Automotive Bushing Market Size, Share & Industry Analysis, By Application (Suspension, Engine, Chassis, Interior, Exhaust, and Transmission), By Vehicle Type (Passenger cars (Hatchback/Sedan, and SUVs), and Commercial Vehicles (LCV (Light Commercial Vehicles), Heavy Trucks, Buses & Coaches and Others)), By Material (Rubber, Polyurethane, Brass, Aluminum, Bronze, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

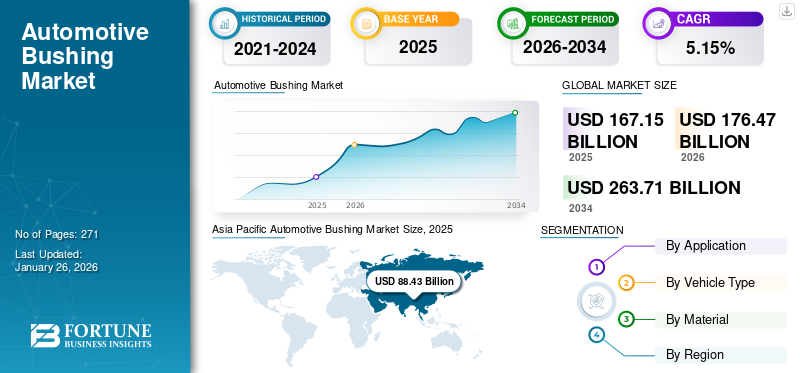

The global automotive bushing market size was valued at USD 167.15 billion in 2025 and is projected to grow from USD 176.47 billion in 2026 to USD 263.71 billion by 2034, exhibiting a CAGR of 5.15% during the forecast period. Asia Pacific dominated the global market with a share of 52.90% in 2025.

Automotive bushes, also known as bushings, are rubber or polyurethane components that connect moving parts of a vehicle's suspension and steering to the chassis. They act as a cushion or isolator, reducing vibrations, noise, and harshness while improving ride comfort and handling.

The market is a vibrant and growing sector, fueled by increasing vehicle production, technological advancement in automotive technology, and consumer demand for smoother and quieter rides. Bushings, which act as cushions between moving parts, are crucial for reducing noise, vibration, and harshness (NVH), improving ride comfort, and enhancing vehicle stability.

Numerous key players, including Continental AG, ZF, Sumitomo Riko Co., Ltd., and Vibracoustic GmbH, dominate the market share. Other significant players in the market are BOGE Rubber & Plastics, Delphi Technologies, and DuPont de Nemours, Inc. These companies focus on innovation, strategic partnerships, and mergers & acquisitions to strengthen their market positions, particularly in advanced polyurethane bushings.

The COVID-19 pandemic had a profound and multifaceted impact on the global market, as it disrupted the supply chains, production, and demand dynamics. While the industry has largely recovered, the pandemic's effects continue to shape market trends, including supply chain restructuring, material shortages, and accelerated adoption of advanced bushing technologies. The pandemic accelerated digital transformation in the automotive sector, with a growing emphasis on predictive maintenance solutions. Sensor-equipped smart bushings, which monitor wear and tear in real time, gained traction as fleet operators sought to minimize downtime and maintenance costs. Companies, including Continental and Bosch, integrated IoT-enabled bushings that transmit data to cloud platforms, allowing for proactive component replacements.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Automotive Bushing Market Trends

Emergence of Smart Sensor-Integrated Bushings is a Dominant Trend in the Market

A transformative trend reshaping the automotive bushing market growth is the integration of smart technologies and sensors into bushing systems, driven by the automotive industry's shift toward connected, autonomous, and electric vehicles (EVs). Traditional bushings—passive components designed to dampen noise and vibration—are evolving into active, data-driven systems capable of real-time performance optimization. This shift is fueled by growing demand for enhanced vehicle safety, predictive maintenance, and personalized driving experiences, positioning sensor-equipped bushings as critical enablers of next-generation mobility. Leading suppliers and automakers are investing heavily in R&D to capitalize on this trend, with recent innovations highlighting the fusion of material science IoT.

The integration of sensors and electronic control units (ECUs) into bushings marks a paradigm shift. These "smart bushings" monitor variables such as vibration frequency, temperature, load stress, and road conditions, transmitting data to vehicle control systems to dynamically adjust suspension stiffness, stability, and ride comfort. For instance, in March 2024, Continental AG's Vibracoustic division launched its Active Bush technology, which uses embedded accelerometers and strain gauges to detect road imperfections. The system communicates with the vehicle's ECU to instantly modify bushing stiffness, reducing cabin vibrations by up to 50% in EVs. Similarly, in February 2024, Tenneco's Smart Bushing Platform was introduced to employ machine learning algorithms to predict component wear, enabling proactive maintenance and extending the bushing lifespan by 30%. Such innovations are critical for autonomous vehicles (AVs), where consistent ride quality and sensor stability are non-negotiable.

The rapid adoption of EVs and AVs is accelerating this trend. EVs, with their quiet powertrains, amplify the perceptibility of road noise, necessitating bushings that actively counteract disturbances. Tesla's Cyber truck, released in late 2023, features sensor-laden bushings in its adaptive air suspension system, which uses real-time data to adjust damping forces based on payload and terrain. Meanwhile, AVs require ultra-precise vibration control to ensure the reliability of onboard sensors. In April 2024, Aptiv PLC collaborated with ZF Friedrichshafen to develop AI-driven Bushings for AVs, which use vibration data to map road surfaces and optimize path-planning algorithms.

MARKET DYNAMICS

Market Drivers

Rise of Advanced Suspension Systems and Vehicle Comfort Enhances the Bushings Demand

The global market is experiencing significant growth due to the increasing demand for advanced suspension systems that enhance ride comfort, handling precision, and overall vehicle performance. As consumers become more discerning about driving experiences and automakers prioritize cabin refinement, the role of bushings in noise, vibration, and harshness (NVH) reduction has been crucial. This trend is particularly evident in the luxury vehicle segment, where brands such as Mercedes-Benz, BMW, and Audi are pushing the boundaries of suspension technology. However, it's also trickling down to mass-market vehicles as comfort becomes a key differentiator in competitive markets.

Modern suspension systems are evolving rapidly, with multi-link setups, adaptive dampers, and air suspension becoming increasingly common, even in mid-range vehicles. These sophisticated systems place new demands on bushings, requiring them to provide not just vibration isolation but also precise control of wheel movement. For instance, the latest BMW 7 Series features an active role stabilization system that relies on specially designed hydraulic bushings capable of adjusting their stiffness in milliseconds. According to BMW's 2023 technical bulletin, these "active comfort bushings" reduce body roll by up to 60% while improving ride comfort over rough surfaces. Similarly, Mercedes-Benz's E-Active Body Control system, introduced in the 2024 E-Class, uses sensor-equipped bushings that communicate with the suspension computer 1,000 times per second to optimize the ride quality. These numbers underscore this technological shift.

A 2023 report by IHS Markit revealed that 42% of new vehicles sold in North America and Europe now feature some form of advanced suspension system, up from 28% in 2018. This percentage is projected to reach 58% by 2028, driven largely by consumer demand for superior ride comfort. The same report estimates that vehicles with these advanced systems use 15-20% more bushings than conventional suspensions, and these bushings are typically 30-50% more expensive due to their specialized designs and materials.

Market Restraints

Volatility in Raw Material Prices and Supply Chain Disruptions to Hamper the Market Growth

A critical restraining factor that reduce automotive bushing market size is the ongoing volatility in raw material prices, compounded by supply chain disruptions, which have intensified production costs and operational uncertainties. Automotive bushings, predominantly made from natural rubber, polyurethane, or synthetic rubber, are heavily reliant on commodity markets and global logistics networks. Recent geopolitical tensions, climate-related challenges, and post-pandemic economic shifts have aggravated price fluctuations and supply instability, directly impacting manufacturers' profitability and capacity to meet the growing demand.

Natural rubber, a primary material for bushings, has experienced significant price surges due to constrained supply from major producers such as Thailand, Indonesia, and Vietnam. In March 2023, Rubber News reported a 30% year-on-year increase in natural rubber prices, driven by adverse weather conditions, labor shortages, and rising fertilizer costs. For instance, Thailand, responsible for 35% of global natural rubber output, faced prolonged monsoon rains in 2022–2023, reducing latex yields. Simultaneously, Indonesia contended with deforestation policies limiting plantation expansion. Synthetic rubber, an alternative derived from petroleum, is similarly vulnerable. Crude oil price instability, influenced by the Russia-Ukraine conflict and OPEC+ production cuts, has kept synthetic rubber costs elevated. This dual dependency on natural and synthetic rubber leaves bushing manufacturers with limited flexibility, as substitution or inventory hedging strategies are costly and logistically complex.

Geopolitical disruptions have further fragmented the supply chains. The Russia-Ukraine war, for example, disrupted shipments of critical chemicals such as carbon black used in rubber reinforcement and hindered logistics routes through Eastern Europe. A February 2023 Supply Chain Dive analysis highlighted that 40% of European automotive suppliers faced delays in raw material deliveries, extending lead times for components such as bushings by 20–30 days. Similarly, U.S.-China trade tensions continue to reverberate, thus hampering the market growth.

Market Opportunities

Integration of Smart Bushings with IoT and Sensor Technology can be a Transformative Opportunity for the Market

The market is poised for significant growth, driven not only by the rise of electric vehicles (EVs) but also by the integration of advanced technologies such as the Internet of Things (IoT) and sensor systems into traditional automotive components. The most transformative opportunities lie in the development of smart bushings, innovative components embedded with sensors to enable real-time monitoring of wear, vibration, and performance. These intelligent bushings align with the automotive industry's shift toward connected, autonomous, and predictive maintenance solutions, offering enhanced durability, cost efficiency, and performance optimization.

Recent advancements in sensor technology and IoT connectivity have enabled automotive suppliers to reimagine bushings as "smart" components. For instance, in April 2024, Continental AG unveiled a breakthrough in bushing technology with its ActiveVibe Bushings, which integrate micro-sensors to monitor stress, temperature, and degradation in real-time. These sensors transmit data to vehicle control systems, enabling predictive maintenance alerts and optimizing suspension performance dynamically. Continental emphasized that such technology reduces unplanned downtime by up to 30% in commercial fleets, addressing a critical pain point for logistics and ride-hailing services.

In March 2024, ZF Friedrichshafen announced its Next-Generation Intelligent Bushings, designed explicitly for autonomous vehicles. These bushings use advanced elastomers and composite materials to minimize noise, vibration, and harshness (NVH), while embedded sensors provide feedback to autonomous driving systems to enhance ride comfort and stability. ZF highlighted that their bushings improve the accuracy of LiDAR and camera systems by reducing vibrations that could distort sensor data, a critical factor for the safety and reliability of self-driving cars.

Segmentation Analysis

By Application

Surging Demand for Luxury and Lightweight Vehicles to Fuel the Adoption of Suspension Bushing

By application, the market is segmented into suspension engine, chassis, interior exhaust, and transmission.

The suspension segment is expected to hold the highest share of 41.10% in 2026 and is also the fastest-growing segment. The suspension segment is experiencing significant growth due to the increasing demand for enhanced ride comfort and vehicle stability. Modern vehicles, especially electric and luxury cars, require advanced suspension systems to manage the unique weight distribution and torque characteristics. For instance, in June 2024, Bosch Automotive Service Solutions introduced new tool kits designed for the efficient removal and installation of heavy-duty suspension bushings, highlighting the industry's focus on improving suspension maintenance and performance.

The suspension segment is followed by transmission. The increasing complexity of modern transmissions, coupled with the demand for smoother driving experiences, has driven the need for advanced transmission bushings. The demand for bushings which can handle higher loads and stress associated with new vehicle technologies, including advanced transmissions, is fueling the growth of the segment.

All other segments have considerable growth. Engine bushings isolate engine vibrations from the chassis and passenger compartment, contributing to NVH (Noise, Vibration, and Harshness) reduction. Durable bushings that can withstand high temperatures and pressures in the engine compartment are significant.

Chassis bushings connect the suspension to the vehicle body, improving handling and stability. They are essential for providing a robust chassis structure, especially in vehicles with electric powertrains.

Interior bushings are crucial for passenger comfort, absorbing noise and vibration within the cabin.

Exhaust bushings help isolate exhaust system vibrations, ensuring smooth operation and minimizing noise.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Increasing Demand, Rising Disposable Incomes, and Urbanization Enhanced the Adoption of SUVs

The market is segmented by vehicle type into passenger cars (Hatchback/Sedan, SUVs) and commercial vehicles (LCV (Light Commercial Vehicles), heavy trucks, buses & coaches, and others).

The passenger cars segment is expected to dominate the market share of 63.22%in 2026, due to the high demand for passenger vehicles globally and the increasing integration of bushings for NVH reduction, leading to a smoother and more comfortable ride. The demand for bushings in hatchbacks and sedans is rising due to increased consumer expectations for comfort and noise reduction. Hatchback and sedan vehicles prioritize comfort, fuel efficiency, and affordability, necessitating high-quality bushings to reduce noise, vibration, and harshness (NVH). The integration of advanced bushing materials, such as polyurethane and composites, enhances ride quality and extends component lifespan.

- For instance, in January 2024, Renault SA announced the launch of five new passenger cars in India, including C SUV, B+ SUV, and electric vehicles, integrating high-performance automotive bushings to meet the increasing comfort standards.

SUVs, known for their off-road capabilities and heavier structures, require robust bushing solutions to handle increased loads and stresses. The growing popularity of SUVs globally has led to a surge in demand for specialized bushings that can withstand these conditions. The SUV segment's fastest growth contributes to the overall market expansion by enabling advancements in bushing technology to meet the demands of heavier and more performance-oriented vehicles.

The commercial vehicle segment is expected to experience substantial growth, driven by increasing manufacturing and sales, especially in the LCV and heavy truck sectors. LCVs, such as vans and pickup trucks, are used for a variety of transportation needs and require bushings for durability and longevity, especially in crucial conditions. Heavy-duty trucks require robust bushings to withstand heavy loads and rough terrains, contributing to a significant portion of the demand in this segment. Buses and coaches require bushings for passenger comfort and stability, especially during long-distance travel. This category includes specialized vehicles including military vehicles and other niche applications where bushings play a significant role. The trend toward electric vehicles (EVs) and hybrid vehicles is also influencing the bushing market, as these vehicles require different bushing materials and designs to optimize performance and NVH.

By Material

Significant Vibration-Damping Properties and Cost-Effectiveness Contributes to the Segmental Growth of Rubber

The market, by material, is segmented into rubber, polyurethane, brass, aluminum, bronze, and others.

Rubber segment is projected to hold the highest share of 62.59% in 2026. Rubber remains a dominantly used material for bushings due to its excellent vibration-damping properties and cost-effectiveness. However, advancements in rubber technology are leading to the development of high-damping rubber components.

- For example, in February 2024, Sumitomo Rubber Industries announced a USD 50 million investment to increase the production of high-damping rubber components at their facilities in Thailand, addressing the growing need for vibration control in the automotive industry within Asia Pacific region.

Polyurethane bushings are expected to grow at a higher CAGR during the forecast period as they offer superior durability, resistance to chemicals, and better performance under load compared to rubber. They are growingly used in performance and heavy-duty applications. Manufacturers, including Vibracoustic are offering steering column bushings made of polyurethane to help reduce vibrations and allow drivers a more secure and comfortable driving experience.

Aluminum bushings are experiencing significant growth as they are lightweight and offer good corrosion resistance, making them suitable for applications where weight reduction is crucial. The automotive industry's focus on fuel efficiency and emission reduction is encouraging the adoption of aluminum bushings in vehicle manufacturing. Brass, bronze, and other segments have considerable growth in the market.

AUTOMOTIVE BUSHING MARKET REGIONAL OUTLOOK

Regionally, the market is categorized into North America, Europe, Asia Pacific, and the Rest of The World.

Asia Pacific

Asia Pacific Automotive Bushing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Well-established Automotive Component Industry in China and Japan to Fuel Market Growth in Asia Pacific

Asia Pacific contributed 52.90% to the global market in 2025, with a valuation of USD 88.43 billion, and is projected to reach USD 93.86 billion in 2026. The growing investment in advanced automotive activities in the region is expected to fuel market growth. The supportive government initiatives in India and China, such as ‘Make in India’ and ‘Startup India,’ are set to fuel the development of advanced manufacturing facilities for automotive components. The growing demand for heavy commercial vehicles due to increasing industrial activities in the region is expected to drive Asia Pacific automotive bushing market size. The Japan market is projected to reach USD 10.83 billion by 2026, the China market is projected to reach USD 54.66 billion by 2026, and the India market is projected to reach USD 17.72 billion by 2026.

Europe

The Europe market generated USD 33.23 billion in 2025, representing 19.88% of the global market landscape, and is expected to reach USD 34.83 billion in 2026, due to the presence of many leading automotive manufacturers, such as Volkswagen AG, Stellantis NV, Mercedes-Benz Group AG, Bayerische Motoren Werke (BMW) AG, and Renault SA. These players are focusing on the development of advanced luxury vehicles with high-quality interiors. These advanced luxury vehicles are integrating bushing to improve the quality and safety of passengers’ travel experiences. The UK market is projected to reach USD 5.28 billion by 2026, and the Germany market is projected to reach USD 6.32 billion by 2026.

North America

In 2025, North America represented USD 35.44 billion, accounting for 21.20% of the worldwide market, and is projected to grow to USD 37.17 billion in 2026. North America has established an automotive sector that emphasizes research and development, leading to the adoption of sophisticated engine bushes that improve performance and efficiency. The presence of major automotive manufacturers and a strong supply chain further support the market expansion. The U.S. market is growing rapidly, driven by factors such as increased vehicle comfort and fuel efficiency, rise of electric vehicles (EVs), and investments in autonomous technology. The U.S. market is projected to reach USD 25.46 billion by 2026.

Rest of the World

Rest of the World contributed approximately USD 10.05 billion to the global market in 2025, accounting for 6.00% share, and is expected to reach USD 10.61 billion in 2026. Rest of the World is experiencing significant growth. This expansion is fueled by factors such as increased vehicle production, adoption of electric vehicles, stringent environmental regulations, and the demand for enhanced vehicle performance and comfort. Manufacturers are responding to these trends by developing advanced bushing technologies and materials, positioning themselves to meet the evolving needs of the automotive industry in these regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Vibracoustic SE is Poised to be the Leading Market Player, Driven by its Vast Product Offerings and Extensive Market Presence

Vibracoustic SE stands as a global leader in automotive Noise, Vibration, and Harshness (NVH) solutions, with a specialized focus on bushings. Their product portfolio encompasses a wide range of components, including chassis bushings, engine mounts, and suspension systems, tailored for both internal combustion engine (ICE) vehicles and battery electric vehicles (BEVs). In February 2023, Vibracoustic introduced optimized chassis bushings designed to address the increased weight and NVH challenges associated with BEVs. These bushings feature low-hardening rubber compounds and innovative designs to enhance durability and ride comfort.

Sumitomo Riko Company Limited is another prominent Japanese supplier specializing in anti-vibration rubber components, including automotive bushings. Their extensive product lineup features engine mounts, suspension bushings, and other NVH-related components, catering to a diverse range of vehicles. The company leverages its expertise in polymer materials to develop products that meet the evolving demands of modern vehicles, including those with electrified powertrains. Sumitomo Riko's global footprint spans Asia, North America, and Europe, allowing them to collaborate closely with international OEMs. Their commitment to research and development ensures continuous innovation, positioning them as a reliable partner in the automotive related sector.

LIST OF KEY AUTOMOTIVE BUSHING COMPANIES PROFILED

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Jotex Rubber Industrial Co., Ltd. (Taiwan)

- Sumitomo Riko Company Limited (Japan)

- DuPont de Nemours, Inc. (U.S.)

- BOGE Rubber & Plastics (Belgium)

- Vibracoustic SE (Germany)

- Hyundai Polytech India Pvt. Ltd. (India)

- Nolathane (Australia)

- Hutchinson Paulstra (France)

KEY INDUSTRY DEVELOPMENTS

- In May 2025, MAHLE unveils HD technology, claiming superiority over original equipment parts in Korea. MAHLE HD's technological prowess includes MAHLE HD ball pins, MAHLE HD rubber bushings, and MAHLE HD stabilizer links.

- In April 2025, Vibracoustic, a leading global automotive noise, vibration, and harshness (NVH) expert, engineered state-of-the-art solutions that significantly enhance the driving comfort and experience of a premium electric pickup truck. Air springs, jounce bumpers, and hydro bushings tackle unwanted excitations and support the performance of the all-electric pickup truck.

- In March 2025, DuPont Interconnect Solutions (ICS), a leading material solutions and systems design partner within DuPont Electronics & Industrial, addresses signal integrity and power and thermal management challenges.

- In April 2024, WinPart, a leading distributor of high-quality automotive Spare parts, announced its exclusive partnership with Kavo Parts, a renowned supplier of Spare Parts for passenger cars light commercial vehicle in Europe. This strategic alliance marks a significant milestone in WinPart's commitment to providing customers with an extensive range of affordable top-tier products.

- In June 2023, Hyundai Polytech Mexico expanded in Coahuila. The company invested USD 13 million to expand its existing plant, reaching a cumulative investment of USD 24 million. The new extension will be for the manufacturing of plastic auto parts by thermoforming, precision injection, steering parts, anti-vibration systems, dust covers, and a wide variety of rubber parts.

REPORT COVERAGE

The global Automotive Bushing market report provides detailed market analysis and focuses on key aspects such as leading companies, vehicle types, design, and technology. Besides this, the report offers insights into the latest market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.15% from 2026 to 2034 |

|

Unit |

Value (USD Billion) Volume (Million Units) |

|

Segmentation |

Application

Vehicle Type

Material

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the market is projected to reach USD 263.71 billion by 2034.

The market is expected to grow at a CAGR of 5.15% during the forecast period.

The rise of advanced suspension systems and increased vehicle comfort driving demand for bushings.

The Asia-Pacific region led the market in 2025.

The Asia-Pacific region's bushing market size share was USD 88.43 billion in 2025.

Continental AG, Vibracoustic SE, and ZF Friedrichshafen AG are among the major market players operating in the industry.

- 2021-2034

- 2025

- 2021-2024

- 271

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us