Automotive Lighting Market Size, Share & Industry Analysis, By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and Heavy Commercial Vehicles), By Technology (LED, Halogen, and Xenon), By Product Type (Interior (Ambient Lamp, Reading Lamp, Backlighting, and Others) and Exterior (Headlamps, Tail lamps, Brake lamps, Signal Lamp, Exterior decoration lamp, Exterior Illumination Function Lamp, Others), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

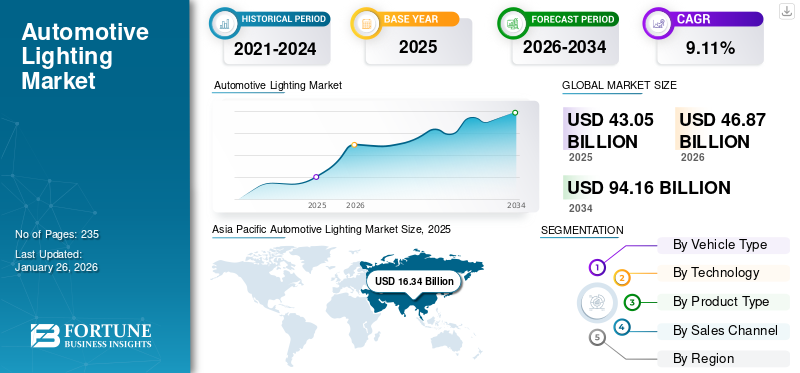

The global automotive lighting market size was valued at USD 43.05 billion in 2025 and is projected to grow from USD 46.87 billion in 2026 to USD 94.16 billion by 2034, exhibiting a CAGR of 9.11% during the forecast period. Asia Pacific dominated the global market with a share of 37.94% in 2025.

Automotive lighting is essential in passenger cars as it improves the driver's vision. It assists the driver in detecting uneven road tracks, movement of other vehicles, pedestrians, and other road hazards. It gives the interiors and exteriors of the vehicle a fashionable appeal while also increasing the visibility of other passing cars. Automotive lights are mounted in various areas, including the vehicle's front, side, back, and inside.

The increasing number of road accident cases is one of the major factors driving the global automotive lighting market growth. The overall demand for vehicle lights is closely tied to the number of vehicles sold. When automobile sales are high, the demand for lights increases accordingly. Vehicle manufacturers require lights as essential components during the production process. As the production of vehicles increases, so does the demand for lights.

Stringent safety regulations imposed by governments and regulatory bodies often require vehicles to have specific types of lights, such as daytime running lights, High-Intensity Discharge (HID) headlights, or LED tail lights. These regulations can surge the demand for specific lighting technologies. Advancements in lighting technology, such as transitioning from traditional halogen bulbs to LED technology or HID lights can surge the product’s demand as consumers and manufacturers seek more efficient, longer-lasting lighting solutions.

Moreover, increasing awareness about road safety and proper vehicle lighting encourages consumers to maintain and upgrade their lighting systems, driving the demand for quality lights. Demand for vehicle lights can vary based on factors, such as climate conditions (extreme weather requiring specialized lighting) and vehicle usage patterns (off-road vehicles may require specific lighting configurations). The demand for these lights can be cyclical and may vary in response to economic conditions, automotive industry trends, and regulatory changes.

The automotive lighting market is characterized by several major players that significantly influence its dynamics through technological advancements, product innovation, and strategic partnerships. Key companies include Valeo, a French automotive supplier known for its cutting-edge lighting solutions and emphasis on energy efficiency. Hella, a German manufacturer, specializes in both conventional and advanced lighting technologies, particularly adaptive lighting systems that enhance vehicle safety and visibility.

Osram, another prominent player from Germany, focuses on smart lighting technologies and LED solutions, catering to the increasing demand for energy-efficient automotive lighting. These players are not only competing on product innovation but also on sustainability, as the automotive industry increasingly prioritizes environmentally friendly solutions. The collaborative efforts in R&D and strategic mergers and acquisitions among these major players are pivotal in shaping the future of automotive lighting technology.

Download Free sample to learn more about this report.

Automotive Lighting Market Trends

Rising Adoption of Advanced Vehicle Lighting Technologies to Boost Market Growth

The adoption of advanced vehicle lighting technology has steadily increased in recent years. This can be attributed to several factors, including technological advancements, safety regulations, consumer preferences, and the desire for enhanced aesthetics. Light Emitting Diode (LED) technology has become increasingly popular in vehicle lighting. LEDs offer several advantages: energy efficiency, longer lifespan, faster response times, and a wide range of design possibilities. Automakers widely adopt LED headlights, tail lights, and interior lighting for improved visibility, durability, and distinctive styling options. Adaptive lighting systems are gaining traction in the automotive industry. These systems use sensors and advanced algorithms to adjust headlights' direction, intensity, and beam patterns based on factors, such as vehicle speed, steering angle, and environmental conditions. Adaptive lighting enhances visibility, improves safety, and reduces glare for drivers and other road users.

Laser lighting technology is an emerging trend in the automotive industry. Laser headlights use laser diodes to generate an intense and focused beam of light, providing improved visibility and a longer illumination range than traditional lighting technologies. Laser lighting offers potential advancements in brightness, efficiency, and compactness. The increasing advancement and investment in lighting technology will boost the market’s growth. For instance, in April 2021, Ford, one of the leading automotive manufacturers, developed a smart lighting system that points beams in the approaching corners, preventing obstacles more efficiently.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Strict Government Regulations on Lighting for Better Visibility and Safety to Boost Market Progress

Stringent lighting regulations have driven developed countries to advance the vehicle lighting industry on a global scale. Effective vehicle lighting is crucial, particularly when navigating busy highways. Governments around the world are concerned about road accidents. According to the World Health Organization (WHO), traffic collisions kill 1.3 million people annually. Most countries lose 3% of their GDP due to road accidents. Therefore, enhancing driving conditions is vital, which can be achieved partly by improving the lighting system. In 2011, the European Union mandated using Daytime Running Lights (DRLs) on all new motor vehicles to increase road safety.

Stringent government regulations mandating the use of improved lighting systems in vehicles to enhance visibility and safety are expected to drive growth in the automotive lighting market. These regulations often dictate specific standards for lighting performance, including brightness, color temperature, and beam patterns, to ensure optimal visibility for drivers and other road users. Compliance with these regulations requires automakers to invest in advanced lighting technologies, such as LED and adaptive lighting systems, which offer superior illumination and can adapt to varying driving conditions. As a result, there is an increasing demand for innovative lighting solutions from automotive manufacturers and suppliers.

Furthermore, rising concerns about road safety and the need to reduce accidents are prompting governments to enforce stricter regulations on vehicle lighting. Improved visibility provided by advanced lighting systems can help prevent accidents, particularly in adverse weather conditions or low-light environments. The purpose of DRL is to assist other road users in seeing the car, not to help the driver see the road. According to the U.S. Department of Transportation's National Highway Traffic Safety Administration (NHTSA), DRL reduced fatal road accidents by 13.8%. This regulation will positively impact the global automotive lighting market growth.

MARKET RESTRAINTS

High Cost of LED Lights to Restrain Market Growth

LED lamps generate a lot of heat, which is controlled by installing other cooling equipment. This increases the cost of LED light and is expected to restrain its adoption over the forecast period. High voltage sensitivity will also hinder the use of LEDs during the forecast period. These lights require a current below the indicated ratings and a voltage above the threshold. Such a specific power supply needed by LEDs is anticipated to hamper its quality and restrain its use.

MARKET OPPORTUNITIES

The Shift Towards Electric Vehicles (Evs) Is Creating Significant Opportunities, As These Vehicles Often Incorporate Advanced Lighting Systems.

The shift towards electric vehicles (EVs) presents a unique opportunity for the automotive lighting market, as these vehicles frequently utilize cutting-edge lighting systems to enhance both aesthetics and functionality. EV manufacturers are increasingly focused on creating visually striking designs that differentiate their vehicles in a competitive marketplace, and innovative lighting solutions play a crucial role in achieving this goal. Features such as illuminated grilles, distinctive daytime running lights (DRLs), and customizable ambient lighting not only improve the vehicle's visual appeal but also reinforce brand identity. Furthermore, advanced lighting technologies, such as adaptive headlights and intelligent lighting systems that adjust to driving conditions, enhance safety by improving visibility in various environments.

The integration of smart lighting capabilities, supported by connectivity features, allows for added functionality such as communication with external devices or vehicles, promoting the concept of smart mobility. As the demand for EVs continues to rise, the automotive lighting sector is presented with the opportunity to develop and implement innovative solutions that cater to the unique needs of electric vehicles, ultimately driving growth and expansion in the market.

MARKET CHALLENGES

Increasing Competition from Both Established Automakers And New Entrants

Increasing competition from both established automakers and new entrants poses a significant challenge in the automotive lighting market. Established automakers, leveraging their extensive experience, robust supply chains, and established relationships with suppliers, often have the resources to develop advanced lighting technologies quickly and efficiently. They can integrate these innovations into their vehicles, enhancing their offerings and solidifying their market positions. However, this level of competition also drives the need for continuous innovation and improvement, putting pressure on manufacturers of automotive lighting to differentiate their products and maintain relevance in the market.

SEGMENTATION ANALYSIS

By Vehicle Type

Increasing Demand for Advanced Lighting Systems to Propel Passenger Vehicles Segment Growth

Based on vehicle type, the market is segmented into passenger vehicles, light commercial vehicles, and heavy commercial vehicles. The passenger vehicles segment is expected to dominate the market during the forecast period. A passenger vehicle is a common mode of transportation globally. The increasing passenger vehicle sales and advancement in lighting technology are anticipated to boost the segment’s growth. Also, increasing demand for electric vehicles is anticipated to propel the segment’s growth as all-electric vehicles are equipped with high-end lighting setups. Moreover, the increase in per capita income is a major factor propelling the sales of passenger vehicles, which will indirectly boost the segment’s growth.

The demand for Light Commercial Vehicles (LCVs) operating in the market is on the rise, driven by factors, such as increased urbanization, growing emphasis on e-commerce, and need for efficient logistics & transportation solutions. Businesses are investing in LCVs to enhance their operational capabilities, leading to a surge in the demand for advanced lighting systems that improve safety and visibility, especially in urban environments.

The demand for automotive lighting in heavy commercial vehicles is also on the rise, primarily due to the increasing use of these vehicles in logistics, construction, and infrastructure projects. As regulations around safety and visibility become more stringent, manufacturers are prioritizing the development of advanced lighting solutions that enhance performance and durability in challenging driving conditions.

To know how our report can help streamline your business, Speak to Analyst

By Technology

LED Segment Accounted for Largest Market Share Due to Lower Energy Consumption and Excellent Power Output

Based on technology, the market is classified into halogen, LED, and xenon.

The LED segment dominated the market accounting for 65.17% market share in 2026. The low energy consumption and excellent power output of LED as compared to halogen are likely to help the segment grow. Leading manufacturers are focusing on developing advanced LED lights that will eventually replace halogen bulbs. For instance, in September 2024, Forvia Hella, a global automotive supplier, launched series production of an RGB LED rear combination lamp with full-color light animations in China for the first time. This innovative product features a range of new light-based functionalities, catering to the growing demand for unique branding and personalization options.

The halogen segment is anticipated to hold the second-largest position in the market over the forecast period. It has witnessed steady growth over the forecast period. Halogen lights are most commonly used in heavy vehicles due to their unique characteristics and low heat compared to LED. Also, halogen lights provide better visibility, improving drivers' safety and comfort.

By Product Type

Exterior Lighting Segment Dominates Market Due to Rising Adoption of LED Headlamps

By product type, the market is segmented into interior and exterior.

The exterior segment is further segregated into headlamps, tail lamps, brake lamps, signal lamps, exterior decoration lamps, exterior illumination function lamps, and others. The exterior lighting segment is projected to dominate the market with a share of 74.75% in 2026, driven by the increasing adoption of LED headlamps, which offer superior brightness, energy efficiency, and a longer lifespan compared to traditional halogen bulbs. As consumers and manufacturers prioritize safety and aesthetics, the demand for advanced lighting solutions, including adaptive headlights and daytime running lights, has surged. Additionally, stringent regulatory standards and growing awareness of energy conservation will further fuel the shift toward LED technology in vehicle exterior lighting, solidifying its market leadership.

Additionally, the growth of this segment can be attributed to partnerships and acquisitions, which have led to advancements in technology. For instance, in October 2024, Remsons Holding Ltd. obtained a 51% stake in BEE Lighting, enabling the company to penetrate the automotive lighting sector. This acquisition will broaden product offerings, extend market reach, and boost customer satisfaction. BEE Lighting focuses on advanced technologies in automotive headlamps and lighting. Together, the two companies aim to achieve growth in the luxury and electric vehicle markets.

The interior lighting segment is also anticipated to grow significantly during the forecast period. The segment is further segregated into ambient lamp, reading lamp, backlighting, and others. The segment’s growth is attributed to the rising adoption of enhanced internal lighting systems in mid and high-end vehicles.

By Sales Channel

OEM Segment Holds Largest Market Share Due to Increase in Vehicle Production

Based on sales channel, the market is classified into OEM and aftermarket.

The OEM segment is expected to account for 75.34% of the market in 2026, due to increasing vehicle production and advancements in lighting technology, such as LED and adaptive lighting systems that enhance safety and aesthetics. The segment’s growth is further fueled by rising consumer demand for energy-efficient lighting solutions and regulatory pressures for improved visibility and safety features in new vehicles.

Manufacturers are focusing on innovative designs and integration of smart technologies to position themselves to capitalize on the growing trend of electric and autonomous vehicles. These vehicles need advanced lighting solutions. Consequently, the OEM segment is expected to play a pivotal role in shaping the future of automotive lighting.

The aftermarket segment of the market is projected to experience significant growth due to various factors, including an increasing emphasis on vehicle customization, advancements in LED technology, and heightened consumer awareness regarding road safety and energy efficiency.

AUTOMOTIVE LIGHTING MARKET REGIONAL OUTLOOK

Asia Pacific Held Highest Market Share Owing to Increasing Vehicle Production

The market is studied across North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Lighting Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific maintained a strong presence in the global market, reaching USD 16.34 billion in 2025, accounting for 37.94% share, and is expected to reach USD 17.87 billion in 2026. The Asia Pacific automotive lighting market held the largest share in 2024 due to the rising production of vehicles in the region. The growing demand for vehicles, including passenger and commercial vehicles, is fueling the regional market’s growth. As vehicle production continues to rise, so does the demand for automotive lighting systems. The Japan market is projected to reach USD 2.83 billion by 2026, the China market is projected to reach USD 9.62 billion by 2026, and the India market is projected to reach USD 2 billion by 2026.

Factors influencing the regional market’s growth include technological advancements, increased vehicle production, changing consumer preferences, and stricter safety regulations. In the automotive industry, automotive lighting manufacturers have advanced significantly, particularly LED lighting. North America is a hub of automotive manufacturing, with several major automakers and manufacturing plants being present across the region. The U.S. is anticipated to dominate the region. The country attributable to the integration of advanced technologies, a rise in electric vehicle adoption, stricter safety regulations, and evolving consumer preferences toward aesthetics and sustainability. These factors are likely to create a dynamic market environment, offering ample opportunities for innovation and expansion in the automotive lighting sector. The U.S. market is projected to reach USD 8.31 billion by 2026.

Europe

The Europe region captured 30.28% of the global market in 2025, generating USD 13.04 billion in revenue, and is projected to reach USD 14.22 billion in 2026. Europe is anticipated to grow at a healthy rate during the forecast period. The government's regulations are complementing the market’s growth in this region. Since 2011, the European Union has made it mandatory to use Daytime Running Lights (DRLs) across Europe. This region's dominance in the market is expected to be maintained by the early adoption of innovative automotive lighting solutions by major key players. The UK market is projected to reach USD 1.59 billion by 2026, while the Germany market is projected to reach USD 4.87 billion by 2026.

North America

In 2025, the North America market stood at USD 10.14 billion, representing 23.54% of global demand, and is projected to grow to USD 10.97 billion in 2026.

Rest of the World

The Rest of the World market generated USD 3.54 billion in 2025, representing 8.23% of the global market landscape, and is expected to reach USD 3.8 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations and Partnerships Helped Magneti Marelli Maintain Dominant Market Position

Magneti Marelli is a significant market player. The company's global market position is strengthened by increasing partnerships and collaborations with other major companies to create high-end components. The company's constant R&D efforts have resulted in the development of novel technologies, which is one of the main reasons for its supremacy in the market. CK Holdings announced the acquisition of Magneti Marelli from Fiat Chrysler on May 2, 2019. Magneti Marelli CK Holdings will manage the company's operations.

LIST OF KEY AUTOMOTIVE LIGHTING COMPANIES PROFILED

- Hella KGaA Hueck & Co. (Germany)

- Valeo (France)

- Marelli Corporation (Italy)

- Koninklijke Philips (Netherlands)

- KOITO MANUFACTURING CO., LTD (Japan)

- Stanley Electric Co., Ltd (Japan)

- SL Corporation (South Korea)

- HASCO Vision Technology Co. Ltd (China)

- ZKW Group (Austria)

- OPmobility (France)

- Changzhou Xingyu Automotive Lighting Systems Co. Ltd (China)

- Hyundai Mobis (South Korea)

- Continental AG (Germany)

- Flex-N-Gate (United States)

- MIND Electronics Appliance Co., Ltd (China)

KEY INDUSTRY DEVELOPMENTS

- April 2024 - Dominant Opto announced that it will become the second supplier of interior automotive lighting using connected technology from ams Osram.

- April 2024 - ams OSRAM (SIX: AMS), a prominent player in intelligent sensors and emitters, collaborated with DOMINANT Opto Technologies, a top Malaysian manufacturer of automotive LED solutions. This strategic partnership focused on integrating ams OSRAM's Open System Protocol (OSP) into DOMINANT Opto Technologies' next-generation intelligent RGB LEDs, which are designed for automotive ambient lighting.

- June 2023 - In a groundbreaking development, Motherson, in partnership with Marelli, inaugurated the Motherson Automotive Lighting Tool Room. This marked a historic milestone as the inaugural establishment of its kind in India solely focused on automotive lighting.

- April 2023 - Continental AG introduced its automotive lighting product NightViu for construction and off-road vehicles. The company introduced 16 new products under the NightViu product line. The products are specifically engineered for construction, mining, and off-road equipment applications.

- January 2023 - Nichia and Infineon launched an industry-first high-definition micro-LED matrix solution. Automotive LED lighting technology has developed rapidly in recent years as a means for vehicle manufacturers to enhance driving comfort and road safety. In this regard, matrix LED technology for adaptive driving beam has become an important headlight feature for selective road illumination.

REPORT COVERAGE

The report provides a detailed market analysis and focuses on key aspects, such as leading companies, services, and product applications. Besides this, it offers insights into the market trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.11% from 2026 to 2034 |

|

Unit |

Value (USD Billion) and Volume (Million Units) |

|

Segmentation |

By Vehicle Type

|

|

By Technology

|

|

|

By Product Type

|

|

|

By Sales Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights global report says that the market was valued at USD 43.05 billion in 2025 and is projected to reach USD 94.16 billion by 2034.

The market is expected to record a CAGR of 9.11% during the forecast period.

Growing awareness regarding road safety is expected to drive the market’s growth.

Asia Pacific led the global market in 2026.

China led the global market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 235

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us