Automotive Fuel Filter Market Size, Share & Industry Analysis, By Filter Type (Inline Fuel Filters, Cartridge Fuel Filters, Spin-on Fuel Filters, and In-tank Fuel Filters), By Vehicle Type (Two Wheeler, Passenger Cars, and Commercial Vehicles), By Distribution Channel (OEM, and Aftermarket), By Fuel Type (Petrol/Diesel and Gas), By Material (Synthetic Fiber, Cellulose/Paper, and Composite/Nano), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

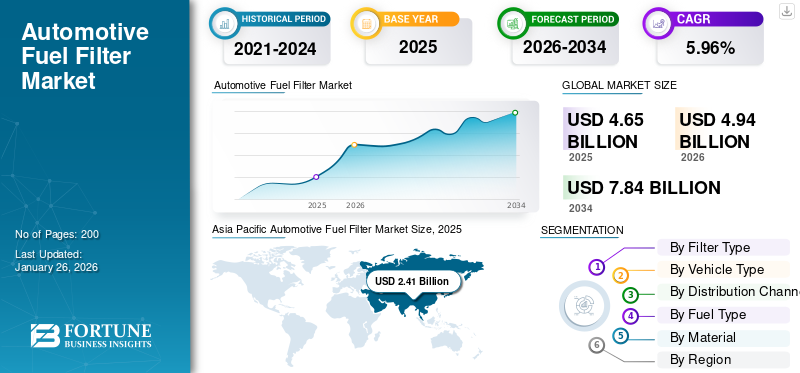

The global automotive fuel filter market size was valued at USD 4.65 billion in 2025. The market is projected to grow from USD 4.94 billion in 2026 to USD 7.84 billion by 2034, exhibiting a CAGR of 5.96% during the forecast period. The Asia Pacific dominated the global market, accounting for a 51.85% share in 2025.

Automotive fuel filters are mechanical components that remove particulate contaminants, water, and other impurities from fuel before it reaches the engine’s fuel pump and injectors. Typically placed inline, within a cartridge housing, as a spin-on canister, or inside the fuel tank, they protect precision components and maintain combustion efficiency. Filter materials trap debris while facilitating a controlled flow. They are used across two-wheelers, passenger cars, and commercial vehicles globally. Regular replacement of these filters prevents clogging, preserves fuel-system reliability, and reduces emissions and engine wear.

The market supplies replacement and OEM filtration products to protect internal combustion engines across mature and emerging vehicle fleets. Vehicle parc size, regulatory emission norms, standards, technological shifts to high-pressure direct injection, and the gradual electrification of transport drives the demand for these filters. Suppliers compete on filtration efficiency, OEM fitment, module integration, and supply-chain reliability. Major manufacturers include MANN+HUMMEL, Bosch, MAHLE, DENSO, Hengst, Donaldson (Fleetguard), WIX, Baldwin, Purolator, FRAM, Purflux (Sogefi), Valeo, AISIN, UFI, K&N, ACDelco, NAPA, Sakura, and Champion.

Tariffs on imported filter components or finished assemblies will raise input costs and disrupt just-in-time supply chains, prompting manufacturers to relocate production, increase local sourcing, or pass costs to distributors and consumers. Protective duties can advantage domestic producers but reduce cross-border competition and delay the adoption of advanced or module designs. For global suppliers, tariff volatility increases inventory, hedging, and compliance expenses, complicating long-term contracts. Conversely, low-tariff regimes will support efficient global sourcing, scale economies, and stable aftermarket pricing and margins.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Technical Shift to High-Pressure Fuel Delivery Systems Drives Market Growth

One major driving factors for the global automotive fuel filter market is the rapid technical shift to high-pressure fuel delivery systems. Mainly gasoline direct injection (GDI) and advanced diesel common-rail systems, which demand far finer, more reliable filtration and integrated module designs. As manufacturers fit high-pressure pumps and precision injectors to improve fuel economy and lower tailpipe emissions, fuel filters must remove smaller particulates and water while maintaining low pressure drop; this raises demand for multilayer synthetic and composite media, in-tank modules, and integrated water separators. The pace is measurable: government data show that 73% of light-duty vehicles produced in 2023 were equipped with gasoline direct injection, underscoring the widespread retrofit of precision fuel systems and corresponding filtration needs.

At the same time, electrification trends temper long-term ICE volumes. IEA projections estimates global electric light-duty vehicle sales to be roughly about 40% by 2030. However, near- and mid-term ICE fleets remain large, pertaining the demand for filtration replacement and aftermarket. Recent industry developments illustrate this dynamic, major suppliers are expanding GDI coverage and part ranges to meet service demand, and regulatory tightening, such as Euro 7, is pushing OEMs to adopt cleaner, higher-precision, fuel efficient systems that rely on advanced filtration. For suppliers and distributors, this means rising requirements for higher-efficiency media, greater SKU complexity (in-tank modules vs simple inline elements), and stronger OEM qualification cycles. At the same time, aftermarket channels must keep more differentiated, higher-spec parts to serve modern injectors and pumps. Overall, system electrification reallocates long-term demand, but ongoing GDI/C-rail penetration and regulatory pressure are fueling near-term growth in advanced fuel-filter products.

MARKET RESTRAINTS

Fast and Continual Rise of Electric Vehicles (EVs) Hinders the Market Growth

The single most crucial restraining factor for the market is the rapid and sustained rise of electric vehicles (EVs), which directly reduces the installed base of internal-combustion engines (ICEs) that require fuel filtration and replacement parts. As automakers accelerate EV model launches and policy drivers push fleet electrification, the addressable unit demand for fuel filters (both OEM fitment and aftermarket replacements) progressively shrinks: global battery-electric vehicle sales reached roughly 10.8 million units in 2024, capturing about 14.5% of light-duty vehicle sales, and EV sales are further expected to reach the 20 million-unit annual scale in 2025. That structural substitution lowers long-term replacement cycles, compresses aftermarket volumes per vehicle, and forces filter suppliers to reallocate R&D and production capacity toward fewer ICE platforms or diversify into EV servicing or other filtration niches.

Several large OEM strategies and regulatory debates create regional uncertainty. In contrast, legacy announcements (GM’s 2035 light-vehicle EV target and Ford’s push to all-electric passenger ranges in Europe by 2030) signal long-term ICE decline, industry pushback, and tactical shifts (manufacturers asking for flexible 2035 rules or adjusting EV targets) introduce timing risk for suppliers and distributors. For filter manufacturers, this means they plan for declining unit demand in mature markets, managing inventory and tooling for shrinking ICE platforms, and investing in new product lines, all while protecting margins in the market where volumes and pricing power are likely to erode over the medium term.

MARKET OPPORTUNITIES

Accelerating Shift Toward Higher Biofuel Blends and Alternative Liquid Fuels Generates Beneficial Growth Opportunities

A major, high-impact growth opportunity for the global automotive fuel-filter market is the accelerating shift toward higher biofuel blends and alternative liquid fuels that forces OEMs, suppliers, and aftermarket players to upgrade filtration technology and materials. As countries scale biodiesel and bio-blend mandates, fuel chemistry changes (higher polarity, greater free fatty acids, increased microbial risk, and different solvent properties) create new failure modes for traditional cellulose material and simple water separators; this drives demand for chemically resistant synthetic and composite/nano material, improved coalescers, and integrated water-separation modules.

Fleet and infrastructure changes amplify this opportunity. Indonesia’s planned B50 biodiesel step would require about 20.1 million kilolitres of palm-oil biofuel annually, a dramatic increase from B40 levels, meaning widespread fuel-system exposure to heavier blends and a surge in replacement/retrofit needs. Global policy and energy scenarios also point to a substantive rise in renewable liquid fuels. MANN+HUMMEL has released CO₂-reduced and sustainability-focused filter products while major filtration OEMs are publicly highlighting innovations for cleaner fuel handling and contamination control. Practically, this opportunity translates into new OEM specifications, retrofit kits for legacy vehicles, aftermarket premium SKUs, and value-added services (contamination testing, installation kits, warranty programs). Suppliers that accelerate certified media testing, corrosion-resistant housings, and localized aftermarket rollouts in high-blend markets) can capture an outsized share as fuels diversify globally.

AUTOMOTIVE FUEL FILTER MARKET TRENDS

Proliferation of Factory-Integrated Autonomy Kits and Retrofit Partnerships is One of the Significant Market Trends

A major current trend in the global automotive fuel-filter market growth is the rapid push toward sustainable, higher-performance filters and module designs driven by OEMs’ low-emission goals, tighter fuel-system tolerances (GDI/common-rail), and buyer demand for lower lifecycle impact. Suppliers are replacing conventional cellulose with advanced synthetic and composite/nano material that deliver finer particle capture, better water coalescence, and longer service life, while simultaneously reducing carbon footprints via recycled or plant-based inputs and greener production. This trend is measurable in product rollouts and catalog expansions: leading suppliers have published larger, more advanced catalog portfolios (MANN-FILTER added over 125 new filter types in its 2024–2026 catalogs) and introduced CO₂-reduced, plant-based filter lines and easy-service kits to lower waste and simplify maintenance.

Most modern light-duty vehicles now use precision fuel systems (73% of light-duty vehicles produced in 2023 were equipped with gasoline direct injection), creating demand for filters that balance ultra-fine filtration with low pressure drop. At the module level, fuel-supply modules with integrated long-life in-tank filters are being positioned as lifetime-service items, further shifting design emphasis from disposable metal cans to engineered, durable assemblies that support circularity and reduced parts turnover. Newsflow shows suppliers moving on both fronts, product launches for sustainable media and clinic-friendly service kits, plus OEM-grade in-tank module engineering that promises fewer replacements over vehicle life. Collectively, sustainability mandates, tighter fuel-system tolerances, and suppliers’ public product programs are converging to reconfigure materials, servicing patterns, and procurement economics across global fuel-filter value chains.

Download Free sample to learn more about this report.

Segmentation Analysis

By Filter Type

Inline Fuel Filters Dominate Owing to Their Simplicity, Retrofitability, and Broad Legacy Fitment

Based on filter type, the market is segmented into inline fuel filters, in-tank fuel filters, cartridge fuel filters, and spin-on fuel filters.

Inline fuel filters remain the dominant filter-type as they are simple, have low-cost, can be easily serviced, and widely used across legacy and emerging markets where vehicle fleets are older or maintenance is decentralized with a share of 35.08% in 2026. Their external placement and modular design make them the default choice for millions of light and commercial vehicles that still use lower-complexity fuel systems, and are the common replacement SKU in aftermarket channels. The rise of precision fuel systems increases demand for finer inline elements in service markets, as many older platforms are retrofitted with higher-precision injectors. Recent product activity shows suppliers expanding advanced inline offerings. MANN+HUMMEL announced sustainable/plant-based filter lines and showcased new cleaner-mobility filter models at FILTECH, reflecting OEM and aftermarket demand for higher-performance inline replacements that meet modern tolerances while remaining serviceable. Inline dominance thus sustains large aftermarket volumes, driving development of higher-efficiency media in a familiar form factor, and anchors global replacement inventories.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Passenger Cars Dominate Due to Sheer Parc Size and Frequent Replacement Cycles

On the basis of vehicle type, the market is classified into passenger cars, two-wheelers, and commercial vehicles.

Passenger cars dominate the demand because they constitute the largest segment of the on-road fleet in most regions.with a share of 62.61% in 2026 They typically account for greatest number of replacement filters over a vehicle’s life. Passenger car fleets comprises majority of light-duty vehicle registrations globally, and increasing penetration of high-pressure fuel systems in this class raises requirements for higher-precision filtration in both OEM and aftermarket segments. Governments and regulators pushing for tighter real-world CO₂ and fuel-efficiency standards have led to the downsizing and adoption of direct-injection. This technical shift translates to more frequent, higher-spec replacement parts for passenger cars. Industry signals include broad product rollouts targeted at passenger-car service channels and OEM catalog expansions; in March 2025, MANN+HUMMEL and MAHLE have broadened passenger-car filter ranges in recent exhibitions. As passenger cars are numerically dominant and are often serviced in organized channels, their filter-replacement economics drive SKU complexity, inventory strategies, and new media adoption across the global automotive fuel filter market demand.

By Distribution Channel

Aftermarket is Expected to Grow at the Highest CAGR Due to Its Fleet Aging and Decentralized Servicing

According to distribution channel, the market is categorized into OEM and aftermarket.

The aftermarket will grow at the highest CAGR during the forecast period because most vehicles are serviced off-warranty by independent garages, chains, and owner/DIY channels, particularly in emerging markets and the large installed base of older vehicles in mature markets with a share of62.43% in 2026. Aftermarket share is supported by long replacement cycles, availability of budget and premium SKUs, and broad distribution networks that supply millions of replacement units annually. Aging vehicle parc and distributed servicing patterns propels operators to prefer easily-sourced inline and cartridge replacements rather than factory modules; suppliers and distributors therefore prioritize aftermarket catalog depth and regional availability. The aftermarket’s distribution channel growth shapes production runs, pricing tiers, and media selection, pushing manufacturers to offer both cost-effective cellulose elements and higher-spec synthetic/composite replacements to capture cross-sectional demand.

By Fuel Type

Petrol/Diesel Dominate As ICE Fleet Constitutes the Majority of Global on-Road Stock

The market, as per fuel type is segmented into gas and petrol/diesel.

Petrol and diesel fuels remain the dominant fuel types. Despite accelerating electrification, internal-combustion powertrains still represent the bulk of global vehicle stock and hence the recurrent replacement market for fuel filtration with a share of 77.23% in 2026. Even with electric car sales exceeded ~14 million in 2023 and rose further in 2024, a large share of the global fleet remains ICE-powered, sustaining substantial filter replacement volumes for years. The technical complexity of modern petrol and diesel systems, gasoline direct injection, and common-rail diesel requires finer filtration and water separation, further increasing per-unit filter performance and aftermarket spend. Recent industry includes OEMs requiring higher-precision filters for modern petrol/diesel engines and suppliers expanding CO₂-reduced and higher-efficiency product lines in 2024–2025 to meet both environmental and performance requirements. As long as ICE vehicles remain a significant growth factor for global VIO and petrol/diesel filtration demand will drive the largest part of the market.

By Material

Cellulose/Paper Dominates Owing to Its Cost-Effectiveness and Vast Installed Base

The market, as per material, is categorized into synthetic fiber, cellulose/paper, and composite/nano.

Cellulose/paper material still dominates the global market because it offers a low-cost, reliable solution for the vast installed base of conventional vehicles, especially in cost-sensitive and high-volume replacement markets. Its pleated construction is easy to manufacture, performs adequately in many petrol/diesel vehicles, and yields adequate durability for typical service intervals; hence, cellulose remains preferable for both OEM entry-level fitments and mainstream aftermarket SKUs.

While the demand for synthetic and composite materials are growing, driven by high-pressure injection systems and OEM premium specifications, cellulose’s cost advantage and entrenched distribution channels keeps it dominant material globally. Suppliers’ activity shows a dual strategy: continuous mass production of cellulose elements for volume markets while launching synthetic/composite lines for high-spec applications. Because cellulose underpins the largest unit volumes, it shapes manufacturing capacity, pricing tiers, and aftermarket stocking policies globally.

AUTOMOTIVE FUEL FILTER MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Automotive Fuel Filter Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific maintained a strong presence in the global market, reaching USD 2.41 billion in 2025, accounting for 51.85% share, and is expected to reach USD 2.54 billion in 2026. Asia Pacific leads global automotive fuel filter market share driven by its massive vehicle production and rapidly expanding vehicle parc in China and India. China alone accounted for nearly 31 million light vehicle production/sales figures in recent reporting, with domestic brands surging in 2024, creating outsized OEM and aftermarket replacement volumes. Rapid fleet growth, extensive two-wheeler markets, and regions pursuing biofuel/CNG blends raise filtration complexity; manufacturers are scaling capacity and launching region-specific, higher-efficiency media. Although EV uptake is strong in parts of Asia Pacific, the overall ICE fleet remains large, keeping replacement demand robust; suppliers are increasing in-tank module offerings and sustainable-media lines to serve both OEM and aftermarket channels. Recent CAAM reporting in January 2025, and global EV sales summarizes the growing importance of dual pressures of growth and electrification.The Japan market is projected to reach USD 0.28 billion by 2026, the China market is projected to reach USD 1.48 billion by 2026, and the India market is projected to reach USD 0.52 billion by 2026.

North America

In 2025, the North America market stood at USD 0.88 billion, representing 18.85% of global demand, and is projected to grow to USD 0.94 billion in 2026. North America’s market is shaped by a large installed light-vehicle fleet, strong organized aftermarket channels, and steady replacement demand as owners maintain aging ICE vehicles while EV adoption scales. The U.S. light-vehicle market remains sizeable, supporting aftermarket volumes and parts distribution networks that prioritize availability and SKU depth. Aftermarket distribution expansion and private-label strategies reinforce stock depth. Concurrently, rising EV sales are moderating long-term ICE volumes. Still, not erasing near-term replacement cycles, suppliers are therefore increasing advanced inline and cartridge SKUs to serve modern injectors while maintaining legacy cellulose lines. Recent supplier sustainability product launches reflect parallel demand for higher-efficiency media with lower lifecycle impact.The U.S. market is projected to reach USD 0.56 billion by 2026.

The U.S. market is replacement-driven, dominated by aftermarket channels, and increasingly requires higher-spec filters for GDI and modern diesel engines. U.S. vehicle-registration tables (FHWA Highway Statistics 2023) show a large light-vehicle base, sustaining aftermarket unit demand; meanwhile, suppliers are expanding premium and sustainable product lines to meet both emission and service-channel expectations.

Europe

The Europe region captured 23.87% of the global market in 2025, generating USD 1.11 billion in revenue, and is projected to reach USD 1.19 billion in 2026. Europe’s fuel-filter market is strongly influenced by stringent emissions and type-approval rules that drive OEM filter specification upgrades and increased adoption of precision filtration. The region maintains a large vehicle parc and organized dealer/service networks, which creates predictable OEM and aftermarket demand for higher-spec filters, particularly for passenger cars. OEM/regulatory pressure toward lower real-world emissions has accelerated adoption of finer media and integrated modules, while industry debates around implementation timelines introduce timing risk. Manufacturers are adjusting inventories and product launches accordingly. Recent ACEA registration updates and ongoing regulatory discussions shape procurement cycles and product qualification timelines.The UK market is projected to reach USD 0.23 billion by 2026, while the Germany market is projected to reach USD 0.28 billion by 2026.

Rest of the World (RoW)

The Rest of the World market generated USD 0.25 billion in 2025, representing 5.43% of the global market landscape, and is expected to reach USD 0.27 billion in 2026. RoW’s fuel-filter market is heterogeneous. Latin America, MENA, and Africa show steady replacement demand due to older fleets and strong aftermarket servicing. Regional fuel shifts increase the need for chemically resistant media and water-separation modules. Latin America’s significant CNG/LPG vehicle base sustains gas-fuel filter demand. Suppliers must balance cost-sensitive cellulose production with targeted synthetic/composite SKUs for markets adopting higher-blend fuels.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Leadership, Strong Investment, and Continuous Innovation by MANN+HUMMEL Drives Competitive Edge

MANN+HUMMEL is widely regarded as the world’s leading automotive filtration manufacturer. Its leadership stems from its decades worth OEM partnerships, a large global manufacturing footprint, deep R&D in filter media and module integration, and early investments in synthetic and composite media. The company supplies original equipmemt and aftermarket fuel filters for passenger cars, commercial vehicles, and two-wheelers, and supports global platforms with localized production and qualification capabilities. Its fuel-filter portfolio includes inline elements, cartridge housings, spin-on canisters, in-tank modules, and integrated fuel-supply modules, plus water-separators and application-specific media (cellulose, synthetic, and composite/nano). Strong quality systems, broad OEM homologations, and extensive aftermarket distribution cements its top position.

Robert Bosch GmbH ranks as the second major global player due to its dominant role in powertrain systems, long-standing OEM relationships, and cross-domain expertise in sensors, pumps, and filtration. Bosch’s strength comes from an integrated system supply combining fuel pumps, pressure regulation, fuel-management electronics, and filters, allowing turnkey modules for modern gasoline and diesel engines. Its fuel-filter product range covers inline filters, cartridge elements, spin-on assemblies, in-tank modules, water separators, and engineered media optimized for GDI and common-rail systems. Rigorous validation, worldwide manufacturing, and deep aftermarket reach through established parts channels make Bosch the natural second-place leader in fuel filtration.

LIST OF KEY AUTOMOTIVE FUEL FILTER COMPANIES PROFILED

- MANN+HUMMEL (Germany)

- Robert Bosch GmbH (Germany)

- MAHLE GmbH (Germany)

- DENSO Corporation ( Japan)

- Hengst SE & Co. KG (Germany)

- Donaldson Company, Inc. ( U.S.)

- Filtration Group (U.S.)

- Cummins Filtration (U.S.)

- Baldwin Filters (U.S.)

- FRAM (U.S.)

- Sogefi (Italy)

- K&N Engineering ( U.S.)

- Valeo (France)

- Aisin Seiki (Japan)

- UFI Filters (Italy)

KEY INDUSTRY DEVELOPMENTS

- In March 2025, Parker Hannifin inaugurated a new fuel-filter assembly line at its Chennai facility, a project developed in collaboration with Ashok Leyland. The state-of-the-art line increases local production capacity, improves throughput, and shortens delivery times for fuel-filter assemblies that support Ashok Leyland’s powertrain programs, reinforcing Parker’s manufacturing footprint in India.

- In January 2025, Steelbird International showcased its range of filters and rubber parts at the Bharat Mobility Auto Expo 2025 in New Delhi. Marking its 60th year, Steelbird presented some 3,000 products, including roughly 300 filter variants and 1,500 rubber parts, highlighting its breadth across air, oil, fuel, and cabin filters and its long legacy in India’s components sector.

- In January 2025, UAE-based Naphtha Group LLC-FZ acquired SDK Group (manufacturer of oil filter, fuel, and air filters branded Filtr.uz); Uzbekistan’s Competition Committee approved the deal after determining it would not materially affect market competition. SDK Group, headquartered in Andijan and founded in 2009, now joins Naphtha’s distribution network as the new owner.

- In April 2024, Lumax Cornaglia Auto Technologies (LCAT) opened a new manufacturing facility near Pune to produce blow-moulded plastic components, including plastic fuel tanks, Fuel filters, urea tanks, and degassing tanks for commercial vehicles and four-wheelers. The plant adds roto-moulding capability and houses R&D, production, assembly, and warehousing, supporting customers such as Tata Motors, Toyota India, and Stellantis. The move reinforces a trend toward lighter, non-corrosive plastic fuel tanks that reduce weight and cost versus metal alternatives.

- In December 2023, Uno Minda launched a durable range of commercial-vehicle filters (air, oil, and fuel) developed in collaboration with Roki of Japan. The new lineup is built for heavy-duty Indian operating conditions, meets OEM standards, and is positioned for the aftermarket with competitive pricing emphasizing improved contamination protection and engine life.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.96% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Filter Type · Inline Fuel Filters · Cartridge Fuel Filters · Spin-on Fuel Filters · In-tank Fuel Filters |

|

By Vehicle Type · Two Wheeler · Passenger Cars · Commercial Vehicles |

|

|

By Distribution Channel · OEM · Aftermarket |

|

|

By Fuel Type · Petrol/ Diesel · Gas |

|

|

By Material · Synthetic Fiber · Cellulose/Paper · Composite/Nano |

|

|

By Region · North America (By Filter Type, By Vehicle Type, By Distribution Channel, By Fuel Type, By Material, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Filter Type, By Vehicle Type, By Distribution Channel, By Fuel Type, By Material, and By Country ) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Filter Type, By Vehicle Type, By Distribution Channel, By Fuel Type, By Material, and By Country ) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Filter Type, By Vehicle Type, By Distribution Channel, By Fuel Type, and By Material) |

Frequently Asked Questions

The global automotive fuel filter market size was valued at USD 4.65 billion in 2025. The market is projected to grow from USD 4.94 billion in 2026 to USD 7.84 billion by 2034, exhibiting a CAGR of 5.96% during the forecast period.

In 2025, the market value stood at USD 4.65 billion.

The market is expected to expand at a CAGR of 5.96% during the forecast period.

The petrol/diesel segment led the market in the fuel segment.

Rising technical shift to high-pressure fuel delivery systems drives the market trends.

Top players include MANN+HUMMEL, Bosch, MAHLE, DENSO, and Hengst.

Asia Pacific dominated the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us