Automotive Garage Equipment Market Size, Share & Industry Analysis, By Equipment Type (Lifting & Handling Equipment, Tire & Wheel Service Equipment, Wheel Alignment Systems, Diagnostics & Testing Equipment, Air & Pneumatic Systems, and others), By Vehicle Type Serviced (Hatchback & Sedans, SUVs, LCVs, and HCVs), By Propulsion Type (ICE and Electric), By End-user (Authorized/OEM Dealer Workshops, Independent Multi-brand Garages, and others), By Technology/Automation Level (Manual/Conventional Equipment, Semi-automatic Equipment, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

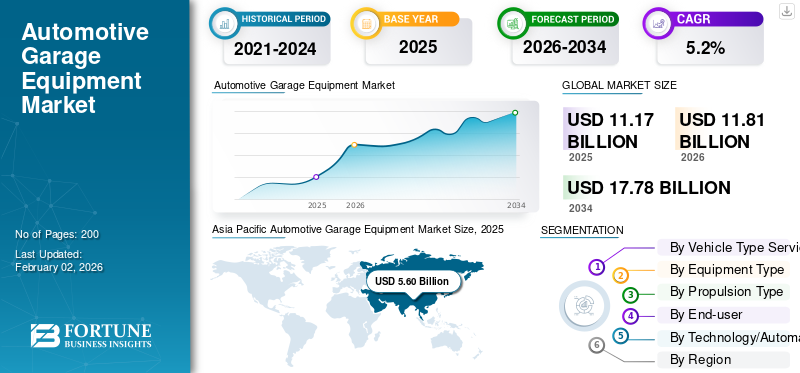

The global automotive garage equipment market size was valued at USD 11.17 billion in 2025. The market is projected to grow from USD 11.81 billion in 2026 to USD 17.78 billion by 2034, exhibiting a CAGR of 5.2% during the forecast period. Asia Pacific dominated the global automotive garage equipment market with a market share of 50.13% in 2025.

Automotive garage equipment includes tools and machines used for vehicle maintenance, repair, inspection, and servicing, enabling safe, efficient, and accurate operations across independent garages and authorized service centers for all vehicle types. The market growth is driven by rising vehicle parc, increasing repair and maintenance needs, stricter safety and emission regulations, growing vehicle complexity, electrification trends, and the expansion of organized service networks globally.

Major players in the market include Bosch, Snap-on, Atlas Automotive Equipment, Hunter Engineering, Rotary Lift, and Launch Tech, competing through advanced diagnostics, automation, digital integration, and safety-focused solutions.

Download Free sample to learn more about this report.

Automotive Garage Equipment Market Takeaways

- 2025 Market Size: USD 11.17 Billion

- 2026 Market Size: USD 11.81 Billion

- 2034 Forecast Market Size: USD 17.78 Billion

- CAGR: 5.2% from 2026–2034

- Asia Pacific dominated the automotive garage equipment market with a 50.13% share in 2025.

- Diagnostic equipment is the dominant category and is projected to grow at a CAGR of 6.3% during the forecast period.

- The EV segment is expected to register the fastest growth, expanding at a CAGR of 15.6% through 2034.

North America

North America is witnessing steady growth due to its aging vehicle fleet, strong aftermarket demand, and increasing adoption of advanced diagnostic and calibration systems.

Europe

Europe held the second-largest market position, driven by stringent emission regulations, mandatory inspections, and growing ADAS and EV penetration.

Asia Pacific

Asia Pacific led the global market in 2025 and remains the fastest-growing region, supported by rising vehicle ownership, EV adoption, and workshop modernization.

U.S.

Market growth is supported by a large aging vehicle parc, strict safety and emissions standards, and rising demand for AI-enabled diagnostic and calibration equipment.

Japan

The market benefits from advanced automotive technologies, strong vehicle maintenance standards, and increasing demand for precision diagnostic and servicing equipment.

Read More

AUTOMOTIVE GARAGE EQUIPMENT MARKET TRENDS

Digitalization and Automation Transforming Workshop Operations

A major market trend is the shift toward digitalized and automated garage environments. Workshops are increasingly adopting connected diagnostic platforms, cloud-based service management systems, sensor-enabled lifts, and automated tire and wheel equipment. The integration of data analytics improves workflow efficiency, reduces human error, and enhances service accuracy. Touchless inspection systems, remote diagnostics, and software updates are gaining traction. This trend is driven by technician shortages, rising labor costs, and the need for faster vehicle turnaround times. In November 2025, Solera launched its ShopCentral cloud-based platform for automotive repair shops, unifying customer communication, scheduling, parts pricing, and billing to streamline operations and boost profitability.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Vehicle Parc and Aging Fleet to Drive Equipment Demand

The growing global vehicle parc, combined with an aging fleet in mature markets, is a key driver for the automotive garage equipment market. Older vehicles require frequent maintenance, diagnostics, wheel alignment, lifting, and component replacement, increasing workshop dependency. Simultaneously, rising vehicle ownership in emerging economies is expanding the installed base of serviceable vehicles. This directly boosts the demand for lifts, tire changers, alignment systems, and diagnostic tools across independent garages and authorized service centers, ensuring consistent equipment utilization and replacement cycles. In April 2025, SIAM data showed India produced 3.10 crore vehicles in fiscal year 2024-25, up from 2.84 crore; domestic vehicle sales reached 2.56 crore units, including 1.96 crore two-wheelers and 43 lakh passenger vehicles, expanding the vehicle parc and long-term service demand.

MARKET RESTRAINTS

High Capital Investment and Cost Sensitivity May Limit Product Adoption

A major restraint is the high upfront cost associated with advanced automotive garage equipment, particularly automated lifts, ADAS calibration systems, and digital diagnostics. Small and unorganized garages, especially in developing regions, often operate on thin margins and delay capital investments. Inflationary pressures, volatile steel prices, and higher interest rates further restrict financing capabilities. As a result, workshops frequently extend equipment life cycles, prefer refurbished machinery, or limit technology upgrades, slowing the overall adoption of modern, high-value automotive garage equipment.

MARKET OPPORTUNITIES

Electrification and ADAS Create New Revenue Opportunities for Workshops

The increasing penetration of electric vehicles and ADAS-equipped vehicles presents significant opportunities for market players. EVs require specialized lifts, battery handling systems, insulation tools, and thermal management equipment. Similarly, ADAS features demand calibration systems, alignment precision tools, and software-enabled diagnostics. Workshops upgrading capabilities to service these vehicles can command higher service revenues. Equipment manufacturers benefit by offering EV-ready, ADAS-compatible, and modular solutions, enabling workshops to future-proof operations and expand service portfolios. In June 2023, at Automechanika Birmingham, Launch Tech UK showcased its latest ADAS calibration and diagnostic tools, including ADAS Pro+ and ADAS Mobile, attracting thousands of garages and technicians and highlighting the rising workshop demand for advanced calibration solutions.

MARKET CHALLENGES

Technician Skill Gaps and Training Requirements to Create Challenges for Market Growth

The rapid evolution of vehicle technologies acts as a key challenge for the expansion of the market. Advanced diagnostics, EV systems, and ADAS calibration require skilled technicians capable of operating sophisticated equipment. However, many regions face technician shortages and limited access to structured training programs. Without adequate skills, workshops underutilize advanced equipment or avoid adoption altogether. Equipment suppliers increasingly need to bundle training, digital support, and user-friendly interfaces to overcome this barrier and sustain long-term automotive garage equipment market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type Serviced

High Vehicle Parc and Routine Servicing Needs to Propel Hatchbacks & Sedans Segmental Dominance

Based on vehicle type serviced, the market is segmented into hatchbacks & sedans, SUVs, LCVs, and HCVs.

The hatchbacks & sedans segment dominates the market due to their large global vehicle parc and frequent maintenance cycles. These vehicles require regular tire servicing, alignment, lifting, fluid management, and diagnostics, ensuring steady equipment utilization. High penetration across urban markets, ride-hailing fleets, and personal ownership sustains aftermarket servicing volumes. Independent garages and authorized workshops prioritize equipment compatible with passenger cars, reinforcing sustained replacement demand and incremental upgrades rather than rapid technology shifts.

The LCV segment is poised to expand at a CAGR of 7.1% over the forecast period. Expanding e-commerce, urban logistics, and last-mile delivery fleets accelerate LCV servicing needs, driving the demand for higher-capacity, durable garage equipment.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Type

Established ICE Vehicle Base to Ensure Consistent Garage Equipment Utilization Driving ICE Segment Growth

Based on propulsion type, the market is segmented into ICE and electric vehicles.

The ICE (internal combustion engine) vehicles segment dominates the automotive garage equipment demand due to their overwhelming presence in the global vehicle parc. These vehicles require frequent mechanical repairs, emission checks, fluid replacement, and powertrain diagnostics. Established service procedures, standardized tools, and widespread technician familiarity support the steady demand for lifts, alignment systems, diagnostics, and fluid management equipment. The long service life of ICE models continues to drive the majority of automotive control arm demand across both developed and emerging markets.

The EV segment is anticipated to surge at a CAGR of 15.6% over the analysis period. The rapid EV adoption increases the demand for specialized lifts, battery handling, insulation tools, and software-enabled diagnostics across modern workshops. In 2024, The International Energy Agency reported that the global electric car sales exceeded 17 million, accounting for over 20% of all new cars sold worldwide, with China dominating and EVs continuing strong growth.

By Equipment Type

Rising Vehicle Complexity and Regulatory Compliance to Drive Diagnostics & Testing Equipment Leadership

By equipment type, the market is divided into lifting & handling equipment, tire & wheel service equipment, wheel alignment systems, diagnostics & testing equipment, air & pneumatic systems, fluid management & lubrication equipment, and workshop tools & service bay equipment.

The diagnostics and testing equipment dominates the market due to increasing vehicle electronics, software-controlled systems, and stringent emission and safety regulations. Modern vehicles require frequent fault-code analysis, sensor testing, ECU diagnostics, and calibration to ensure compliance and performance. The growing adoption of ADAS, connected features, and electrified powertrains further increases the reliance on advanced diagnostic tools across workshops. Continuous software updates, recurring calibration needs, and mandatory inspection norms support sustained replacement demand, making diagnostics both the dominant and fastest-growing equipment category expanding at a CAGR of 6.3% over the forecast period.

The tire and wheel service equipment holds the second-largest share and is estimated to expand at a CAGR of 5.5% over the forecast period. The expansion of the segment is supported by a growing vehicle parc, frequent tire replacements, and increasing demand for routine wheel maintenance services.

By End-user

Broad Vehicle Coverage and Cost Flexibility to Strengthen Independent Multi-Brand Garage Dominance

By end-user, the market is categorized into authorized/OEM dealer workshops, independent multi-brand garages, tire specialists & quick-service chains, fleet & commercial vehicle servicing workshops, and inspection & testing centers.

The independent multi-brand garages segment holds the largest automotive garage equipment market share, as they service diverse vehicle makes and models across passenger and light commercial segments. Their focus on cost-effective maintenance, high service volumes, and aftermarket repairs drives the demand for versatile equipment such as lifts, tire changers, alignment systems, and diagnostics. Expanding vehicle parc, aging fleets, and consumer preference for affordable servicing sustain consistent equipment utilization and periodic upgrades across independent workshops.

The fleet & commercial vehicle servicing workshops segment is poised to grow at a CAGR of 6.7% over the forecast period. The rapid expansion of logistics, ride-hailing, leasing, and corporate fleets increases the demand for heavy-duty, high-throughput garage equipment and predictive diagnostics. In December 2025, Softing launched a hybrid diagnostic solution for software-defined vehicles, combining traditional and service-oriented diagnostics to support ADAS, electrification, and complex vehicle systems across workshops and OEM service networks.

By Technology/Automation Level

Balanced Cost, Efficiency, and Reliability to Sustain Semi-Automatic Equipment Demand

On the basis of technology/automation level, the market is categorized into manual/conventional equipment, semi-automatic equipment, and fully automatic/digitally enabled equipment.

The semi-automatic equipment segment dominates the market as the technology offers an optimal balance between affordability, productivity, and operational reliability. These systems reduce manual effort while maintaining technician control, making them suitable for a wide range of workshops. Semi-automatic lifts, tire changers, and alignment systems are widely adopted due to lower capital costs, easier maintenance, and minimal training requirements. Their compatibility with both legacy and modern vehicles ensures stable demand across developing and mature markets.

The fully automatic/digitally enabled equipment is likely to expand at a CAGR of 6.6% over the forecast period. Rising labor costs, skill shortages, and digital integration needs accelerate the adoption of fully automatic, connected, and software-driven garage equipment. In November 2025, Revv raised USD 20 million to expand its AI-driven auto repair platform, enhancing predictive diagnostics, repair estimates, and workflow automation to streamline shop operations and improve customer service.

Automotive Garage Equipment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Garage Equipment Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and is the fastest-growing market, driven by increasing vehicle ownership, urbanization, and rising middle-class incomes. Large two-wheeler, passenger car, and LCV parc across China, India, and Southeast Asia sustains high servicing volumes. The increasing formalization of workshops, entry of organized service chains, and growing penetration of diagnostics and semi-automatic equipment support market expansion. EV adoption and tightening emission regulations further accelerate the demand for advanced garage equipment across the region. In July 2024, East Auto showcased new advanced diagnostic systems, digital service workflows, and connected workshop tools aimed at enhancing repair accuracy, reducing turnaround times, and integrating software-driven maintenance for modern vehicles.

Europe

Europe is the second-largest market for automotive garage equipment, driven by stringent emission regulations, mandatory inspections, and high service quality standards. An aging vehicle parc across Western Europe sustains aftermarket demand, while EV and ADAS penetration boosts the adoption of advanced diagnostics and calibration equipment. Well-established independent garages and OEM dealer networks support steady equipment replacement cycles.

North America

North America shows steady growth supported by a mature vehicle parc, high average vehicle age, and strong demand for aftermarket services. Strict safety, emission, and inspection norms drive the adoption of advanced diagnostics, alignment, and ADAS calibration systems. Growth in fleet, logistics, and dealership networks increases the demand for heavy-duty and high-throughput equipment.

The U.S. market is driven by a large and aging vehicle parc, high average vehicle age, and strong demand for aftermarket repairs. Strict safety, emissions, and inspection regulations increase the reliance on advanced diagnostics, alignment, and ADAS calibration equipment. Rising fleet, logistics, and ride-hailing activity further boost the demand for high-capacity, automated, and digitally enabled automotive garage equipment across independent and dealership workshops. In April 2025, Launch Tech USA introduced AI-powered PredictaFix integration into its diagnostic tools, using CarTechIQ’s AI to analyze DTCs, prioritize root causes, and offer precise repair suggestions, accelerating diagnostics and improving first-time fix accuracy.

Rest of the World

The rest of the world, including South America, the Middle East, and Africa, exhibits moderate growth driven by rising motorization and expanding vehicle parc. Increasing urbanization and a gradual shift from informal repair shops to organized workshops support equipment adoption. The demand remains focused on basic lifts, tire equipment, and diagnostics due to cost sensitivity.

COMPETITIVE LANDSCAPE

Key Industry Players

Automation, Digital Diagnostics, and Service Network Expansion Define Competitive Intensity

The automotive garage equipment market is shaped by increasing automation, digital diagnostics, and expanding global service networks. Key players such as Bosch, Snap-on, Atlas Automotive Equipment, Hunter Engineering, Rotary Lift, and Launch Tech compete through advanced diagnostic platforms, ADAS calibration systems, and durable lifting and tire service solutions. To gain an edge over competitors, companies are integrating software-enabled tools, offering EV- and ADAS-ready equipment, and bundling training and aftersales support. Strategic acquisitions, distributor partnerships, and localized manufacturing help optimize costs, expand regional presence, and address diverse workshop requirements across mature and emerging markets. In September 2025, Bosch introduced an AI-enabled diagnostic platform for multi-brand workshops, enabling faster fault detection, remote software updates, and improved compatibility with electric and software-defined vehicles, enhancing productivity for independent and authorized service centers globally.

LIST OF KEY AUTOMOTIVE GARAGE EQUIPMENT COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Snap-on Incorporated (U.S.)

- Hunter Engineering Company (U.S.)

- Launch Tech Co., Ltd. (China)

- Vehicle Service Group (U.S.)

- Ravaglioli S.p.A. (Italy)

- Rotary Lift (U.S.)

- Atlas Automotive Equipment (U.S.)

- Nussbaum Automotive Solutions (Germany)

- MAHA Maschinenbau Haldenwang GmbH & Co. KG (Germany)

- Autel Intelligent Technology Corp., Ltd. (China)

- Continental AG (Germany)

- Symach S.p.A. (Italy)

- Aro Equipments Pvt. Ltd. (India)

- Gray Manufacturing Company, Inc. (U.S.)

- Arex Test Systems B.V. (Netherlands)

- Teco S.r.l. (Italy)

- Boston Garage Equipment Ltd. (U.K.)

- OTC Tools (U.S.)

- Innova Electronics Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In May 2025, Hunter Engineering released a WinAlign vehicle-database upgrade that added hundreds of new and updated alignment records plus software features such as TPMSpecs and reset procedures, VIN-recall support, and ADAS-related procedures. This would help shops keep alignment workflows current as new models enter bays.

- In October 2024, Snap-on Total Shop Solutions announced SEMA demos spanning ADAS calibration, wheel aligners, tire changers, balancers, and collision tools, highlighting innovations such as a next-gen wheel aligner V4400 Commander and new in-ground collision repair equipment, BenchRack Versa.

- In September 2024, TEXA showcased repair-bay technology previews, including the IDC6 diagnostic software with AI, a stronger MULTIHUB interface, and systems for fast alignment checks and ADAS setup. In addition, it also exhibited EV-focused tools such as an EV charging/diagnostic station and EV cooling-system maintenance solutions.

- In August 2024, Autel introduced the MaxiSYS IA700 modular ADAS calibration frame, emphasizing compact setup while supporting optical positioning, unlevel-floor compensation, and alignment pre-check, aimed at reducing calibration variance and making ADAS workflows more repeatable across different shop floor conditions.

- In July 2024, VSG previewed Automechanika launches, including a Bluetooth, battery-powered CCD wheel aligner controlled by tablet, faster clamps to shorten setup time, an All Vehicles 2-post lift arm concept for broader reach points, and a new mobile column lift concept.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type Serviced, By Propulsion, By Equipment Type, By End-user, By Technology/Automation Level, and By Region |

|

By Vehicle Type Serviced |

· Hatchback/Sedan · SUVs · Light Commercial Vehicles (LCVs) · Heavy Commercial Vehicles (HCVs) |

|

By Propulsion Type |

· ICE · Electric |

|

By Equipment Type |

· Lifting & Handling Equipment · Tire & Wheel Service Equipment · Wheel Alignment Systems · Diagnostics & Testing Equipment · Air & Pneumatic Systems · Fluid Management & Lubrication Equipment · Workshop Tools & Service Bay Equipment |

|

By End-user |

· Authorized/OEM Dealer Workshops · Independent Multi-brand Garages · Tire Specialists & Quick-service Chains · Fleet & Commercial Vehicle Workshops · Inspection & Testing Centers |

|

By Technology/Automation Level |

· Manual/Conventional Equipment · Semi-automatic Equipment · Fully Automatic/Digitally Enabled Equipment |

|

By Geography |

· North America (By Vehicle Type Serviced, By Propulsion, By Equipment Type, By End-user, By Technology/Automation Level, and By Country) o U.S. o Canada o Mexico · Europe ( By Vehicle Type Serviced, By Propulsion, By Equipment Type, By End-user, By Technology/Automation Level, and By Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type Serviced, By Propulsion, By Equipment Type, By End-user, By Technology/Automation Level, and By Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World ( By Vehicle Type Serviced, By Propulsion, By Equipment Type, By End-user, By Technology/Automation Level ) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.17 billion in 2025 and is projected to reach USD 17.78 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 5.60 billion.

The market is expected to exhibit a CAGR of 5.2% during the forecast period of 2026-2034.

The ICE segment leads the market in terms of propulsion type.

Expanding vehicle parc and aging fleet are key factors fueling market growth.

Key players such as Bosch, Snap-on, Atlas Automotive Equipment, Hunter Engineering, Rotary Lift, and Launch Tech are the leading companies in the market.

Asia Pacific holds the largest share in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us