Automotive Embedded System Market Size, Share & Industry Analysis, By Type (Hardware and Software), By Vehicle Type (Hatchback/Sedan, SUV, Light Duty Vehicle, and Heavy Duty Vehicle), By Application (Powertrain & Energy Management, Chassis & Body Electronics, Safety & Driver Assistance, Infotainment & Human-Machine Interface (HMI) and Connectivity & Telematics), By Propulsion (ICE, HEV, and EV), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

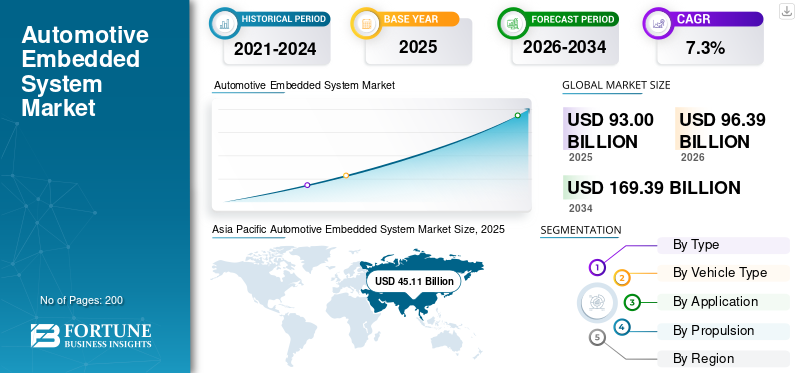

The global automotive embedded system market size was valued at USD 93.00 billion in 2025. The market is projected to grow from USD 96.39 billion in 2026 to USD 169.39 billion by 2034, exhibiting a CAGR of 7.3% during the forecast period. Asia Pacific dominated the global market with a market share of 48.51% in 2025.

The market refers to the global industry focused on the design, development, integration, and commercialization of dedicated hardware & software systems embedded within vehicles to perform specific control, monitoring, communication, and safety functions. These systems consist of microcontrollers, sensors, actuators, embedded software, and Real-Time Operating Systems (RTOS) that collectively enable vehicle functionalities such as powertrain control, body electronics, infotainment, Advanced Driver Assistance Systems (ADAS), and vehicle networking.

The growth of the market is primarily driven by increasing vehicle electrification, rising adoption of ADAS and autonomous driving technologies, and growing consumer demand for enhanced safety, comfort, and connectivity features. Regulatory mandates related to vehicle safety and emissions, such as mandatory electronic stability control, advanced braking systems, and real-time diagnostics, are further accelerating embedded system integration. Additionally, the shift toward software-defined vehicles, over-the-air (OTA) updates, and connected car ecosystems is increasing the complexity and content value of embedded electronics per vehicle, thereby acting as a key market growth driver across both passenger car and commercial vehicle segments.

The automotive embedded system market is moderately consolidated, with major OEMs and Tier-1 suppliers investing in predictive analytics platforms. Some of the leading companies are Continental AG, Bosch, Delphi Technologies, Siemens Mobility, Garrett Motion, and ZF Friedrichshafen. Cloud-based maintenance platforms, AI-enabled diagnostic software, and collaboration with automotive manufacturers is the primary focus of these companies to increase product supply. Pitstop, Noregon Systems, and Uptake Technologies are upcoming companies that are providing machine-learning-based solutions with real-time vehicle health insights.

Download Free sample to learn more about this report.

Automotive Embedded System Market Key Takeaways

- 2025 Market Size: USD 93.00 billion

- 2026 Market Size: USD 96.39 billion

- 2034 Forecast Market Size: USD 169.39 billion

- CAGR: 7.3% from 2026–2034

- Asia Pacific dominated the automotive embedded system market with a 48.51% share in 2025.

- The powertrain and energy management segment is expected to witness the fastest growth at a CAGR of 8.3% during the forecast period.

- The HEV segment is projected to record the highest growth rate, expanding at a CAGR of 8.9% over the forecast period.

Asia Pacific

Asia Pacific remains the leading regional market, supported by high vehicle production, growing EV adoption, and increasing integration of connected vehicle technologies across major automotive manufacturing hubs.

North America

North America benefits from strong demand for ADAS, infotainment, and connected vehicle solutions, supported by the presence of leading OEMs, semiconductor companies, and technology providers.

Europe

Europe continues to witness steady growth due to stringent emission regulations, advanced vehicle safety standards, and increasing deployment of embedded systems in premium and mid-range vehicles.

U.S.

The market is driven by rising adoption of software-defined vehicles, advanced driver assistance systems, and high consumer demand for connected mobility features.

Japan

Strong automotive manufacturing capabilities, rapid adoption of intelligent vehicle technologies, and continued investment in hybrid and electric vehicle development support market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Integration of ADAS and Vehicle Safety Technologies Drive Market Growth

The rising integration of Advanced Driver Assistance Systems (ADAS) and vehicle safety technologies is a major driver for the automotive embedded system market growth, as automakers increasingly prioritize safety, automation, and regulatory compliance. ADAS functionalities such as adaptive cruise control, lane departure warning, forward collision avoidance, automatic emergency braking, and driver monitoring systems rely on complex embedded architectures that integrate sensors, Electronic Control Units (ECUs), and real-time embedded software. The growing adoption of these systems is driven by stringent safety regulations globally, including mandatory safety features and higher crash-test rating requirements across key automotive markets. Additionally, increasing consumer demand for enhanced driving safety and convenience, particularly in passenger vehicles, is prompting OEMs to offer ADAS features across mid-range and entry-level models. Technological advancements in sensor fusion, artificial intelligence, and high-performance computing platforms are further increasing the embedded content per vehicle.

- In June 2025, Mahindra & Mahindra introduced Level 2 Advanced Driver Assistance Systems (ADAS) in the Scorpio-N. In addition, the company has launched a new Z8T variant, enhancing the appeal and accessibility of the premium Z8 range. The company also introduced Level 2 ADAS in the premium Z8L variant with features such as:

- Forward Collision Warning

- Automatic Emergency Braking

- Adaptive Cruise Control with Stop & Go

- Smart Pilot Assist

- Lane Departure Warning

- Lane Keep Assist

- Traffic Sign Recognition

- High Beam Assist

MARKET RESTRAINTS

Semiconductor Supply Chain Volatility and Component Shortages May Limit Market Growth

Semiconductor supply chain volatility and persistent component shortages represent a significant restraint for the market, directly affecting production continuity and technology adoption. Automotive embedded systems rely heavily on automotive-grade microcontrollers, processors, memory chips, sensors, and power management ICs, all of which require long qualification cycles and strict reliability standards. Disruptions caused by geopolitical tensions, trade restrictions, natural disasters, and capacity constraints at semiconductor foundries have led to extended lead times and fluctuating component prices. These challenges disproportionately affect the automotive sector due to its lower prioritization compared to consumer electronics in semiconductor allocation. As a result, OEMs and Tier 1 suppliers face delays in vehicle production, deferred launches of embedded-intensive features such as ADAS, and increased procurement costs. Despite long-term investments in localized manufacturing and supply chain diversification, semiconductor volatility continues to act as a structural restraint on automotive embedded system market growth.

MARKET OPPORTUNITIES

Expansion of Connected Vehicle and Over-the-Air (OTA) Update Ecosystems Create Growth Prospects

The expansion of connected vehicle technologies and over-the-air (OTA) update ecosystems represents a significant market opportunity, as vehicles function as digitally connected platforms. Embedded systems play a critical role in enabling real-time data exchange, vehicle-to-cloud communication, telematics, infotainment, and remote diagnostics. The growing adoption of OTA updates allows OEMs to remotely deploy software enhancements, security patches, and feature upgrades without requiring physical service interventions, significantly improving vehicle lifecycle management and customer experience. This shift is driving demand for secure, high-performance embedded processors, middleware, and communication modules capable of supporting continuous connectivity and data integrity. Additionally, OTA-enabled architectures enable automakers to introduce subscription-based features and post-sale monetization models, expanding revenue opportunities. As cybersecurity requirements and data volumes increase, embedded system providers offering robust encryption, secure boot, and update management capabilities are expected to gain a competitive advantage. Overall, the rapid expansion of connected and OTA-enabled ecosystems is strengthening the strategic importance of embedded systems in modern vehicles.

AUTOMOTIVE EMBEDDED SYSTEM MARKET TRENDS

Increasing Use of Automotive Operating Systems and Middleware Standardization

The increasing adoption of automotive operating systems and middleware standardization is a key market trend shaping the automotive embedded system market, as OEMs seek to manage growing software complexity and improve development efficiency. Standardized automotive operating systems and middleware platforms enable seamless communication between hardware components, application software, and vehicle networks, reducing dependency on proprietary solutions. This approach supports greater software reuse across vehicle platforms and model variants, significantly lowering development time and costs. Additionally, standardized middleware facilitates easier integration of advanced functionalities such as ADAS, connectivity, and OTA updates while ensuring compliance with functional safety and cybersecurity requirements.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Hardware Segment’s Dominance Driven by Rising Electronic Content and Critical Role of Automotive Grade Components

On the basis of type, the market is classified into hardware and software.

The hardware segment dominates the automotive embedded system market share due to the critical role of physical components in vehicle functionality and safety. Automotive embedded hardware includes microcontrollers (MCUs), microprocessors (MPUs), sensors, actuators, memory devices, and communication ICs, all of which are essential for executing real-time control and monitoring functions. This dominance is driven by the increasing electronic content per vehicle, particularly with the rising adoption of ADAS, electrification, and connected vehicle technologies. Advanced applications such as radar-based safety systems, Battery Management Systems (BMS), and centralized vehicle computing platforms require high-performance, automotive-grade hardware with stringent reliability and safety certifications.

The software segment is poised to grow at the fastest CAGR of 8.1% over the analysis period.

By Vehicle Type

SUVs Dominate Driven by Premium Positioning and High Integration of Advanced Embedded Technologies

In terms of vehicle type, the market is categorized into hatchback/sedan, SUV, light duty vehicle, and heavy duty vehicle.

SUVs dominate the automotive embedded system market share by vehicle type, owing to their higher average selling price, premium positioning, and greater integration of advanced electronic features. SUVs typically incorporate a wide range of embedded systems, including advanced ADAS, multi-zone infotainment, digital cockpits, powertrain control modules, and connectivity solutions. Consumer preference for safety, comfort, and intelligent driving features has led OEMs to prioritize SUVs for the deployment of next-generation embedded technologies.

- Tesla launched a pilot for its unsupervised FSD service in Austin, Texas, in June 2025. This initiative is underpinned by continued advancements in their AI and embedded systems, including hardware 4.0 (AI4) FSD components and a new front bumper camera in updated vehicles for better environmental awareness.

The SUV segment is poised to depict a CAGR of 8.0%, showcasing the fastest growth over the analysis period.

By Application

Dominance of Powertrain and Energy Management Applications Driven by Electrification and Emission Compliance Requirements

Based on application, the market is segmented into powertrain & energy management, chassis & body electronics, safety & driver assistance, infotainment & Human-Machine Interface (HMI), and connectivity & telematics.

Powertrain and energy management dominate the market due to their critical role in vehicle performance, efficiency, and regulatory compliance. Embedded systems in this segment control engine management, transmission systems, Battery Management Systems (BMS), power electronics, and thermal management across ICE, hybrid, and electric vehicles. The growing adoption of electrified powertrains has significantly increased the complexity and value of embedded controllers, sensors, and real-time software required for energy optimization and safety. Stringent emission and fuel-efficiency regulations further drive demand for precise electronic control systems.

The powertrain and energy management segment is poised to grow at a CAGR of 8.3%, showcasing the fastest growth over the analysis period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion

Dominance of is ICE Propelled by Large Installed Base and Regulatory-Driven Powertrain Optimization

Based on propulsion, the market is segmented into ICE, EV, and HEV.

The ICE segment continues to dominate the automotive embedded system market due to the large global installed base of conventional vehicles and their ongoing production across both developed and emerging markets. Embedded systems in ICE vehicles are extensively used for Engine Control Units (ECUs), transmission control, fuel injection, ignition timing, emission monitoring, and on-board diagnostics. Stringent emission regulations and fuel-efficiency standards are compelling OEMs to deploy increasingly sophisticated embedded controllers and sensors to optimize combustion and reduce pollutants.

- In March 2024, Toyota introduced updated Internal Combustion Engine (ICE) variants for the Corolla and Camry models. These vehicles feature enhanced embedded engine management systems designed to meet tightening regulatory standards. This allows for continuous monitoring of engine health and performance. This optimizes fuel delivery for efficiency and reduced emissions.

The HEV segment is poised to grow at a CAGR of 8.9%, showcasing the fastest growth over the analysis period.

Automotive Embedded System Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Embedded System Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the automotive embedded system market due to high vehicle production volumes, rapid technology adoption, and expanding automotive manufacturing bases across China, Japan, South Korea, and India. The region benefits from strong demand for both passenger and commercial vehicles, coupled with increasing integration of embedded systems across mass-market and premium segments. China, in particular, is driving growth through aggressive adoption of electric vehicles, connected car platforms, and intelligent cockpit technologies.

- For instance, in August 2024, BYD launched the updated Song Plus DM-i in China, integrating advanced embedded ADAS features such as adaptive cruise control, lane-keeping assist, and an intelligent infotainment system powered by a centralized embedded computing platform features increasingly offered in mid-range price segments.

North America

North America represents a technologically advanced market for automotive embedded systems, driven by strong adoption of ADAS, connected vehicle technologies, and software-defined vehicle architectures. The region benefits from the presence of leading OEMs, Tier 1 suppliers, and semiconductor companies, particularly in the U.S. High consumer demand for safety, infotainment, and connectivity features especially in SUVs and pickup trucks continues to support embedded system integration.

Europe

Europe is a key market for automotive embedded systems, driven by stringent emission regulations, advanced safety mandates, and strong penetration of premium and mid-range vehicles with high electronic content. European OEMs are at the forefront of deploying embedded systems for powertrain optimization, ADAS, and centralized vehicle architectures. The region’s early adoption of functional safety and cybersecurity standards further supports demand for sophisticated embedded software and hardware.

Rest of the World

The rest of the world, including Latin America and the Middle East & Africa, represents an emerging market for automotive embedded systems. Growth in these regions is primarily driven by gradual increases in vehicle production, rising safety awareness, and improving regulatory frameworks.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Embedded Computing, Software Platforms, and Cloud Alliances Reshaping Competition

The automotive embedded system market is dominated by leading Tier-1 suppliers and technology companies such as Bosch Mobility Solutions, Continental AG, ZF Friedrichshafen AG, Siemens, NXP Semiconductors, Renesas Electronics, and Qualcomm. These players offer integrated embedded hardware, software platforms, and middleware supporting powertrain control, ADAS, connectivity, and infotainment applications. Competitive differentiation is driven by strong OEM partnerships, investments in software-defined vehicle architectures, and capabilities in functional safety and cybersecurity.

A key competitive lever is Software-Defined Vehicle (SDV) readiness, where players bundle embedded hardware with standardized software layers to reduce OEM integration burden. For instance, Bosch and Microsoft have focused on a vehicle-to-cloud software platform approach aimed at reducing integration complexity and enabling OTA updates at fleet scale. Meanwhile, Continental has emphasized cloud-based development and virtualization approaches to speed embedded software cycles for high-performance vehicle computers.

LIST OF KEY AUTOMOTIVE EMBEDDED SYSTEM COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Denso Corporation (Japan)

- Aptiv PLC (Ireland)

- Valeo SA (France)

- Magna International Inc. (Canada)

- Hitachi Astemo Ltd. (Japan)

- Hyundai Mobis (South Korea)

- Forvia (Faurecia + HELLA) (France)

- NXP Semiconductors (Netherlands)

- Infineon Technologies AG (Germany)

- Texas Instruments Incorporated (U.S.)

- Renesas Electronics Corporation (Japan)

- STMicroelectronics (Switzerland)

- Vector Informatik GmbH (Germany)

- Wind River Systems (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: General Motors announced that select 2025 and 2026 Cadillac and Chevrolet vehicles will soon receive native Apple Music integration directly in their infotainment systems via an over-the-air (OTA) update. This enhancement reflects broader trends in automotive embedded systems where automakers are increasingly embedding rich multimedia apps and connected services directly into vehicle software ecosystems.

- December 2025: Nissan announced plans to develop a Tesla-like camera-based autonomous driving system, partnering with AI specialist Wayve, targeting a launch on models such as Armada, Pathfinder, and Rogue by 2028 highlighting future embedded ADAS and AI software integration.

- July 2024: Volkswagen launched updated Golf featuring new embedded content primarily through an upgraded electronic architecture, including the MIB4 (Modular Infotainment Matrix, generation 4) infotainment system and the integration of new ADAS. The hardware and software of the infotainment systems are completely new, based on the fourth-generation MIB platform. This delivers faster performance and improved stability for functions such as navigation, App-Connect, streaming, and air conditioning control.

- May 2025: XPENG launched MONA M03 Max, an all-electric hatchback sedan, offering advanced ADAS and premium features at an accessible price point of USD 20,000 in the Chinese EV market.

- January 2024: Hyundai introduced the refreshed Creta for India equipped with Level 2 ADAS, a digital cockpit, and enhanced embedded infotainment and connectivity systems, marking a significant upgrade in embedded content for a high-volume mid-range SUV.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.3% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Vehicle Type, Application, Propulsion, and Region |

|

By Type |

· Hardware · Software |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · Light Duty Vehicle · Heavy Duty Vehicle |

|

By Application |

· Powertrain & Energy Management · Chassis & Body Electronics · Safety & Driver Assistance · Infotainment & Human-Machine Interface (HMI) · Connectivity & Telematics |

|

By Propulsion |

· ICE · EV · HEV |

|

By Geography |

· North America (By Type, Vehicle Type, Application, Propulsion, and Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Type, Vehicle Type, Application, Propulsion, and Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Type, Vehicle Type, Application, Propulsion, and Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Type, Vehicle Type, Application, Propulsion, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 93.00 billion in 2025 and is projected to reach USD 169.39 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 45.11 billion.

The market is expected to exhibit a CAGR of 7.3% during the forecast period.

The SUV segment led the market by vehicle type.

Rising integration of ADAS and vehicle safety technologies drive market growth.

Asia Pacific dominated the market in 2025 in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us