Automotive Carbon Brush Market Size, Share & Industry Analysis, By Application (Engine Electronic System, Comfort System, Safety and Chassis Electronic System, and Body Electronic System), By Brush Grade (Carbon Graphite, Electrographite, Graphite, Metal Graphite, and Silver Graphite), By Vehicle Type (Hatchback/Sedan, SUVs, LCV, and HCV), By Propulsion (ICE and Electric), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

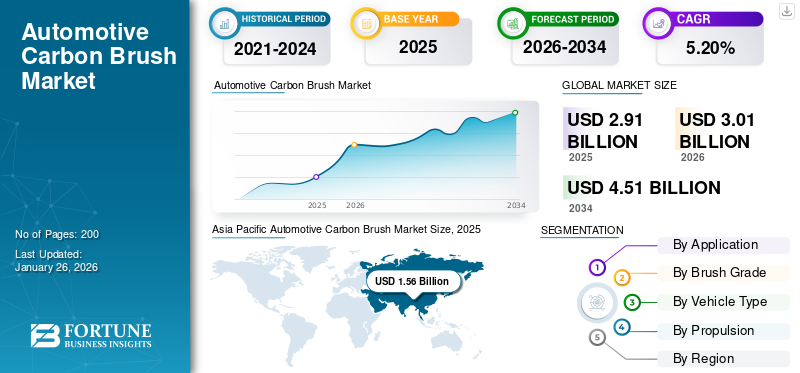

The global automotive carbon brush market size was valued at USD 2.91 billion in 2025. The market is projected to grow from USD 3.01 billion in 2026 to USD 4.51 billion by 2034, exhibiting a CAGR of 5.20% during the forecast period. Asia Pacific dominated the global market with a share of 53.57% in 2025.

Automotive carbon brushes function as a crucial link for conducting electrical current between the static and moving elements of a motor in a vehicle. Within a generator or motor, the commutator revolves along a shaft while the stationary carbon brush interfaces with it, facilitating the passage of electricity and enabling circuit completion. This setup ensures the smooth flow of electrical energy, which is essential for the proper operation of the motor or generator.

EVs run on electric motors, and their in-vehicle functions, such as power windows, power tailgate, and others, are also dependent on motors. Thus, the rising demand for electric vehicles drives the market growth. However, the development of brushless motors, eliminating the need for carbon brushes, hinders market growth. The development of carbon brushes that can withstand higher temperatures, greater mechanical stress, and increased electrical loads fuels market growth over the forecast period.

Major players in the automotive carbon brush market include companies such as Mersen, Schunk Carbon Technology, and Morgan Advanced Materials, among others. These companies specialize in producing high-quality carbon brushes used in automotive motors, alternators, and starters. They focus on innovation, durability, and performance to meet the growing demand for electric vehicles and energy-efficient automotive systems.

During the COVID-19 pandemic, the decrease in vehicle sales and production hindered the demand for automotive brushes. Factory shutdowns and lockdowns witnessed a decline in the supply and demand of raw materials required for the manufacturing of vehicles, causing supply chain disruption. While the pandemic witnessed lower automotive production and sales, the demand for electric vehicles elevated further during the pandemic. This supported the automotive carbon brush market post-COVID-19 pandemic.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

AUTOMOTIVE CARBON BRUSH MARKET TRENDS

Increasing Demand for EVs Propels Market Development

EVs rely on electric motors for propulsion, which necessitates the use of carbon brushes. These brushes are critical components in electric motors, facilitating the transfer of electrical energy to mechanical energy by maintaining contact between stationary and rotating parts. As the adoption of EVs continues to rise globally, the demand for automotive carbon brushes increases proportionally providing energy efficiency. This growth is fueled by environmental concerns, government regulations promoting cleaner transportation, and advancements in battery technology, which help in longer driving ranges and faster charging times.

For instance, the International Energy Agency (IEA) forecasts continued strength in electric car sales for 2024, with an estimated 17 million units expected to be sold by the end of the year. First-quarter sales witnessed a notable increase of around 25% compared to the same period in 2023, underscoring sustained growth in the overall market.

MARKET DYNAMICS

MARKET DRIVERS

Integration of Advanced Electronics in Modern Vehicles Influence Market Demand

Modern vehicles feature a plethora of electronic components, including sensors, actuators, control units, and electric motors. Many of these components require carbon brushes for proper operation, particularly electric motors used in various systems, such as power windows, HVAC systems, and windshield wipers. Advanced electronic systems demand higher performance from carbon brushes to ensure reliable and efficient operation. Carbon brushes need to meet stringent requirements for conductivity, wear resistance, and reliability to support the increased electrical loads and operating conditions of modern automotive applications. Thus, the integration of advanced electronics in modern vehicles fuels the automotive carbon brush market growth.

MARKET RESTRAINTS

Development of Brushless Motors Poses Challenges to Market Growth

Brushless motors operate without the need for carbon brushes, unlike traditional brushed motors. Instead, they utilize electronic commutation, which eliminates the need for physical brushes to maintain electrical contact. As brushless motors become more prevalent in automotive applications, the demand for carbon brushes decreases, impacting the growth prospects of the automotive carbon brush market.

In November 2022, WEBER DRIVETRAIN, an Electric Vehicle (EV) start-up, inaugurated its automated manufacturing plant situated in Pune's Chakan district. Under the 'Make in India' initiative, the company has pledged an investment of Rs 35 crore for Phase 1 of this facility. This manufacturing hub will feature extensive automation, including cutting-edge semi-robotics, to produce Brushless DC Electric (BLDC) Motor hub motors and EV controllers in compliance with Indian regulatory norms.

MARKET OPPORTUNITIES

Adoption of EVs Drives Market Growth Opportunities

EVs rely heavily on electric motors, which use carbon brushes to ensure smooth operation, efficient power transfer, and extended motor life. As EV sales increase, the demand for high-quality carbon brushes rises, particularly for motors in electric drivetrains, power steering, and other critical systems. Additionally, carbon brushes help improve motor efficiency and reduce wear, which is crucial for EV performance. With governments pushing for cleaner transportation and automakers prioritizing sustainability, the EV market is expanding rapidly. This surge directly boosts the carbon brush market, as manufacturers focus on developing advanced, durable brushes tailored to meet the specific needs of electric vehicles.

The International Energy Agency stated that, in 2023, nearly 14 million electric cars were sold globally. This marked a 35% increase from 2022, and the total number of electric cars on the roads reached 40 million.

MARKET CHALLENGES

High Cost of Raw Materials Poses Challenge to Market Growth

Carbon brushes are made from materials such as graphite, copper, and other specialized composites, which can be expensive and subject to price fluctuations. As these raw materials become more costly, manufacturers face increased production costs, which can either reduce profit margins or result in higher prices for end consumers. This impacts the affordability and competitiveness of carbon brushes, especially in cost-sensitive markets. Additionally, supply chain disruptions, such as those caused by geopolitical tensions or natural disasters, can further inflate material prices, causing instability in the market. These challenges make it difficult for manufacturers to scale efficiently and meet the increased demand, particularly in emerging automotive sectors such as electric vehicles.

SEGMENTATION ANALYSIS

By Application

Stringent Safety Regulations Develop Safety and Chassis Electronic System Market Growth

Categorized by application, the market is segmented into engine electronic system, comfort system, safety and chassis electronic system, and body electronic system.

The safety and chassis electronic system segment is projected to account for 35.99% of the market share in 2026.

The segment is also estimated to develop at the fastest-growing CAGR over the forecasted period. Stringent safety regulations enforced by regulatory bodies and governments worldwide compel automotive manufacturers to integrate advanced safety systems into vehicles. These regulations often mandate features such as anti-lock braking systems, electronic stability control, traction control systems, and other chassis-related safety features.

The body electronic system held the second-largest market share in 2024. Modern vehicles increasingly offer a wide range of comfort and convenience features controlled by electronic systems. These may include power windows, central locking, electric mirrors, adjustable seats, climate control systems, keyless entry, and interior lighting systems. Consumer demand for such features drives the integration of body electronic systems into vehicles.

To know how our report can help streamline your business, Speak to Analyst

By Brush Grade

High-performance Characteristics enhances the Market Adoption of Electrographite

Segmented by brush grade, the market includes carbon graphite, electrographite, graphite, metal graphite, and silver graphite.

The electrographite brush grade segment is expected to hold a share of 31.70% in 2026. Electrographite brushes are known for their high-performance characteristics, including excellent electrical conductivity, low friction, and high-temperature resistance. As automotive applications require brushes that can withstand demanding operating conditions, such as ability to withstand high temperatures and electrical loads, electrographite brushes are preferred for their superior performance and reliability.

The silver graphite segment is attributed to develop with the fastest-growing CAGR over the forecast period. Silver graphite brushes are versatile and can perform well under a wide range of operating conditions encountered in automotive applications, including varying temperatures, speeds, and electrical loads. This versatility makes them suitable for use in different types of vehicles and across various automotive systems. As this type of brush grade is used in traction motors for EVs, the rise of electric vehicles also plays a substantial role in driving the segmental market growth over the forecast period.

By Vehicle Type

SUV's is the Leading Vehicle Type Due to its Versatility and Safety Benefits

Categorized by vehicle type, the market encompasses hatchback/sedan, SUVs, LCV, and HCV.

The SUV vehicle type segment dominated the global market with a market share of 42.65% in 2026. SUVs have witnessed significant growth in popularity worldwide due to their versatility, spaciousness, and perceived safety benefits. Consumers are increasingly opting for SUVs over traditional sedans or hatchbacks, driving the demand for these vehicles. As SUVs become more popular, the demand for components requiring carbon brushes used in their electrical systems increases proportionally, fueling the segmental growth.

The HCV segment is attributed to develop with the fastest growing CAGR during 2025-2032. HCVs are gaining traction in the integration of advanced technologies such as ADAS systems, AEB systems, and the electrification of HCV, among others, which require carbon brushes. This drives the segment's growth in the considered automotive carbon brush market forecast period.

By Propulsion

Large Existing Fleet of ICE Vehicles Drives Segmental Demand

Categorized by propulsion, the market encompasses ICE and electric.

The ICE propulsion segment dominated the global market with a market share of 2.18% in 2026. Despite the rise of electric and hybrid vehicles, the majority of vehicles on the road still propel on internal combustion engines. This large existing fleet of ICE vehicles drives the ongoing demand for replacement parts and components, including carbon brushes used in various electrical systems such as starters, alternators, and ignition systems. This fuels the segment's market growth.

The electric segment is estimated to develop with the fastest-growing CAGR during the 2025-2032. Government incentives, subsidies, and tax breaks aim at promoting electric vehicle adoption to help reduce the upfront cost barrier for consumers. Additionally, as economies of scale are achieved in the production of EVs and their components, manufacturing costs decrease, making electric vehicles more affordable and attractive to a wider range of consumers. Thus, as demand for EVs grows, the carbon brush required for these types of vehicles augments the market growth of the segment over the forecast period. For instance, According to the U.S. Internal Revenue Service (IRS), individuals may be eligible for a tax credit of up to USD 7,500 under Internal Revenue Code Section 30D if they purchase a new, qualified PHEV or FCV. The Inflation Reduction Act of 2022 has modified the regulations governing this credit for vehicles acquired between 2023 and 2032.

AUTOMOTIVE CARBON BRUSH MARKET REGIONAL OUTLOOK

By region, the market is studied across North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Carbon Brush Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Rapid Economic Growth in Asia Pacific Fuels Regional Market Growth

Asia Pacific region held the largest automotive carbon brush market share in 2025. The region is also attributed to having the fastest CAGR of 5.3%. The region is home to some of the world's largest automotive markets, including China, Japan, India, and South Korea. The rapid growth of the automotive industry in these countries, driven by factors such as increasing urbanization, rising disposable income, and expanding middle-class populations, contributes to the demand for automotive carbon brush in the region. The Japan market is projected to reach USD 0.27 billion by 2026, the China market is projected to reach USD 0.87 billion by 2026, and the India market is projected to reach USD 0.19 billion by 2026. Asia Pacific maintained a strong presence in the global market, reaching USD 1.56 billion in 2025, accounting for 53.57% share, and is expected to reach USD 1.62 billion in 2026.

North America

The North American region held the second-largest market share in 2024. The North American market for heavy-duty vehicles, including trucks, buses, and construction equipment, is substantial. These vehicles rely on electrical systems for various functions, such as starting, charging, and lighting. As a result, there is a significant demand for carbon brushes used in the electrical systems of heavy-duty vehicles. The U.S. market is projected to reach USD 0.49 billion by 2026. In 2025, the North America market stood at USD 0.74 billion, representing 25.27% of global demand, and is projected to grow to USD 0.76 billion in 2026.

In the U.S., the market is driven by the growing demand for electric vehicles (EVs), which require high-performance electric motors. The shift toward green energy, stricter emissions regulations, and technological advancements in automotive further fuel this growth. Additionally, the expanding automotive aftermarket sector, where carbon brushes are essential for vehicle maintenance and repairs, also contributes significantly to the market’s expansion

Europe

Europe held a significant market share in 2024 as the region is experiencing significant growth in the EV market, with governments implementing policies and incentives to embrace the adoption of EVs. Initiatives such as financial incentives, emission regulations, and infrastructure development contribute to the growth of electric vehicle sales, consequently increasing the demand for carbon brushes used in electric motors and other electrical systems. The UK market is projected to reach USD 0.03 billion by 2026, while the Germany market is projected to reach USD 0.14 billion by 2026. The Europe region captured 14.96% of the global market in 2025, generating USD 0.44 billion in revenue, and is projected to reach USD 0.45 billion in 2026.

Rest of the World

The rest of the world market comprises Latin America (excluding Mexico) and the Middle East & Africa region. Major cities, such as Dubai, Abu Dhabi, and others, witnessed growth in demand for luxury vehicles. Luxury vehicles are equipped with advanced technologies that require carbon brushes for their operation. The Rest of the World market generated USD 0.18 billion in 2025, representing 6.21% of the global market landscape, and is expected to reach USD 0.18 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Product Innovation, Partnerships, and Expansion Fuels Competitive Landscape

The competitive landscape for the global automotive carbon brush market is characterized by the presence of several prominent market players, each striving to maintain or expand their market share through various strategies such as product innovation, mergers and acquisitions, geographic expansion, and partnerships. Key players include Mersen, Morgan Advanced Materials, and Schunk Group, among others. Morgan Advanced Materials is one of the leading players in the market and is known for its expertise in advanced materials technology. The company provides high-performance carbon brushes designed to deliver optimal performance and reliability in automotive systems.

List of Automotive Carbon Brush Companies

- MERSEN (France)

- Helwig Carbon Products, Inc. (U.S.)

- OMNISCIENT INTERNATIONAL (India)

- Toyo Tanso Co., Ltd. (Japan)

- Morgan Advanced Materials (U.K.)

- Schmidthammer Elektrokohle GmbH (Germany)

- AVOCarbon (Germany)

- Schunk Carbon Technology (Germany)

- Carbon Brush Company Pvt. Ltd. (India)

- Shree Auto Electronics (India)

- PanTrac (Germany)

KEY INDUSTRY DEVELOPMENTS

- April 2024 - Toyo Tanso Co., Ltd. showcased its offerings at the "HANNOVER MESSE 2024" in Germany held between April 22nd and April 26th, 2024. The company planned to present its range of mechanical carbon products at its booth during the event.

- April 2024 - SKF devised an innovative remedy for a developing issue in Electric Vehicle (EV) powertrain design. The SKF Conductive brush ring establishes a dependable electrical link between an EV eAxle rotor shaft and its housing, thereby enhancing the anticipated lifetime of eAxles. When paired with SKF Hybrid ceramic ball bearings, it additionally diminishes parasitic current effects, reducing the risk of premature failure in bearings and associated components.

- March 2024 - Helwig Carbon launched Multi-Flex and Tri-Flex designs. The company's Multi-Flex and Tri-Flex designs provide dual benefits: better performance on uneven comm surfaces and decreased circulating currents from individually wired wafers. Splitting the DC motor brush into multiple wafers increases contact points, leveraging Newton's Second Law to reduce force and ensure consistent contact. These split brushes are commonly used in high-voltage motors, reversing motors, elevators, slip rings, and heavy industries.

- December 2023 - Toyo Tanso Co., Ltd. published a 2023 integrated report. In the report, the company stated that around 11.0% of its net sales are generated by carbon products for general industries, and the company offers carbon brushes for automobiles and other products.

- October 2023 - Toyo Tanso Co., Ltd. joined the renewable energy exhibitions in Taiwan in October 2023. It showcased carbon brushes for wind and hydropower generation, aiming to support global decarbonization efforts and reduce power generation costs. The company also displayed CNovel porous carbon for next-gen batteries.

- March 2021 - ICP Wind expanded its partnership portfolio, teaming up closely with Schunk, one of the global leaders in carbon and ceramic solutions. Together, they target the wind energy market. Schunk's Carbon Technology ensures efficient current transfer, low maintenance, and noise reduction in wind power systems. Schunk carbon brushes excel in slip rings of double-fed asynchronous generators, offering durability in various environmental conditions.

REPORT COVERAGE

The market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the factors above, it encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

CAGR of 5.20% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Application

|

|

By Brush Grade

|

|

|

By Vehicle Type

|

|

|

By Propulsion

|

|

|

By Region

|

Frequently Asked Questions

As per a study by Fortune Business Insights, the market size was valued at USD 2.91 billion in 2025.

The market is expected to grow at a CAGR of 5.20% over the forecast period.

By vehicle type, the SUVs segment held the largest market share in 2025.

In 2025, the Asia Pacific market size stood at USD 2.91 billion.

The integration of advanced electronics in modern vehicles influences the market demand.

Mersen, Morgan Advanced Materials, and Schunk Group are among the top key players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us