Automotive Junction Box Market Size, Share & Industry Analysis, By Type (Fuse Box / Relay Box, Power Distribution Box, Body Control Junction Box, Engine Compartment Junction Box, Passenger Compartment Junction Box, and Smart Junction Box (SJB)), By Vehicle Type (Hatchback/Sedan, SUV, Light Commercial Vehicles, and Heavy Commercial Vehicle), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

Automotive Junction Box Market Size and Future Outlook

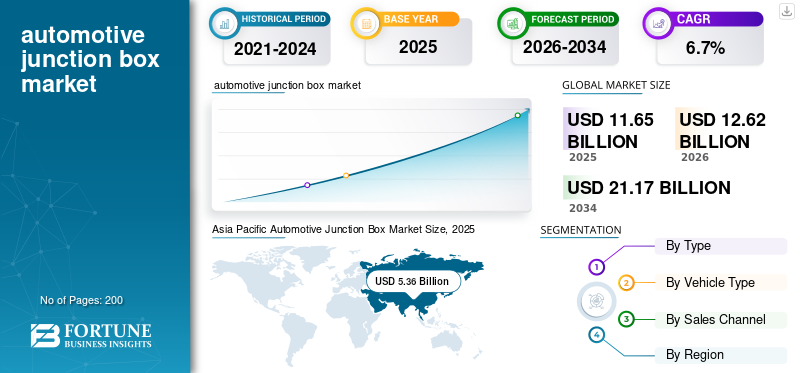

The global automotive junction box market size was valued at USD 11.65 billion in 2025. The market is projected to grow from USD 12.62 billion in 2026 to USD 21.17 billion by 2034, exhibiting a CAGR of 6.7% during the forecast period. Asia Pacific dominated the global automotive junction box market with a market share of 46.01% in 2025.

An automotive junction box is a key electrical distribution unit in vehicles that houses fuses, relays, and control circuits. It acts as the central hub that manages and protects power flow to various electrical and electronic systems, including lighting, HVAC, infotainment, engine control modules, ADAS components, and safety systems. Modern vehicles increasingly use smart junction boxes or intelligent power distribution units (iPDUs) that replace conventional fuses/relays with solid-state switches, enabling precise diagnostics, weight reduction, and improved electrical efficiency.

The automotive junction box market is experiencing steady growth, driven primarily by the rising complexity of vehicle electrical architectures, the rapid adoption of EVs and hybrids, and the integration of advanced safety and comfort features. As automakers shift toward zonal and centralized E/E architectures, advance junction boxes, especially smart variants, are becoming more sophisticated. Based on industry association data trends from OICA vehicle production, ACEA, SIAM, and EV-volumes, the global market is expected to expand at a 5-7% CAGR from 2025 to 2030, with EV platforms accounting for the fastest-growing segment due to higher power distribution demands. Additional growth factors include stricter safety and electronics requirements, increased semiconductor integration, and the shift toward modular and lightweight power distribution systems.

The dominant players in the market include a mix of global Tier-1 suppliers specializing in vehicle electrical systems. These automotive junction box companies lead due to strong OEM partnerships, high-volume production capabilities, and expertise in electrical and electronic (E/E) architecture design. Major players include Mitsuba Corporation, Sumitomo Electric Industries, Lear Corporation, TE Connectivity, Yazaki Corporation, Furukawa Electric, Minda Industries, Robert Bosch GmbH, Continental AG, and HELLA GmbH & Co. KGaA. These suppliers control a large portion of OEM procurement due to their established electrical component portfolios, ability to integrate intelligent switching technologies, and involvement in the development of next-generation smart junction boxes for EVs.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Vehicle Electrification and E/E Architecture to Propel Market Growth

The growing integration of advanced driver-assistance systems (ADAS), sophisticated infotainment platforms, enhanced comfort features, and always-on connectivity is significantly increasing the electrical and electronic complexity of modern vehicles. Each of these systems requires reliable, high-capacity power distribution and precise control, which traditional fuse and relay boxes can no longer manage efficiently. As a result, automakers are shifting toward advanced power distribution architectures that use smart, modular junction boxes capable of handling higher loads, supporting faster signal response, and providing real-time diagnostics. These intelligent units help manage the expanding network of sensors, controllers, and electronic modules while reducing wiring complexity and improving vehicle safety, reliability, and energy efficiency. This shift is directly driving market demand for junction boxes that can support the evolving electrical needs of connected and increasingly autonomous vehicles. This is expected to boost the automotive junction box market growth in the coming years.

MARKET RESTRAINTS

Semiconductor Supply Constraints to Restrain Market Growth

The production of smart automotive junction boxes depends heavily on power electronics, microcontrollers, and semiconductor components that enable functions such as solid-state switching, real-time diagnostics, and intelligent power distribution. However, the global semiconductor shortage has constrained the availability of these critical parts, creating bottlenecks in manufacturing and delaying deliveries to automakers.

Since smart automotive junction boxes require more advanced chips than conventional fuse boxes, suppliers face higher vulnerability during shortages, leading to increased production costs, longer lead times, and challenges in meeting OEM demand. This supply pressure not only slows the adoption of next-generation electrical architectures but also forces manufacturers to prioritize limited chip supply across vehicle systems, sometimes causing delays in model launches or a temporary shift back to simpler electrical junction box solutions.

MARKET OPPORTUNITIES

Expansion of EV and Hybrid Vehicle Production to Create Lucrative Growth Opportunities

The rapid expansion of electric and hybrid vehicle production is creating a strong growth opportunity for smart junction boxes, which play a critical role in managing the higher voltage and more complex power distribution requirements of these vehicles. According to IEA, Electric car sales reached 14 million units in 2023, up from 10 million in 2022. Unlike traditional internal combustion engine vehicles, EVs rely heavily on advanced electrical architectures to support battery systems, inverters, onboard chargers, and multiple high-power auxiliary loads. This requires junction boxes equipped with solid-state switching, integrated diagnostics, and enhanced thermal management to ensure safe and efficient operation. As automakers scale up EV manufacturing and introduce more sophisticated platforms, the demand for these intelligent power distribution units is rising sharply. Consequently, smart junction boxes, due to their higher value, advanced functionality, and essential role in EV safety and performance, are becoming one of the fastest-growing revenue segments in the overall market.

MARKET CHALLENGES

Meeting High Reliability Standards for Safety-Critical Systems to Hamper Market Growth

Meeting high reliability standards for safety-critical automotive systems presents a significant challenge for junction box manufacturers. These components must operate flawlessly under harsh conditions, including extreme temperatures, exposure to moisture, constant vibration, and fluctuating electrical loads. As vehicles become more electronics-intensive, especially EVs with higher voltage systems, the stress on junction boxes increases, demanding even stronger materials, precise thermal management, and more advanced protective circuitry. Ensuring long-term reliability requires rigorous testing, specialized design processes, and substantial investment in research and development to meet global safety regulations such as ISO 26262. For suppliers, balancing these high durability requirements with cost efficiency and compact packaging becomes a major engineering hurdle. Failure to meet these standards can result in system malfunctions that affect critical safety functions, making reliability compliance both technically demanding and essential.

AUTOMOTIVE JUNCTION BOX MARKET TRENDS

Rising Use of Software-Defined Electrical Systems is a Significant Market Trend

The automotive industry is rapidly transitioning toward software-defined electrical systems, where vehicle functions are increasingly controlled, updated, and optimized through software rather than hardware changes. This evolution supports over-the-air (OTA) updates, remote diagnostics, and continuous performance improvements, requiring an electrical architecture that is flexible, programmable, and capable of communicating seamlessly across vehicle domains. Smart junction boxes equipped with microcontrollers, solid-state switches, and advanced communication interfaces fit perfectly into this model, as they enable power distribution to be managed and reconfigured through software commands, rather than manual fuse or relay replacements. As OEMs move toward centralized and zonal architectures to support software-defined vehicles, smart junction boxes become essential components that bridge power and data flows. This trend directly accelerates the adoption of intelligent, software-controlled power distribution units in both EVs and next-generation ICE platforms.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Standardization of Fuse Box / Relay Box Solution in Vehicles Contributed to Segment Growth

On the basis of type, the market is classified into fuse box/relay box, power distribution box, body control junction box, engine compartment junction box, passenger compartment junction box, and smart junction box (SJB).

The fuse box / relay box segment dominated the market as these components have been the standard solution for power distribution and circuit protection in vehicles for decades. Their simple design, low cost, proven reliability, and ease of integration make them highly suitable for mass-market vehicles, especially in emerging markets where cost sensitivity is high and advanced electrical architectures are not yet widely adopted. Most internal combustion engine (ICE) vehicles still rely on conventional fuse and relay boxes to handle essential electrical loads such as lighting, HVAC, and engine controls. As the global vehicle fleet remains dominated by ICE models, many of which use well-established 12V systems, this segment continues to command the largest share of overall demand. The extensive installed base, mature supply chain, and low replacement cost also help maintain its market leadership.

Smart Junction Boxes (SJBs) are the fastest-growing segment due to the rapid electrification of vehicles and the shift toward software-defined and zonal electrical architectures. EVs and hybrid vehicles require higher voltage management, real-time diagnostics, solid-state switching, and thermal real-time monitoring capabilities that traditional fuse and relay boxes cannot provide. Smart junction boxes offer programmable power management, enhanced safety features, weight reduction, and OTA-compatible diagnostic functions, making them essential for modern and future vehicle platforms. As automakers transition from distributed to centralized electrical architectures, the need for intelligent, compact, multi-functional power distribution units rises sharply. This technological shift, combined with the exponential growth of EV production globally, is driving the rapid adoption and achieving a double-digit growth rate for smart junction boxes and iPDUs.

By Vehicle Type

Increasing Demand for Feature-rich Vehicles Propels SUV Segment Growth

In terms of vehicle type, the market is categorized into hatchback/sedan, SUV, light commercial vehicles, and heavy commercial vehicle.

SUVs dominate the market primarily as they have become the most popular vehicle type globally, driven by strong consumer demand for larger, more versatile, and feature-rich vehicles. SUVs typically incorporate a higher number of electrical and electronic components compared to smaller vehicles, including advanced infotainment systems, multiple safety and driver-assistance features, climate control zones, power-operated tailgates, all-wheel-drive controls, and enhanced lighting systems. This increased electrical load requires more complex and higher-capacity junction boxes, often with multiple fuse and relay modules or integrated smart power distribution units. Additionally, automakers have expanded SUV lineups across all price segments from compact to full-size, leading to higher production volumes and greater consumption of electrical components. As a result, the SUV segment contributes significantly more to junction box demand than sedans or hatchbacks, both due to its market size and its inherently higher electrical architecture complexity.

For Example:

According to IEA, SUVs accounted for 46% of all global light-vehicle sales in 2023, up from just 22% in 2015.

The hatchback and sedan segment continues to grow in the market primarily due to its large global production base and steady electrification of mass-market passenger cars. These vehicle types dominate volumes in price-sensitive and high-population markets across Asia Pacific, Eastern Europe, Latin America, and parts of the Middle East.

The light commercial vehicle segment is witnessing strong growth due to the expansion of e-commerce, urban logistics, and last-mile delivery services worldwide. LCVs typically operate for longer duty cycles and support multiple electrical subsystems such as fleet telematics, refrigeration units, liftgates, and advanced driver-assistance features for safety and efficiency.

Growth in the heavy commercial vehicle industry is driven by infrastructure development, freight transportation demand, and increasing regulatory requirements for safety and emissions compliance. Although HCV production volumes are lower than passenger vehicles, each vehicle incorporates substantially more complex and higher-value electrical architectures, including multiple high-capacity power distribution units, relay boxes, and control junction boxes.

To know how our report can help streamline your business, Speak to Analyst

By Sales Channel

Increasing Demand for Advanced Technology to Boost OEM Segment Growth

Based on sales channel, the market is segmented into OEM and aftermarket.

The OEM segment is anticipated to dominate the market as junction boxes are core components installed during the vehicle manufacturing process, making OEMs the primary buyers for high-volume, factory-fitted power distribution units. Automakers rely on Tier-1 suppliers to deliver highly customized, vehicle-specific junction boxes that meet strict safety, reliability, and integration requirements. As modern vehicles, especially SUVs, EVs, and premium models, adopt more complex electrical architectures, the demand for sophisticated OEM-installed junction boxes increases significantly. OEMs also prefer long-term supply contracts with established suppliers, ensuring consistent demand and stable volume. Since every new vehicle produced requires at least one junction box (often multiple in EVs), OEM installations naturally account for the largest share of the market, supported by rising global vehicle production and the shift toward smart, integrated electrical systems.

The aftermarket is the fastest-growing segment as older vehicles and high-mileage fleets increasingly require replacement of junction boxes due to wear, corrosion, overheating, or electrical failures. As vehicle parc (vehicles in use) continues to grow globally, the pool of aging cars needing electrical repairs expands each year. This is anticipated to boost the segment's future growth.

Automotive Junction Box Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific accounted for the largest automotive junction box market share in 2025, with a valuation of USD 5.36 billion, driven by its commanding position in global vehicle manufacturing. OICA data indicate that Asia remained the world’s largest vehicle-producing region in 2024, accounting for nearly 59% of the total global output. In the same year, the region recorded vehicle sales of about 54.9 million units. This sustained growth in vehicle production is indirectly accelerating demand for automotive junction boxes across the region, with China poised to maintain its dominance due to robust and rising vehicle demand.

Asia Pacific Automotive Junction Box Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America is experiencing significant growth in the market due to its strong adoption of advanced vehicle technologies, high consumer demand for SUVs and pickup trucks, and rapid expansion of electric vehicle (EV) production. Major OEMs such as GM, Ford, Tesla, and Stellantis are heavily investing in EV manufacturing, which increases the demand for smart junction boxes and intelligent PDUs.

The U.S. is anticipated to dominate the North American market. This growth is supported by large-scale investments in EV and battery manufacturing, driven by federal incentives that include domestic sourcing and localization initiatives. The country’s strong pickup truck and SUV production base, combined with rising integration of ADAS, connected features, and electrified powertrains, is significantly increasing junction box complexity and value per vehicle.

Europe

Europe is also witnessing strong market growth driven by aggressive vehicle electrification targets, regulatory pressure for advanced safety systems, and rapid adoption of software-defined vehicles. The European Union’s mandate for zero-emission new cars by 2035, along with strict NCAP safety requirements, is pushing automakers to redesign electrical architectures with higher levels of intelligence, diagnostics, and power efficiency. European OEMs such as Volkswagen, BMW, Mercedes-Benz, Volvo, and Stellantis are leading the transition to zonal architectures and smart junction boxes across their EV platforms. Additionally, Europe has one of the highest ADAS installation rates globally and a strong emphasis on lightweight, efficient electrical systems, which further accelerates demand for next-generation junction boxes.

Rest of the World

The rest of the world, encompassing Latin America and the Middle East & Africa, is expected to register moderate growth. This expansion is largely fueled by rising vehicle production and sales in emerging markets, where improving disposable incomes and a gradual move toward electrified and premium vehicles are accelerating the adoption of advanced safety and driver-assistance technologies.

COMPETITIVE LANDSCAPE

Key Industry Players:

Industry Participants Focus on Strategic Partnerships to Meet Diverse Industry Needs

The automotive junction box market is moderately fragmented, with a mix of global Tier-1 suppliers, regional manufacturers, and emerging players competing across different vehicle categories and technologies. One of the major automotive junction box producers dominating the market is Yazaki Corporation, a global leader in automotive electrical distribution systems. Yazaki leads as it has long-standing strategic partnerships with leading automakers worldwide, supplying wiring harnesses, fuse boxes, and junction boxes integrated directly into OEM vehicle platforms. Its ability to design high-reliability, high-current electrical components at scale, combined with deep expertise in power distribution and vehicle electronics, makes it a preferred supplier for both ICE and EV platforms.

LIST OF KEY AUTOMOTIVE JUNCTION BOX COMPANIES PROFILED

- Yazaki Corporation (Japan)

- Sumitomo Electric Industries, Ltd. (Japan)

- Furukawa Electric Co., Ltd. (Japan)

- Robert Bosch GmbH (Germany)

- TE Connectivity Ltd. (Switzerland)

- Continental AG (Germany)

- Minda Corporation (UNO Minda Group) (India)

- Hella GmbH & Co. KGaA (FORVIA HELLA) (Germany)

- Lear Corporation (U.S.)

- Mitsuba Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- In September 2025, Aptiv announced it would separate its wiring harness and power distribution division into an independent company by March 2026. This business includes junction boxes, PDUs, and high-voltage EV distribution units.

- In May 2025, the Light Duty business segment of Dorman Products, Inc. announced the release of hundreds of new automotive repair solutions. One of the highlights includes a smart junction box for select aging Dodge Dakota pickup trucks, manufactured to help restore malfunctioning electrical equipment to factory specifications.

- In September 2024, NXP Semiconductor released the MC33777 battery junction box controller chip designed to monitor and protect battery systems in EV and hybrid-EV (HEV) vehicles. Compliant with ASIL-D requirements, the new IC redundantly measures battery pack currents, voltages, and temperatures. It also uses onboard diagnostics to initiate protective actions when it detects fault conditions. Its high level of integration eliminates the need for separate discrete components, external actuators, and processors, saving design time, board space, and cost.

- In July 2024, ON Semiconductor announced a major multi-year agreement with Volkswagen Group, under which it will serve as the primary supplier of an advanced power box solution for Volkswagen’s next-generation electric vehicle platforms. This strategic partnership strengthens ON Semiconductor’s position in the high-voltage power distribution domain. It reflects the growing industry shift toward intelligent, semiconductor-driven junction box and power management systems designed specifically for EV architectures.

REPORT COVERAGE

The global automotive junction box market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.7% from 2025-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Vehicle Type, Sales Channel, and Region |

| By Type |

|

| By Vehicle Type |

|

| By Sales Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.65 billion in 2025 and is projected to reach USD 21.17 billion by 2034.

In 2025, the market value stood at USD 5.36 billion.

The market is expected to exhibit a CAGR of 6.7% during the forecast period (2026-2034).

The SUV segment led the market by vehicle type.

The key factor driving the market is increasing vehicle electrification and E/E architecture.

Yazaki Corporation (Japan), Sumitomo Electric Industries, Ltd. (Japan), TE Connectivity Ltd. (Switzerland), Robert Bosch GmbH (Germany), and Continental AG (Germany) are some of the prominent players in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us