experience, advanced technologically, and strong global presence. Its dominance is attributed to its comprehensive portfolio of automotive hydraulic brake systems, including advanced technologies such as ABS and EBD. These systems enhance vehicle safety and comply with stringent regulatory standards. Bosch's commitment to innovation and customer-centric strategies further solidifies its position. For instance, Bosch has been investing heavily in research and development to improve brake system efficiency and safety, aligning with global trends toward enhanced vehicle safety and sustainability.

Continental AG is the second major leading market player in the market. The company's strong position is due to its advanced braking technologies and strategic partnerships with major automotive manufacturers. Continental's product portfolio includes a range of hydraulic brake components and systems designed to meet high safety standards. The company's focus on innovation, particularly in electric and autonomous vehicle technologies, supports its growth in the market. Continental's global reach and commitment to customer satisfaction also contribute to its success. For example, Continental has been expanding its operations in regions such as Asia Pacific to capitalize on growing vehicle production and demand for advanced brake systems.

LIST OF KEY AUTOMOTIVE HYDRAULIC BRAKE SYSTEMS COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- ZF Friedrichshafen AG (Germany)

- Continental AG (Germany)

- Aisin Seiki Co., Ltd. (Japan)

- Brembo S.p.A. (Italy)

- Hitachi Astemo, Ltd. (Japan)

- Delphi Technologies (U.K.)

- Akebono Brake Industry Co., Ltd. (Japan)

- Mando Corporation (South Korea)

- Nissin Kogyo Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- February 2025 - Bosch successfully tested its new hydraulic brake-by-wire system on public roads, covering over 3,300 kilometers across different climate zones to the Arctic Circle. The system eliminates mechanical connections between the brake pedal and brake system, enhancing safety and efficiency.

- January 2025 - ZF has achieved a significant milestone in the automotive industry, securing a major contract with a global OEM to supply its innovative brake-by-wire technology. This partnership highlights the company’s Electro-Mechanical Brake (EMB) system, which is integrated with traditional components and offers a hybrid braking solution that combines electric and hydraulic systems.

- January 2025 - Automotive product manufacturer ADVIK has completed the acquisition of Powersports MTG, a German motorcycle mechanical and hydraulic braking system and clutch system manufacturer. The acquisition, completed via ADVIK's Singapore subsidiary, will enhance its hold on premium motorcycle safety components. Through its next-gen advanced braking technology, ADVIK will offer hydraulic braking and clutch systems to global markets.

- November 2023 - ZF pioneered an electric brake-by-wire system for forthcoming software-defined vehicles. This advanced Brake System eliminates the necessity for brake fluid while also enabling the possibility of combining electric and hydraulic brake systems. Developed across ZF's research and development hubs in China, the U.S., and Germany, this innovative brake system targets the global market.

- October 2021 - Brembo goes brake-by-wire and eliminates hoses with a new Sensify system. The Sensify system removes nearly all the hydraulic components from the brake system, leaving no physical connection between the pedal and the discs, and it has its digital brains capable of using Artificial Intelligence (AI) to determine the correct amount of braking for each wheel under a range of different circumstances.

REPORT COVERAGE

The global automotive hydraulic brake systems market research report provides a detailed market analysis and focuses on key aspects such as leading companies, vehicle types, design, and technology. Besides this, the report offers insights into the latest market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.40% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type

By Propulsion Type

By Technology

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market is projected to reach USD 38.50 billion by 2034.

The market is expected to register a CAGR of 4.40% during the forecast period of 2026-2034.

The need for enhanced safety efficient vehicles is driving the market growth.

Asia Pacific led the market in 2025 and is also estimated to depict the fastest growth rate.

Robert Bosch GmbH, ZF Friedrichshafen AG, Continental AG, Aisin Seiki Co., Ltd. and Brembo S.p.A. are some of the major shareholders.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us