Automotive Traction Control System Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, LCV, and HCV), By Component (Sensors, Electronic Control Unit (ECU), Hydraulic Modulators, and Wireless Accelerometers), By System Type (Mechanical Linkage, Electrical Linkage, Hydraulic Systems, and Electronic Traction Control (ETC)), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

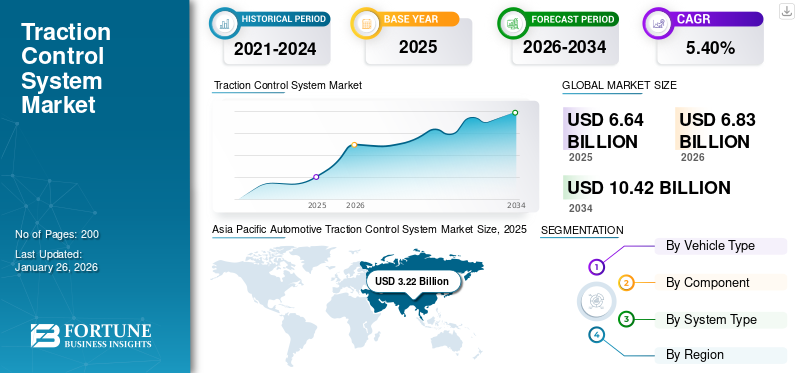

The global automotive traction control system market size was valued at USD 6.64 billion in 2025 and is projected to grow from USD 6.83 billion in 2026 to USD 10.42 billion by 2034, exhibiting a CAGR of 5.40% during the forecast period. Asia Pacific dominated the global market with a share of 48.40% in 2025.

An automotive Traction Control System (TCS) is a safety feature designed to prevent wheel spin during acceleration by monitoring wheel speed and adjusting engine power or applying braking force to individual wheels. It works alongside an Anti-Lock Braking System (ABS) and Electronic Stability Control (ESC) to enhance vehicle stability, particularly on slippery surfaces such as ice, snow, or wet roads.

Modern TCS systems use advanced sensors and algorithms to optimize traction, improve driver control, and reduce accidents caused by loss of grip. Recent advancements include integration with Electric Vehicle (EV) powertrains and autonomous driving systems, such as ZF’s EVOline TCS, which enhances efficiency in EVs. Governments of different countries, including India, are mandating TCS in new vehicles under the Bharat NCAP safety norms.

The global automotive TCS market is driven by stringent safety regulations, rising consumer demand for Advanced Driver-Assistance Systems (ADAS), and the growing adoption of electric and autonomous vehicles. Asia Pacific dominates due to high vehicle production and regulatory pushes, such as China’s GB 7258 standards requiring TCS in commercial vehicles. Europe follows closely, with Euro NCAP incentivizing TCS adoption through safety ratings. Manufacturers including Bosch and Continental are innovating TCS for EVs, for instance, Bosch’s integrated braking systems for hybrids. The market is expanding as older vehicles retrofit TCS modules. Partnerships between tech firms (e.g., Nvidia) and automakers aim to enhance TCS software for self-driving cars.

The COVID-19 pandemic disrupted supply chains, delaying TCS component production and vehicle assembly. Automakers such as Toyota and Ford faced semiconductor shortages, slowing TCS integration in new models. However, the post-2021 recovery witnessed accelerated demand for safety technologies as consumers prioritized vehicles with advanced features. Governments also reinforced safety mandates; for instance, the U.S. NHTSA proposed updated standards for electronic stability systems, indirectly boosting TCS adoption. The shift toward EVs post-COVID further propelled TCS innovation, with companies including Continental developing lightweight, energy-efficient modules. While temporary setbacks occurred, the long-term focus on vehicle safety and electrification has strengthened the TCS market’s growth trajectory.

Download Free sample to learn more about this report.

Automotive Traction Control System Market Trends

Rapid Adoption of TCS in Two-Wheelers and Commercial Vehicles is an Emerging Trend

A significant trend is the expansion of TCS applications beyond passenger vehicles, particularly into two-wheelers and commercial vehicles. With rising road safety concerns in densely populated regions, governments push TCS adoption in motorcycles and heavy-duty trucks. For example, India’s Ministry of Road Transport and Highways mandates TCS for two-wheelers above 125cc to reduce accidents caused by wheel spin on wet roads. Robert Bosch GmbH responded by introducing motorcycle-specific TCS units, such as the Motorcycle Stability Control (MSC) system, which reduces accident risks by 30% in models such as the BMW Motorrad.

In commercial vehicles, Knorr-Bremse launched the iTEBS X braking system in 2023, featuring Automatic Traction Control (ATC) for trailers to prevent jackknifing and improve load stability. Similarly, Eaton in May 2024, developed the ELocker differential for hybrid SUVs, combining TCS with electric drivetrains to enhance off-road traction. These innovations address the unique demands of logistics and construction sectors, where vehicle downtime due to traction issues incurs significant costs.

The trend is further amplified by rising EV adoption. EVs necessitate precise torque management to balance regenerative braking and traction, prompting companies such as ZF to design EVOline TCS systems that optimize energy recovery without compromising grip. Such advancements underscore the shift toward application-specific TCS solutions, ensuring relevance across diverse vehicle categories and driving conditions. This diversification broadens market reach and reinforces TCS as a cornerstone of modern automotive safety.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Growing Need for Enhanced Safety-Efficient Vehicles is Driving Market Growth

The stringent government regulations mandating vehicle safety technologies are the primary driving force in the global Traction Control System (TCS) market. Governments worldwide enforce stricter safety norms to reduce road accidents, compelling automakers to integrate advanced systems, including TCS. For instance, India’s Bharat NCAP (New Car Assessment Program), implemented in 2023, mandates TCS in new vehicles to enhance stability on slippery surfaces and improve crash safety ratings. Similarly, China’s GB 7258 standards require TCS in commercial vehicles to mitigate skidding risks during heavy-load operations. In Europe, the Euro NCAP safety ratings incentivize automakers to adopt TCS by linking it to higher vehicle safety scores, influencing consumer purchasing decisions.

Manufacturers are responding with innovations tailored to these regulations. For example, Continental AG introduced its Green Caliper technology, which integrates TCS with regenerative braking in Electric Vehicles (EVs) to comply with emission reduction mandates. Bosch developed hybrid-specific TCS modules that optimize traction while managing energy recovery in EVs16. These advancements align with global trends toward electrification and autonomous driving, where TCS ensures stability in complex powertrains. Additionally, emerging markets including Brazil and Indonesia are adopting TCS retrofitting policies for older vehicles, expanding aftermarket opportunities.

The Asia Pacific region, particularly China and India, dominates due to high vehicle production volumes and regulatory pushes. For example, India’s focus on two-wheeler safety has spurred TCS adoption in motorcycles, with Bosch launching dedicated systems for models such as the TVS Apache RTR 310. Such regulatory and technological partnership accelerates TCS penetration, making compliance a critical growth aspect for automakers and suppliers.

Market Restraints

Limited Consumer Awareness Regarding TCS Hampers Market Growth

One of the major factors restraining the global automotive traction control system market growth is the limited consumer awareness and acceptance in emerging markets. In regions including India and Brazil, many consumers prioritize affordability over advanced safety features, which can limit the adoption of TCS in budget-friendly vehicles. This lack of awareness about the benefits of TCS, such as improved safety and vehicle stability, hampers market growth by reducing demand for these systems in cost-sensitive markets.

Another significant restraint is the compatibility issues with older vehicle models. Integrating TCS into existing vehicles can be challenging due to differences in electronic architectures and the need for extensive testing to ensure compatibility. This complexity discourages retrofitting efforts, limiting the aftermarket potential for TCS systems. For instance, manufacturers such as Continental AG and Robert Bosch GmbH face challenges in developing TCS solutions that are backward compatible with older models, which slows down the adoption rate in the aftermarket segment.

Additionally, supply chain disruptions have become a critical concern. The COVID-19 pandemic highlighted vulnerabilities in global supply chains, affecting the availability of components necessary for TCS systems. Such disruptions can lead to production delays and increased costs, further restraining market growth. Despite these challenges, the market continues to evolve with innovations such as wireless accelerometers and advanced sensors, which aim to enhance TCS performance and appeal to consumers.

Market Opportunities

Rising Integration of TCS with Advanced Driver Assistance Systems (ADAS)

Governments worldwide are mandating TCS adoption to reduce accidents, with India’s Bharat NCAP and AIS-156 standards (for EV safety) pushing manufacturers to incorporate TCS in new models. The market is fueled by increasing EV sales and autonomous vehicle development. Technological developments include AI-driven predictive traction control and integration with Vehicle-to-Everything (V2X) communication for proactive hazard detection. For example, Bosch and Continental AG are enhancing TCS algorithms to work seamlessly with regenerative braking in EVs, improving energy efficiency.

Hyundai and Kia have introduced torque vectoring TCS in high-performance EVs to optimize wheel grip. Governments are also tightening norms, such as the EU’s Euro NCAP protocols, which prioritize TCS in safety ratings. Manufacturer updates, such as ZF Friedrichshafen’s next-gen TCS for commercial vehicles, addressing slippery road conditions. Additionally, India’s AIS-156 Amendment 3 mandates robust Battery Management Systems (BMS) in EVs, indirectly boosting TCS demand for stability during regenerative braking. The U.S. NHTSA and Euro NCAP 2025–2035 roadmaps further emphasize TCS as a core component of collision avoidance systems.

Segmentation Analysis

By Vehicle Type

Increasing Demand, Rising Disposable Incomes, and Urbanization Contribute to Growing Adoption of SUVs

The global market is segmented by vehicle type into hatchback/sedan, SUVs, LCV (Light Commercial Vehicles), and HCV (Heavy Commercial Vehicles).

The SUV segment is rising significantly due to the increasing popularity of SUVs worldwide, particularly in North America and Europe. SUVs require advanced TCS to manage their higher weight and center of gravity, enhancing stability on various terrains. This growth contributes to the overall market by driving demand for sophisticated TCS systems that handle diverse driving conditions. SUV is the fastest-growing segment, driven by consumer preferences for larger vehicles and government regulations mandating safety features in all vehicle types. For instance, Continental AG has developed TCS solutions specifically for SUVs, focusing on improved traction and stability during off-road driving. This innovation aligns with the growing demand for SUVs and enhances overall market growth by providing advanced safety features.

Hatchback/sedan segment possesses significant growth due to its large market share in passenger vehicles, especially in Asia Pacific. The segment dominates due to high global production volumes and regulatory mandates for safety features in mass-market vehicles. For instance, Euro NCAP and Bharat NCAP require TCS in new models, accelerating adoption in budget and mid-range cars. Technological developments include AI-driven TCS integration with ADAS in models such as the Honda City and Toyota Corolla.

LCVs are gaining traction with fleet operators prioritizing safety and fuel efficiency. Regulations like EU’s Euro 7 norms mandate TCS in LCVs to reduce accidents. ZF Friedrichshafen introduced modular TCS kits for electric LCVs, optimizing battery range. HCVs adoption is rising due to stringent safety standards and autonomous trucking trends. Volvo Trucks and Daimler integrate TCS with predictive cruise control to enhance freight safety.

By Component

Electronic Control Units (ECUs) Dominate due to its Critical Role in TCS

The market is segmented by component into sensors, Electronic Control Unit (ECU), hydraulic modulators, and wireless accelerometers.

The ECU segment is dominating the market due to its central role in processing sensor data and controlling TCS functions.

Sensors are the fastest-growing segment due to technological advancements, which enhance TCS performance by providing real-time data on wheel speed and traction conditions. This growth is crucial as it enables more precise control over vehicle stability, contributing significantly to the overall market by improving safety and efficiency.

The integration of wireless accelerometers is gaining traction as they offer easier installation and reduced system complexity, making them attractive for future vehicle designs. Bosch has introduced wireless accelerometer systems that improve TCS reliability and reduce vehicle weight, aligning with trends toward lighter, more efficient vehicles. This innovation supports market growth by enhancing system reliability and reducing production costs.

By System Type

Higher Efficiency and Reliability of Electronic Traction Control (ETC) Contributes Toward its Rapid Growth

The market is segmented by system type into mechanical linkage, electrical linkage, hydraulic systems, and Electronic Traction Control (ETC).

The Electronic Traction Control (ETC) is the fastest-growing segment, driven by its ability to integrate with advanced vehicle systems including ABS and ESC, enhancing overall vehicle stability and safety. For instance, ZF TRW in September 2024, developed ETC systems that optimize traction in real-time, using advanced algorithms to predict road conditions and adjust vehicle dynamics accordingly. This innovation supports market growth by providing advanced safety features that appeal to consumers seeking high-performance vehicles.

The electrical linkage segment is dominant and growing rapidly due to its efficiency and reliability compared to mechanical systems. Electrical linkages reduce vehicle weight by replacing mechanical components with electronic ones, aligning with industry trends toward lighter vehicles and reduced emissions.

AUTOMOTIVE TRACTION CONTROL SYSTEMS MARKET REGIONAL OUTLOOK

The global automotive Traffic Control System (TCS) market is segmented into North America, Europe, Asia Pacific, and the rest of the world based on its geographies.

Asia Pacific

Asia Pacific Automotive Traction Control System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Increasing Adoption of Automation in Vehicle Manufacturing Drive Asia Pacific Market Growth

The Asia Pacific market was valued at USD 3.22 billion in 2025, capturing 48.40% of global revenue, and is estimated to reach USD 3.29 billion in 2026, accounting for the largest share due to high vehicle production and sales in China, Japan, and India. The region's growth is driven by increasing disposable incomes, urbanization, and government initiatives to enhance road safety through advanced vehicle technologies. The rising demand for passenger and commercial vehicles in Asia Pacific fuels the adoption of TCS, contributing significantly to the overall market growth.

North America

North America contributed 28.47% to the global market in 2025, with a valuation of USD 1.89 billion, and is projected to reach USD 1.95 billion in 2026. North America is the second-largest market, driven by investments in research and development of vehicle safety features. The U.S., Canada, and Mexico are key contributors, strongly focusing on integrating advanced safety systems including TCS in vehicles to meet stringent safety standards. The growth in North America supports the overall market by driving demand for sophisticated TCS systems, particularly in luxury and high-performance vehicles.

Europe

Europe accounted for USD 1.13 billion in 2025, representing 17.03% of the global market share, and is projected to reach USD 1.18 billion in 2026. Europe also experiences steady growth, influenced by stringent safety regulations and consumer awareness about vehicle safety. European manufacturers such as Continental AG and Robert Bosch GmbH are innovating TCS technologies to comply with Euro NCAP safety ratings, which incentivize the adoption of advanced safety features. This regulatory environment ensures that TCS remains a critical component in European vehicles, contributing to the market's expansion.

Rest of the World

The rest of the world, including regions including Latin America and the Middle East, is growing slower but benefits from increasing vehicle sales and government efforts to enhance road safety. As these regions develop economically and adopt more stringent safety standards, they are expected to contribute more significantly to the global TCS market in the future.

Overall, Asia Pacific's dominance and North America's steady growth drive the global market forward, with Europe and the rest of the world playing crucial supporting roles.

COMPETITIVE LANDSCAPE

Key Industry Players

Robert Bosch GmBH is Poised to Solidify its Leading Position Driven by its Technological Innovations and Extensive Market Presence

Robert Bosch GmbH is a top player in the automotive traction control system market. Bosch's dominance stems from its extensive portfolio of advanced automotive technologies, including sophisticated braking systems. The company's expertise in integrating Automotive Traction Control Systems with other safety features including Electronic Stability Control (ESC) enhances vehicle safety and performance. Bosch's commitment to innovation is evident in its development of cutting-edge braking solutions, such as the vacuum-independent, electro-hydraulic integrated power brake, which supports autonomous driving and electric vehicles.

With a strong presence across regions, Bosch benefits from its ability to adapt technologies to meet diverse regulatory standards and consumer demands. Bosch's market share is bolstered by its strategic partnerships and continuous investment in research and development. For instance, Bosch's collaboration with other industry leaders to enhance braking technologies further solidifies its position in the market. As a key player, Bosch's products and solutions are integral to the growth of the automotive traction control system market share globally.

Continental AG is another major global player operating in the market. Continental's strength lies in its comprehensive range of automotive safety solutions, including advanced automotive traction control system systems that enhance vehicle stability and safety. The company's focus on system integration and technological advancements has made it a preferred partner for many OEMs. Continental's market share is significant, with a substantial presence in regions such as Europe, with a high demand for advanced safety features. The company’s commitment to innovation, such as integrating the Automotive Traction Control System with other safety technologies, supports its position as a leading supplier of automotive safety systems.

LIST OF KEY AUTOMOTIVE TRACTION CONTROL SYSTEM COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Denso Corporation (Japan)

- ZF Friedrichshafen AG (Germany)

- Autoliv Inc. (Sweden)

- Hitachi Automotive Systems Limited (Japan)

- Knorr-Bremse AG (Germany)

- ADVICS CO., LTD. (Japan)

- Nissin Kogyo (Japan)

- Delphi Automotive LLP (U.K.)

KEY INDUSTRY DEVELOPMENTS

- May 2024: Eaton’s ELocker differential was chosen for a new plug-in hybrid SUV, offering superior control and traction with electronically controlled gears, ensuring optimal performance in challenging conditions.

- December 2023: Sensata Technologies announced that its innovative Brake Force Sensor has been selected by leading automotive brake system manufacturers for integration into next-generation Electromechanical Brake (EMB) systems. The sensor directly measures clamping force within the foundation brake, enabling closed-loop control of calipers and drums, enhancing braking performance, safety, and regenerative braking capabilities in passenger cars.

- December 2023 Knorr-Bremse reported the official start of volume production of the new iTEBS X, an enhanced version of an intelligent Electronic Trailer Braking system, which also includes Automatic Traction Control (ATC).

- October 2023: Bosch announced plans to integrate traction control systems into all motorcycles, aiming to reduce road accidents by 30%. They launched the MSC traction control unit for the TVS Apache RTR 310.

- January 2022: NTN Corporation expanded its wheel speed sensor range by adding 100 new references, enhancing the precision of traction control systems in vehicles.

REPORT COVERAGE

The global automotive traction control system market research report provides detailed market analysis and focuses on key aspects such as leading companies, vehicle types, design, and technology advances. Besides this, the report offers insights into the latest market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.40% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type

By Component

By System Type

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market is projected to reach USD 10.42 billion by 2034.

The market is expected to register a CAGR of 4.9% during the forecast period of 2026-2034.

Pursuit of enhanced safety efficient vehicles is driving the market growth.

Asia Pacific led the automotive traction control system market in 2025.

Robert Bosch GmbH, ZF Friedrichshafen AG, Continental AG, Denso, and Autoliv hold a major market share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us