Automotive Control Panel Market Size, Share & Industry Analysis, By Technology (Manual, Digital, Touch-based and Others), By Functionality (Center Console Control Panels, HVAC Control Panels, Door Control Panels, Steering-Mounted Control Panels, Instrument Cluster Panels and Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles), By Sales Channel (OEM and Aftermarket) and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

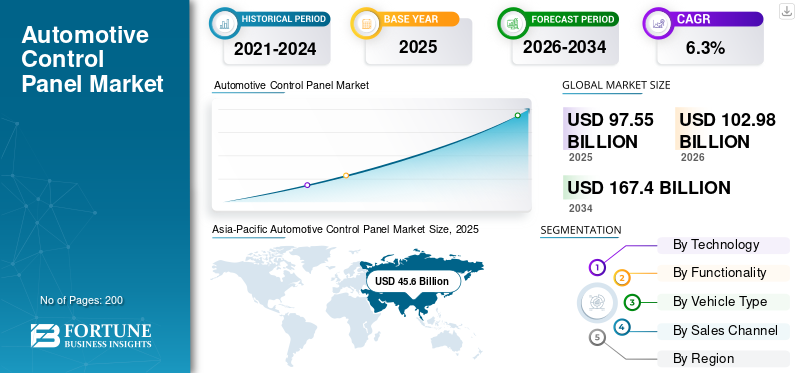

The global automotive control panel market size was valued at USD 97.55 billion in 2025. The market is projected to grow from USD 102.98 billion in 2026 to USD 167.40 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period. Asia Pacific dominated the global automotive control panel market with a market share of 46.75% in 2025.

The automotive control panel refers to the collection of interfaces, both physical and digital, that allow drivers and passengers to operate essential vehicle functions. These panels include center console controls, instrument clusters, HVAC interfaces, door switches, steering-mounted controls, and emerging touch and haptic surfaces. Together, they form the primary human-machine interaction (HMI) layer inside a vehicle, enabling users to manage climate, infotainment, driving information, communication, lighting, and a growing set of in-cabin features. As vehicles become more software-driven and feature-rich, the control panel has evolved from simple mechanical buttons to integrated digital ecosystems.

The relevance of automotive control panels has increased significantly as consumer expectations shift toward intuitive, personalized, and digitally connected cabin experiences. Modern vehicles rely on these interfaces to consolidate complex functions into accessible formats, reducing driver distraction while enhancing comfort and safety. Control panels also play a critical role in overall vehicle aesthetics, perceived quality, and brand identity. Premium models, in particular, use large digital displays, ambient lighting, haptic feedback, and customizable layouts to differentiate themselves, making the control panel a central element in competitive positioning among automakers.

The market is experiencing strong growth due to the rapid digitalization of the cockpit, rising penetration of touch-based infotainment systems, increased adoption of digital clusters, and the fast-expanding presence of advanced EVs and SUVs that require more sophisticated interfaces. Electrification is a major driver, as EVs often feature larger displays, centralized controls, multi-zone HVAC systems, and richer software-based interactions. Additionally, regulatory emphasis on safety is pushing automakers to integrate smarter clusters and advanced driver information modules. The shift toward connected vehicles and over-the-air updates also increases the value and complexity of control panels.

Leading manufacturers are innovating through the integration of digital cockpits, larger curved displays, haptic-touch surfaces, and multi-display architectures. Companies are focusing on consolidating ECUs, enabling seamless interaction across screens, and developing energy-efficient display technologies. Suppliers are also leveraging AI-based personalization, gesture recognition, and voice-assisted interfaces to elevate user experience. As competition intensifies, Tier-1 suppliers and OEMs are moving toward software-defined interiors, modular panel architectures, and advanced manufacturing techniques to support scalable, cost-effective production.

Download Free sample to learn more about this report.

Automotive Control Panel Market Key Takeaways

- 2025 Market Size: USD 97.55 billion

- 2026 Market Size: USD 102.98 billion

- 2034 Forecast Market Size: USD 167.40 billion

- CAGR: 6.3% from 2026–2034

- Asia Pacific dominated the automotive control panel market with a 46.75% share in 2025.

- Digital Control Technologies accounted for the largest market share.

- Center Console Control Panels are expected to remain the dominant product segment.

Asia Pacific

Strong EV production and digital cockpit adoption continue to drive regional leadership.

North America

Premium EVs and connected cabin technologies support steady market expansion.

Europe

Advanced cockpit systems and sustainable vehicle technologies fuel market growth.

U.S.

Rising adoption of software-defined cabins and intelligent HMI systems boosts demand.

Japan

Expanding vehicle electronics and digital cockpit integration support steady market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Software-Defined and Connected Cockpits Drives the Market Growth

Automakers are rapidly transitioning toward software-defined interiors that unify displays, controls, and digital services. Connected cockpits enhance personalization, enable OTA updates, and integrate advanced HMI features, significantly boosting user experience. This shift increases reliance on high-value digital control panels, especially in EVs and premium vehicles, where integrated screens dominate cabin architecture.

- For instance, in January 2025, BMW announced its next-generation iDrive and Panoramic Vision dashboard display, which enables software-defined interfaces, personalized layouts, and connected digital services across its upcoming models.

MARKET RESTRAINTS

Growing Cybersecurity and data privacy vulnerabilities restrict the market growth

As control panels become increasingly connected and software-intensive, vehicles are exposed to heightened risks of data breaches, remote hacking, and unauthorized system access. OEMs must comply with stricter cybersecurity frameworks, adding substantial development complexity and regulatory burden. These concerns slow the adoption of fully networked control interfaces and require ongoing security updates and architecture redesign.

- For instance, in July 2023, CISA issued a public advisory highlighting cybersecurity vulnerabilities in multiple automotive infotainment and telematics systems, warning that remote exploitation could affect vehicle controls.

MARKET OPPORTUNITIES

Advancements in Sensor and Display Technologies are Boosting the Market

Rapid improvements in automotive-grade displays, capacitive touch systems, haptic feedback, and interior sensing technologies are enabling richer, safer, and more interactive control panels. Higher-resolution screens, flexible OLEDs, and interior radar/IR sensors enhance both usability and design freedom, creating new revenue opportunities for Tier-1 suppliers and semiconductor companies.

- For instance, in November 2025, LG Display showcased its latest automotive OLED technologies at CES, including curved and flexible cockpit displays designed for next-generation control interfaces.

MARKET CHALLENGES

Creating Screen-Centric Designs Without Hurting Usability acts as a challenge for the market

A major challenge is designing large-screen or touch-heavy control panels that remain intuitive and distraction-free. Overreliance on touch surfaces can reduce tactile feedback and slow driver response. OEMs must strike a balance between minimalism and ergonomics, ensuring that critical functions remain accessible without requiring complex menu navigation.

AUTOMOTIVE CONTROL PANEL MARKET TRENDS

Expansion of Pillar-to-Pillar and Curved Display Layouts is Trending in the Market

OEMs are adopting wide, continuous displays that replace traditional clusters and center consoles with streamlined digital surfaces. These layouts support multi-touch, customizable interfaces, allowing designers to minimize mechanical switches while delivering a premium visual experience. The trend is accelerating as EV platforms favor simplified, screen-focused interiors.

- For instance, in January 2024, Stellantis unveiled its STLA SmartCockpit at CES, featuring a wide, integrated display surface tailored for immersive infotainment and AI-driven interaction.

Download Free sample to learn more about this report.

Segmentation Analysis

By Technology

Digital Technologies Dominate as Automakers Shift Toward Connected, Software-Defined Cabins

On the basis of technology, the market is segmented into manual, digital, touch-based, and others.

Digital control technologies dominate because modern vehicles increasingly rely on integrated infotainment systems, domain controllers, and air-quality control systems that enhance temperature, humidity, and air-quality management. Rising EV penetration, increasing demand for connected interfaces, and stricter environmental regulations accelerate digital adoption across both residential and commercial mobility applications.

- For instance, Hyundai’s 2024 models feature digital cockpit platforms with consolidated HMI, climate, and air-quality monitoring functions, reflecting the region’s push toward advanced environmental control systems.

By Functionality

Center Console Control Panels Lead Due to Central Role in Vehicle HMI and Environmental Management Systems

On the basis of functionality, the automotive control panel market is segmented into center console control panels, HVAC control panels, door control panels, steering-mounted control panels, instrument cluster panels, and others.

Center console control panels dominate, acting as the primary interface for infotainment, navigation, cabin climate, and air-quality management systems, forming the core of modern connected cabins. With the increasing integration of control technologies and digital ecosystems, center consoles will significantly influence the automotive control panel market share and the overall control system market size during the forecast period.

- For instance, Mercedes-Benz’s MBUX center display integrates HVAC, air-quality filtering, and infotainment functions, aligning with global sustainability goals by optimizing energy use.

By Vehicle Type

Passenger Cars Dominate Owing to High Production Volumes and Demand for Advanced Environmental Control Systems

On the basis of vehicle type, the market is segmented into passenger cars, LCVs, and HCVs.

Passenger cars dominate the market because they represent the largest global production segment and increasingly incorporate digital cockpits, climate control systems, and air-quality control systems to meet consumer expectations for comfort and safety. In the Asia Pacific, especially, rising urbanization and EV adoption boost demand for advanced environmental control systems in passenger cars.

- For instance, Toyota equips its passenger models, including the Corolla and Camry, with PM2.5 air-quality filters and climate-optimized control panels to enhance indoor air quality.

To know how our report can help streamline your business, Speak to Analyst

By Sales Channel

OEM Channel Dominates Due to Integrated Environmental and Digital Control Technology Installation

On the basis of sales channel, the market is segmented into OEM and aftermarket.

OEM dominates because automakers increasingly integrate digital HMI systems, climate-management controls, and temperature, humidity, and air-quality sensors during production. OEM-installed systems ensure compatibility with vehicle software platforms, support global environmental control system architectures, and meet regulatory expectations for cabin emissions and air filtration, strengthening their hold on market share throughout the forecast period.

Automotive Control Panel Market Regional Outlook

By regional, the automotive control panel market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia-Pacific Automotive Control Panel Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region dominates the automotive control panel market, driven by its expanding vehicle production base, rising digital cockpit adoption, and strong penetration of EVs and connected models. China, Japan, India, and South Korea lead the region with large-scale manufacturing ecosystems, rapid integration of control technologies, and a growing shift toward software-defined interiors. Increasing emphasis on air quality control systems and advanced HVAC interfaces also supports Asia Pacific’s leadership, especially as countries introduce stricter environmental regulations and align cockpit systems with user-centric design expectations.

- For instance, in 2024, Hyundai Motor Company expanded production across its Asia Pacific facilities, including Korea and India, equipping new models with advanced infotainment systems, digital clusters, and upgraded climate control panels, thereby reinforcing demand for next-generation control interfaces.

North America

North America follows the Asia Pacific, supported by strong production of SUVs, pickup trucks, and premium EVs that rely heavily on integrated HMI units, large touchscreens, and intelligent air-quality control systems. The U.S. leads regional demand as automakers incorporate larger displays, connected infotainment platforms, and domain controllers across high-volume models. Growing investment in software-defined cabin architectures also enhances the region’s adoption of advanced cockpit management systems.

Europe

Europe ranks third, backed by its engineering leadership, high adoption of premium vehicles, and growing emphasis on sustainable, energy-efficient cockpit technologies. Automakers in Germany, France, and the UK increasingly deploy curved displays, multi-display layouts, and climate-optimized interfaces that support improved temperature, humidity, and air-quality management inside the vehicle cabin. Rising EV production further drives demand for refined digital control solutions.

Rest of the World

The rest of the world is experiencing a steady automotive control panel market growth driven by expanding vehicle ownership and the gradual adoption of digital cockpit features in mid-range models. Rising assembly operations and improving supply chains support demand for modern control panels, although overall market share remains smaller compared to Asia Pacific, North America, and Europe.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Reshaping the Software-Defined Interior Ecosystem

The global automotive control panel market is moderately concentrated and highly innovation-driven, with leading Tier-1 suppliers, display specialists, and semiconductor partners shaping next-generation digital cockpits. Key players are competing on integrated HMI platforms, advanced control technologies, domain controllers, and display systems that blend instrument clusters, center consoles, and rear-seat interfaces into unified software-defined experiences. Several manufacturers are also embedding temperature, humidity, and air-quality management systems within cockpit architectures to address rising expectations around indoor air quality and compliance with environmental regulations, especially in the Asia Pacific.

Bosch and Continental focus on cockpit integration platforms that consolidate infotainment, driver information, air-quality monitoring, and ADAS visualization into central compute units, often built on high-performance automotive SoCs. Visteon and Harman are pushing digital cockpit domain controllers, Android-based infotainment, and upgradeable platforms that address the increasing demands for more capable, connected cabins. Display leaders such as LG Display and Panasonic are expanding portfolios of curved, pillar-to-pillar, transparent, and OLED-based panels tailored for premium interiors. At the same time, Japanese and Korean electronics suppliers strengthen their position through long-term OEM partnerships and scalable module designs. Other notable participants include semiconductor firms and cloud/voice partners that enable graphics, connectivity, and AI-driven personalization, collectively influencing the global environmental control system capabilities integrated within modern cockpits.

- For instance, in January 2024, Bosch and Qualcomm jointly showcased a central vehicle computer that combines digital cockpit and driver-assistance functions on a single SoC, underscoring the shift toward unified, software-defined interior architectures.

LIST OF KEY AUTOMOTIVE CONTROL PANEL COMPANIES PROFILED

- Honeywell International Inc. (U.S.)

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Denso Corporation (Japan)

- Visteon Corporation (U.S.)

- Panasonic Automotive Systems Co., Ltd. (Japan)

- Valeo SE (France)

- Marelli Corporation (Japan)

- Hyundai Mobis Co., Ltd. (South Korea)

- Magna International Inc. (Canada)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Hyundai Mobis revealed M.VICS 5.0, combining a large adaptive display, driver monitoring, haptic controls, and integrated wellness features designed for premium EV interiors.

- April 2025: MediaTek introduced its Dimensity Auto Cockpit Platform C-X1 and Auto Connect MT2739 at Auto Shanghai 2025, targeting intelligent cockpits and integrating generative-AI enhanced interfaces. The platform promises powerful processing for digital instrument clusters, infotainment, and advanced HMI systems, accelerating the shift toward software-defined interiors.

- October 2024: Visteon introduced the latest SmartCore domain controller, enabling integrated cluster, infotainment, and driver monitoring on one consolidated ECU. It supports OTA personalization and reduces wiring complexity for OEMs.

- January 2024: Qualcomm & Bosch central computer for cockpit and ADAS

Qualcomm and Robert Bosch introduced a central vehicle computer at CES 2024 that runs infotainment and advanced driver-assistance functions on a single Snapdragon Ride Flex SoC, enabling software-defined architectures and reducing hardware complexity in digital cockpits. - January 2024: Continental’s Swarovski Crystal Center Display Continental debuted the Crystal Center Display, the first automotive screen fully embedded in a transparent Swarovski crystal housing, using microLED for extreme brightness and contrast, and winning a CES 2024 Innovation Award in vehicle tech and design.

REPORT COVERAGE

The global automotive control panel market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.3% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Technology, Functionality, Vehicle Type, Sales Channel, and Region |

|

By Technology |

· Manual · Digital · Touch-based · Others |

|

By Functionality |

· Center Console Control Panels · HVAC Control Panels · Door Control Panels · Steering-Mounted Control Panels · Instrument Cluster Panels · Others |

|

By Vehicle Type |

· Passenger Cars · Light Commercial Vehicles · Heavy Commercial Vehicles |

|

By Sales Channel |

· OEM · Aftermarket |

|

By Region |

· North America (By Technology, Functionality, Vehicle Type, Sales Channel, and Country) o U.S. o Canada o Mexico · Europe (By Technology, Functionality, Vehicle Type, Sales Channel, and Country) o U.K. o Germany o France o Italy o Rest of Europe · Asia Pacific (By Technology, Functionality, Vehicle Type, Sales Channel, and Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 97.55 billion in 2025 and is projected to reach USD 167.40 billion by 2034.

In 2025, the market value stood at USD 45.64 billion.

The market is expected to exhibit a CAGR of 6.3% during the forecast period of 2026-2034.

The passenger cars segment led the market by vehicle type.

Rising adoption of software-defined and connected cockpits is driving the growth of the automotive control panel market.

Bosch, Continental, Honeywell, and Hyundai Mobis are some of the prominent players in the market.

Asia-Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us