Automotive Domain Controller Market Size, Share & Industry Analysis, By Domain (Powertrain, Body & Chassis, Infotainment, and ADAS), By Vehicle Type (Passenger Cars and Commercial Vehicles), By Propulsion (Electric and IC Engine), By Application (Active Safety, Body Control, User Experience, and Powertrain Management), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

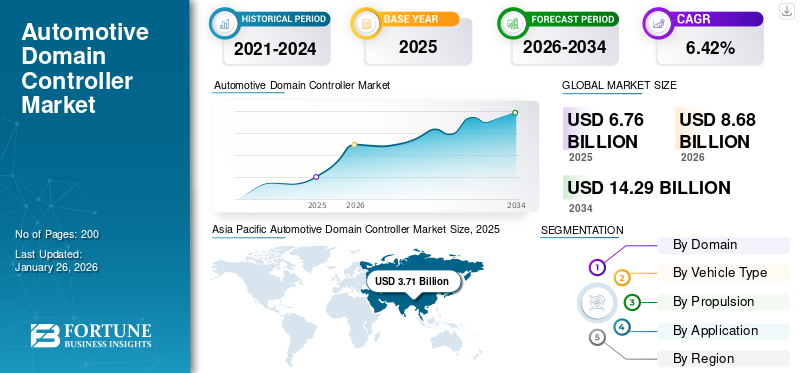

The global automotive domain controller market size was valued at USD 6.76 billion in 2025. The market is projected to grow from USD 8.68 billion in 2026 to USD 14.29 billion by 2034, exhibiting a CAGR of 6.42% from 2026-2034. Asia Pacific dominated the automotive domain controller market with a market share of 54.81% in 2025.

An automotive domain controller is a advanced Electrical/Electronic (E/E) architecture system utilized in modern vehicles, including cars and commercial trucks. This computing unit manages a range of features and functions specific to vehicle domains, such as advanced driver assistance systems (adas), cockpit systems, and body controls. By consolidating multiple electronic control units (ECUs) into fewer central units, domain controllers enhance efficiency, reduce the physical space for electronic components and minimize costs associated with raw material usage. This evolution in vehicle architecture addresses the growing complexity of automotive systems.

The COVID-19 pandemic profoundly impacted the global Automotive Domain Controller (DCU) market, causing disruptions in supply chains and a decline in consumer demand. As automotive production slowed due to factory shutdowns and restrictions, the DCU market, which relies heavily on the availability of semiconductor components and advanced software, faced significant delays. The shortage of semiconductor chips, a critical component in DCUs, reduced vehicle production globally, particularly affecting the launch of new vehicles with advanced infotainment and autonomous driving features. By 2024, market began to show signs of recovery, driven by the transition toward electrified and autonomous vehicles, which fueled the demand for DCUs. The rising importance of software and data processing capabilities in vehicles is helping the market, as automakers focus on offering superior connectivity, safety features, and driver assistance technologies.

Download Free sample to learn more about this report.

AUTOMOTIVE DOMAIN CONTROLLER MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 6.76 billion

- 2026 Market Size: USD 8.68 billion

- 2034 Forecast Market Size: USD 14.29 billion

- CAGR: 6.42% from 2026–2034

- Asia Pacific dominated the automotive domain controller market with a market share of 54.81% in 2025.

- The IC engine segment will account for 83.26% market share in 2026.

North America

North America contributed 22.39% to the global market in 2025, with a valuation of USD 1.51 billion, and is projected to reach USD 1.93 billion in 2026.

Europe

Europe accounted for USD 1.33 billion in 2025, representing 19.67% of the global market share, and is projected to reach USD 1.7 billion in 2026.

Asia Pacific

The Asia Pacific market was valued at USD 3.71 billion in 2025, capturing 54.81% of global revenue, and is estimated to reach USD 4.77 billion in 2026.

U.S.

The U.S. market is likely to be accounted for a value of USD 1.3 billion in 2026.

Japan

Japan is likely to hit USD 0.62 billion in 2026.

Read More

Automotive Domain Controller Market Trends

Shift Toward Centralized Zonal Architecture is a Current Trend

A significant trend shaping the global automotive domain controller market growth is transitioning from traditional ECU-based designs to centralized zonal architectures. This approach organizes vehicle functionalities into zones based on physical proximity (e.g., front, rear, left, right), with domain controllers managing each zone, replacing the need for dedicated ECU for every function. This shift addresses the growing complexity of vehicle electronic systems as vehicles become more connected, autonomous, and electrified.

Traditional vehicle architectures often include up to 100 ECUs, resulting in complex wiring harnesses and higher system weight. Zonal architectures consolidate these ECUs into fewer, more powerful domain controllers that manage multiple systems within a specific vehicle zone. This reduces wiring length, system weight, and costs, making vehicles lighter and more energy-efficient—critical advantage for electric vehicles (EVs). For example, BMW is adopting zonal architectures for its next-generation EV platforms, streamlining design and improving scalability.

Moreover, zonal architectures enable OEMs to scale vehicle platforms more efficiently using standardized hardware across models, while differentiating features via software. This scalability is essential for manufacturers developing modular EV platforms, such as Hyundai’s E-GMP and Volkswagen’s MEB, which rely on zonal domain controllers to support diverse vehicle configurations and market requirements.

Download Free sample to learn more about this report.

LATEST OPPORTUNITY

Rapid Electric Vehicle (EV) Expansion Presents a Major Opportunity to Market Players

EVs rely heavily on advanced electronic architectures to manage complex systems, including battery management, powertrain optimization, thermal control, and infotainment. Domain controllers are ideally suited to meet the requirements of EV platforms due to their ability to centralize and optimize system performance while reducing the overall complexity of electrical and electronic systems.

High-voltage batteries and power electronics in EVs require precise management to safety, efficiency, and longevity. Domain controllers simplify this process by integrating functions such as battery management systems (BMS), motor control units, and energy recovery systems into a centralized computing platform. For example, Tesla’s Model 3 and Model Y platforms employ centralized domain controllers to manage their battery and powertrain systems, enabling real-time energy usage and thermal management optimization.

As OEMs increasingly adopt modular EV platforms, domain controllers provide scalability to support diverse vehicle models and configurations. Platforms such as Hyundai’s E-GMP and Volkswagen’s MEB leverage domain controllers to standardize architectures while allowing customization for specific vehicle types. This approach reduces development costs and accelerates time-to-market, making it crucial for OEMs targeting for mass-market EV adoption.

Automotive Domain Controller Market Growth Factors

Increasing Integration of Advanced Driver Assistance Systems (ADAS) and Autonomous Driving (AD) Features Drives Market Growth

The rapid advancements of ADAS and autonomous driving technologies is a key driver for the growth of the global market. As vehicles become increasingly intelligent, the traditional Electronic Control Unit (ECU)-based architecture faces challenges in managing the complexity of modern automotive electronics. Domain controllers, which consolidate multiple ECUs into a centralized architecture, have emerged as a solution to handle the computational demands and ensure seamless integration of ADAS and autonomous driving systems.

ADAS features, such as adaptive cruise control, lane-keeping assistance, and automatic emergency braking, require real-time data processing from various sensors, including cameras, LiDAR, and radar. Domain controllers are efficiently process this high-volume data efficiently and make quick decisions, ensuring safety and performance. For example, the Volkswagen Group has incorporated domain controllers supplied by Continental AG supplied into its MEB electric vehicle platform, enabling Level 2 and 3 autonomous driving functions.

As automakers progress toward higher levels of automation (Levels 3–5), domain controllers becomes plays a critical role. They offer the scalability needed to integrate advanced software algorithms, artificial intelligence (AI), and machine learning models. For instance, Tesla’s Full Self-Driving (FSD) system leverages a centralized architecture akin to a domain controller to handle its neural network-based autonomous driving capabilities.

RESTRAINING FACTORS

High Development and Integration Costs to Restrain Market Growth

One of the key significant challenges restraining the growth of the global automotive domain controller market is the high development and integration costs associated with these advanced systems. Domain controllers represent a shift from traditional ECU-based architectures to centralized computing platforms, necessitating significant investment in hardware, software, and system integration.

Domain controllers rely on advanced processors, GPUs, and specialized microchips to handle the computational needss of modern vehicles, particularly those equipped with advanced driver assistance systems (ADAS) or autonomous driving features. The cost of designing, testing, and manufacturing these high-performance components is substantial. For instance, the NVIDIA DRIVE Orin platform, widely adopted by OEMs such as Mercedes-Benz and Volvo, costs significantly more than traditional ECUs due to its advanced capabilities and AI processing power.

The software ecosystem for domain controllers is equally complex and expensive to develop. It involves writing millions of lines of code to manage tasks ranging from ADAS to infotainment and connectivity. This complexity requires extensive validation and testing to meet safety standards such as ISO 26262 for functional safety. According to Bosch, one of the leading players in the market, the cost of software development for domain controllers can account for up to 40% of the total cost of the system.

Automotive Domain Controller Market Segmentation Analysis

By Domain Analysis

ADAS Segment Lead due to Increasing Demand for Autonomous Vehicles

Based on domain, the market is segmented into powertrain, body & chassis, infotainment, and ADAS.

The ADAS segment is projected to dominate the market with a share of 51.82% in 2026, primarily driven by the growing demand for autonomous and semi-autonomous driving technologies. ADAS functions such as adaptive cruise control, lane-keeping assist, automatic emergency braking, and collision avoidance are essential for enhancing vehicle safety. Centralizing these functions into domain controllers allows faster, more reliable data processing from essential sensors such as cameras, radar, and LiDAR, which are vital for enabling driver assistance features. For example, in 2023, Tesla’s Full Self-Driving (FSD) system utilized a powerful domain controller that integrates data from multiple sensors to provide enhanced safety and driver-assistance features. Tesla’s approach to using a central computing platform for ADAS allows for real-time decision-making and constant updates via over-the-air software improvements.

The infotainment segment is anticipated to register the fastest growth rate over the forecast period. The growth of this segment is credited to the increasing demand for advanced infotainment and cockpit domain controller market systems that provide drivers real-time vehicle data, such as vehicle conditions, entertainment, and other features. Domain controllers are highly suited to handle multiple functions, making them integral as connected systems become standard in modern vehicles.

The powertrain and body & chassis segments are also expected to witness a noteworthy growth. The growing focus of automakers on predictive technology and improving in-vehicle experience are the primary factors responsible for the growth of these segments during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type Analysis

Passenger Cars Dominated Due to Rising Demand for Connected Technologies

Based on vehicle type, the market is segmented into passenger cars and commercial vehicles.

The passenger cars segment held the largest market share and is estimated to retain its dominance throughout the forecast period. This growth is driven by consumer demand for connected and autonomous technology that enhance the driving experience. Moreover, the increased disposable income of consumers and higher production rates contribute to the high demand for passenger cars. The passenger cars segment is expected to lead the market, contributing 89.02% globally in 2026.

The commercial vehicle segment is expected to register a CAGR of 14.60% during the forecast period, owing to the increased integration of connected technology in light commercial vehicles, such as utility trucks, cargo vans, and pick trucks. Various commercial vehicle fleet owners are recognizing the importance of fleet tracking and telematics systems, which require high computational power to carry out various functions and optimize the efficiency of operations. Additionally, the growing focus on optimizing fleet management operations is likely to contribute to the segment’s growth.

By Propulsion Analysis

IC Engines Segment Led due to Well-established Infrastructure for Conventional Cars

Based on propulsion, the market is segmented into electric and IC engine.

The IC engine segment will account for 83.26% market share in 2026. The IC engine segment held a major market share and is estimated to hold its dominance throughout the forecast period. The high reliability of IC engines and well-supported technology and infrastructure suitable for conventional cars will contribute to the segment’s growth. Additionally, while the electrification of vehicles is evolving at a rapid pace, the lack of robust EV infrastructure in many economies continues to encourage consumer preference for IC engine vehicles over electric ones.

The electric segment is expected to register a CAGR of 19.50% during the forecast period owing to the increasing emphasis of automakers, governments, and consumers on carbon neutrality and reducing the global carbon footprint. Moreover, electric vehicles require more electrical components that come with safety and monitoring functions, such as range, battery capacity, battery management software, and various other features. These few factors are expected to augment the demand for these controllers in the future as more EVs roll out on the roads.

By Application Analysis

Active Safety Applications Dominated Due to Rising Need for Safer Driving Experience

Based on application, the market is segmented into active safety, body control, user experience, and powertrain management.

The Active Safety segment is expected to account for 57.24% of the market in 2026. The growth of active safety applications is dominating and driving the expansion of the automotive domain controller market by prompting automakers to invest in integrated systems capable of managing complex sensor data in real-time. Increasing pressure from governments and regulatory bodies to improve road safety has led to a shift toward domain controllers, which centralize these safety systems, improve reliability, and reduce the number of ECUs in vehicles. The widespread adoption of active safety features, along with advances in sensor technologies and data processing capabilities, is accelerating the growth of the segment.

Integrating infotainment, navigation, and voice control systems has made user experience a key focus for automakers. The growth of these applications is tied directly to domain controllers, which ensure seamless operation of all onboard digital systems. Manufacturers such as Hyundai and Ford are investing in these controllers to enhance the driving experience. This emphasis on connectivity and user engagement necessitates more advanced domain controllers, further propelling and contributing to the market growth.

The body control and powertrain management segments are also expected to grow considerably owing to the increased focus of automakers on achieving a more streamlined E/E architecture in the vehicle. The powertrain management segment is projected to exhibit a CAGR of 12.50% during the forecast period.

REGIONAL INSIGHTS

In terms of region, the market is categorized into Europe, North America, the Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Automotive Domain Controller Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The Asia Pacific market was valued at USD 3.71 billion in 2025, capturing 54.81% of global revenue, and is estimated to reach USD 4.77 billion in 2026. Asia Pacific is the dominant and fastest-growing region in the global market due to its large automotive manufacturing base, rapid adoption of electric vehicles (EVs), and strong push for smart, connected mobility solutions. The region led the largest market value of USD 3.71 billion in 2025, and in 2026, the region led the value of USD 4.77 billion. Key automotive manufacturers, including Toyota, Honda, and Hyundai, are embracing centralized domain controllers to integrate the growing number of sensors, electric powertrains, and vehicle safety systems. This trend is especially prevalent in markets such as China, Japan, and South Korea, with a strong push toward sustainability, EV adoption, and autonomous driving. The market in China is expected to account for USD 2.23 billion in 2026. India is projected to be USD 0.5 billion and Japan is likely to hit USD 0.62 billion in 2026.

North American

North America contributed 22.39% to the global market in 2025, with a valuation of USD 1.51 billion, and is projected to reach USD 1.93 billion in 2026. North American automotive manufacturers, including Ford, General Motors, and Tesla are heavily investing in innovative vehicle technologies such as electric and autonomous driving systems, which rely on sophisticated domain controllers to integrate multiple vehicle functions. The region is expected to be the second-largest market with a value of USD 1.51 billion in 2025, with the second-fastest CAGR of 10.10% during the forecast period. Additionally, the growing emphasis on vehicle safety has propelled the adoption of advanced driver assistance systems (ADAS), a trend supported by governmental regulations to enhance road safety standards. The U.S. market is likely to be accounted for a value of USD 1.3 billion in 2026.

Europe and the Rest of the World

Europe and the Rest of the World also held decent shares in the global market in 2025. The high demand for advanced road and driver safety systems and stringent laws for road and traffic safety is expected to increase the adoption of these controllers for ADAS. Europe accounted for USD 1.33 billion in 2025, representing 19.67% of the global market share, and is projected to reach USD 1.7 billion in 2026. The U.K. market is likely to be USD 0.08 billion in 2026. On the other hand, Germany is likely to reach USD 0.4 billion in 2026 and France is projected to be USD 120 million in 2025.

The Rest of the World is also expected to grow considerably, owing to higher demand for connected autonomous technology in the Middle Eastern countries. The Rest of the World region captured 3.10% of the global market in 2025, generating USD 0.21 billion in revenue, and is projected to reach USD 0.29 billion in 2026.

KEY INDUSTRY PLAYERS

Major Market Players to Focus On New Product Launches to Meet Unique Computing Needs

The competitive landscape of the market is characterized by well-established players and high competition. The market is consolidated with, with all major companies maintaining a strong presence in the automotive and domain controller industry. Organizations such as Aptiv, Renesas, and Continental are actively introducing these controllers to their product offerings, recognizing the shift toward centralized computing E/E architecture.

Few other players, such as Ambarella and Samsung, are collaborating to develop advanced domain controllers to meet the unique computing needs of next-generation EVs and conventional vehicles. Companies are also introducing domain controllers specially designed for ADAS, one of the primary segments driving the demand for these controllers. Thus, major companies are constantly vying for market share through mergers and new product launches.

List of Top Automotive Domain Controller Companies:

- STMicrocontrollers (Switzerland)

- Visteon Corporation (U.S.)

- Infineon Technologies (Germany)

- Robert Bosch GmbH (Germany)

- Aptiv PLC (Ireland)

- Renesas (Japan)

- Texas Instruments (U.S.)

- Panasonic Corporation (Japan)

- Nxp Semiconductors (Netherlands)

- Continental AG (Germany)

- Monolithic Power Systems (Japan)

- Valeo (France)

KEY INDUSTRY DEVELOPMENTS:

- December 2024- Panasonic Automotive Systems collaborated with Arm team on SDV standardization. The two companies would adopt and extend a device virtualization framework, shifting from a hardware-centric to a software-first model to speed up automotive industry development cycles.

- August 2024- Elektrobit collaborated with Chinese new energy vehicle maker NETA Auto and Hirain Technologies (HIRAIN) to develop NETA Auto's first integrated gateway domain controller project, the Haozhi Supercomputer XPC-S32G platform. The project features a service-oriented architecture (SOA) software design within an electronic/electrical architecture (EEA) framework.

- January 2023: Harman International Inc., an automotive technology supplier, showcased its new platform, Ready Upgrade, which includes fully upgradable hardware and software product lines. It also features three families of OEM-grade cockpit domain controllers, advanced software, and other products.

- January 2023: Ambarella, one of the leading companies in automotive E/E architecture, expanded its domain controller product family by introducing a new AI-based domain controller. The controller is designed to carry out numerous ADAS and autonomous driving technology functions.

- June 2022: Valeo and BMW Motors signed a contract for the supply of ADAS domain controllers, enabling BMW vehicles to map and understand their surroundings in real-time, enhancing the vehicle’s advanced ADAS functions.

REPORT COVERAGE

The automotive domain controller market forecast report provides a detailed market analysis and focuses on key aspects, such as leading companies, product types, and key product applications. Besides this, it offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.42% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Domain

By Vehicle Type

By Propulsion

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market was valued at USD 8.68 billion in 2026 and is projected to reach USD 14.29 billion by 2034.

The market is expected to register a growth rate (CAGR) of 6.42% during the forecast period.

Increasing integration of Advanced Driver Assistance Systems (ADAS) and autonomous driving features are expected to drive market growth.

Asia Pacific dominated the automotive domain controller market with a market share of 54.81% in 2025.

Active safety applications is the leading application of domain controllers in the global market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us