Automotive Internet of Things (IoT) Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, LCVs, and HCVs), By Component Type (Hardware, Software, and Services), By Connectivity Type (Cellular, Wifi/Bluetooth, Satellite, DSRC/C-V2X), By Application (Fleet Management, Telematics & Vehicle Tracking, Predictive Maintenance, ADAS & Safety Systems, Infotainment & Navigation, Usage-Based Insurance (UBI), V2X & Autonomous Driving Systems), By Vehicle Propulsion (ICE and Electric), By End-user (Private and Commercial), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

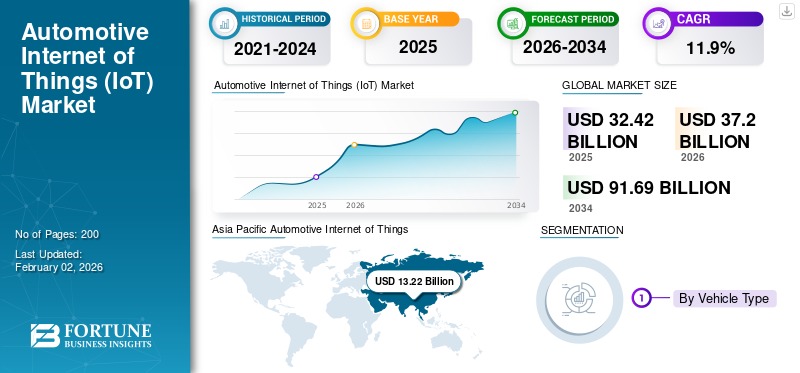

The global automotive Internet of Things (IoT) market size was valued at USD 32.42 billion in 2025. The market is projected to grow from USD 37.20 billion in 2026 to USD 91.69 billion by 2034, exhibiting a CAGR of 11.9% during the forecast period. Asia Pacific dominated the automotive Internet of Things (IoT) market, with a 40.78% market share in 2025.

The global automotive internet of things (IoT) market encompasses connected vehicle technologies integrating sensors, cloud computing, and data analytics to enhance vehicle performance, safety, and user experience. Growth is fueled by the rising adoption of connected cars, advancements in 5G connectivity, and increasing emphasis on telematics and predictive maintenance. Integration of IoT enables real-time monitoring, vehicle-to-everything (V2X) communication, and over-the-air software updates. The surge in autonomous vehicle development and smart mobility solutions further accelerates demand. Additionally, collaborations between automakers and tech firms, along with regulatory focus on road safety and emission reduction, are shaping the market’s evolution toward intelligent transportation systems.

Key players in the global market include Bosch, Continental AG, Harman International, Qualcomm Technologies, and Cisco Systems. These companies focus on developing advanced telematics, connectivity, and vehicle-to-everything (V2X) communication solutions. Strategic collaborations with automakers and cloud service providers, along with investments in AI, cybersecurity, and 5G infrastructure, strengthen their position in enabling intelligent, connected, and data-driven mobility ecosystems across the automotive sector.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Nationwide V2X and 5G Connectivity Accelerates Market Adoption

Adoption of IoT in automotive gains momentum as governments and industry coalesce around interoperable V2X and high-bandwidth cellular connectivity. Scaling roadside units, cellular C-V2X pilots, and harmonized rollout roadmaps unlock safety, traffic efficiency, and new data-driven services for automakers, fleets, and city operators. As coverage deepens, connected features such as real-time hazard warnings, cooperative perception, telematics, become default expectations in new models, reinforcing ecosystem growth and supplier investment. In August 2024, USDOT released a national plan to accelerate V2X deployment and paired it with around USD 60 million in grants.

MARKET RESTRAINTS

Cybersecurity and Software-Update Compliance Increases Cost Pressures in Market

Meeting stringent cybersecurity and OTA-management rules raises development, validation, and compliance costs across platforms and regions. OEMs must implement certified cybersecurity management systems, secure update pipelines, and auditability, extending beyond premium segments to mass market vehicles. This elevates bill-of-materials and engineering expenditure, slowing adoption for new IoT technologies features in cost-sensitive models. In July 2024, UNECE regulations R155 cybersecurity and R156 software updates, became mandatory for all new vehicles produced in the European Union, formalizing these obligations and associated costs.

MARKET OPPORTUNITIES

After-Sales Data Access Unlocks New Services and Revenue Streams for Market

Expanded access to connected-vehicle data enables third-party maintenance, insurance, fleet optimization, and value-added apps, fostering competitive after-sales marketplaces. Standardized sharing frameworks lower integration friction for startups and suppliers, while consumers gain choice over service providers. Automakers and platforms can monetize consented data through analytics and API products without hardware changes, amplifying margins. In September 2025, the European Union Data Act began applying, granting users control over data from connected devices, including cars, and opening opportunities for innovative after-sale services.

AUTOMOTIVE INTERNET OF THINGS (IoT) MARKET TRENDS

Software-Defined Vehicles and AI-Enhanced Infotainment Trends Gain Market Momentum

Automotive internet of things (IoT) is trending toward SDV architectures with centralized compute, continuous OTA updates, and AI assistants. This enables rapid feature releases, personalization, and lifecycle upgrades independent of hardware refreshes. Open, updatable infotainment stacks shorten app lead times and strengthen developer ecosystems, while voice-first copilots bridge in-car and cloud experiences. In May 2025, Volvo deepened its partnership with Google to lead Android Automotive versions and showcased Gemini AI integration in the EX90, signaling faster, AI-centric SDV rollouts.

MARKET CHALLENGES

Ecosystem Complexity and Partnership Volatility Disrupt Market Growth

Automotive internet of things (IoT) spans chipset vendors, cloud providers, OS stacks, and app ecosystems, making coordination hard and timelines fragile. Shifts in platform strategy, cost priorities, or talent can upend cockpit, connectivity, or telematics programs, forcing re-architecture and delaying features. Suppliers must hedge integrations and maintain multi-cloud, multi-OS options to reduce single-point risk. In May 2025, Amazon and Stellantis ended their SmartCockpit collaboration, illustrating how strategic pivots can derail connected-software plans despite prior commitments.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

Premium Feature Adoption and Higher Per-Vehicle Value Anchor SUV Dominance

Based on vehicle type, the market is segmented into hatchback/sedan, SUVs, LCVs, and HCVs.

SUVs lead automotive internet of things (IoT) revenue as high-trim models standardize rich connectivity, ADAS, and over-the-air update stacks, lifting IoT content per vehicle. Flagship launches often debut new infotainment systems OS versions, and embedded AI assistants in SUVs before cascading to lower segments, reinforcing consumer expectations for connected vehicles experiences. This pull-through effect sustains supplier roadmaps and app ecosystems centered on SUVs across regions and price bands. In May 2025, Volvo named the EX90 its lead Android Automotive partner vehicle and showcased Gemini AI integration and rapid OS upgrades.

LCVs are scaling IoT fastest as fleets deploy connected diagnostics, route optimization, and uptime services to cut downtime and costs in last-mile delivery. In March 2025, Ford Pro expanded connected FORDLiive uptime services for Transit vans.

By Component Type

Subscription-Based Telematics and Connected Solutions Strengthen Service Segment Leadership

In terms of component type, the market is segregated into hardware, software, and services.

The services segment leads the automotive internet of things (IoT) market, driven by the growing adoption of subscription-based telematics, remote diagnostics, and predictive maintenance platforms. Automakers are shifting toward service-centric business models, generating continuous revenue streams through connected packages that enhance vehicle uptime and customer engagement. Integration with AI-powered analytics and cloud ecosystems further solidifies the segment’s dominance by extending value throughout the vehicle lifecycle. In November 2024, BMW detailed autumn ConnectedDrive upgrades, expanding video streaming, in-car gaming, digital payments, and remote software updates, highlighting post-sale monetization through OTA.

Software is witnessing rapid growth as vehicles transition to software-defined architectures, enabling continuous updates and feature scalability.

By Connectivity Type

Extensive Network Coverage and Data Reliability Uphold Cellular Connectivity Market Share

On the basis of connectivity type, the market is categorized into cellular, Wi-Fi/bluetooth, satellite, and DSRC/C-V2X.

Cellular connectivity maintains dominance in the market due to its wide global network coverage, high data throughput, and robust reliability for real time data on vehicle applications. The integration of 4G and rapidly expanding 5G infrastructure enables seamless telematics, infotainment, navigation, and over-the-air (OTA) updates. Automakers prefer cellular links for their scalability, interoperability, and consistent performance across regions, establishing them as the foundational layer of connected mobility. In February 2024, Cisco emphasized connected-car initiatives at MWC, positioning vehicles as secure, cloud-managed IoT endpoints leveraging 5G for telematics, V2X, and edge computing.

DSRC/C-V2X is expected to develop at the fastest-growing compound annual growth rate (CAGR) over the automotive internet of things (IoT) market forecast period, facilitating direct vehicle-to-vehicle and vehicle-to-infrastructure communications for low-latency safety and cooperative driving use cases.

By Application

Immersive Digital Experience Engines Strengthen Infotainment & Navigation Segment Growth

By application, the market is segmented into fleet management, telematics & vehicle tracking, predictive maintenance, ADAS & safety systems, infotainment & navigation, usage-based insurance (UBI), and V2X & autonomous driving systems.

Infotainment & navigation applications lead the market as OEMs prioritize rich user-interfaces, smartphone integration, voice assistants, and live map updates. These systems not only enhance driver experience but also serve as gateways to connectivity services, data monetization, and aftermarket subscriptions, driving higher content per vehicle and recurring revenues. Stand-alone systems evolve into digital cockpits that span entire vehicle lifetimes, reinforcing their dominance in IoT application stacks.

Applications supporting vehicle-to-everything (V2X) communication and autonomous driving systems are growing most rapidly, propelled by safety mandates, smart-city infrastructure rollouts, and the push toward Level 2 and Level 3 advanced driver assistance systems (ADAS) in automated vehicles. In November 2024, the Federal Communications Commission approved new spectrum rules to accelerate C-V2X deployment across the U.S. road network.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Propulsion

Legacy ICE Architecture Anchors ICE Segment Dominance

By vehicle propulsion, the market is segregated into ICE and electric.

The ICE vehicle segment holds major share in automotive internet of things (IoT) penetration as it represents the largest installed base globally, providing economies of scale for telematics modules, connectivity subscriptions, and service models. Suppliers can amortize IoT hardware and cloud investments across millions of ICE units, making aftermarket and OEM roll-outs more commercially viable. Additionally, regulatory transitions are gradual, allowing OEMs to continue leveraging connected features on ICE platforms.

Electric vehicles are the fastest-growing propulsion segment for automotive internet of things (IoT) as electrification demands smart battery systems, charging-ecosystem connectivity, and advanced telematics, all contributing to higher IoT content per vehicle. In February 2024, Xiaomi unveiled its first electric vehicle, the SU7, featuring the HyperOS IoT ecosystem and five core automotive technologies, including smart-cabin connectivity and autonomous-driving integration, marking its formal entry into the EV market.

By End-user

High Feature Integration and Personalized Connectivity Uphold Private Segment Dominance

Based on the end-user, the market includes private and commercial.

Private segment dominate the market as rising consumer demand for in-car connectivity, entertainment, navigation, and safety applications drives widespread adoption of telematics and smart infotainment systems. Automakers are integrating AI-based assistants, remote vehicle control, and subscription-based digital services, creating personalized mobility experiences and consistent revenue streams. Continuous upgrades through OTA updates and integration with smartphones strengthen the private segment’s leadership in connected mobility. In June 2023, Mercedes‑Benz integrated ChatGPT into its MBUX voice assistant via Azure OpenAI, offering natural-language dialogues, OTA rollout for 900,000 vehicles, and expanded hands-free interaction. The commercial segment are fastest-growing due to rapid adoption of IoT to optimize fleet operations, route efficiency, and predictive maintenance, enhancing logistics visibility and reducing downtime. In June 2025, Geotab launched Routing & Optimization solution, enabling fleets to reduce mileage by 15–30%, boost on-time arrivals to 98%, and enhance productivity through advanced dispatching and real-time task management.

Automotive Internet of Things (IoT) Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

ASIA PACIFIC

Asia Pacific Automotive Internet of Things (IoT) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest share in 2025 and is estimated for the fastest automotive internet of things (IoT) market growth as China’s policy support, dense supplier base, and rapid urbanization accelerate C-V2X corridors, smart-city pilots, and high connected-vehicle penetration. Japan and South Korea advance ADAS/HD-map services, while India’s evolving AIS and 5G build-out also generate automotive internet of things (IoT) market demand. Scale economics and localized software stacks fuel competitive pricing and feature velocity. In April 2025, the Car Connectivity Consortium (CCC) expanded its presence in the Asia Pacific region (especially China), supporting member automakers in deploying the CCC Digital Key and advancing connected-vehicle ecosystems with embedded IoT connectivity standards.

EUROPE

Europe maintains the second-largest share as regulatory alignment and digital-product strategies drive consistent uptake of connected features. Mandatory cybersecurity/OTA frameworks and emerging data-sharing rules push standardized platforms, enabling pan-EU service scaling and cross-border 5G corridors. Automakers intensify SDV programs, shortening software release cycles and expanding paid services. In September 2025, Telenor IoT launched IoT Drive, a Europe-tailored in-car connectivity platform built on its Managed Connectivity service and Consumer Connect architecture, enabling automakers and OEMs to deploy vehicle-embedded IoT, remote diagnostics, and telematics across European markets.

NORTH AMERICA

In North America, robust 4G/5G footprints, cloud ecosystems, and high connected-feature adoption drive the internet of things iot market in the automotive sector. OEMs scale embedded telematics, OTA updates, and ADAS subscriptions across large SUV/LCV mixes, while regulators clear paths for safety-critical V2X. Fleet digitalization and maturing data platforms further entrench recurring service revenues. In November 2024, the U.S. FCC adopted final rules enabling nationwide C-V2X operations in the 5.9 GHz band, catalyzing V2X deployments.

The U.S. leads regional growth on the back of expansive carrier 5G rollouts, active federal guidance, and strong OEM software roadmaps. Wide eSIM penetration and maturing OTA pipelines accelerate connected services monetization, while state and city pilots expand V2I infrastructure. In August 2024, USDOT released “Saving Lives with Connectivity: A Plan to Accelerate V2X Deployment,” outlining nationwide actions and funding to scale V2X, followed by FCC final C-V2X rules in November 2024.

REST OF THE WORLD

Growth in Rest of the World is paced by fleet-centric telematics, government digitalization programs, and selective 4G/5G upgrades around ports, logistics hubs, and urban corridors. Adoption concentrates on security, compliance, and uptime use cases for commercial vehicles, with OEM/aftermarket mixes varying by country. As data-governance frameworks evolve, ministries increasingly formalize telemetry exchange to monitor assets and works. In December 2024, Brazil’s Ministry of Transport issued Ordinance No. 595/2024 to promote telematics and inter-agency data exchange for infrastructure oversight.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Integration and Connected Mobility Platforms Define Competitive Landscape

The global automotive internet of things (IoT) market features a moderately consolidated vendor landscape, with major players such as Robert Bosch GmbH, Continental AG, Harman International Industries, Qualcomm Technologies Inc., and NXP Semiconductors N.V. driving innovation across connected-vehicle telematics, software services, and domain controllers. These companies are investing in IoT enabled AI cockpit systems, V2X connectivity, and over-the-air update platforms to strengthen their global footprint. In October 2024, Bosch announced a strategic collaboration with U.S. chip-startup Tenstorrent to standardize automotive chiplets and accelerate connected-vehicle infrastructure deployment.

LIST OF KEY AUTOMOTIVE INTERNET OF THINGS (IOT) MARKET COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Harman International Industries Inc. (U.S.)

- Qualcomm Technologies Inc. (U.S.)

- NXP Semiconductors N.V. (Netherlands)

- Nvidia Corporation (U.S.)

- Mobileye N.V. (Israel)

- Texas Instruments Inc. (U.S.)

- Cisco Systems Inc. (U.S.)

- Thales SA (France)

- IBM Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Aptiv PLC (Ireland)

- Denso Corporation (Japan)

- Valeo SA (France)

- Ford Motor Company (U.S.)

- General Motors Company (U.S.)

- Volkswagen AG (Germany)

- Volvo Car Corporation (Sweden)

KEY INDUSTRY DEVELOPMENTS

- In May 2025, Volvo and Google expanded their partnership to deliver Android Automotive OS updates faster, including Gemini integration, positioning Volvo as a Google reference hardware platform for in-car AI, voice, and services.

- In May 2025, Apple’s CarPlay Ultra debuted first with Aston Martin, extending Apple’s interface into instrument clusters and vehicle controls—raising competitive pressure on cockpit platforms.

- In October 2024, Bosch and Tenstorrent partnered to standardize chiplet-based automotive processors, aiming to lower cost and accelerate AI-capable compute for cockpit, ADAS, and connectivity domains.

- In October 2024, Qualcomm unveiled Elite-tier Snapdragon Digital Chassis platforms powered by Oryon CPUs to boost cockpit, connectivity, and automated-driving performance for software-defined vehicles, reinforcing modular compute and over-the-air upgradability across automakers’ lineups.

- In March 2024, GM, Magna, and Wipro formed SDVerse, a marketplace matching buyers and sellers of embedded automotive software to streamline sourcing for software-defined vehicles.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.9% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, By Component Type, By Connectivity Type, By Application, By Vehicle Propulsion, By End-user, and By Region |

|

Vehicle Type |

· Hatchback/Sedan · SUVs · LCVs · HCVs |

|

Component Type |

· Hardware · Software · Services |

|

Connectivity Type |

· Cellular · Wi-Fi/Bluetooth · Satellite · DSRC/C-V2X |

|

Application |

· Fleet Management · Telematics & Vehicle Tracking · Predictive Maintenance · ADAS & Safety Systems · Infotainment & Navigation · Usage-Based Insurance (UBI) · V2X & Autonomous Driving Systems |

|

Vehicle Propulsion |

· ICE · Electric |

|

End-user |

· Private · Commercial |

|

By Region |

· North America (By Vehicle Type, By Component Type, By Connectivity Type, By Application, By Vehicle Propulsion, By End-user, and By Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, By Component Type, By Connectivity Type, By Application, By Vehicle Propulsion, By End-user, and By Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, By Component Type, By Connectivity Type, By Application, By Vehicle Propulsion, By End-user, and By Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World (By Vehicle Type, By Component Type, By Connectivity Type, By Application, By Vehicle Propulsion, By End-user, and By Sub-region) o South America o The Middle East o Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 32.42 billion in 2025 and is projected to reach USD 91.69 billion by 2034.

In 2025, the market value stood at USD 13.22 billion.

The market is expected to exhibit a CAGR of 11.9% during the forecast period of 2026-2034.

The cellular segment led the market by connectivity type.

Nationwide V2X and 5G connectivity accelerates market adoption.

Key players in the global automotive internet of things (IoT) market include Bosch, Continental AG, Harman International, Qualcomm Technologies, and Cisco Systems.

Asia Pacific held the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us